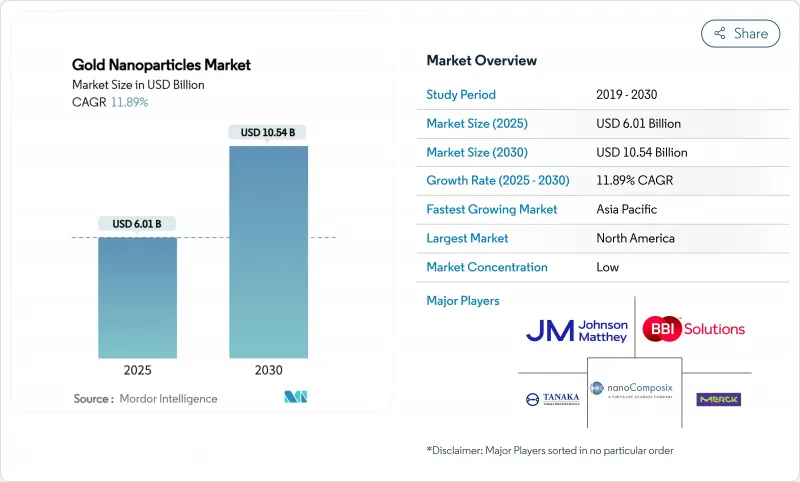

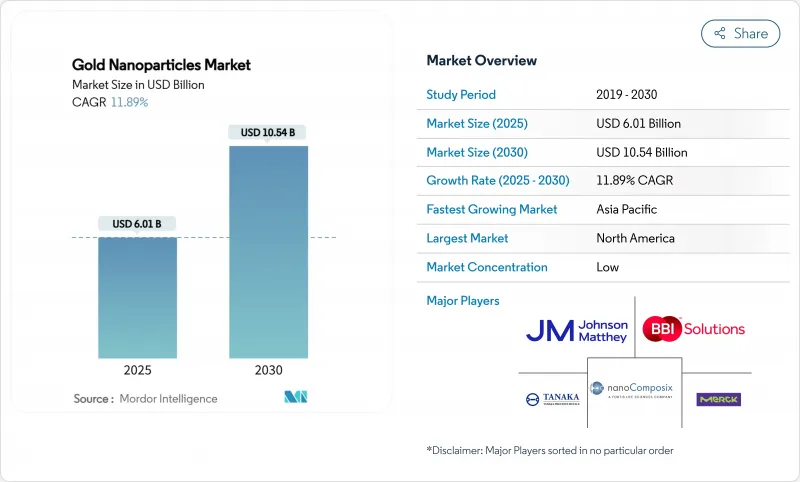

금 나노입자 시장 규모는 2025년에 60억 1,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 11.89%로, 2030년에는 105억 4,000만 달러에 달할 것으로 예상됩니다.

정밀의료 프로그램 증가, 일렉트로닉스의 소형화의 지속, 연속 플로우 그린 합성의 진보가, 헬스 케어, 반도체, 에너지, 환경 등의 이용 사례에 있어서의 고순도 나노입자 수요를 총체적으로 밀어 올리고 있습니다. 표적 약물전달 플랫폼은 이미 현재 매출의 26.11%를 차지하고 있으며, 규제 당국이 더 많은 theranostic 시험을 승인함에 따라 계속 투자를 하고 있습니다. 연속 흐름 합성 라인과 마이크로플루이딕스 합성 라인은 급속히 규모를 확대하고 있으며, 배치 변동 및 유해 폐기물의 양을 줄이면서 생산자의 운영 비용을 절감하고 있습니다. 수요 측면에서 건강 관리는 최대 성장을 보여주지만, 유연한 센서와 프린티드 센서가 실험실에서 대량 생산으로 전환함에 따라 전자 분야가 가장 높은 성장 속도를 보이고 있습니다. 금 가격 변동은 여전히 경영 위험이지만 단위당 귀금속 부하를 줄이는 코팅 및 재활용 노력은 당분간 마진 변동을 완화시킵니다.

병원, 위탁 연구 기관 및 장치 제조업체는 수동 약물 운반체를 넘어 단일 금 코어로 이미징과 치료를 결합한 다기능 세라노시스 구조로 이동하여 임상가는 광열 가열로 종양을 파괴하는 동시에 실시간으로 치료를 추적 할 수 있습니다. DNA 바코드화된 나노입자 라이브러리를 통해 종양의사는 한 환자 샘플에서 여러 페이로드 조합을 스크리닝할 수 있어 전임상시험 기간을 단축하고 치료하기 어려운 악성 종양의 연주 효율을 높일 수 있습니다. 규제당국은 명확한 생체적합성을 나타내는 나노의약품의 심사경로를 앞당겨 미국의 3가지 임상 프로그램이 2025년 중에 2단계로 이행하도록 지원하고 있습니다. 조사팀은 또한 동일한 플라즈몬 가열 원리를 저침습 뇌 자극에 응용할 수 있는 신경계면 코팅 연구도 진행하고 있습니다. 데이터 세트가 장기적인 안전 프로파일을 검증함에 따라, 병원 구매 그룹은 표준 이미지 처리 콘솔과 통합된 나노입자 유도 소작 시스템에 예산을 기록하게 되었습니다. 이러한 전환은 10년대 중반까지 금 나노입자 시장의 CAGR에 총 3.2% 포인트를 추가합니다.

스마트 워치, 전자 텍스타일, 이식형 센서의 제조업체는 초박형 회로에 금 나노와이어를 삽입해 전도성을 높이는 한편, 굽힘 반경을 1mm 이하로 억제하고 있습니다. 포토닉스의 연구에 따르면, 유기 태양전지의 광흡수체에 10nm의 구체를 내장하면, 국재화된 표면 플라즈몬 증폭에 의해 전력 변환 효율을 30% 이상 높일 수 있습니다. RFID 개발자는 금 시드를 활용하여 기가헤르츠 주파수에서 안테나 이득을 높이고 태그 크기를 늘리지 않고도 판독 범위를 넓힐 수 있습니다. 120℃ 이하의 온도에서 소결하는 잉크젯 인쇄 가능한 나노입자 잉크는 웨어러블에 사용되는 PET 및 TPU 필름과 호환되므로 생산 준비성이 높습니다. 일본, 한국, 대만 공장에서는 이미 상업 출하를 시작했으며 전 세계 노트북, 스마트폰, IoT 모듈 분야에 공급하고 있습니다.

지정학적 충격 속에서 투자자가 도피처를 찾아 나노입자 제조업체의 원재료비를 다년간 고가로 밀어 올렸기 때문에 2025년 상반기의 벤치마크 금 가격은 약 25% 상승했습니다. 상장투자신탁은 같은 기간에 160톤 이상을 추가하여 산업채널에서 공급을 빨아들였습니다. 많은 장치 OEM은 분기별로 계약을 맺고 있지만, 스팟 가격 상승은 몇 주 이내에 특수 잉크 및 시약 카탈로그에 반영되어 진단 및 프린티드 전자 제품의 틈새 분야에서 프로젝트 시작을 늦추고 있습니다. 헤지는 부분적인 구제책이 되지만, 운전자금의 필요성을 높이고, 규모가 작은 기업을 압박합니다. 칩당 금속 함유량을 30% 삭감할 수 있는 보호막이 타격을 완화하고 있지만, 두꺼운 생체 적합성 쉘을 요구하는 의료 분야에서는 채용이 치우쳐지고 있습니다. 이 억제는 현재 가격이 안정되거나 재활용 수율이 개선될 때까지 당분간의 CAGR을 2.3포인트 낮춥니다.

화학 환원은 2024년 금 나노입자 시장 규모의 40.55%를 차지했으며 북미와 유럽에서 확립된 배치 인프라에 뿌리를 둔 레거시 포지션입니다. 그러나 다운스트림 유저는 현재 보다 엄격한 입도 분포와 보다 낮은 용매 실적를 요구하고 있으며, 2030년까지의 CAGR이 12.45%를 나타내 견조한 연속 플로라인에 조달 결정을 기울이고 있습니다. 플랜트의 오퍼레이터는 전구체의 흐름을 전단하여 미크론 두께의 필름으로 하는 와류 유체 모듈을 개장하여 균일한 핵형성을 촉진하는 동시에 부산물인 수소를 현장에서 보일러 연료로서 회수합니다. AI가이드 센서는 체류시간 루프를 실시간으로 조정하여 다분산성 지수를 0.08 미만으로 억제하여 제약회사 고객의 로트간 재현성을 높이고 있습니다.

또한 플로우 리액터는 수성 매체와 상압을 사용하므로 시트레이트의 배치 공정에 비해 에너지 강도를 1/3 가까이 줄일 수 있습니다. 동일한 스키드에 적층된 시드-매개 성장 체계는 시스템을 열지 않고도 막대, 프리즘 및 코어 쉘 구성을 생산할 수 있어 오염 위험을 최소화할 수 있습니다. 고해상도 바이오센서 개발자는 플로우 스위치 프로그래밍에 의해 생성된 맞춤형 형상을 통합하는 것이 증가하고 있으며, 범용 콜로이드를 훨씬 웃도는 마진 프리미엄을 획득하고 있습니다. 분석가들은 검증 배치가 확장됨에 따라 2028년까지 연속 흐름의 생산 능력 점유율이 30%를 넘어 규제 대상의 치료·진단 최종 용도의 새로운 기준 표준으로서의 지위가 확고해질 것으로 예상하고 있습니다.

북미는 2024년 세계 매출의 36.33%를 차지하며 연구개발 예산의 윤택함, 품질을 표준화하는 FDA의 감독, 학술연구소와 위탁제조업체의 교량을 하는 통합 공급망에 지지되었습니다. 보스턴과 샌디에고의 산학 컨소시엄은 종양학, 심장 병학, 신경학에 응용을 목적으로 나노입자 IP의 라이선스를 제공하는 신흥 기업의 스핀 오프를 지원합니다. 2025년 미국 국립보건연구소를 통해 제공되는 자극 보조금은 국내 조종사 능력을 더욱 확대하고 임상 등급 재료의 리드 타임을 단축합니다.

아시아태평양의 CAGR은 12.98%로 가장 빠르며 중국의 대규모 콜로이드 반응기, 인도 제네릭 의약품 부문 확대, 일본의 센서 혁신 생태계를 반영하고 있습니다. 광동성과 절강성의 정책 인센티브는 ISO 14001 벤치마크를 충족하는 연속 흐름 라인에 대해 자본 지출의 최대 20%를 환불하여 녹색 생산 실적를 신속하게 추진합니다. 서울과 신죽에 본사를 둔 반도체 기업은 고밀도 인터포저와 열 인터페이스 패드용으로 나노입자를 대량으로 소비하고 있으며, 아세안의 전자기기 수출기업은 물류 트래커와 스마트 패키지 라벨에 인쇄 안테나를 사용하고 있습니다.

유럽은 규제의 엄격함과 지속가능성 리더십의 균형을 유지하면서 그린케미스트리 업그레이드와 순환형 경제의 파일럿 시험을 우선하는 호라이즌 유럽 보조금을 통해 시장 개척을 지원하고 있습니다. 독일 자동차 공급업체는 차세대 연료전지 차량용으로 설계된 금 촉매 NOx 환원 모듈을 검증하고 있습니다. 한편, 북유럽의 의료기술 클러스터는 POC(Point-of-Care)를 목적으로 한 신속 패혈증 검사에 나노입자 태그를 통합하여 EU의 '암 박멸 계획' 하에서 공중위생의 우선 과제에 임하고 있습니다.

The Gold Nanoparticles Market size is estimated at USD 6.01 billion in 2025, and is expected to reach USD 10.54 billion by 2030, at a CAGR of 11.89% during the forecast period (2025-2030).

Escalating precision-medicine programs, persistent electronics miniaturization, and progress in continuous-flow green synthesis collectively lift demand for high-purity nanoparticles across healthcare, semiconductor, energy, and environmental use cases. Targeted drug-delivery platforms already account for 26.11% of current revenue and continue to attract investment as regulators approve more theranostic trials. Continuous-flow and microfluidic synthesis lines are scaling rapidly, lowering batch variability and hazardous-waste volumes while cutting operating expenses for producers. On the demand side, healthcare commands the largest uptake, yet the electronics segment registers the highest growth velocity as flexible and printed sensors migrate from lab to mass production. Gold-price volatility remains an operational risk, but coatings that reduce precious-metal loading per unit and recycling initiatives buffer near-term margin swings.

Hospitals, contract research organizations, and device makers are moving beyond passive drug carriers to multifunction theranostic constructs that combine imaging and therapy on a single gold core, enabling clinicians to destroy tumors via photothermal heating while concurrently tracking treatment in real time. DNA-barcoded nanoparticle libraries now let oncologists screen several payload combinations inside one patient sample, cutting preclinical timelines and raising response rates for hard-to-treat malignancies. Regulatory agencies have accelerated review pathways for nanomedicines that demonstrate clear biocompatibility, helping three US clinical programs move into Phase II during 2025. Research teams are also probing neural-interface coatings that could translate the same plasmonic heating principle to minimally invasive brain stimulation. As datasets validate long-term safety profiles, hospital purchasing groups are earmarking budget for nanoparticle-guided ablation systems that integrate with standard imaging consoles. These transitions collectively add 3.2 percentage points to the gold nanoparticles market CAGR through mid-decade.

Smart-watch, e-textile, and implantable sensor makers insert gold nanowires into ultrathin circuitry to raise conductivity while keeping bending radii below 1 mm, a key threshold for comfortable skin-mounted patches. Photonics research shows that embedding 10 nm spheres inside organic solar-cell photo-absorbers can lift power-conversion efficiency by more than 30% through localized surface-plasmon amplification RFID developers leverage gold seeds to boost antenna gain at gigahertz frequencies, widening read ranges without increasing tag size. Production readiness is high thanks to inkjet-printable nanoparticle inks that sinter at temperatures below 120 °C, compatible with PET and TPU films used in wearables. The electronics driver injects 2.8 points into forecast CAGR, with commercial shipments already ramping at factories in Japan, South Korea, and Taiwan that supply the global notebook, smartphone, and IoT modules sectors.

Benchmark bullion prices climbed almost 25% during the first half of 2025 as investors sought havens amid geopolitical shocks, pushing nanoparticle producers' raw-material spend to multi-year highs. Exchange-traded funds added more than 160 tonnes during the same window, siphoning supply from industrial channels. Many device OEMs lock quarterly contracts, yet spot spikes feed through to specialty ink and reagent catalogs within weeks, delaying project launches in diagnostics and printed-electronics niches. Hedging offers partial relief but raises working-capital needs, squeezing small firms that lack scale. Protective coatings that enable 30% metal-content reduction per chip are mitigating the blow, though adoption is uneven in medical segments that demand thicker biocompatible shells. The restraint subtracts 2.3 points from near-term CAGR until bullion prices stabilize or recycling yields improve.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Chemical reduction accounted for 40.55% of the gold nanoparticles market size in 2024, a legacy position rooted in established batch infrastructure across North America and Europe. Yet downstream users now demand tighter particle-size distributions and lower solvent footprints, tipping procurement decisions toward continuous-flow lines that log a robust 12.45% CAGR to 2030. Plant operators retrofit vortex-fluidic modules that shear precursor streams into micron-thick films, promoting uniform nucleation while capturing hydrogen coproduct for on-site boiler fuel. AI-guided sensors adjust residence-time loops in real time, holding polydispersity indexes below 0.08 and elevating lot-to-lot reproducibility for pharmaceutical customers.

The shift also intersects with green-chemistry imperatives because flow reactors use aqueous media and ambient pressure, slashing energy intensity by nearly one-third versus citrate batch routes. Seed-mediated growth schemes layered onto the same skid allow production of rods, prisms, and core-shell configurations without opening the system, minimizing contamination risk. Developers of high-resolution biosensors increasingly embed bespoke shapes generated via flow-switch programming, capturing margin premiums well above commodity colloids. As validation batches scale, analysts expect continuous-flow capacity share to pass 30% by 2028, cementing its status as the new reference standard for regulated therapeutic and diagnostic end uses.

The Gold Nanoparticles Market Report is Segmented by Synthesis Method (Chemical Reduction, Green/Biological Synthesis, and More), Application (Imaging, Targeted Drug Delivery, and More), End-User Industry (Electronics & Semiconductors, Healthcare & Life Sciences, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 36.33% of global revenue in 2024, underpinned by deep R&D budgets, FDA oversight that standardizes quality, and integrated supply chains bridging academic labs with contract manufacturers. Academic-industry consortia in Boston and San Diego help spin off start-ups that license nanoparticle IP for oncology, cardiology, and neurology applications. Stimulus grants channeled through the National Institutes of Health in 2025 further enlarge domestic pilot capacities, ensuring short lead times for clinical-grade material.

Asia-Pacific posts the swiftest 12.98% CAGR, reflecting China's large-scale colloid reactors, India's expanding generics sector, and Japan's sensor innovation ecosystem. Policy incentives in Guangdong and Zhejiang provinces reimburse up to 20% of capital outlays for continuous-flow lines that meet ISO 14001 benchmarks, fast-tracking green production footprints. Semiconductor companies headquartered in Seoul and Hsinchu consume rising nanoparticle volumes for high-density interposers and thermal-interface pads, while ASEAN electronics exporters use printed antennas in logistics trackers and smart-package labels.

Europe balances regulatory rigour with sustainability leadership, supporting market development through Horizon Europe grants that prioritize green-chemistry upgrades and circular-economy pilot trials. German automotive suppliers validate gold-catalyzed NOx-reduction modules engineered for next-generation fuel-cell vehicles. Meanwhile, Nordic med-tech clusters incorporate nanoparticle tags into rapid-sepsis tests aimed at point-of-care settings, addressing public-health priorities under the EU's Beating Cancer Plan.