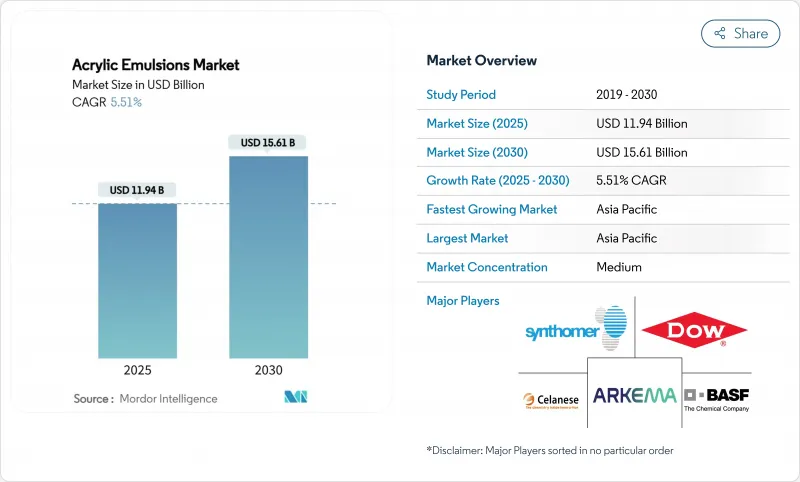

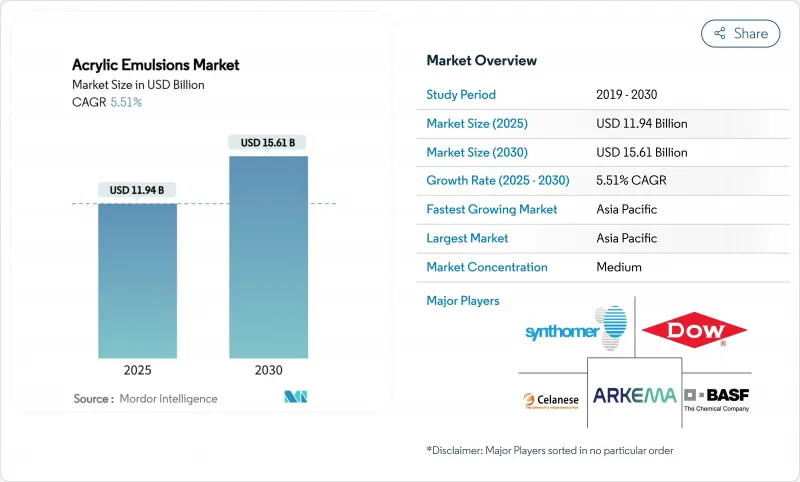

아크릴 에멀전 시장 규모는 2025년에 119억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.51%로, 2030년에는 156억 1,000만 달러에 이를 것으로 예상됩니다.

수용성 제제에 유리한 규제 압력, 아시아태평양의 견조한 인프라 지출, 디지털 인쇄 기술의 급속한 채용이 이러한 확대를 뒷받침하고 있습니다. 페인트 제조업체, 접착제 제조업체, 제지 회사는 미국, 캐나다, 유럽 연합(EU)의 낮은 VOC 규칙에 대한 적합성을 보장하기 위해 솔벤트 시스템에서 수성 시스템으로의 전환을 계속하고 있습니다. 동시에 제조업체는 프리미엄 틈새 시장을 획득하기 위해 자기 가교형 및 PFAS 프리 화학물질에 투자하고 있으며, 미국과 네덜란드에서는 생산 능력의 증강이 공급의 안정을 지키고 있습니다. 원료 가격의 변동은 마진을 압박하지만 기술 업그레이드와 지속가능성에 대한 헌신은 가치 기반 가격 설정에 여유를 가져오고 단량체 비용이 변동하더라도 생산자는 수익성을 유지할 수 있습니다.

캘리포니아는 건축용 평판 도료의 VOC 함량을 50g/L로 제한하고 있으며, 배합업자는 용제를 많이 포함하는 화학물질을 단계적으로 삭감할 필요가 있습니다. 미국 환경보호청은 에어로졸 도료의 준수 기한을 2027년 1월까지 연장하여 용제형에 필적하는 수성 배합을 완성할 시간을 생산자에게 주었습니다. 캐나다에서는 2024년 1월에 130개의 소비자 제품 카테고리에서 VOC 규제가 시행되어 아크릴 에멀전에 수요를 유도하는 세계 규제 변화가 강화되었습니다. 따라서 생산자는 외부 가교제를 사용하지 않고 필름 경도를 높이는 자기 가교 시스템을 확대하여 대응 가능한 시장을 넓히고 있습니다. 이러한 정책의 움직임은 아크릴 에멀전 시장에 다년간의 전망을 제공하고 단량체 비용의 변동을 상쇄하는 데 도움이 됩니다.

중국의 2025년 예산은 GDP 성장률 5% 목표를 유지해 1조 1,100억 달러의 인프라 지출에 뒷받침되고 있는 한편, 인도는 2025-2026년의 자본 지출을 11.1% 증가한 11조 1,100억 루피로 확대했습니다. 새로운 고속도로, 지하철, 산업 단지는 아크릴 분산체를 사용하는 건축용 페인트, 콘크리트 첨가제, 연포장용 접착제의 소비를 증가시킵니다. 동남아 전역에서는 제조업의 이전이 공장 건설을 촉진하고 생산량을 증대시키고 있습니다. 아크릴 에멀전은 내구성, 접착성, 낮은 악취성을 갖추고 있기 때문에 환경 기준의 강화에 대응해야 하는 건설업자에게 바인더로 선정되고 있습니다. 중간소득층의 소득수준 상승도 주택의 교체주기에 박차를 가해 기준선 수요의 저견도를 유지하고 있습니다.

수성 폴리우레탄 디스퍼전은 내약품성이나 내마모성으로 아크릴을 능가하는 경우가 많고, 자동차 트림, 바닥재, 고내구성 금속 도료로 그 지위를 확립하고 있습니다. 최근 2K UV 경화형 폴리우레탄 화학물질 조사는 저배기 가스 성능의 획기적인 발전을 강조하고 있습니다. 아크릴은 하이브리드 설계와 자기 가교 네트워크에서 이에 대응하고 있지만, 매우 높은 스트레스 환경에서의 격차는 여전히 남아 있으며, 일부 프리미엄 틈새 시장에서 점유율 확대를 멈추고 있습니다. 그럼에도 불구하고, 아크릴 수지는 중간 성능 층에서 비용과 공정의 우위를 유지하며 완전한 교체가 아닌 균형 잡힌 경쟁을 보장합니다.

스티렌-아크릴 등급은 2024년 세계 매출의 45.18%를 차지했습니다. 그것의 균형 잡힌 경도, 내수성, 가격에 의해 내장 건축 도료나 종이의 포화 라인의 주력 제품으로서 자리매김하고 있습니다. 2030년까지 스티렌-아크릴계의 수량은 꾸준히 증가하지만, 사용자가 비닐계를 많이 포함하는 시스템으로 다양화됨에 따라 이 부문의 점유율은 하강선을 따라갈 것으로 보입니다. 비닐 아크릴계 에멀전은 유연한 건축용 접착제, 실란트, 저온 코팅 보드 수요에 힘입어 연률 6.22%를 나타낼 것으로 전망됩니다. 순수 아크릴 에멀전은 착색과 UV 내구성이 최우선으로 하는 고광택 외벽이나 쿨 루프 엘라스토머에 사용되어 고급품의 지위를 차지하고 있습니다.

고급 자기 가교 기술이 이 계층을 강화하고 있습니다. 스티렌-아크릴계 로드 실런트에 있어서 DAAM-ADH 네트워크는 기존 그레이드보다 접착 강도를 50% 이상 향상시킨다고 하는 연구 결과가 나와 있습니다. 생산자는 고객이 최소한의 실험실 재조합으로 Tg와 경도를 미세 조정할 수 있는 모듈형 플랫폼을 판매하고 있어 시장 투입까지의 시간을 절약하고 있습니다. 한편, 비닐 아크릴계 수지공급자는 라미네이트 바닥재와 웨더 배리어막의 열 사이클을 견디는 가소제 프리의 유연성을 강조하고 있습니다. 순수 아크릴은 지속가능성을 중시하는 건축가를 대상으로 바이오의 단량체 옵션을 활용하여 저가의 화학제품과의 가치 격차를 넓히고 있습니다.

아시아태평양은 2024년 세계 매출의 46.21%를 차지했고, 2030년까지의 CAGR은 6.09%를 나타낼 전망입니다. 중국의 바밴드 사이트의 확장은 활기 넘치는 유틸리티용 페인트의 소비에 현지 바인더를 공급하고, 인도의 설비 투자 파이프라인의 증강은 새로운 상업시설과 주택의 바닥 면적에 직결됩니다. 베트남과 인도네시아와 같은 ASEAN 회원국은 OECD 구매자 기준을 충족하기 위해 수성 페인트에 의존하는 수출 지향 가구 및 포장 클러스터를 보유하고 있습니다. 또한 이 지역에는 세계 규모의 원료 공장이 있어, 종합 제조업체가 비용 압력과의 균형을 잡아 규모의 경제를 추진할 수 있게 하고 있습니다.

북미는 여전히 규제 동향 세터입니다. EPA의 에어로졸 규제 개정과 CARB의 낮은 VOC 캡은 지속적인 R&D 투자를 강력하지만 동시에 검증된 컴플라이언스 신임을 가진 기존 기업을 옹호합니다. 미국 인프라 투자 및 고용 촉진법(Infrastructure Investment and Jobs Act)을 기반으로 한 인프라 갱신은 교량, 교통 허브, 공공 건축물에 대한 투자를 하고 있으며, 이들 모두에 내구성이 있는 저 냄새 도료가 사용되고 있습니다. 2024년에 시행되는 캐나다 국가 전체의 VOC 규정은 요구사항을 조화시키고 국경을 넘어 제품 포트폴리오를 간소화했습니다. 멕시코의 마키라도라 네트워크는 수출 승인을 얻기 위해 수성 마감을 지정하는 가전 및 자동차 제조업체를 유치하고 있습니다.

유럽은 지속가능성의 리더십을 중시하고 있습니다. BASF의 바이오베이스 에틸 아크릴레이트로의 이동과 네덜란드의 분배 확대는 화학 밸류체인의 탈탄소화를 위한 이 지역의 추진력을 보여줍니다. 독일은 건축 효율 보조금을 통해 쿨 루프 리노베이션을 지원하고 반사형 아크릴 막 시장을 확대하고 있습니다. 프랑스와 영국은 공공 조달에서 순환 경제 기준을 추진하고 수명주기 평가의 뒷받침이있는 수지를 우월합니다. 남미와 중동, 아프리카는 합쳐져도 세계 소비량의 10%에 미치지 못하지만, 도시화의 진전과 주택 융자에 대한 접근성 향상으로 주택의 교체와 인프라 정비 프로젝트가 촉진되어 장기적인 상승을 가져옵니다.

The Acrylic Emulsions Market size is estimated at USD 11.94 billion in 2025, and is expected to reach USD 15.61 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030).

Regulatory pressure that favors water-borne formulations, steady infrastructure spending in Asia-Pacific, and rapid adoption of digital printing technologies underpin this expansion. Paint makers, adhesive formulators, and paper converters continue to switch from solvent to water-borne systems to secure compliance with low-VOC rules in the United States, Canada, and the European Union. At the same time, manufacturers are investing in self-crosslinking and PFAS-free chemistries to capture premium niches, while capacity additions in the United States and the Netherlands safeguard supply security. Though feedstock price volatility presses margins, technology upgrades and sustainability commitments provide headroom for value-based pricing, enabling producers to preserve profitability even when monomer costs fluctuate.

California continues to cap VOC content for flat architectural paint at 50 g/L, compelling formulators to phase out solvent-rich chemistries. The United States Environmental Protection Agency extended aerosol coating compliance dates to January 2027, granting producers time to perfect water-based blends that match solvent-borne performance. Canada enforced VOC limits across 130 consumer product categories in January 2024, reinforcing a global regulatory shift that channels demand toward acrylic emulsions. Producers are therefore scaling self-crosslinking systems that raise film hardness without external crosslinkers, widening the addressable market. These policy moves give the acrylic emulsions market multi-year visibility and help offset monomer-cost swings.

China's 2025 budget maintains a 5% GDP growth target, supported by USD 1.11 trillion in infrastructure outlays, while India increased 2025-26 capital expenditure by 11.1% to INR 11.11 lakh crore. New highways, metros, and industrial parks lift consumption of architectural coatings, concrete additives, and flexible packaging adhesives that employ acrylic dispersions. Across Southeast Asia, manufacturing relocations drive factory construction, magnifying volumes. Because acrylic emulsions provide durability, adhesion, and low odor, they remain the binder of choice for builders that must meet tightening environmental standards. Rising middle-class income levels also spur residential repaint cycles, keeping baseline demand resilient.

Water-borne polyurethane dispersions often outclass acrylics in chemical and abrasion resistance, allowing them to gain ground in automotive trim, wood flooring, and heavy-duty metal coatings. Recent research on 2K UV-curable polyurethane chemistries highlights breakthroughs in low-emission performance. While acrylics answer with hybrid designs and self-crosslinking networks, the gap in very high-stress environments remains, capping share growth in select premium niches. Yet acrylics retain cost and process advantages in the mid-performance tier, ensuring balanced competition rather than outright displacement.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Styrene-acrylic grades held 45.18% of global revenue in 2024. Their balanced hardness, water resistance, and price position them as the workhorse for interior architectural paint and paper saturation lines. Through 2030, styrene-acrylic volumes will climb steadily, but the segment's share will edge downward as users diversify into vinyl-rich systems. Vinyl-acrylic emulsions are set to grow 6.22% annually, riding demand for flexible construction adhesives, sealants, and low-temperature coated boards. Pure acrylics command the premium tier, favored in high-gloss exterior walls and cool-roof elastomeric where colour retention and UV durability are paramount.

Advanced self-crosslinking technologies reinforce this hierarchy. Studies show DAAM-ADH networks in styrene-acrylic road sealants boost bond strength by more than 50% over conventional grades. Producers market modular platforms that let customers fine-tune Tg and hardness with minimal lab reformulation, saving time to market. Meanwhile, vinyl-acrylic suppliers stress plasticizer-free flexibility that withstands thermal cycling in laminate flooring and weather-barrier membranes. Pure acrylics leverage bio-based monomer options to target sustainability-conscious architects, widening the value gap versus lower-priced chemistries.

The Acrylic Emulsions Market Report is Segmented by Type (Pure Acrylic Emulsion, Styrene Acrylic Emulsion, and Vinyl Acrylic Emulsion), Application (Paints and Coatings, Construction Material Additives, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific contributed 46.21% of global revenue in 2024 and will post a 6.09% CAGR to 2030. China's Verbund site expansions supply local binders for booming public-works paint consumption, while India's elevated capex pipeline translates directly into fresh commercial and residential floor space. ASEAN members such as Vietnam and Indonesia host export-oriented furniture and packaging clusters that rely on water-borne coatings to meet OECD buyer standards. The region also houses world-scale feedstock plants, enabling integrated players to balance cost pressure and drive economies of scale.

North America remains a regulatory trendsetter. The EPA's revised aerosol rules and CARB's low-VOC caps force continuous R&D investment, yet they simultaneously defend incumbents with proven compliance credentials. Infrastructure renewal under the U.S. Infrastructure Investment and Jobs Act pumps spending into bridges, transit hubs, and public buildings, all of which favor durable, low-odor coatings. Canada's country-wide VOC regulations, effective 2024, harmonize requirements and simplify cross-border product portfolios. Mexico's maquiladora network attracts appliance and automotive manufacturers that specify water-borne finishes to secure export approvals.

Europe emphasizes sustainability leadership. BASF's shift to bio-based ethyl acrylate and the Dutch dispersion expansion illustrate the region's drive to decarbonize the chemicals value chain. Germany supports cool-roof retrofits through building-efficiency subsidies, widening the market for reflective acrylic membranes. France and the United Kingdom promote circular-economy criteria in public procurement, favoring resins with life-cycle-assessment backing. Although South America and the Middle-East and Africa together represent less than 10% of global consumption, rising urbanization and increased access to mortgage financing encourage residential repainting and infrastructure projects, providing long-run upside.