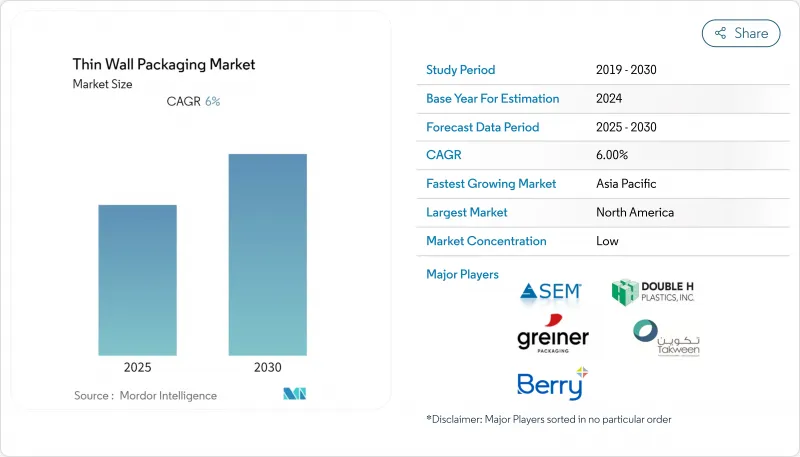

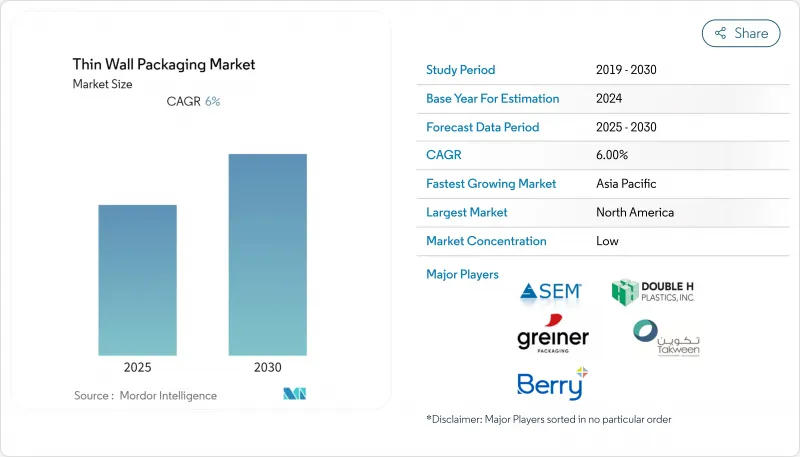

얇은 벽 포장 시장은 2025년에 477억 5,000만 달러에 이르고, 2030년에는 689억 5,000만 달러에 달할 것으로 예상됩니다.

이는 건전한 CAGR 7.63%를 나타내 식품, 식음료, 화장품, 전자상거래 채널 수요 증가를 뒷받침합니다.

온라인 소매와 관련된 물류 성장, 운임을 줄이는 재료 효율적인 설계 목표, 재활용 가능한 형식에 대한 법적 지원 강화가 상승세를 뒷받침하고 있습니다. 폴리프로필렌이 여전히 주력 수지라는 것은 변함이 없지만, 브랜드 소유자가 확대 생산자 책임 규칙을 준수하려고 경쟁하고 있기 때문에 바이오폴리머의 보급이 가속화되고 있습니다. 핫 러너 사출 성형 및 인라인 압출 열 성형의 제조 기술 혁신은 두께를 1mm 이하로 유지하면서 높은 처리량을 유지합니다. 지역적으로는 북미가 수량의 리더를 유지하고 있지만, 아시아태평양이 도시화, 배식의 보급, 가처분 소득의 상승을 배경으로 가장 급속히 확대되고 있습니다. 이러한 요소들이 결합됨에 따라, 얇은 벽 포장 시장은 향후 5년간 브랜드 차별화, 비용 억제, 탄소 감소를 위한 중심 플랫폼으로 자리매김할 것입니다.

온라인 소매의 급속한 확대로 얇은 벽 포장 시장은 치수 중량 수수료를 최소화하면서 자동 분류에 견디는 설계로 향하고 있습니다. Levain Bakery와 같은 브랜드는 제조 공정을 8단계에서 4단계로 줄이고 서브mm 크기의 용기를 채용함으로써 포장 효율을 50% 향상시켰습니다. 이 용기는 완성 센터 내에서 원활하게 운반됩니다. ReadyWise는 필요에 따라 적절한 크기의 패키지를 사용하여 매주 100만 개의 파우치를 배송하여 운송 비용과 저장 공간을 동시에 절감합니다. 자동화에 대응하고 공간을 최적화함으로써, 얇은 용기는 단순한 비용 절감 방법이 아니라 전자상거래의 확장성을 위한 인프라에 필수적인 요소가 되었습니다.

도시 지역의 소비자는 전자 레인지에서 요리 할 수있는 분량이 관리되는 식사에 끌려 들지만, 재료를 왜곡하지 않고 안전하게 가열 할 수있는 포장이 필요합니다. Curefit은 현재 신선도 유지와 신속한 재가열 사이클을 위해 설계된 용기로 매일 3만 5,000식의 조리된 식품을 출하하고 있으며, 외식 산업의 회복이 수지 수요 증가를 고배리어 얇은 설계로 유도하고 있는 것을 보여주고 있습니다. 투명한 뚜껑은 충동 구매를 촉진하고 열성형 베이스는 정확한 벽 캘리브레이션을 이용하여 수지를 절약하고 구조적 무결성을 유지합니다.

영국은 현재 재활용률 30% 미만의 포장재에 톤당 200 파운드를 과세하고 있으며, 재활용 인프라에 자금을 충당하지 않고 연간 7억 파운드를 징수하고 있습니다. 스페인은 2023년에 처녀 플라스틱에 대한 킬로그램당 과세를 시작했고, 독일은 2025년까지 실시를 늦추었기 때문에 투자 예측에 암클라우드가 들어가고 있습니다. 이러한 정책은 컴플라이언스 비용을 팽창시켜 인증 재활용 원료 흐름과 폐쇄 루프 파트너십으로의 전환을 가속화합니다.

2024년 얇은 벽 포장 시장에서의 컵의 점유율은 36.3%에 달하며, 식음료의 리뉴얼 오픈이나 외출처에서의 왕성한 음용 습관에 지지되었습니다. 이 부문은 낮은 재료 대 부피비, 자동 충전 호환성, 브랜드 친화적인 인쇄면과 같은 이점이 있습니다. 커피 체인과 퀵 서비스 레스토랑에서는 100℃의 충전 온도로 변형하지 않고 견딜 수 있는 지속 가능한 컵의 시험이 펼쳐져 2030년까지 성장이 계속되고 있습니다.

그릇과 뚜껑 카테고리는 2030년까지 연평균 복합 성장률(CAGR) 7.9%를 나타낼 것으로 예상됩니다. 사업자는 상품의 신선도를 어필하고 가스 플래쉬에 의한 유통기한 연장을 지원하는 투명한 뚜껑을 우선합니다. 인라인 열성형의 발전으로 기존에는 무거운 라이벌에만 적용된 낙하 시험 기준에 부합하는 평균 벽부 400마이크론의 그릇이 가능합니다. 트레이, 튜브, 항아리는 유제품, 과자류, 퍼스널케어의 틈새 분야에서 계속 중요하며, 각각 모양과 장벽의 사용자 정의를 활용하여 선반의 차별화를 유지하고 있습니다.

폴리프로필렌은 범용성이 높은 가공창, 내습성, 유리한 가격 성능비에 의해 2024년의 얇은 벽 포장 시장 점유율의 43.2%를 획득했습니다. 그러나 얇은 벽 포장 시장에서는 PLA와 PHA 수지의 이용이 활발해지고 있으며, 컨버터는 퇴비화 가능성과 재활용 함량의 의무에 대응하려고 약기가 되었기 때문에 CAGR은 8.3%로 확대하고 있습니다.

프라운호퍼 연구소는 기존 LDPE 라인에서 제조할 수 있는 80% 바이오 플렉서블 PLA 필름을 발표했습니다. 한편, PHA의 선구자인 그린팀은 마이크로플라스틱의 흔적을 남기지 않고 6개월 이내에 분해되는 가정에서 퇴비화 가능한 냄비를 검증했습니다. PET는 산소의 영향을 받기 쉬운 조리된 샐러드로 틈새 존재감을 유지하고 있지만, 폴리스티렌과 PVC는 규제 당국의 감시가 엄격해짐에 따라 점유율을 떨어뜨리고 있습니다.

얇은 벽 포장 시장은 포장 유형(튜브, 항아리, 냄비, 기타), 소재(폴리프로필렌, 폴리에틸렌테레프탈레이트, 폴리스티렌, 기타), 제조 공정(사출 성형, 기타), 최종 사용자 산업(음식, 화장품 및 퍼스널케어, 의약품·영양 보조 식품, 공업·가정 용품), 지역에 따라 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 정착한 밀 서비스 사업, 정교한 리사이클 채널, 경량화 툴킷의 조기 채용을 배경으로 2024년 얇은 벽 포장 시장의 28.2%를 유지했습니다. 브랜드 소유자는 연방 및 주 플라스틱 법률을 준수하는 컴플라이언스 지원 팩의 대가로 비싼 수지 가격을 계속 흡수하고 있습니다. 미국은 여전히 고급 핫 러너 시스템의 기술 혁신의 중심지이며 캐나다는 공공 부문의 조달 정책을 기관식 프로그램에서 PCR 채용을 향해 유도하고 있습니다.

아시아태평양의 2030년까지의 CAGR은 9.5%로 예측되어, 급속한 도시화, 중간층의 구매력의 증대, 식료품의 옴니 채널화로의 급격한 변화에 지지되고 있습니다. 수량은 중국이 선도하고 있지만, 1인당 인도와 인도네시아가 가장 빠른 확대를 기록하고 있습니다. 인도 식품 안전 기준국에 의한 식품 접촉 용도에서 재활용 플라스틱의 승인은 PCR을 많이 사용하는 얇은 디자인의 진입 장벽을 더욱 낮춥니다. 지역 컨버터는 폴리프로필렌과 신흥 바이오 수지 모두에 대응할 수 있는 다층 압출·열성형 라인에 다액의 투자를 실시해 공급의 탄력성을 높이고 있습니다.

유럽은 일찍부터 지속가능성을 의무화하고 대륙에서 순환성에 중점을 두고 있기 때문에 큰 점유율을 차지하고 있습니다. 플라스틱세와 EPR제도는 비용압력을 강화하지만 동시에 씰의 무결성을 희생하지 않고 30% 이상의 재활용률을 실현할 수 있는 기업에 보답하는 것입니다. 독일, 프랑스, 북유럽은 소매업체가 개인 라벨의 구색으로 단일 소재 포장을 추진하는 가운데, IML 채용의 온상이 되고 있습니다. 동유럽 국가들은 노동 비용이 낮을 수 있도록 도와주며 같은 규제의 한계를 극복하면서 서유럽 수요를 충족시키는 수탁 제조의 허브로 부상하고 있습니다.

중동 및 아프리카 클러스터는 특히 냉동유제품의 수출과 고내열성 PP컵을 요구하는 지역의 QSR 체인에서 초기이지만 유망한 전망을 제공합니다. 남미의 성장은 농산물의 부가가치와 편의 형식에 매료되는 중간층의 확대에 연결되어 있습니다. 브라질의 수지 현지 생산은 비용면에서 유리하지만, 신뢰성이 낮은 재활용 인프라가 순환형 재료 조달을 제한하고 PCR을 풍부하게 포함한 얇은 제품의 보급을 늦추고 있습니다.

The thin wall packaging market stands at USD 47.75 billion in 2025 and is forecast to reach USD 68.95 billion by 2030, reflecting a healthy 7.63% CAGR that underscores rising demand across food, beverage, cosmetics and e-commerce channels.

Upward momentum is fuelled by logistics growth tied to online retail, material-efficient design targets that cut freight charges, and tightening legislative support for recyclable formats. Polypropylene remains the workhorse resin, yet biopolymer penetration is accelerating as brand owners race to meet extended producer responsibility rules. Manufacturing innovation in hot-runner injection molding and inline extrusion-thermoforming keeps throughput high while driving wall thickness below 1 mm. Regionally, North America retains volume leadership, but Asia-Pacific is expanding fastest on the back of urbanization, meal-delivery adoption and rising disposable incomes. These converging factors combine to position the thin wall packaging market as a central platform for brand differentiation, cost containment and carbon reduction over the next five years.

Rapid online retail expansion pushes the thin wall packaging market toward designs that withstand automated sortation while minimizing dimensional weight fees. Brands such as Levain Bakery cut process steps from eight to four and achieved a 50% packaging-efficiency gain by adopting sub-millimeter containers that flow smoothly through fulfillment centers.ReadyWise uses on-demand right-sized packs to move 1 million pouches weekly, trimming freight costs and floor space simultaneously. Automation compatibility and space optimization make thin wall formats infrastructure-critical for e-commerce scalability rather than a simple cost lever.

Urban consumers gravitate to microwave-ready, portion-controlled fare that requires packaging capable of safe heating without material distortion. Curefit now dispatches 35,000 ready meals daily in containers engineered for freshness retention and rapid reheat cycles, illustrating how food-service recovery steers incremental resin demand toward high-barrier thin wall designs. Transparent lids encourage impulse purchase while thermoformed bases exploit precise wall calibration to conserve resin and uphold structural integrity.

The United Kingdom now levies GBP 200 per tonne on packaging below 30% recycled content, extracting an anticipated GBP 700 million annually without earmarking funds for recycling infrastructure. Spain launched a per-kilogram tax on virgin plastic in 2023, while Germany's implementation delay until 2025 clouds investment forecasts. These policies inflate compliance costs and encourage accelerated transitions toward certified recyclate streams and closed-loop partnerships.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cups generated a 36.3% share of the thin wall packaging market in 2024, underpinned by food-service reopenings and robust on-the-go beverage rituals. The segment benefits from low material-to-volume ratios, automated filling compatibility and brand-friendly print surfaces. Growth persists through 2030 as coffee chains and quick-service restaurants widen sustainable cup trials capable of withstanding 100 °C fill temperatures without deformation.

The bowls and lids category is projected to post a 7.9% CAGR to 2030, catalyzed by global meal-kit subscriptions and refrigerated fresh-cut produce. Operators prioritize transparent lids that showcase product freshness and support gas-flush shelf-life extensions. Advances in inline thermoforming enable bowls with 400-micron average wall sections that match drop-test standards formerly associated only with heavier rivals. Trays, tubs and jars remain vital for dairy, confectionery and personal-care niches, each leveraging geometry and barrier customization to maintain shelf differentiation.

Polypropylene captured 43.2% of thin wall packaging market share in 2024 due to its versatile processing window, moisture resistance and favorable price-performance ratio. Yet, the thin wall packaging market is witnessing brisk uptake of PLA and PHA resins, which are expanding at an 8.3% CAGR as converters scramble to meet compostability and recycled-content mandates.

The Fraunhofer Institute unveiled an 80% bio-based flexible PLA film that runs on conventional LDPE lines, signaling cost-effective integration potential for high-clarity applications. Meanwhile, PHA pioneer Green Team validated home-compostable pots that decompose within six months without microplastic traces. PET sustains niche relevance in oxygen-sensitive prepared salads, while polystyrene and PVC continue to lose share amid tightening regulatory scrutiny.

Thin Wall Packaging Marke is Segmented by Packaging Type (Tubs, Jars, Pots, and More), Material (Polypropylene, Polyethylene Terephthalate, Polystyrene, and More), Manufacturing Process (Injection Molding, and More), End-User Industry (Food and Beverage, Cosmetics and Personal Care, Pharmaceuticals and Nutraceuticals, Industrial and Household Goods), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 28.2% of the thin wall packaging market in 2024 on the back of entrenched meal-service businesses, sophisticated recycling channels and early adoption of light-weighting toolkits. Brand owners continue to absorb premium resin pricing in return for compliance-ready packs that navigate federal and state plastics legislation. The United States remains the innovation locus for advanced hot-runner systems, while Canada channels public-sector procurement policies toward PCR adoption in institutional food programmes.

Asia-Pacific is projected to achieve a 9.5% CAGR to 2030, underpinned by rapid urbanization, growing middle-class purchasing power and a sharp shift toward omni-channel grocery. China leads volume, but India and Indonesia post the fastest per-capita expansion. The Food Safety and Standards Authority of India's clearance for recycled plastic in food contact applications further lowers entry barriers for PCR-rich thin wall designs. Regional converters invest heavily in multilayer extrusion-thermoforming lines configurable for both polypropylene and emerging bio-resins, boosting supply resilience.

Europe commands significant share by virtue of early sustainability mandates and a continental focus on circularity. Plastic taxes and EPR regimes intensify cost pressures yet simultaneously reward companies capable of delivering 30% or greater recycled content without sacrificing seal integrity. Germany, France and the Nordics are hotbeds for IML adoption as retailers push mono-material packaging in private-label assortments. Eastern European nations, aided by lower labour costs, emerge as contract-manufacturing hubs that feed Western demand while navigating identical regulatory thresholds.

The Middle East and Africa cluster offers nascent but promising prospects, particularly in frozen-dairy exports and regional QSR chains that seek high-heat-resistant PP cups. South American growth is tethered to agricultural value-addition and an expanding middle class attracted to convenience formats. Local resin production in Brazil provides cost advantage; however, unreliable recycling infrastructure limits circular material sourcing, slowing penetration of PCR-rich thin wall offerings.