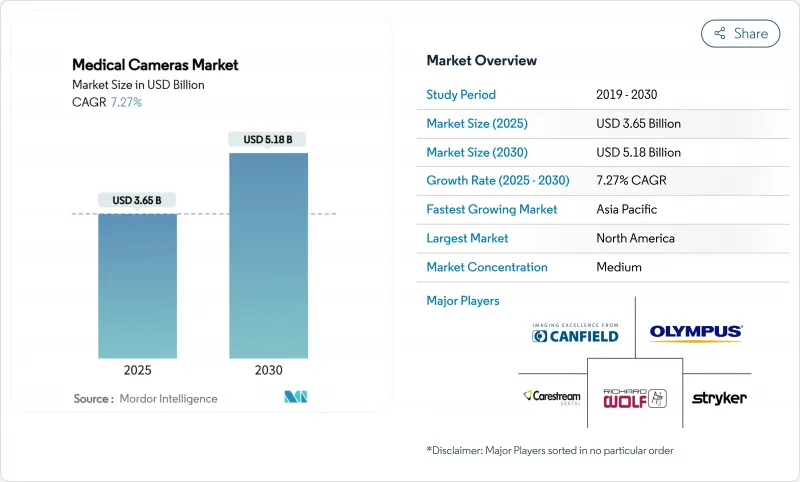

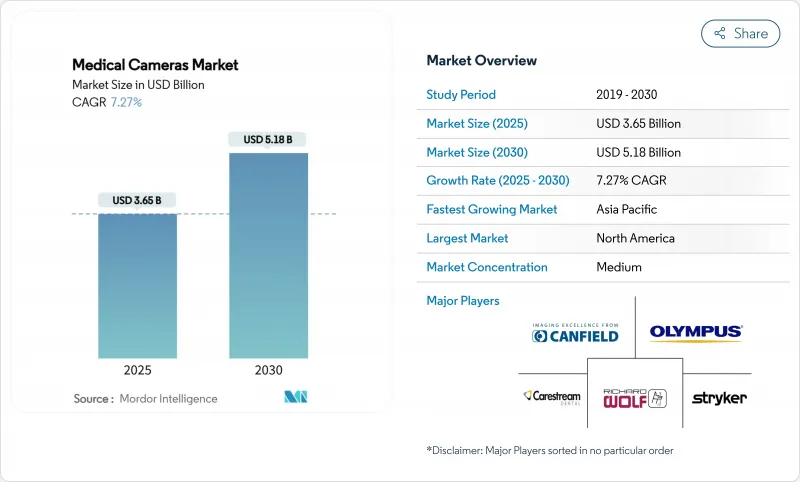

의료용 카메라 시장 규모는 2025년에 36억 5,000만 달러로 추계되어 예측 기간(2025-2030년)의 CAGR은 7.27%로, 2030년에는 51억 8,000만 달러에 이를 것으로 예상됩니다.

이 확장은 표준 화질에서 초고화질의 4K 및 8K 영상으로의 전환, 저침습 수술의 상승, 종양학, 심장 병학, 소화기 병학에서 꾸준한 수술 절차의 성장으로 추진됩니다. 일회용 내시경과 캡슐 내시경에 대한 수요는 감염 관리 프로토콜이 강화되는 반면, 병원은 수술 시간을 단축하고 환자 회복을 가속화하는 기술 업그레이드를 추구하는 가운데 높아지고 있습니다. 아시아태평양은 정부 프로그램에 의해 국내 의료기기 제조가 촉진되고 주목을 받고 있지만, 북미는 프리미엄 이미징 플랫폼의 조기 도입으로 최대의 설치 베이스를 유지하고 있습니다. 경쟁 정보의 핵심은 카메라 생태계에 인공지능(AI)을 통합하여 병변의 자동 감지와 실시간 조직 특성화를 실현하는 것입니다.

외과의사의 보고에 따르면, HD의 4배의 픽셀 밀도는 이전에 몰랐던 미세혈관 패턴과 미묘한 종양의 가장자리를 드러내고 조기 절제를 가능하게 하고 재수술의 필요성을 감소시킵니다. Narrow Band Imaging 및 Blue Light와 같은 특수 이미지 모드는 이러한 4K 카메라에 번들되어 악성 및 양성 조직의 식별을 더욱 선명하게 합니다. 학술센터에서는 보다 선명한 시각화로 보조 이미지에 대한 의존도가 줄어들기 때문에 수술 시간의 단축을 기록하고 있습니다. 풀 4K 스택은 20만 달러 이상이기 때문에 자본 예산은 여전히 장애물이지만, 리스 제도와 실적 증명 데이터가 조달 결정을 용이하게 하고 있습니다. 부품 가격이 하락함에 따라 지역 병원은 정기적인 교체 사이클 중에 기존 HD 시스템을 업그레이드할 것으로 예측됩니다.

소화기 내시경 검사와 폐 내시경 검사의 세계 건수는 스크리닝 프로그램과 당일치료에 대한 기호에 따라 증가하고 있습니다. 선종의 검출률을 2자리 상승시키는 AI 대응 카메라 헤드를 이용 가능하게 됨으로써, 지불자는 상환을 확대하도록 촉구되고 있으며, 유럽과 북미에서 기기의 갱신이 진행되고 있습니다. 단일 사용 범위는 재처리의 번거로움을 없애고 교차 오염의 위험을 줄입니다. 외래 수술 센터(ASC)는 병원의 오버플로우를 흡수하기 위해 생산 능력을 확대하고 있으며 제조업체는 비용에 민감한 구매자를 위해 가격 설정을 미세 조정해야 합니다. 일회용 무선 카메라 모듈을 제공하는 시장 진출기업은 ASC 수요를 받아들이는 좋은 위치에 놓여 있습니다.

프리미엄 4K 타워에는 고급 광학 장비, 프로세서 및 모니터가 결합되어 있으며, 총액은 수술실 1개당 20만 달러를 초과합니다. 연간 서비스 계약과 센서의 재교정이 평생 비용을 증가시키기 때문에 예산에 제약이 있는 시설에서는 급속한 도입이 진행되지 않습니다. 신흥 시장의 병원에서는 수년간의 설비 자금이 승인될 때까지 업그레이드를 연기하는 경우가 많으며 교환 사이클이 길어지고 있습니다. 제조업체 각사는 단계적인 제품 라인업과 프로시저별 지불에 의한 자금 조달을 도입하여 초기 도입의 장애물을 낮추고 있습니다. 반면에, 일회용 카메라는 멸균 비용을 필요로 하지 않지만, 손익분기점을 넘어도 사례당 경제성이 양호하다는 것을 증명해야 합니다.

내시경 카메라는 소화기과, 비뇨기과, 호흡기과의 검사실에서 필수적이기 때문에 2024년 의료용 카메라 시장에 35.16%를 공헌했습니다. 캡슐형 및 단일 사용 모델의 CAGR은 8.03%로 확대되었지만, 이는 유행 후 멸균 기준에 따른 감염 관리의 필요성을 반영합니다. 제조업체 각사는 광학계를 서브밀리 직경까지 소형화해, 8시간 화상을 무선 전송하는 삼키는 장치를 실현해, 원격 스크리닝 프로그램에의 적용 범위를 확대하고 있습니다. 신경 외과용 4K 로봇 시스템으로 대표되는 수술 중 현미경 카메라는 입체적인 깊이를 요구하는 신경 외과 의사를 끌어들이고 있습니다. 치과용 카메라와 피부과용 카메라는 틈새 위치를 차지하고 있으며, AI로 강화된 피부 병변 영상은 원격 피부과의 확대가 예상됩니다.

단일 사용 형식으로의 전환은 병원 내에서 확립된 재처리 워크플로우에 대한 도전과 동시에 멸균 장치를 제거하여 공급망을 효율화합니다. 스코프, 프로세서 및 AI 분석을 통합 키트에 번들하는 카메라 제조업체는 각 기술에 대한 경상 수익을 높이고 있습니다. 캡슐 유형과 일회용 채택이 증가함에 따라 벤더는 임상 신뢰성 기준을 충족하기 위해 안전한 데이터 전송과 배터리 수명을 보장해야합니다.

고해상도는 2024년에도 지배적이며 49.03%의 수익을 얻었습니다. 그럼에도 불구하고, 4K/8K 유닛은 CAGR 8.68%로 진전하고 있으며, 이것은 선명함과 깊이 지각의 향상에 대한 외과의의 기호에 의한 것입니다. 초고화질 기기의 의료용 카메라 시장 규모는 mm 이하의 정확도가 중요한 안과와 뇌신경 수술로 가장 빠르게 확대되고 있습니다. 4K로 업그레이드하는 병원에서는 디스플레이를 대형화하여 여러 번 정렬하지 않고도 팀에서 시각화할 수 있어 워크플로우를 향상시킬 수 있습니다.

그러나 업그레이드에는 호환 가능한 레코더와 4배의 데이터 처리량을 처리하기 위한 네트워크 대역폭이 필요합니다. 마이그레이션을 용이하게 하기 위해 공급업체는 기존 모니터와의 호환성을 유지하면서 HD와 4K 피드 사이를 자동 스케일링하는 하이브리드 컨트롤 유닛을 제공합니다. 병변의 감지 및 운영 시간 단축의 지표로 입증 가능한 이익을 얻을 수 있기 때문에 특히 투자 회수 모델이 4년 이내의 투자 회수를 문서화하는 경우에는 조달 승인이 가속화되고 있습니다.

북미는 병원이 AI 대응 4K 스택으로 업그레이드하고 상환이 저침습 수술을 지원하기 때문에 2024년 매출 점유율 35.17%로 최대 지역 바이어를 유지했습니다. 미국은 유리한 청구 코드와 내시경적 개입에 대한 외과 의사의 선호를 확립하는 데 도움을 받으며 세계 수술 건수를 선도하고 있습니다. 캐나다는 단일 청소년 이미징과 같은 감염 통제 강화를 선호하는 주 수준의 자금 지원으로 이어집니다.

아시아태평양은 CAGR 10.19%로 확대되고 있으며, 외과 인프라에 대한 공공 투자, 캡슐 내시경의 급속한 보급, 중국과 인도에서 국내 제조의 장려가 그 원동력이 되고 있습니다. 중국 병원은 Tier-3 인증을 충족하기 위해 수술실 개조를 진행하고 있으며 입찰로 4K 대응을 지정하는 경우도 많습니다. 인도의 MedTech 장려제도는 광학부품의 수입관세를 인하하고 2차 의료시설에 있어서 가격 감을 향상시키고 있습니다.

독일과 프랑스 병원이 통합 수술실로 옮겨가기 때문에 유럽에서는 안정적인 수요가 있습니다. 스칸디나비아 국가는 원격 의료 보급률의 높이를 반영하여 대장 검진용 무선 캡슐 카메라를 일찍부터 채용하고 있습니다. 중동에서는 사우디아라비아와 아랍에미리트(UAE)의 주요 의료 도시가 3D 내시경 스위트를 통합하는 하이브리드 수술실을 지정하여 고가치 수요 포켓을 형성합니다. 라틴아메리카와 아프리카 공헌은 작지만 감염 통제 업그레이드에 중점을 둔 다자간 개발 은행의 자금 조달을 볼 수 있습니다.

The Medical Cameras Market size is estimated at USD 3.65 billion in 2025, and is expected to reach USD 5.18 billion by 2030, at a CAGR of 7.27% during the forecast period (2025-2030).

This expansion is propelled by the transition from standard-definition to ultra-high-definition 4K and 8K visualization, the rise of minimally invasive surgery, and steady procedure growth in oncology, cardiology, and gastroenterology. Demand for single-use and capsule endoscopes is rising as infection-control protocols tighten, while hospitals pursue technology upgrades that shorten operating times and speed patient recovery. Asia-Pacific is gaining prominence as government programs foster domestic medical-device manufacturing, yet North America retains the largest installed base because of early adoption of premium imaging platforms. Competitive momentum centers on integrating artificial intelligence (AI) into camera ecosystems to deliver automated lesion detection and real-time tissue characterization.

Surgeons report that four-fold pixel density relative to HD exposes microvascular patterns and subtle tumor margins that previously went unnoticed, enabling earlier resection and reducing the need for repeat procedures. Specialty imaging modes such as Narrow Band Imaging and Blue Light are bundled with these 4K cameras, further sharpening discrimination between malignant and benign tissue. Academic centers are documenting shorter operating times because clearer visualization lessens reliance on adjunct imaging. Capital budgets remain a hurdle because a full 4K stack costs upward of USD 200,000, yet leasing schemes and proof-of-outcome data are easing procurement decisions. As component prices fall, community hospitals are forecast to upgrade legacy HD systems during scheduled replacement cycles.

Global procedure volumes for gastrointestinal and pulmonary endoscopy are rising alongside screening programs and a preference for day-case interventions. The availability of AI-enabled camera heads that elevate adenoma detection by double-digit percentages is encouraging payers to extend reimbursement, driving equipment refreshes across Europe and North America. Single-use scopes eliminate re-processing labor and reduce cross-contamination risk an imperative solidified after the COVID-19 pandemic. Ambulatory surgery centers (ASCs) are expanding capacity to absorb overflow from hospitals, compelling manufacturers to fine-tune pricing for these cost-sensitive buyers. Market entrants offering disposable, wireless camera modules are well positioned to capture ASC demand.

A premium 4K tower couples high-grade optics, processors, and monitors that together exceed USD 200,000 per operating room. Annual service contracts and sensor re-calibration amplify lifetime cost, deterring budget-constrained facilities from rapid adoption. Emerging-market hospitals often postpone upgrades until multi-year equipment funds are approved, lengthening replacement cycles. Manufacturers are introducing tiered product lines and pay-per-procedure financing to lower upfront barriers. Meanwhile, disposable camera formats eliminate sterilization expense but require proof that per-case economics remain favorable beyond the break-even utilization threshold.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Endoscopy cameras contributed 35.16% to the medical cameras market in 2024 as they remain indispensable across gastroenterology, urology, and pulmonology suites. Capsule and single-use models are escalating at an 8.03% CAGR, reflecting infection-control imperatives that align with post-pandemic sterilization standards. Manufacturers are miniaturizing optics to sub-millimeter diameters, enabling swallowable devices that wirelessly transmit images for eight hours, expanding reach to remote screening programs. Intraoperative microscopy cameras, exemplified by 4K robotic systems for neurosurgery, are attracting neurosurgeons seeking stereoscopic depth. Dental and dermatology cameras hold niche positions, with AI-enhanced skin-lesion imaging poised for tele-dermatology expansion.

The shift toward single-use formats challenges established re-processing workflows in hospitals yet offers supply-chain efficiencies by removing sterilization equipment. Camera makers that bundle scopes, processors, and AI analytics into integrated kits are achieving higher recurring revenue per procedure. As capsule and disposable adoption rises, vendors must ensure secure data transmission and battery longevity to satisfy clinical reliability standards.

High-definition remained the dominant resolution in 2024, capturing 49.03% revenue as legacy fleets continue to serve routine cases. Nevertheless, 4K/8K units are advancing at 8.68% CAGR, driven by surgeon preference for enhanced clarity and depth perception. The medical cameras market size for ultra-high-definition equipment is expanding fastest in ophthalmology and neurosurgery where sub-millimeter accuracy is critical. Hospitals upgrading to 4K realize workflow gains when larger displays permit team visualization without repeated positioning.

Upgrading, however, requires compatible recorders and network bandwidth to handle quadrupled data throughput. To ease transition, suppliers offer hybrid control units that auto-scale between HD and 4K feeds, preserving compatibility with existing monitors. Demonstrable gains in lesion detection and reduced operating-time metrics are accelerating procurement approvals, particularly when return-on-investment models document payback within four years.

The Medical Cameras Market Report is Segmented by Product Type (Dental Cameras, Dermatology Cameras, Endoscopy Cameras, Ophthalmology Cameras, and More), Resolution (Standard-Definition Cameras, and More), Sensor Technology (CCD, CMOS, SCMOS), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the largest regional buyer with 35.17% revenue share in 2024 as hospitals upgraded to AI-ready 4K stacks and reimbursement supports minimally invasive surgery. The United States leads global procedure volumes, assisted by favorable billing codes and established surgeon preference for endoscopic interventions. Canada follows with province-level funding that prioritizes infection-control enhancements such as single-use imaging.

Asia-Pacific is expanding at a 10.19% CAGR, fuelled by public-sector investment in surgical infrastructure, rapid adoption of capsule endoscopy, and domestic manufacturing encouragement in China and India. China's hospitals are retrofitting operating rooms to meet Tier-3 accreditation, often specifying 4K readiness in tenders. India's MedTech incentive scheme is lowering import duties on optical components, improving affordability for secondary-tier facilities.

Europe posts steady demand as German and French hospitals transition to integrated operating rooms, though budget constraints temper replacement speed. Scandinavian countries are early adopters of wireless capsule cameras for colorectal screening, reflecting high tele-health penetration. In the Middle East, flagship medical cities in Saudi Arabia and the United Arab Emirates are specifying hybrid ORs with built-in 3D endoscopy suites, creating pockets of high-value demand. Latin America and Africa are smaller contributors but are witnessing procurement financed by multilateral development banks focused on infection-control upgrades.