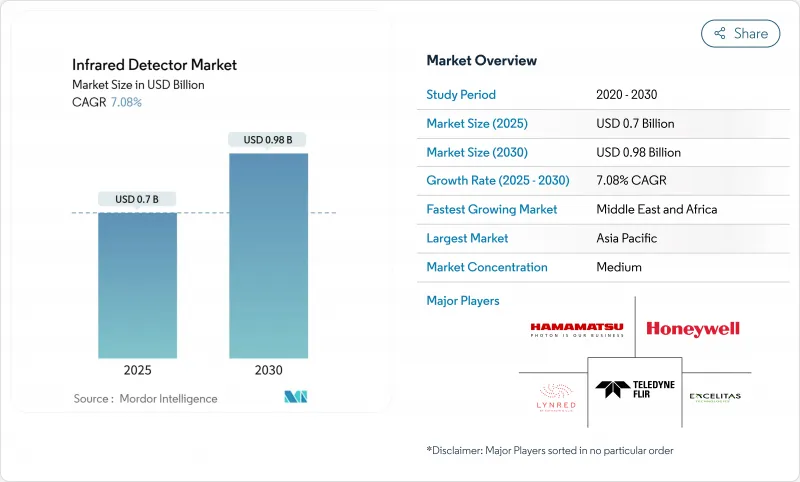

적외선 검출기 시장 규모는 현재 7억 달러로, 2030년에는 CAGR 7.08%를 나타내 9억 8,000만 달러에 이를 것으로 예상되고 있습니다.

소형화된 비냉각 마이크로 볼로미터 어레이, 자율주행차용 LiDAR 등급 근적외선 센서, 유럽연합에서의 예지보전 서모그래피의 의무화 등이 당면한 기세를 지원합니다. 그린 수소 공장에서의 적외선 가스 누출 감지 시스템의 보급, 동아시아의 반도체 검사 수요 증가, 방위성 주도의 고감도 냉각 어레이에 대한 의욕이 성장 궤도를 더욱 강화합니다. 갈륨과 게르마늄공급 제한에서 벗어나는 공급망 재편은 검출기 재료의 대체를 가속화하는 반면, 인수 주도의 통합은 밸류체인 각 층의 경쟁 전략을 형성하고 있습니다. 이러한 역학의 상호작용으로 적외선 검출기 시장은 지속적인 확대와 기술의 다양화가 예상되고 있습니다.

Aalto 대학의 게르마늄 기반 포토다이오드는 1.55μm으로 응답성을 35% 향상시켜, 서브밀리와트의 전력 엔벨로프를 유지하면서 열 드리프트에 대처하는 비용 효율적인 CMOS 호환 제조를 가능하게 했습니다. MEMS와 경량 신호 처리 로직의 융합은 스마트 빌딩의 엔드포인트에 지속적인 온도 모니터링을 추진하고, 아시아 부품 제조업체는 무선 연결을 번들로 하여 소비자용 전자기기의 포트폴리오 전체에서 부가가치 서비스를 수익화하고 있습니다.

2024년 EU 기계 규제에서는 위험 평가 프로토콜이 성문화되었고 서모그래피는 컴플라이언스 검증에 필수적입니다. 컨디션 기반 모니터링을 통해 에너지 집약형 플랜트는 시간당 10만 달러를 초과하는 다운타임을 줄이고, AI를 활용한 분석으로 이상 감지를 자동화하여 스킬 제약을 완화하고 투자 안건을 강화합니다.

ITAR 및 와세너 규정은 미국 원산 서브시스템을 포함한 카메라 수출의 60%를 제한하고 고정비를 상승시키는 이중 제품 라인을 강요합니다. 유럽 제조업체는 공급망의 현지화를 진행하고 있지만, 갈륨과 게르마늄을 둘러싼 지정학적 긴장이 타임라인 리스크를 증폭시키고 있습니다.

2024년 적외선 검출기 시장의 65%를 열 검출기가 차지했습니다. 그러나 빛 또는 양자 기반 장치는 방어 및 과학적 이용 사례가 더 높은 감도를 선호하기 때문에 CAGR 8.5%를 나타낼 전망입니다. 양자 검출기의 적외선 검출기 시장 규모는 유기 반도체 광 검출기가 픽셀 레벨 패터닝 없이 5.55X1012 존스의 비검출률을 입증하고 제조 오버헤드의 감소를 시사했기 때문에 확대가 예측됩니다.

열 검출기는 비냉각 작동과 초기 비용이 낮기 때문에 여전히 소비자 및 건물 자동화 용도의 주류를 차지하고 있습니다. 양자 어레이의 AI 지원 온칩 처리는 현재 군사 재고의 실시간 위협 분류를 제공합니다. KAIST의 실내 온도에서 적외선 광 검출기는 극저온 장벽을 제거하고 양자 아키텍처를 휴대용 및 배터리 구동 플랫폼에 배치했습니다.

비냉각 어레이는 설계자가 저전력 소비와 단순한 통합을 중시했기 때문에 2024년 매출의 78%를 차지했습니다. 그러나 냉각 아키텍처는 극단적인 비거리를 요구하는 방어 프로그램과 관련하여 CAGR 8.2%를 나타낼 전망입니다. Lynred의 ATI320은 비냉각 감도를 높이고 과거의 성능 경계를 모호하게 하려는 움직임을 명확하게 보여줍니다.

적외선 검출기 시장 전체의 60% 가까이를 차지하는 군사 분야에서는 대함선용이나 장거리 표적용 광학계에 냉각형이 채용되고 있습니다. 크기, 무게 및 전력 최적화로 스털링 냉각 패키지는 무인 항공기와 휴대용 런처에 적합합니다. 냉각 모듈과 비냉각 모듈을 결합한 하이브리드 페이로드가 부상하고 있으며, 부대 지휘관은 비용과 임무 프로파일의 균형을 맞출 수 있습니다.

중국의 EV 제조업체가 LiDAR의 전개를 확대해, 대만과 한국의 주조소가 SWIR 검사 라인을 증강했기 때문에 아시아태평양이 2024년의 지출액의 42%를 차지했습니다. 현지 LiDAR 기업의 특허 리더십은 지역 혁신의 깊이를 강조하고 최종 용도 클러스터에 대한 근접성은 공급망을 단축시킵니다. 일본의 성숙한 일렉트로닉스 섹터는 고급 패키징 서비스를 제공하고 인도의 국경 경비 투자는 고감도 냉각 수요를 밀어 올립니다.

북미는 왕성한 방어 예산과 독자적인 센서 IP를 활용하고 있으며, 텔레다인은 2024년 4분기에 15억 230만 달러의 매출을 기록해 지속적인 조달 사이클을 뒷받침했습니다. ITAR 조항은 국내 벤더를 보호하는 한편 수출을 복잡하게 하고 있으며, 해외 바이어의 지역 분산 전략을 촉구하고 있습니다. 캐나다와 멕시코는 열화상 카메라가 운영의 회복력을 높이는 자동차 산업과 채굴 산업을 지원합니다.

유럽은 써모그래피를 컴플라이언스 감사에 통합하는 기계 안전 규정 및 환경 지침 하에서 꾸준히 성장하고 있습니다. Lynred의 8,500만 유로(9,100만 달러)의 시설 확장은 공급 라인의 위험을 줄이기 위한 생산 능력의 현지화를 입증합니다. 북유럽 국가에서는 스마트 빌딩의 도입이 진행되고 있으며, 중동 및 아프리카에서는 그린 수소 메가 프로젝트와 보안 인프라 업그레이드를 배경으로 CAGR이 8.9%를 나타낼 것으로 예측되고 있습니다.

The infrared detector market size is currently valued at USD 0.70 billion and is projected to reach USD 0.98 billion by 2030, advancing at a 7.08% CAGR.

Miniaturized uncooled microbolometer arrays, LiDAR-grade near-infrared sensors for autonomous vehicles, and mandatory predictive-maintenance thermography in the European Union underpin near-term momentum. Wider deployment of infrared gas-leak detection systems in green-hydrogen plants, expanding semiconductor inspection demand in East Asia, and defense-driven appetite for higher-sensitivity cooled arrays further reinforce the growth trajectory. Supply-chain realignment away from restricted gallium and germanium sources is accelerating substitutions in detector materials while acquisition-led consolidation is shaping competitive strategies across value-chain tiers. The interplay of these dynamics positions the infrared detector market for sustained expansion and technology diversification.

Aalto University's germanium-based photodiodes raised responsivity by 35% at 1.55 μm, enabling cost-effective CMOS-compatible fabrication that tackles thermal drift while sustaining sub-milliwatt power envelopes.MEMS convergence with lightweight signal-processing logic is pushing continuous thermal monitoring into smart-building endpoints, and Asian component makers are bundling wireless connectivity to monetise value-added services across consumer electronics portfolios.

The 2024 EU machinery regulation codifies risk-assessment protocols that make thermal imaging integral to compliance validation. Condition-based monitoring reduces downtime that can exceed USD 100,000 per hour in energy-intensive plants, and AI-enabled analytics now automate anomaly detection, easing skills constraints and strengthening investment cases.

ITAR and Wassenaar regimes constrain 60% of camera exports that contain US-origin subsystems, forcing dual product lines that elevate fixed costs. European manufacturers are localising supply chains, yet geopolitical tensions around gallium and germanium amplify timeline risks.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, thermal detectors captured 65% of the infrared detector market. Photo- or quantum-based devices are, however, expanding at an 8.5% CAGR as defense and scientific use cases favor higher sensitivity. The infrared detector market size for quantum detectors is forecast to widen as organic semiconductor photodetectors demonstrated specific detectivity of 5.55X1012 Jones without pixel-level patterning, signaling lower fabrication overheads.

Thermal detectors still dominate consumer and building-automation applications due to uncooled operation and lower upfront costs. AI-enabled on-chip processing inside quantum arrays is now providing real-time threat classification for military inventories, a shift likely to recalibrate procurement strategies. KAIST's room-temperature mid-infrared photodetector removes cryogenic barriers, positioning quantum architectures for handheld and battery-operated platforms.

Uncooled arrays delivered 78% of 2024 revenue as designers prized low power and simple integration. Yet cooled architectures are advancing at 8.2% CAGR tied to defense programs that demand extreme range. Lynred's ATI320 underscores the push to elevate uncooled sensitivity, blurring historical performance lines.

The military segment, nearly 60% of the total infrared detector market size, still specifies cooled formats for anti-ship and long-range targeting optics. Size, weight, and power optimisation is making Stirling-cooler packages suitable for drones and portable launchers. Hybrid payloads that combine cooled and uncooled modules are emerging, allowing unit commanders to balance cost and mission profiles.

The Infrared Detector Market is Segmented by Detector Type (Thermal Detector, Photo Detector), Cooling Technology (Uncooled, Cooled), Material (Microbolometer, Ingaas, and More), Spectral Range (NIR, SWIR, and More), Application (Motion Sensing, Thermography, Process Monitoring, and More), End-Use Industry (Aerospace and Defense, Industrial, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 42% of 2024 spending as Chinese EV makers scaled LiDAR rollouts and foundries in Taiwan and South Korea ramped SWIR inspection lines. Patent leadership by local LiDAR firms emphasises regional innovation depth, and proximity to end-use clusters shortens supply chains. Japan's mature electronics sector supplies advanced packaging services, and India's border-security investments boost high-sensitivity cooled demand.

North America leverages strong defense budgets and proprietary sensor IP, with Teledyne recording USD 1,502.3 million Q4 2024 sales that underline sustained procurement cycles. ITAR provisions shield domestic vendors yet complicate exports, prompting regional diversification strategies among international buyers. Canada and Mexico support the automotive and extractive verticals where thermal cameras enhance operational resilience.

Europe grows steadily under machinery-safety regulations and environmental directives that embed thermography into compliance audits. Lynred's EUR 85 million (USD 91 million) facility expansion evidences capacity localisation aimed at de-risking supply lines. Nordic nations champion smart-building deployments, while the Middle East and Africa forecast 8.9% CAGR on the back of green-hydrogen megaprojects and security infrastructure upgrades that specify long-range imagers.