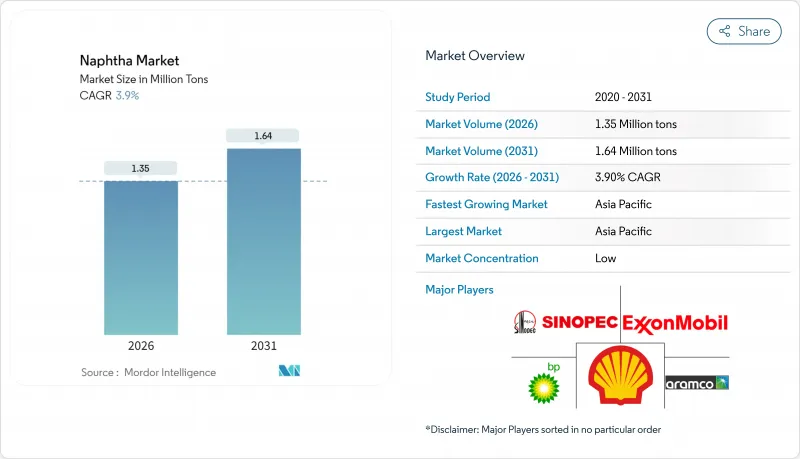

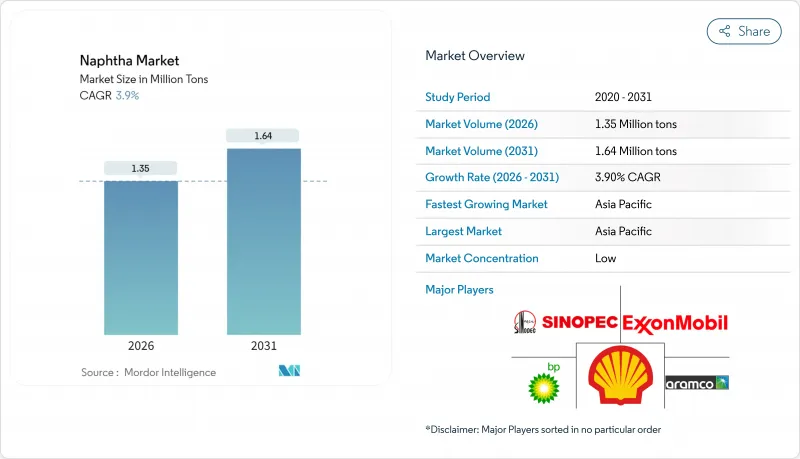

세계의 나프타 시장은 2025년 130만톤에서 2026년 135만톤으로 성장하고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 3.9%로 성장을 지속하여 2031년까지 164만톤에 달할 것으로 예측되고 있습니다.

수요는 올레핀 및 방향족 화합물의 주요 석유화학 원료로서 나프타의 역할에 의해 지원되고 있으며, 에틸렌 수율 향상을 위해 경질 분획을 선호하는 대규모 스팀 크래커에 의해 그 지위가 강화되고 있습니다. 미국 멕시코 걸프의 콘덴세이트 분해 장치에 대한 투자와 아시아의 신규 통합 정유소 건설은 세계 무역 흐름을 재구성하는 한편, 바이오나프타의 생산 능력 증강은 보완적인 저탄소 공급원을 제공합니다. 주요 정유 회사는 업스트림 원유 공급과 하류 석유 화학 전환을 통합하여 밸류체인 전반에 걸쳐 가치를 창출하고 있습니다. 그러나 원유와 나프타의 스프레드 변동, 대체 원료로서의 천연 가스 액체의 매력 증가, 그리고 엄격한 탄소 규제는 마진의 안정성과 자본 배분 결정에 불확실성을 가져옵니다.

중국에서는 파라핀계 조성이 에틸렌 생산량을 극대화하기 때문에 경질 나프타 소비량을 증대시키는 메가크래커의 잇따른 가동이 진행중입니다. 2028년까지 총 0.8-110만 배럴/일의 정제 처리 능력을 가진 신규 설비는 나프타 수율 비율을 높이는 콘덴세이트 분해 장치를 통합 설계하고 있습니다. Hengli Petrochemical 및 Fujian Petrochemical의 생산능력 향상은 수요 상승세를 유지하고 응축유 함량이 많은 원유의 수입이 구조적으로 증가하게 되어 지역 가격이 광범위한 나프타 시장과 일치하도록 촉구합니다. 공급 안정성 확보의 인센티브로 중동 생산자와 아시아 크래커 사업자 간의 장기적인 오프테이크 계약이 체결되어 지역 밸류체인이 더욱 밀접해지고 있습니다. 넷백 계산에 의하면, 스팀 크래커 복합 시설이 1기 증설될 때마다, 지역의 경질 나프타 수요는 연간 150만 톤 증가해, 이 촉진요인이 전체적인 성장에 크게 기여하고 있는 것을 뒷받침하고 있습니다.

바레인의 Bapco 현대화 계획과 Saudi Aramco의 110억 달러 규모의 아미랄 복합시설은 가솔린 옥탄가와 방향족 생산량을 높이기 위해 혼합 원료 크래커와 접촉 개질장치를 동일 입지시키는 전략적 전환을 보여줍니다. 이 모델은 전통적으로 자동차 연료 풀로 유입 된 직류 나프타를 고 마진 석유 화학제품 라인으로 전환하여 정유소 전체의 조익률을 향상시킵니다. 통합은 유틸리티 공유를 통해 에너지 효율을 향상시키고 마진 변동을 완화하는 유연한 원료 메뉴를 제공합니다. AMIRAL 단독으로도 연간 약 500만 톤의 나프타를 필요로 하기 때문에 이 지역은 아시아를 위한 스윙 공급자가 되어, 지역간의 수급 밸런스를 긴밀화시켜, 보다 견조한 나프타 시장을 지원하게 됩니다.

지정학적 사건과 정유소의 가동 정지는 나프타 크랙 스프레드의 급격한 변동을 일으켜, 정유소의 조업 계획에 과제를 가져, 처리량의 삭감을 촉진하고 있습니다. 아덴 만의 제품 유조선에 대한 공격으로 2024년 초에는 아시아 나프타 크랙이 2년 만에 높은 가격을 기록했지만, 재정 거래 화물이 입하함에 따라 스프레드는 급속히 회복되었습니다. 2019년 이후의 미국 정유소 능력은 여전히 피크 때보다 62만 배럴/일 부족해, 세계공급 버퍼는 얇고, 변동성을 증폭시키고 있습니다. 이 불안정성은 악조건 하에서 정유소의 가동률을 최대 8% 저하시켜 트레이더의 운전 자금 요건을 높여 나프타 시장의 확대를 억제하고 있습니다.

2025년 경질 나프타는 세계 나프타 시장의 57.62%를 차지했습니다. 이것은 현대 크래커가 우수한 에틸렌 수율을 얻기 위해 높은 파라핀 함량을 선호하기 때문입니다. 이 부문은 2031년까지 연평균 복합 성장률(CAGR) 4.55%를 보일 것으로 예측되며, 컷 유형 중에서 가장 높은 성장률을 보이고 있습니다. 미국과 아시아의 커패시터트 분리장치의 확장은 크래커의 원료 구성 요건에 맞는 파라핀계 컷의 생산을 목적으로 하고 나프타 시장에서 본 부문의 주도적 지위를 강화하고 있습니다. 10만 배럴/일의 분리장치마다 약 3만 배럴/일의 경질 나프타가 생산되어, 수급 밸런스를 압박하고, 가솔링 등급 원료에 대한 프리미엄을 지지하고 있습니다. 통합 운영자는 마진 사이클을 헤지하고 전체 자산의 가동률을 향상시키기 위해 스플리터의 유체와 개질 장비의 제품을 혼합합니다.

중질 나프타는 방향족 함량이 높고 에틸렌 생산성이 낮기 때문에 성장률은 중간 정도의 단일 자릿수에 머물고 있습니다. 그러나, 옥탄가 향상과 벤젠 톨루엔 크실렌 생성을 목적으로 한 접촉 개질 장치에 있어서는 여전히 필수적인 원료입니다. 백금 주석계 및 백금 레늄계 이원 금속 촉매에 대한 투자에 의해 개질 장치의 내중질성 향상을 도모하고, 중질 원료의 처리 가능 범위가 확대되고 있습니다. 정제업체는 가솔린 스프레드가 축소되었을 때 중질 분획을 수익화하는 수단으로 방향족 제품 판매계약을 활용하여 나프타 시장에 대한 지원적이면서도 활력이 저하된 공헌을 유지하고 있습니다.

나프타 시장 보고서는 유형별(경질 나프타, 중질 나프타), 공급원별(정유소 기반, 바이오나프타 등), 최종사용자 산업별(석유화학, 농업, 페인트 및 코팅, 항공우주, 기타 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양은 2025년에 나프타 시장의 43.65%를 차지했으며, 2031년까지의 CAGR 4.65%로 성장하는 예측은 석유화학제품 및 비료의 동시성장에 기인하고 있습니다. 중국은 2023년 과거 최고의 1,480만 배럴/일의 원유 처리량을 기록해 원료의 자급 기반을 강화했습니다. 반면 인도의 고분자 수요는 2028년까지 3,500만 톤에 이를 전망입니다. Aramco의 Hengli Petrochemical에 대한 10% 투자와 Fujian 프로젝트는 중동 공급과 동아시아 수요 성장을 연결하는 지역 통합을 더욱 추진합니다.

북미에서는 콘덴세이트 분해 장치에 대한 투자와 셰일 액체의 생산 증가로 경질 나프타의 구조적인 공급 과잉 상태가 계속되고 있습니다. 미국의 정유 능력은 2023년 2% 증가했으며, 2024년 초 가동 가능 명목 능력은 1,840만 배럴/일에 달했습니다. 그러나 천연 가솔린(NGL) 공급 급증에 의해 석유화학 수요가 전용되고, 이 지역의 나프타 시장 확대 페이스는 둔화하고 있습니다. 라틴아메리카에 대한 수출 증가와 때때로 유럽에 대한 재정 거래는 계절적 공급 과잉을 상쇄합니다.

유럽의 나프타 수요는 재생가능한 연료 생산이 화석 원료를 대체하기 때문에 소폭으로 축소되지만, 잔류 리포머 설비는 방향족계 제품 및 고옥탄가 가솔린 블렌드 원료를 공급합니다. 정유소는 신규 설비 건설이 아닌 기존 설비의 HVO(고순도 바이오디젤) 및 SAF(지속 가능 항공 연료) 대응 개수를 진행하고 있어, 이것에 의해 기존 나프타의 배출량 감축을 목표로 하는 탄소 포집 파일럿 사업에 대한 투자 여력이 탄생하고 있습니다. 중동지역은 개질장치와 크래커를 결합한 통합 프로젝트를 활용하여 재정거래 기회가 생겼을 때 아시아 및 유럽에 대한 한계 공급원으로서의 지위를 확립합니다. 남미와 아프리카는 나이지리아의 Dangote 정유소(가솔린 나프타를 최대 8만 배럴/일 생산 예정) 등의 프로젝트를 통해 영향력을 확대하고, 지역의 무역수지를 점차 변화시키고 있습니다.

The Naphtha market is expected to grow from 1.30 million tons in 2025 to 1.35 million tons in 2026 and is forecast to reach 1.64 million tons by 2031 at 3.9% CAGR over 2026-2031.

Demand is anchored by naphtha's role as the dominant petrochemical feedstock for olefins and aromatics, a position reinforced by large-scale steam crackers that prefer light fractions for higher ethylene yields. Investments in condensate splitters along the U.S. Gulf Coast and new integrated refineries in Asia are reshaping global trade flows, while bio-naphtha capacity additions provide a complementary, low-carbon supply stream. Leading refiners integrate upstream crude supply with downstream petrochemical conversion to capture value across the chain. However, volatile crude-naphtha spreads, the growing appeal of natural gas liquids as alternative feedstocks, and increasingly stringent carbon regulations inject uncertainty into margin stability and capital-allocation decisions.

China is commissioning a wave of mega-crackers that elevate consumption of light naphtha because its paraffinic composition maximizes ethylene output. New capacity totaling 0.8-1.1 million b/d of refining throughput by 2028 is designed with integrated condensate splitters that raise naphtha yield ratios. Capacity additions at Hengli Petrochemical and Fujian Petrochemical will maintain upward demand momentum, translating into structurally higher imports of condensate-rich crudes and driving regional price alignment with the broader naphtha market. Supply security incentives are prompting long-term offtake agreements between Middle-East producers and Asian crackers, further knitting regional value chains. Net-back calculations suggest that each incremental steam cracker complex boosts regional light naphtha requirements by 1.5 million tons annually, underpinning the driver's substantial contribution to overall growth.

Bahrain's Bapco Modernization Programme and Saudi Aramco's USD 11 billion AMIRAL complex illustrate the strategic shift toward co-locating catalytic reformers with mixed-feed crackers to enhance gasoline octane and aromatic output. The model diverts straight-run naphtha that previously entered the motor-fuel pool into higher-margin petrochemical streams, improving overall refinery gross margins. Integration delivers energy-efficiency gains through shared utilities and furnishes flexible feedstock menus that dampen margin volatility. With AMIRAL alone requiring about 5 million tons of naphtha annually, the region becomes a swing supplier to Asia, tightening inter-regional balances and supporting a more robust naphtha market.

Geopolitical incidents and refining capacity outages drive sharp swings in naphtha crack spreads, challenging refinery scheduling and prompting throughput cuts. An attack on a product tanker in the Gulf of Aden sent Asian naphtha cracks to a two-year high in early 2024, yet spreads retraced swiftly as arbitrage cargoes arrived. With post-2019 U.S. refinery capacity still 620,000 b/d below the peak, global supply buffers remain thin, magnifying volatility. This instability dampens refinery utilization rates by up to 8% in adverse periods and raises working-capital requirements for traders, tempering naphtha market expansion.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Light naphtha generated 57.62% of the global naphtha market in 2025 as modern crackers favor its high paraffin content for superior ethylene yield. The segment is projected to grow at 4.55% CAGR to 2031, the briskest pace among cut types. Condensate splitter expansions in the United States and Asia are calibrated to produce paraffinic cuts that align with cracker slate requirements, reinforcing segment leadership in the naphtha market. Each 100,000 b/d splitter yields around 30,000 b/d of light naphtha, tightening balances and supporting premiums to gasoline-grade material. Integrated operators blend splitter streams with reformer output to hedge margin cycles and improve overall asset utilization.

Heavy naphtha lags with mid-single-digit growth owing to its higher aromatic content and lower ethylene productivity. Nonetheless, it remains an essential feedstock for catalytic reformers that upgrade octane and generate benzene, toluene, and xylenes. Investments in platinum-tin and platinum-rhenium bimetallic catalysts improve reformer severity tolerance, widening the processing window for heavier grades. Refiners leverage aromatics marketing agreements to monetize heavy cuts when gasoline spreads compress, preserving a supportive though less dynamic contribution to the naphtha market.

The Naphtha Market Report is Segmented by Type (Light Naphtha and Heavy Naphtha), Source (Refinery-Based, Bio-Naphtha, and Others), End-User Industry (Petrochemicals, Agriculture, Paints and Coatings, Aerospace, and Other Industries), and Geography (Asia Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Asia-Pacific led the naphtha market with 43.65% share in 2025, and its 4.65% forecast CAGR to 2031 stems from synchronized growth in petrochemicals and fertilizers. China processed a record 14.8 million b/d of crude in 2023, underpinning self-sufficiency in feedstocks, while India's polymer demand is on track to hit 35 million tons by 2028. Aramco's 10% stake in Hengli Petrochemical and the Fujian project further expand regional integration, aligning Middle-East supply with East-Asian demand growth.

North America remains structurally long light naphtha due to condensate splitter investments and rising shale liquids output. U.S. refining capacity climbed 2% in 2023, taking operable nameplate to 18.4 million b/d at the start of 2024. Yet surging NGL availability diverts petrochemical demand, moderating the regional naphtha market expansion pace. Export growth into Latin America and occasional arbitrage to Europe balances seasonal surpluses.

Europe's naphtha demand contracts modestly as renewable fuel production displaces fossil feedstocks, but residual reformer capacity supplies aromatics chains and high-octane gasoline blendstocks. Refiners retrofit existing units for HVO and SAF rather than building greenfield assets, freeing investment for carbon-capture pilots that lower the embedded emissions of conventional naphtha. The Middle East capitalizes on integration projects that couple reformers and crackers, positioning itself as the marginal supplier into Asia and Europe when arbitrage windows open. South America and Africa gain influence through projects such as Nigeria's Dangote refinery, which will produce up to 80 kbd of gasoline and naphtha, gradually transforming regional trade balances.