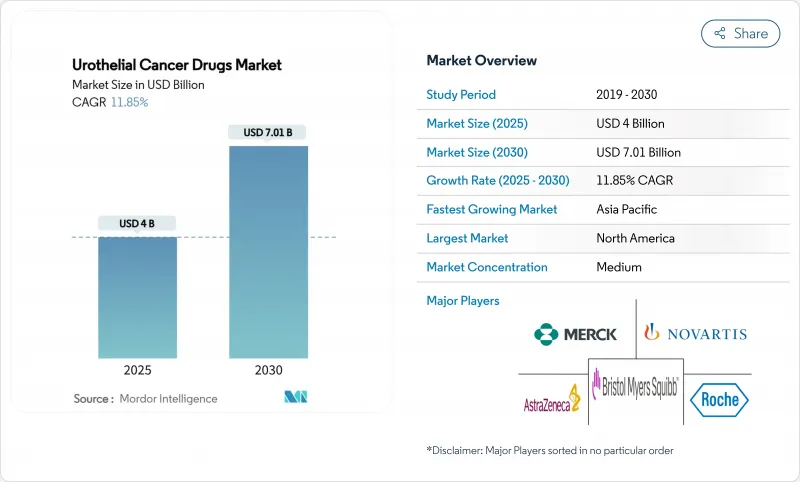

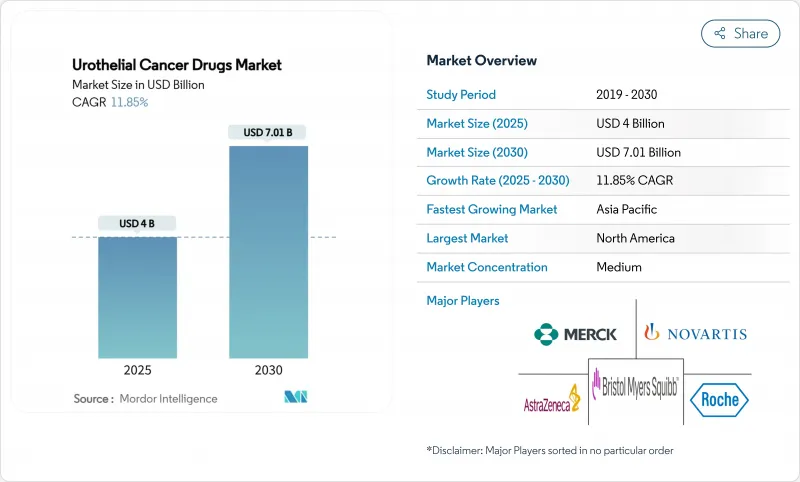

요로상피암 치료제 시장 규모는 2025년 40억 달러, 2030년 70억 1,000만 달러에 이를 것으로 예상되며, 기간 중 CAGR은 11.85%를 나타내 혁신적인 치료에 대한 왕성한 수요를 뒷받침하고 있습니다.

질병 이환율 증가, 면역종양 치료제의 급속한 보급, 항체 약물 복합체(ADC)의 규제 당국에 의한 신속한 승인이 동조하여 성장을 가속하는 한편, 정밀의료에의 지속적인 투자에 의해 표적 치료의 대상이 되는 환자층이 확대되고 있습니다. ADC와 체크포인트 억제제를 결합한 병용 요법은 바이오마커로 유도된 프로토콜이 치료 정밀도를 향상시키고 생존 기간을 연장시키는 한편, 퍼스트라인 기준을 재정의하고 있습니다. 북미는 조기 기술 도입과 까다로운 상환으로 우위를 유지하고 있지만, 아시아태평양은 정력적인 스크리닝 노력과 종양학 인프라 확대로 지역별로 가장 빠른 속도로 성장을 이루고 있습니다. 바실 카르멧 게린(BCG)의 지속적인 부족은 차세대 방광내 약물과 유전자 치료의 기회를 증가시키지만 동시에 이해관계자들이 다루어야 하는 공급망 취약점을 드러냅니다.

세계의 방광암 환자수는 증가의 일도를 따르고 있으며, 고소득국가에서는 악성종양의 톱 6에 랭크 인하고, 신흥국에서는 그 기세가 가속하고 있습니다. 환경 발암 물질, 인구 동태의 고령화, 방광경 스크리닝의 보급에 의해 신규 치료제의 후보가 되는 환자층이 확대되고 있습니다. 아시아태평양의 젊은 환자 집단은 종종 장기간의 병용 치료 요법을 필요로 하는 공격적인 질병 표현형을 보입니다. 상부 요로상피암은 별개의 임상적 질환인 것으로 인식되고, 개별화된 접근을 필요로 하는 새로운 치료 영역이 태어나고 있습니다. 의료 시스템을 통한 비뇨기 종양 전문센터에 대한 투자는 진단에서 치료까지의 간격을 단축하고 시장 총 수요를 확대합니다. 순 효과는 대상 환자의 지속적인 증가이며 이해 관계자에게 수익 가능성을 직접 확대합니다.

펨브롤리주맙과 듀발바맙과 같은 체크포인트 억제제는 2024년에 여러 병기에서 광범위한 제1선택제의 승인을 받았으며 대상 환자 집단에서 시스플라틴 기반 화학요법을 대체했습니다. 듀발바맙의 NIAGARA 시험에서는 전체 생존 기간의 연장이 확인되었고, 가이드라인 개정과 지불자 수락의 계기가 되었습니다. 병용 프로토콜, 특히 엔포르맙 베도틴과 펨브롤리주맙의 병용은 모범 사례를 재정의하고 수익원을 강화하고 있습니다. PD-L1 발현과 종양의 돌연변이 부하를 이용한 바이오마커 알고리즘의 진화는 환자 선택을 정교하게 하고 연주효율을 높입니다. 피하 투여 제형은 물류상의 편의성을 제공하며 지역사회에 대한 보급을 지원합니다. 이러한 요인이 함께 요로상피암 치료제 시장은 호조 궤도를 추적하고 있습니다.

병용 요법의 연간 치료 비용은 신흥 경제 국가에서 환자 1인당 20만 달러를 초과하여 지불자 예산을 압박하며 엄격한 사전 승인 장애물을 부과합니다. 고도로 전문화된 주입 인프라와 집중적인 모니터링은 간접적인 비용을 증가시키고, 한편 보험 적용 범위가 제한되어 신흥 지역에서의 섭취를 제약하고 있습니다. 의약품 지원 프로그램은 선택적인 구제를 가져오지만 광범위한 접근에는 아직 충분하지 않습니다. 가치 기반 계약은 실제 임상 결과를 상환 조건으로 만들고 제조업체가 약제 경제적 이점을 문서화하도록 강제합니다. 바이오시밀러와의 경쟁은 초기 체크포인트 억제제의 가격 설정을 완화시킬 수 있지만, 복잡한 ADC의 제조는 가까운 미래에 제네릭 의약품의 진입을 억제하고 가용성의 압력을 지속시킵니다.

ADC는 가장 빠른 수익 상승을 보였으며 2025년부터 2030년까지 연평균 복합 성장률(CAGR)은 18.65%를 나타낼 것으로 예측됩니다. 이는 Enfortumab bedotin의 EV-302 데이터가 치료되지 않은 전이성 질환에서 생존 벤치마크를 재설정했기 때문입니다. 2024년 요로상피암 시장은 면역요법이 45.51%의 점유율을 차지했지만, 단제로의 연주효율이 두드러지기 때문에 ADC 페이로드를 통합한 병용요법이 상승적인 살종양 효과를 가져올 것으로 기대됩니다. 백금 제형 기반 화학요법은 시스플라틴에 적합한 환자와의 연관성을 유지하며, 유전자 요법과 화학 온열 요법은 BCG 부족이 지속되는 동안 방광의 틈새를 채웁니다.

파이프라인의 너비는 ADC의 기세가 지속되는 것을 보장합니다. 다음 웨이브 컨쥬게이트는 새로운 항원, 최적화된 링커 및 약물 항체 비율의 향상을 추구합니다. 이러한 기술 혁신은 세계적인 규제당국의 지원과 함께 요로상피암 치료제의 ADC 시장 규모를 과거의 상식을 훨씬 넘는 수준으로 끌어올릴 것으로 예측됩니다. 약국과 지불자는 점점 복잡해지는 요법이 일상화됨에 따라 재고, 상환 및 투여 프로토콜을 적응시켜야 합니다.

첫 치료 요법은 2024년 매출의 56.53%를 차지하며 첫 치료 선택의 경제적 중요성을 강조했습니다. 아베맙으로 대표되는 유지요법은 12.85%의 연평균 복합 성장률(CAGR)을 나타내 기세를 유지하고 있습니다. 그것의 내구성의 이점은 무증상 가치를 추구하는 임상의와 지불자 모두에게 공명합니다.

2차 치료 영역은 내성이 나타나는 매우 중요한 영역이며, ADC와 표적 억제제가 전통적인 화학요법에 대한 우월성을 나타낼 것입니다. 써드라인과 살베지 요법은 그 양이 적은 것, 온콜로틱 바이러스와 같은 파괴적인 치료법을 끌어들여, 쉐어를 확대할 가능성이 있습니다. 라인간 약제의 전략적 순서화는 진화하는 실세계 데이터에 근거한 예술이 되고 있으며, 요로상피암 치료제 시장에 있어서 보다 긴 컨트롤의 수평이 약속되고 있습니다.

북미는 견고한 상환, 치밀한 임상시험 인프라, 획기적 신약의 조기 채용으로 2024년 세계 매출의 43.15%를 유지했습니다. 미국 시장의 진화는 메디케어의 정책 갱신과 민간지급기관의 조정과 밀접하게 연관되어 있으며, 양자는 현재 생존기간의 연장을 실증할 수 있는 보상을 주는 가치 기반 계약을 채택하고 있습니다. 캐나다의 각 주가 출자하는 시스템은 협상을 통한 가격 설정이지만 예측 가능한 섭취를 촉진하기 위해 일괄 조달을 협상하고 있습니다. 멕시코와의 국경을 넘는 치료 흐름은 특히 종양 센터가 전문적인 주입 기능을 제공하는 국경주에서 환자 접근을 보완합니다.

유럽에서는 유럽의약청(EEA)이 승인을 조정하고 각국의 의료기술평가(HTA)가 접근을 판정하는 성숙하지만 이로정연한 환경이 있습니다. 독일의 DRG 지불 개혁, 영국의 암 치료제 기금, 프랑스의 ATU 조기 액세스 제도는 리스트 가격의 협상은 엄격한 것, 매력적인 약의 진입을 촉진하는 것입니다. 남유럽은 재정적 제약에 직면하고 있으며 채용은 지연되지만 수요는 사라지지 않습니다. 매니지드 엔트리 계약과 결과 기반 리베이트는 예산의 여유를 점점 더 늘리고 있습니다. 새로운 약물 전략 하에서 공동 임상 평가에 관한 EU 전역에서의 협력은 증거 요건의 합리화를 약속하고 요로상피암 치료제 시장에 이익을 가져다줍니다.

아시아태평양은 CAGR 12.35%를 기록하며 가장 활기찬 프론티어로 부상하고 있습니다. 중국의 수량 기준 조달은 기술 혁신을 방해하지 않고 가격을 억제하는 것을 목표로 하는 반면 일본의 HTA 프로세스는 종양학의 획기적인 가속화를 가속화하고 있습니다. 인도의 점진적인 관민 시스템은 환자 지원 파트너십을 통해 경구 표적 약물을 수용합니다. 호주와 한국은 가치있는 의약품을 신속하게 상환하기 위해 강력한 등록과 실제 임상 데이터를 활용합니다. 그러나 농촌과 도시의 격차, 제한된 바이오마커 검사, 전문의의 편재 등이 지역 전체에 걸쳐 균일한 도입에 대한 역풍이 되고 있습니다.

The urothelial cancer drugs market size stood at USD 4.00 billion in 2025 and is forecast to reach USD 7.01 billion by 2030, expanding at an 11.85% CAGR during the period, underscoring vigorous demand for innovative therapies.

Escalating disease incidence, rapid uptake of immuno-oncology agents, and regulatory fast-tracking of antibody-drug conjugates (ADCs) are synchronizing to propel growth, while sustained investment in precision medicine is widening the patient base eligible for targeted treatment. Combination regimens that marry ADCs with checkpoint inhibitors are redefining first-line standards, even as biomarker-guided protocols improve therapeutic accuracy and extend survival outcomes. North America retains primacy through early technology adoption and generous reimbursement, whereas Asia-Pacific's vigorous screening initiatives and expanding oncology infrastructure drive the fastest regional gains. Persistent bacille Calmette-Guerin (BCG) shortages amplify opportunities for next-generation intravesical agents and gene therapies, yet simultaneously reveal supply-chain vulnerabilities that stakeholders must address.

Global bladder cancer diagnoses continue to climb, ranking among the top six malignancies in high-income nations and accelerating in emerging economies. Environmental carcinogens, aging demographics, and wider access to cystoscopic screening enlarge the addressable pool of candidates for novel therapeutics. Younger patient cohorts in Asia-Pacific increasingly present with aggressive disease phenotypes that demand prolonged, combination treatment regimens. Recognition of upper-tract urothelial carcinomas as a distinct clinical entity is spawning new therapeutic segments requiring tailored approaches. Health-system investment in dedicated uro-oncology centers streamlines diagnosis-to-treatment intervals and enlarges total market demand. The net effect is a durable rise in eligible patients, directly expanding revenue potential for stakeholders.

Checkpoint inhibitors such as pembrolizumab and durvalumab secured broad first-line approvals across multiple disease stages in 2024, displacing cisplatin-based chemotherapy for eligible populations. Durvalumab's NIAGARA study confirmed overall survival gains, catalyzing guideline revisions and payer acceptance. Combination protocols-most prominently enfortumab vedotin plus pembrolizumab-are redefining best practice and intensifying revenue streams. Evolving biomarker algorithms exploiting PD-L1 expression and tumor mutational burden refine patient selection, thus elevating response rates. Subcutaneous formulations offer logistical convenience, supporting diffusion into community settings. Collectively these factors fortify the urothelial cancer drugs market's trajectory.

Annual treatment outlays for combination regimens exceed USD 200,000 per patient in developed economies, straining payer budgets and imposing strict prior-authorization hurdles. Highly specialized infusion infrastructure and intensive monitoring inflate indirect costs, while limited insurance coverage constrains uptake in emerging regions. Pharmaceutical assistance programs generate selective relief yet remain insufficient for widespread access. Value-based contracts are gaining traction, conditioning reimbursement on real-world outcomes and compelling manufacturers to document pharmacoeconomic merit. Biosimilar competition may temper pricing for early checkpoint inhibitors, but complex ADC manufacturing dampens near-term generic entry, sustaining affordability pressures.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

ADCs produced the fastest revenue climb, forecasting an 18.65% CAGR between 2025 and 2030 as enfortumab vedotin's EV-302 data reset survival benchmarks in untreated metastatic disease. Immunotherapy dominated 2024 with a 45.51% slice of the urothelial cancer drugs market, yet plateauing single-agent response rates motivate combination approaches that integrate ADC payloads for synergistic tumor kill. Platinum-based chemotherapy retains relevance for cisplatin-eligible patients, whereas gene therapy and chemohyperthermia fill intravesical niches amid persistent BCG scarcity.

Pipeline breadth ensures continued ADC momentum: next-wave conjugates seek novel antigens, optimized linkers, and enhanced drug-antibody ratios. These innovations, coupled with global regulatory support, are expected to lift the urothelial cancer drugs market size for ADCs well beyond historical norms. Pharmacies and payers will need to adapt inventory, reimbursement, and administration protocols as increasingly complex regimens become routine.

First-line regimens generated 56.53% of 2024 revenues, underscoring the economic significance of initial therapeutic choice. Maintenance therapy, paced by avelumab, owns momentum through a 12.85% CAGR outlook; its durability benefits resonate with both clinicians and payers seeking progression-free value.

Second-line spaces remain pivotal arenas where resistance emerges, inviting ADCs and targeted inhibitors to demonstrate superiority over traditional chemotherapies. Third-line and salvage settings, although smaller in volume, attract disruptive modalities such as oncolytic viruses that could unlock incremental share. The strategic sequencing of agents across lines is becoming an art informed by evolving real-world data, promising longer control horizons for the urothelial cancer drugs market.

The Urothelial Cancer Drugs Market Report is Segmented by Treatment Class (Chemotherapy, Immunotherapy, and More), Line of Therapy (First-Line, Second-Line, and More), Cancer Stage (Metastatic Urothelial Carcinoma, and More), Biomarker Status (FGFR2/3 Altered, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America maintained 43.15% of 2024 global revenue due to robust reimbursement, dense clinical-trial infrastructure, and early adoption of breakthrough designations. U.S. market evolution is closely tied to Medicare policy updates and private payer alignment, both of which now embrace value-based contracts that reward demonstrable survival gains. Canada's provincially funded systems negotiate collective procurement, fostering predictable uptake albeit at negotiated pricing. Cross-border treatment flows with Mexico supplement patient access, particularly in border states where oncology centers provide specialized infusion capability.

Europe presents a mature but methodical environment in which the European Medicines Agency coordinates approvals and national health-technology assessments (HTAs) adjudicate access. Germany's DRG payment reforms, the U.K.'s Cancer Drugs Fund, and France's ATU early-access scheme collectively accelerate entry for compelling agents, though list-price negotiations are stringent. Southern Europe faces fiscal constraints, delaying adoption but not eliminating demand; managed-entry agreements and outcomes-based rebates increasingly unlock budgetary headroom. Pan-EU collaboration on joint clinical assessment under the new Pharmaceutical Strategy promises to streamline evidence requirements, benefiting the urothelial cancer drugs market.

Asia-Pacific, registering a 12.35% CAGR, emerges as the most vibrant frontier, powered by national cancer control plans, insurance expansion, and improving diagnostic reach. China's volume-based procurement aims to tame prices without impeding innovation, while Japan's HTA process accelerates for oncology breakthroughs. India's tiered private-public system is embracing oral targeted agents through patient-assistance partnerships. Australia and South Korea leverage robust registries and real-world data to fast-track reimbursement for high-value medicines. Nonetheless, rural-urban disparities, limited biomarker testing, and uneven specialist density remain headwinds to uniform uptake across the region.