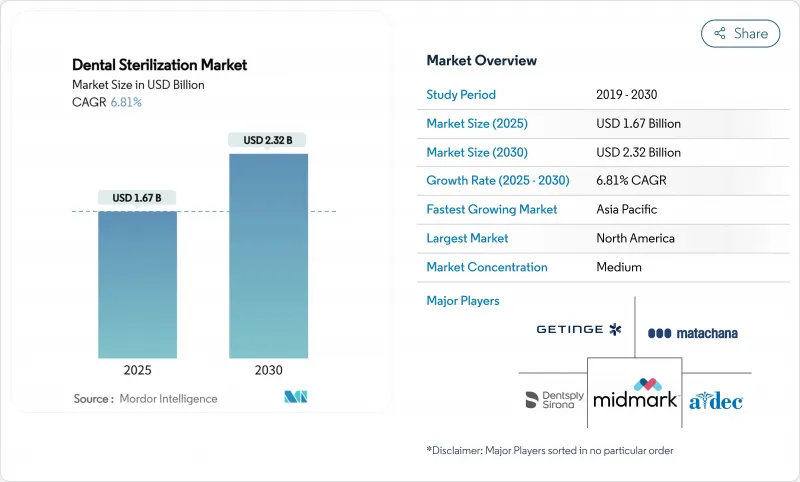

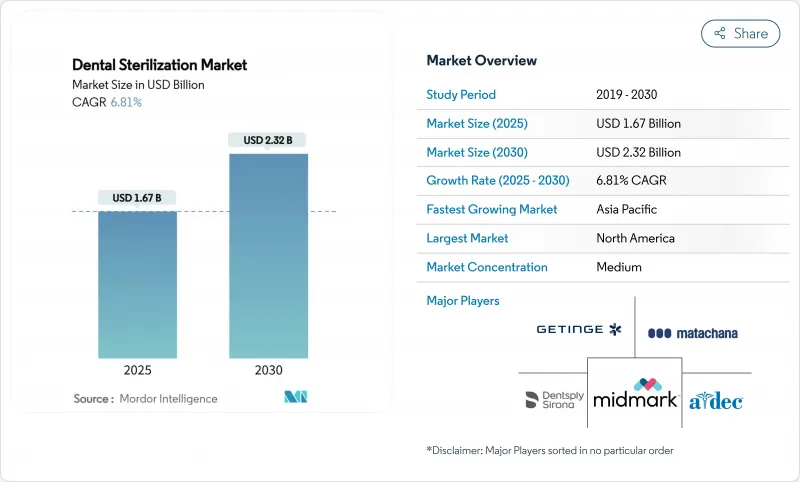

치과 멸균 시장 규모는 2025년에 16억 7,000만 달러로 추정되고 예측 기간 중(2025-2030년)의 CAGR은 6.81%로, 2030년에는 23억 2,000만 달러에 이를 것으로 예상됩니다.

감염 관리 규제 강화, 장비 회전율에 대한 기대를 높이는 디지털 워크플로우 채택 확대, 환경 및 직원의 안전 목표에 따른 꾸준한 기술 업그레이드가 확대를 뒷받침하고 있습니다. 북미는 확립된 상환제도와 스마트 오토클레이브의 조기 도입으로 2024년 매출 점유율은 38.16%를 나타냈습니다. 아시아태평양은 CAGR 8.39%로 성장해 고령화와 치과보험 적용 확대를 배경으로 멸균 인프라 갭을 빠르게 채우고 있습니다. 기구는 여전히 수익의 요인이지만, 일회용 소모품 및 액세서리에 대한 의존도가 높아지면서 구매 패턴이 재구성되어 경상적인 수익원이 증가하고 있습니다. 과산화수소 플라즈마 시스템은 에틸렌 옥사이드를 배출하지 않고 열에 민감한 장비를 처리 할 수 있기 때문에 틈새에서 주류로 전환하고 있습니다. 경쟁의 심각성은 적당하고 유동적입니다. 기존 벤더는 이익률이 높은 틈새 분야에 집중하기 위해 포트폴리오를 정리하고 있으며, 중견 혁신자는 진료 관리 플랫폼과 동기화되는 클라우드 연결 멸균기를 추구하고 있습니다.

2024년에는 2억 8,000만 명의 고령자들이 구강 장애를 경험하고 임상의가 기구의 회전주기를 에스컬레이션하는 복잡한 다중 방문 사례를 다뤘기 때문에 그 부담은 멸균 패턴을 이동시켰습니다. 세계보건기구(WHO)의 구강보건 전략은 감염 예방의 의무를 높이고 있으며, 클리닉은 사이클 타임을 연장하는 것보다 더 큰 용량의 멸균기를 구입하도록 촉구되고 있습니다. 아시아태평양의 신흥 시장은 환자수 증가와 역사적으로 자금 부족이었던 감염제어 인프라라는 두 가지 과제에 직면하고 있으며, 자본제약에도 불구하고 장비의 신속한 도입에 박차를 가하고 있습니다. 질병의 유행과 멸균 수요 간의 연관성은 비선형이며, 복잡한 치료에서는 종종 예약 당 여러 로드가 발생하고 기존 능력이 늘어납니다. 따라서 모듈형 또는 스택 가능한 오토클레이브 형식을 공급하는 제조업체는 이 인구 역학으로 인한 증가를 활용하는 위치에 있습니다.

베니어, 얼라이너, 디지털 스마일 디자인 등의 선택적 심미 치료는 2024년에 급증했으며, 각 치료에는 섬세한 바, 세라믹 프레스, 중합 칩이 사용되기 때문에 반복적으로 증기에 노출되는 것을 견딜 수 없습니다. 이 부문을 담당하는 클리닉은 무균 보증 수준을 유지하면서 60℃ 이하에서 작동하는 과산화수소 플라즈마 또는 오존 기반 시스템에 기울입니다. 수요의 집중은 여전히 미국과 서유럽에 집중되고 있지만, 한국, 일본, 인도의 대도시 중심부에서는 구미의 멸균 기준을 모방한 미용 클리닉이 급성장하고 있습니다. 뷰티를 위한 방문은 종종 꽉 스케쥴로 이루어지기 때문에 시술자는 20분 이내에 장비를 세척할 수 있는 신속한 사이클 오토클레이브를 높이 평가합니다. 깨지기 쉬운 복합 기구용으로 미리 설정된 파라미터를 터치스크린에 내장할 수 있는 벤더는 경쟁 우위를 획득하고 있습니다.

중앙 집중식 재처리 허브는 여러 기지가 있는 치과 의사에게 비용 절감을 약속하지만, 원내 장비 구입에서 자금을 빨아들여 유닛 출하를 억제합니다. 아웃소싱 모델은 물류 인프라와 규제 인증 경로가 성숙한 북미와 서유럽의 일부에서 번성하고 있습니다. 그러나 클리닉에서는 캐스트디 체인의 격차나 택배업체가 지연에 직면할 경우 기구를 사용할 수 없게 되는 시간이 길어질 우려가 있어 보급이 제한되어 있습니다. 제조업체는 멸균기의 판매 감소를 부분적으로 상쇄하기 위해 세척 소독기 및 포장 도구를 타사 공급자에게 공급하여 감수를 완화합니다. 중기적으로는 현장의 빠른 사이클과 아웃소싱의 벌크 로드를 혼합한 하이브리드 모델이 나타날 수 있습니다.

초음파 프리클리너에서 클래스 B 진공 오토클레이브에 이르기까지 모든 멸균 워크플로우를 지원하기 때문에 장비는 2024년 매출의 58.86%를 차지했습니다. 재사용가능한 핸드피스, 미러, 스케일러는 챔버 씰, 필터, 생물학적인디케이터의 교환 사이클을 예측 가능하게 하고, 기준선 수요를 안정시킵니다. 반대로 소모품 및 액세서리, 파우치, 랩 및 화학은 클리닉이 교차 오염의 우려를 억제하기 위해 일회용 장벽을 선호하기 때문에 CAGR 7.92%를 나타낼 전망입니다. 소모품의 치과 멸균 시장 규모는 향후 수년간 성장할 것으로 예측되며, 이는 단발적 자본 구매보다 지속적인 보충을 반영합니다. 제조업체는 멸균기 소프트웨어에 내장된 자동 재주문 포털을 통해 포장 용품을 교차 셀링하여 소모품 수익을 사이클 카운트에 직접 연결하여 마진 가시성을 향상시킵니다. 디지털 추적성 이니셔티브는 감사 로그에 제공되는 로트별 표시기 스트립을 사용하여 클리닉이 모든 로딩을 문서화해야 하므로 액세서리 캡처를 촉진합니다.

내열 트레이와 랙은 장비와 액세서리가 어떻게 융합되는지 보여줍니다. 새로운 플라즈마 모델은 비금속 트레이의 설계를 필요로 하고 코어 유닛의 매출을 보완하는 액세서리 수요 증가를 창출하고 있습니다. 랩 팩 카운트가 가능한 스마트 캐비닛은 하드웨어와 소모품을 통합 에코시스템으로 더욱 연동시킵니다. 체어사이드 CAD/CAM 솔루션을 채용한 클리닉은 밀링 바용으로 조정된 전용 초음파 유닛으로 업그레이드하여 다시 기기 중심 지출의 우위성을 강화하고 있습니다. 소모품 및 액세서리의 점유율은 41.14%에 불과하지만, CAGR이 빠르다는 것은 2030년까지 자본기구에 필적하는 조이익을 만들어 벤더의 수익 믹스와 애프터마켓 전략을 변화시키는 것을 의미합니다.

북미는 2024년 세계 매출의 38.16%를 차지하고 외과적 치과 치료에 환불을 하는 고급 보험 제도와 저속 핸드피스 멸균을 성문화하는 주 수준의 의무에 지지되었습니다. 미국에서는 DSO의 설비 투자가 잇따라 기업 데이터 대시보드와 연계하는 IoT 접속 오토클레이브에 조달이 진행되고 있습니다. 캐나다에서는 주에 의한 감염 관리 업데이트로 진공 건조 및 디지털 보고 기능을 갖춘 B급 유닛에 대한 수요가 증가했습니다. 포화 상태에도 불구하고, 많은 클리닉이 2016년부터 2018년 사이에 스팀 유닛을 설치했으며, 2025년부터 2026년까지 서비스 수명을 맞이하기 때문에 교체 주기가 북미 성장을 긍정적으로 유지하고 있습니다.

유럽은 환경 친화적인 기술의 채택을 가속화하는 높은 규제 결속력으로 이어집니다. 유럽의 치과 멸균 시장 규모는 산화에틸렌을 대체하는 과산화수소에 대한 독일과 프랑스의 관심 증가를 반영하여 향후 수년간 성장할 것으로 예측됩니다. 북유럽에서는 열회수형 오토클레이브에 유리한 에너지 소비량의 상한이 설정되어 있어 킬로와트 아워 정격에 의한 벤더의 차별화가 강화되고 있습니다. 남유럽 업자는 단편적이기 때문에 여전히 정비 장비를 선호하고 설치 기반의 현대화는 억제되었지만 2 차 시장에서의 리노베이션 기회는 확산되고 있습니다.

아시아태평양은 CAGR 8.39%로 다른 어느 지역보다도 뛰어나며, 2030년까지 2억 1,000만 달러 이상의 증수가 전망됩니다. 중국의 Healthy China 2030 계획은 기본적인 스팀 유닛이 필요한 현 수준의 치과 진료소에 투자하고 있지만 Tier-1 도시에서는 현재 심미 치과 거점을 위한 플라즈마 시스템을 주문하고 있습니다. 일본은 고령화 사회의 구강 수술에 초점을 맞추고 임플란트 키트를 관리하기 위해 대용량 클래스 B 멸균기로 업그레이드합니다. 인도와 동남아시아는 의료기기 수입 관세 면제의 혜택을 받는 관민 제휴 클리닉을 통해 도입을 가속화합니다. 중동 및 아프리카는 석유 수출국이 건강 관리로 다각화하고 치과 부문을 통합하는 다과목 센터에 자금을 공급하고 있기 때문에 한자리 중반의 성장을 보여줍니다. 브라질의 수입 규제가 정기적인 병목이지만, 민간 보험의 성장은 상파울루와 산티아고의 현대 클리닉 건설을 지원합니다. LATAM은 통화 변동이 여전히 가장 큰 역풍이며 임대 계약이 자본 구매보다 매력적입니다.

The Dental Sterilization Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 2.32 billion by 2030, at a CAGR of 6.81% during the forecast period (2025-2030).

Expansion is propelled by stricter infection-control regulations, widening adoption of digital workflows that raise instrument-turnaround expectations, and steady technology upgrades that align with environmental and staff-safety goals. North America holds 38.16% revenue share in 2024 thanks to well-established reimbursement systems and early uptake of smart autoclaves. Asia-Pacific, advancing at an 8.39% CAGR, is rapidly closing the sterilization-infrastructure gap on the back of aging populations and expanded dental-insurance coverage. Instruments remain the revenue cornerstone, yet rising reliance on single-use consumables and accessories is reshaping purchase patterns and elevating recurring-revenue streams. Hydrogen-peroxide plasma systems are moving from niche to mainstream because they process heat-sensitive devices without ethylene-oxide emissions. Competitive intensity is moderate and fluid; established vendors are pruning portfolios to concentrate on high-margin niches, while mid-tier innovators pursue cloud-connected sterilizers that sync with practice-management platforms.

An estimated 280 million older adults experienced oral disorders in 2024, and the burden is shifting sterilization patterns as clinicians handle complex, multi-visit cases that escalate instrument-turnaround cycles. The World Health Organization's oral-health strategy elevates infection-prevention obligations, prompting clinics to acquire higher-capacity sterilizers rather than extend cycle times. Emerging Asia-Pacific markets face a dual challenge of rising patient volumes and historically under-funded infection-control infrastructure, spurring fast equipment adoption despite capital constraints. The link between disease prevalence and sterilization demand is non-linear; high-complexity treatments often trigger multiple loads per appointment, stretching existing capacity. Manufacturers that supply modular or stackable autoclave formats are therefore positioned to capitalize on this demographic-driven uptick.

Elective aesthetic treatments such as veneers, aligners, and digital smile design rose sharply in 2024, and each procedure involves delicate burs, ceramic presses, and polymerizing tips that cannot tolerate repeated steam exposure. Clinics serving this segment gravitate toward hydrogen-peroxide plasma or ozone-based systems that operate below 60 °C while maintaining sterility assurance levels. Demand concentration remains highest in the United States and Western Europe, yet metropolitan centers in South Korea, Japan, and India now house fast-growing cosmetic practices that replicate Western sterilization standards. Because aesthetic visits often cluster into tightly scheduled sessions, practitioners value rapid-cycle autoclaves that clear instruments in under 20 minutes. Vendors able to embed pre-set parameters for fragile composite instruments on their touchscreens gain a competitive edge.

Centralized reprocessing hubs promise cost savings for multi-site dentists, but they siphon capital away from in-office equipment purchases, curbing unit shipments. Outsourced models thrive in North America and parts of Western Europe where logistics infrastructure and regulatory accreditation pathways are mature. However, clinics worry about chain-of-custody gaps and longer instrument unavailability when couriers face delays, limiting widespread take-up. Manufacturers mitigate lost revenue by supplying washer-disinfectors and packaging gear to third-party providers, thus partially offsetting lower sterilizer sales. Over the medium term, hybrid models that mix on-site rapid cycles with outsourced bulk loads could emerge.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Instruments commanded 58.86% of 2024 revenue as they underpin every sterilization workflow, from ultrasonic pre-cleaners to class B vacuum autoclaves. Reusable handpieces, mirrors, and scalers create predictable replacement cycles for chamber seals, filters, and biological indicators, steadying baseline demand. Conversely, consumables and accessories, pouches, wraps, and chemistries, are surging at 7.92% CAGR as clinics prioritize single-use barriers to curb cross-contamination fears. The dental sterilization market size for consumables is predicted to grow in the coming years, reflecting continuous replenishment rather than episodic capital buys. Manufacturers cross-sell packaging supplies through auto-reorder portals embedded in sterilizer software, linking consumables revenue directly to cycle counts and improving margin visibility. Digital traceability initiatives amplify accessory uptake because practices must document every load with lot-specific indicator strips that feed audit logs.

Heat-resistant trays and racks illustrate how instruments and accessories converge; new plasma models require non-metallic tray designs, creating incremental accessory demand that complements core-unit sales. Smart cabinets capable of counting wrapped packs further interlock hardware and consumables as integrated ecosystems. Clinics that adopt chairside CAD/CAM solutions upgrade to specialized ultrasonic units tuned for milling burs, again reinforcing the dominance of instrument-centric expenditure. Although consumables and accessories hold only 41.14% share, their faster CAGR means that by 2030 they will generate comparable gross profit to capital instruments, shifting vendor revenue mixes and aftermarket strategies.

The Dental Sterilization Market Report is Segmented by Product (Instruments, Consumables & Accessories), Sterilization Method (Heat/Steam, Hydrogen-Peroxide Plasma, Ethylene Oxide, and More), End User (Hospitals, Clinics, Dental Laboratories, Academic & Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.16% of global revenue in 2024, underpinned by sophisticated insurance systems that reimburse surgical dentistry and by state-level mandates that codify low-speed handpiece sterilization. The United States witnessed a wave of DSO capital investment, directing procurement toward IoT-connected autoclaves that align with enterprise data dashboards. Canada's provincial infection-control updates boosted demand for class B units with vacuum drying and digital reporting, albeit at a slower pace relative to the U.S., owing to fewer practice counts. Despite saturation, replacement cycles keep North American growth positive because many clinics installed steam units between 2016 and 2018 that approach end-of-life in 2025-2026.

Europe follows with high regulatory cohesion that accelerates eco-friendly technology adoption. The dental sterilization market size in Europe is expected to grow in the coming years, reflecting growing German and French interest in hydrogen-peroxide substitutes for ethylene-oxide. Nordic regions set energy-consumption caps that favor heat-recovery autoclaves, reinforcing vendor differentiation on kilowatt-hour ratings. Southern Europe's fragmented practitioner base still prefers refurbished equipment, tempering installed-base modernization but opening secondary-market refurbishment opportunities.

Asia-Pacific outruns every other region at an 8.39% CAGR, adding over USD 210 million in incremental revenue through 2030. China's Healthy China 2030 plan invests in county-level dental clinics that require basic steam units, but Tier-1 cities now order plasma systems for cosmetic dentistry hubs. Japan focuses on aging-society oral surgery, upgrading to larger-capacity class B sterilizers to manage implant kits. India and Southeast Asia accelerate adoption through public-private partnership clinics that benefit from import-duty exemptions on medical devices. The Middle East and Africa post mid-single-digit growth as oil-exporting economies diversify into healthcare, funding multispecialty centers with integrated dental wings. South America shows steady albeit uneven expansion; Brazilian import regulations create periodic bottlenecks, although private insurance growth supports modern clinic builds in Sao Paulo and Santiago. Currency volatility remains the chief headwind in LATAM, making leasing agreements attractive versus outright capital purchase.