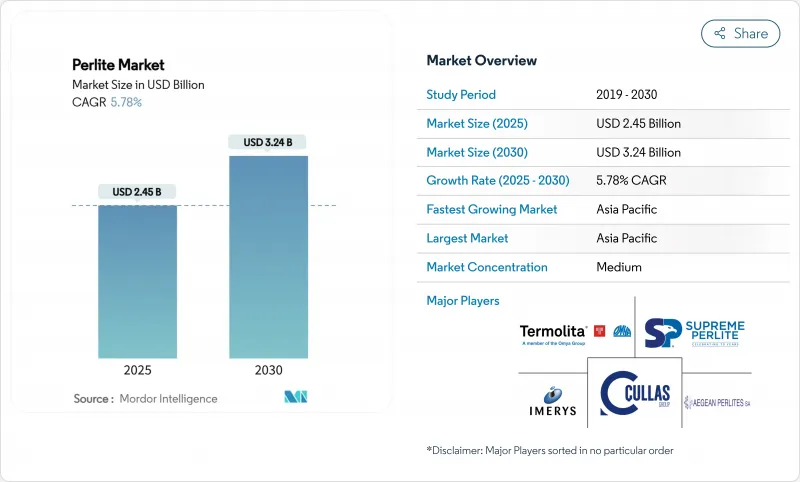

펄라이트 시장 규모는 2025년에 24억 5,000만 달러로 추정되고, 2030년에는 32억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 5.78%를 나타낼 전망입니다.

이 전망은 에너지 효율적인 건설, 원예, 정밀 여과, 극저온 단열재에서 경량 골재의 왕성한 수요를 반영합니다. 특히 유럽과 북미에서는 열성능 벤치마크를 엄격화하는 건축기준법이 수량 성장을 강화하고, 아시아태평양에서는 급속한 도시화가 대규모 인프라 수요를 창출하고 있습니다. 극저온 저장, 공예 음료 여과, 화장품용 특수 등급은 더 높은 금리를 제공하고 제품 혁신을 지원합니다. 튀르키예와 미국에는 풍부한 화산 광석이 있기 때문에 공급은 여전히 충분하지만 물류 비용은 지역별 가격 차이에 영향을 미칩니다.

펄라이트의 콘크리트와 석고는 열 성능을 희생하지 않고 구조 하중을 낮추고 작은 기초에서 더 높은 건물을 가능하게 합니다. 팽창한 입자는 모래나 자갈보다 중량이 최대 80% 가볍기 때문에 운송의 절약으로 이어집니다. 모듈식 건축 공장에서는 현장 조립 시간을 단축하고 엄격한 열 브리지 제한을 충족하기 위해 펄라이트 강화 패널의 지정이 증가하고 있습니다. 조립식 제조 라인은 이 미네랄의 일관성으로 인해 배치 정밀도가 향상되고 불량품이 감소한다는 장점이 있습니다. 중국, 인도, ASEAN 지역의 장기적인 도시화로 인해 펄라이트 시장은 지속 가능한 고층 건축용 경량 골재의 선호 공급원으로 자리매김하고 있습니다.

환경 제어형 농장에서는 뿌리 썩음을 막으면서 수분을 유지하는 무균으로 pH 중성의 재이용 가능한 기질로서 펄라이트가 편리하게 되어 있습니다. 미국과 네덜란드의 상업 온실에서는 펄라이트가 이탄을 많이 포함하는 믹스를 대체하여 수율이 증가했다고 보고하고 있습니다. 업계별로 자동 관개 시스템이 정확한 산소 수준을 유지할 수 있도록 거친 등급이 선택되었습니다. 의료용 대마 전문 재배자는 의약품 재배용으로 인증된 초청정 등급에 프리미엄 가격을 지불합니다. 동남아시아에서 확대되는 도시농업은 현지 가공업자가 높은 운송비를 들이지 않고 신선한 배지를 공급할 수 있게 하고 지역 펄라이트 시장 수요를 뒷받침하고 있습니다.

버미큘라이트, 락울, 팽창 점토는 무게와 R 값으로 직접 경쟁합니다. 재활용 발포 폴리스티렌(EPS) 비드는 높은 사용 온도를 필요로하지 않는 경량 스크리드로 점유율을 늘리고 있습니다. 여과에서 인공 합성 배지는 더 좁은 컷오프 임계값을 달성하고 무균 제약 라인에서 펄라이트의 위치를 위협합니다. 원예 분야에서는 지속가능성이 우수하다고 주장하는 코코넛 코이아와 같은 바이오 라이벌에 직면하고 있습니다. 펄라이트 공급업체가 가격에 민감한 틈새 분야에서의 점유율을 보호하기 위해서는 제품 혁신과 용도 지원이 필수적인 것은 아닙니다.

건축용 석고, 원예용 믹스, 산업용 루즈필 단열재에 널리 받아들여지고 있는 것을 반영하여, 팽창 펄라이트는 2024년에 펄라이트 시장의 67.56%의 점유율을 확보했습니다. 성숙한 채용으로 가격 경쟁력을 유지하고 있으며 공급업체는 물류 효율과 광석 정화를 강조하고 금리를 확보합니다. 전문 제조 업체는 현재 극저온 탱크 내에서 먼지를 견딜 수있는 고밀도 Vapex 및 코팅 등급을 추진하고 있으며, 화장품 제조업체는 얼굴 스크럽 용으로 미세하게 분류 된 분말을 요구하고 있습니다. 신흥의 특수 등급층은 2030년까지 연평균 복합 성장률(CAGR) 6.45%를 나타내 표면기능화에 초점을 맞춘 R&D 지출을 흡수할 것으로 예측됩니다.

Vapex 및 Speciality Grade는 제약용 여과나 공간에 제약이 있는 LNG 모듈에서는 기술적 임계값에 따라 승인이 좌우되므로 불균형한 부가가치를 낳습니다. 치료사는 실란 처리나 폴리머 처리를 실시해, 단가를 범용 팽창 펄라이트의 몇 배로 끌어올리고 있습니다. 아그로퍼라이트는 밸런스드한 보수 능력과 중성 pH를 평가하는 온실에서 안정적인 양을 유지하고 있습니다. 주조 슬래그 제거용 괴광석을 포함한 다른 제품 유형은 소규모 틈새 시장을 차지하지만 고정 고객과의 관계에서 이익을 얻고 있습니다. 포트폴리오의 구성은 펄라이트 시장의 이분화 추세를 보여주며, 한편으로는 대량 생산의 범용 단열재가, 다른 한편으로는 소량 생산의 고가치 엔지니어링 등급이 있습니다.

2024년 소비량은 아시아태평양이 48.75%를 차지했고 2030년까지의 CAGR은 6.88%를 나타낼 전망입니다. 중국의 14차 5개년 계획에서는 조립식 주택과 그린 빌딩이 중시되고 있으며, 모두 경량 골재의 대량 소비국입니다. 인도의 스마트 시티 임무는 펄라이트 패널을 사용하여 사하중과 리노베이션 기간을 줄이는 복합 애플리케이션 개발에 자금을 제공합니다. 일본, 한국, 대만은 전자공장과 하이테크 온실을 위한 초청정 등급을 요구하고 있습니다. 인도네시아와 필리핀의 국내 가공업자들은 수입에 대한 의존도를 낮추기 위해 광석 채굴에 후방 통합하고 있습니다.

북미는 여전히 기술과 특수 등급의 아성입니다. 미국 텍사스 주와 루이지애나 주에 위치한 LNG 수출 터미널에서는 1억 갤런의 저장 탱크에 루즈필 펄라이트가 사용되며 캐나다 대마초 생산자는 원예용 등급을 대량으로 구입하고 있습니다. 미국 난방 냉동 공조 학회(ASHRAE) 90.1-2025와 같은 에너지 기준은 펄라이트의 공동 충전을 포함하여 더 깊은 단열 보수의 방아쇠가되었습니다. 유럽은 EU의 제로 방출 건축 지령의 혜택을 받고 있으며, 독일, 프랑스, 이탈리아의 개수 프로그램에 의해 광물계 단열재의 보급이 가속하고 있습니다. 그리스와 튀르키예의 지중해산 광석 공급은 인건비 상승에도 불구하고 육상비의 경쟁력을 유지하고 있습니다.

남미와 중동 및 아프리카의 점유율은 작지만 전략적입니다. 브라질의 아마존 지역은 보호되기 때문에 도시의 중심부는 수직으로 확장되어 가볍고 수송 에너지가 적은 골재가 선호됩니다. 칠레의 리튬 염수 사업에서는 증발 전의 미립자 제거에 펄라이트 여과 보조제가 채용됩니다. 걸프 협력 회의 국가는 사막의 더위를 완화하기 위해 LNG 픽업 허브를 단열하고 남아프리카의 신흥 온실 클러스터는 물 부족을 보완하기 위해 원예 펄라이트를 조달합니다. 물류와 규모의 과제는 남아 있지만, 이러한 지역은 조기에 투자하는 시장 진출기업에 장기적인 상승 여지가 있습니다.

The Perlite Market size is estimated at USD 2.45 Billion in 2025, and is expected to reach USD 3.24 Billion by 2030, at a CAGR of 5.78% during the forecast period (2025-2030).

The outlook reflects strong demand for lightweight aggregates in energy-efficient construction, horticulture, precision filtration and cryogenic insulation. Construction codes that tighten thermal-performance benchmarks, especially in Europe and North America, reinforce volume growth, while rapid urbanization in the Asia Pacific creates large-scale infrastructure demand. Specialty grades for cryogenic storage, craft-beverage filtration and cosmetics deliver higher margins and anchor product innovation. Supply remains adequate because of abundant volcanic ore in Turkey and the United States, yet logistics costs influence regional pricing differentials.

Perlite concrete and plasters lower structural load without sacrificing thermal performance, enabling taller buildings on smaller foundations . Transportation savings arise because expanded particles weigh up to 80% less than sand and gravel. Modular building factories increasingly specify Perlite-enhanced panels to shorten on-site assembly time and meet stringent thermal-bridge limits. Prefabrication lines benefit from the mineral's consistency, which improves batching accuracy and reduces rejects. Long-term urbanization in China, India and the ASEAN bloc positions the Perlite market as a preferred source of lightweight aggregates for sustainable, high-rise construction.

Controlled-environment farms value Perlite for sterile, pH-neutral, reusable substrates that retain moisture while preventing root rot. Commercial greenhouses in the United States and the Netherlands report yield gains when Perlite replaces peat-heavy mixes. Vertical-farm operators choose coarse grades that allow automated fertigation systems to maintain precise oxygen levels. Specialty growers of medical cannabis pay premium prices for ultra-clean grades certified for pharmaceutical cultivation. Expanding urban agriculture in Southeast Asia positions local processors to supply fresh media without high freight costs, underpinning regional Perlite market demand.

Vermiculite, rock wool, and expanded clay compete directly on weight and R-value, while glass wool often offers a lower installed cost in large-scale commercial projects. Recycled expanded polystyrene (EPS) beads gain share in light screeds that do not require high service temperatures. In filtration, engineered synthetic media achieve narrower cut-off thresholds, threatening Perlite's position in sterile pharmaceutical lines. Horticulture faces bio-based rivals such as coconut coir that claim superior sustainability credentials. Product innovation and application support remain crucial for Perlite suppliers to defend their share in price-sensitive niches.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Expanded Perlite secured a 67.56% share of the Perlite market in 2024, reflecting broad acceptance in construction plasters, horticultural mixes, and industrial loose-fill insulation. Mature adoption keeps prices competitive, and suppliers emphasize logistics efficiency and ore purification to safeguard margins. Specialty producers now promote higher-density Vapex and coated grades that resist dusting inside cryogenic tanks, while cosmetic manufacturers demand finely classified powders for facial scrubs. The emerging specialty tier is projected to expand at a 6.45% CAGR to 2030, absorbing research and development (R&D) spend focused on surface functionalization.

Vapex & Specialty Grades add disproportionate value because technical thresholds govern approval in pharmaceutical filtration and space-constrained LNG modules. Processors apply silane or polymeric treatments that raise unit pricing several-fold relative to commodity expanded Perlite. Agro-Perlite maintains steady volumes in greenhouses that appreciate its balanced water-holding capacity and neutral pH. Other product types, including lump ore for foundry slag removal, occupy smaller niches yet benefit from captive customer relationships. The portfolio mix indicates a Perlite market trend toward bifurcation, high-volume commoditized insulation on one flank and low-volume, high-value engineered grades on the other.

The Perlite Market Report is Segmented by Product Type (Expanded Perlite, Agro-Perlite, and More), Application (Insulation, Fire-Proofing & Refractory, and More), End-Use Industry (Construction & Infrastructure, Horticulture & Agriculture, Industrial Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific accounted for 48.75% consumption in 2024 and is set to expand at a 6.88% CAGR through 2030. China's 14th Five-Year Plan emphasizes prefabricated housing and green buildings, both heavy consumers of lightweight aggregates. India's Smart Cities Mission funds mixed-use developments that use Perlite panels to reduce dead load and renovation timelines. Japan, South Korea, and Taiwan demand ultra-clean grades for electronics fabs and high-tech greenhouses. Domestic processors in Indonesia and the Philippines back-integrate into ore mining to reduce import reliance.

North America remains a technology and specialty-grade stronghold. United States LNG-export terminals in Texas and Louisiana consume loose-fill Perlite for 100-million-gal storage tanks, while Canadian cannabis producers buy horticultural grades in bulk. Energy codes such as American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 90.1-2025 trigger deeper insulation retrofits, including Perlite cavity fills. Europe benefits from the EU zero-emission-building directive, with retrofit programs in Germany, France, and Italy accelerating mineral-based insulation uptake. Mediterranean ore supply from Greece and Turkey keeps landed cost competitive despite higher labor expenses.

South America and the Middle East & Africa together deliver a smaller yet strategic share. Brazil's protected Amazon region prompts urban centers to expand vertically, favoring lightweight, low-transport-energy aggregates. Chilean lithium brine operations adopt Perlite filter aids to remove fine particulates before evaporation. Gulf Cooperation Council countries insulate LNG transshipment hubs to mitigate desert heat, and South Africa's emerging greenhouse cluster sources horticultural Perlite to offset water scarcity. Although logistics and scale challenges persist, these regions present long-term upside for market participants that invest early.