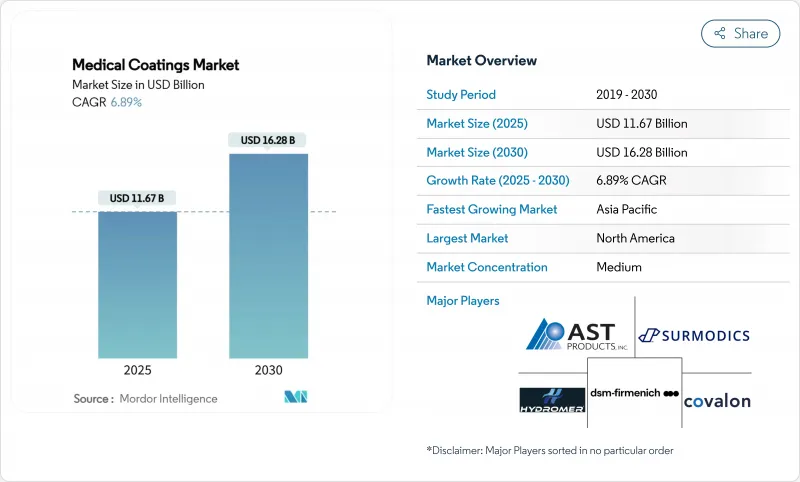

의료용 코팅 시장 규모는 2025년에 116억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 6.89%로, 2030년에는 162억 8,000만 달러에 달할 것으로 예상됩니다.

시장의 기세는 인구의 고령화, 감염 통제의 의무화, 고도로 설계된 표면 기술을 필요로 하는 저침습 수술의 급증의 수렴에 의한 것입니다. 파릴렌의 컨포멀 배리어 특성, 불소 수지의 마찰 저감 기능, 항균 화학은 이제 신세대 임플란트 및 일회용 기기의 핵심 구성 요소가 되고 있습니다. 통합 압력, 원자재 가격 변동, FDA 및 FTC와 같은 규제 당국의 모니터링이 경쟁적 행동을 형성하고 있지만, 스마트 임플란트에 지속적인 벤처 자금을 제공하면 지속적인 성장 가능성을 제시합니다. 지역별로는 북미가 2024년 매출 점유율 34.44%로 수요를 지지한 한편, 아시아태평양은 헬스케어 인프라의 확대와 수술 건수 증가를 배경으로 CAGR 8.99%를 나타낼 전망입니다.

헬스케어 관계자는 현재, 표면공학을, 수동적인 디바이스를, 약제를 전달하고, 생체신호를 감지하고, 감염에 저항하는 능동적인 치료 시스템으로 바꾸는 경로로 간주하고 있습니다. 정형외과에서 항균 보호와 뼈 통합 지원을 동시에 제공하는 다기능 코팅은 이러한 이동의 예입니다. 코팅된 임플란트의 재수술률이 낮음을 입증하는 학술적 증거는 병원이 비싼 가격을 지불할 것을 납득시키는 반면, 장비 제조업체는 환자의 원격 모니터링을 가능하게 하는 센싱 층을 통합하고 있습니다.

유행 시대의 감염 통제 교훈은 일회용 카테터와 수술 도구로의 전환을 가속화했습니다. 코팅 공급업체는 재사용 가능한 기구의 멸균 부담을 없애고 일회용 사용을 목적으로 한 비용 최적화된 친수성 마감으로 대응했습니다. 외래 센터는 회전 속도와 2차 오염 위험을 줄임으로써 혜택을 받으며 코팅된 일회용 기구의 수량 증가를 지원합니다.

2024년 PTFE 부족과 실리콘 전구체 비용 상승으로 인해 많은 코터는 공급 계약의 재협상, 출하 지연, 가격 인상을 강요했습니다. 헤지 능력이 부족한 소규모 업체는 수직 통합 라이벌에 점유율을 빼앗겼습니다. 대기업은 재고 버퍼로 충격을 흡수했지만 에너지 가격의 지속적인 변동은 투입 비용을 예측할 수 없게 만듭니다.

파릴렌 코팅은 2024년에 의료용 코팅 시장의 29.66%를 차지했습니다. 핀홀이 없는 등각 층은 신경 프로브, 심박조율기, 마이크로플루이딕스 칩을 보호하고 중요한 임플란트의 장기적인 신뢰를 지원합니다. 심장병학과 신경조절에 대한 수요는 안정적이지만, 원재료의 부족과 성막 사이클의 길이가 공급자의 비용 압박 요인이 되고 있습니다. 불소 수지 솔루션은 카테터 처리에서 초저 마찰 수요에 견인되어 CAGR 7.45%의 강력한 성장률을 보여줍니다. PFAS 규제의 초점은 불확실성을 높이고 있지만, 구명 의료기기에서는 헬스케어 적용 제외가 예상되고 전망은 유지됩니다. 실리콘 기반 화학물질은 탄성중합체 특성으로 인해 플렉서블 튜브 및 상처 케어 필름과 관련성을 유지하며, 금속 이온 및 바이오세라믹 코팅은 오세오 통합용으로 가치 있는 틈새 시장에 서식하고 있습니다.

의료용 코팅 시장에서 파릴렌 멤브레인은 친수성 탑 코트를 획득하고 불소 수 지층이 항균 첨가제를 채택한다는 처방의 상호 수분을 볼 수 있습니다. 이러한 하이브리드 스택을 제공하는 벤더는 벤더 리스트의 축소를 목표로 하는 OEM과 다년간 계약을 맺고 있습니다. 원자층 증착법의 진보는 파릴렌 상의 산화티탄의 핵 형성을 옹스트롬 수준에서 제어할 수 있게 되어, 배리어 성능이 향상되었습니다.

항균층은 2024년 매출 점유율의 30.56%를 차지하고 바이오필름 형성을 억제하는 병원의 의무화가 원동력이 되었습니다. 은 이온 코팅 및 항생제 코팅은 인공 관절과 중심 정맥 카테터에서 지속적인 병원체 살균률을 나타내며 장비의 안전성을 높입니다. 친수성/윤활성 코팅은 CAGR 7.87%로 가장 빠르게 성장하고 있으며, 구부러진 해부학적 구조를 원활하게 통과해야 하는 신경혈관과 말초의 인터벤션이 그 원동력이 되고 있습니다.

항균성과 윤활성을 결합한 다효과형 제제는 특히 감염과 편안함이 중요한 요도 카테터에서 두드러집니다. 항혈전성 화학 제제는 심혈관 이식편 및 보조 인공 심장과 같은 용도에서 중요한 역할을 합니다. '기타' 바구니에 포함된 약물용출성 옵션은 서방형 스텐트가 새로운 승인을 받으면서 견인력을 늘리고 있지만 중요한 심혈관 분야 이외의 보급에는 여전히 비용이 장벽이 되고 있습니다. OEM은 현재 마찰 계수, 로그 감소 값, 세포 독성 점수 등의 성능 대시보드를 지정하고 코팅업체가 매개변수 전반에 걸쳐 목표를 달성할 것으로 기대하고 있으며 기술 진입의 장애물을 높이고 있습니다.

북미는 2024년 매출의 34.44%를 차지해 선두 자리를 견지했습니다. 병원 구매위원회는 CMS가 의무화한 감염 감소 지표를 지원하는 코팅을 중시하고 안정적인 항균제 판매량을 지원합니다. 캐나다의 의료기기 수출 장려책과 멕시코의 수탁 제조 클러스터도 이 지역의 성장을 자극하고 있습니다.

아시아태평양은 중국의 메이드 인 차이나 2025의 목표와 고령화 사회에서의 처리율 상승에 견인되어 CAGR 8.99%로 가장 빠르게 성장하고 있습니다. 중국 국내 제조업체는 파릴렌과 친수성 화학물질을 통합하여 수입기기와의 성능 차이를 줄이고 일본과 한국 기업은 센서 통합형 임플란트를 개척하고 있습니다. 인도와 ASEAN 시장은 카테터 실험실이 급증함에 따라 기본 실리콘 코팅에서 고급 불소 수지로 마찰을 줄이기 위해 진보하고 있습니다.

유럽은 큰 수익을 올리고 있지만 불소 수지의 미래를 흐리게하는 PFAS의 불확실성에 직면하고 있습니다. 그럼에도 불구하고 독일 정형외과 클러스터와 아일랜드 수출 지향 장치 공장은 플라즈마와 CVD 라인에 대한 투자를 유지하고 있습니다. 브라질의 임플란트 공장에 대한 세제 우대 조치와 사우디아라비아의 "비전 2030"에 의한 의료 정비가 코팅 된 정형외과·심혈관 제품 수요를 높이고 있습니다.

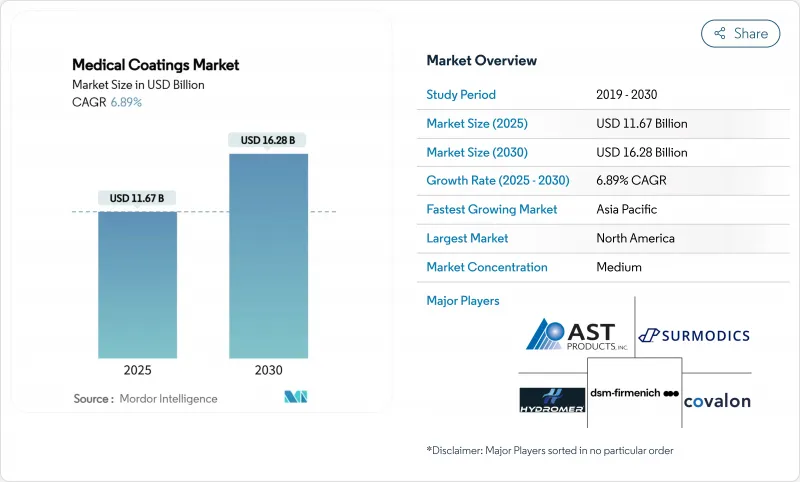

The Medical Coatings Market size is estimated at USD 11.67 billion in 2025, and is expected to reach USD 16.28 billion by 2030, at a CAGR of 6.89% during the forecast period (2025-2030).

The market's momentum comes from the convergence of aging populations, infection-control mandates and a surge in minimally invasive procedures that require highly engineered surface technologies. Parylene's conformal barrier properties, fluoropolymer friction-lowering capabilities and antimicrobial chemistry are now core building blocks in new-generation implants and single-use devices. Consolidation pressures, raw-material price swings and regulatory oversight from bodies such as the FDA and FTC shape competitive behavior, yet sustained venture funding in smart implants signals lasting growth prospects. Regionally, North America anchors demand with 34.44% revenue share in 2024, while Asia Pacific advances at an 8.99% CAGR on the back of healthcare infrastructure expansion and rising surgical volumes.

Healthcare practitioners now view surface engineering as a pathway to transform passive devices into active therapeutic systems that deliver drugs, sense biological signals and resist infection. Multifunctional coatings that simultaneously provide antimicrobial protection and bone-integration support in orthopedics exemplify this shift. Academic evidence demonstrating lower revision rates in coated implants is convincing hospitals to pay premium prices, while device makers integrate sensing layers that enable remote patient monitoring.

Pandemic-era infection-control lessons accelerated the pivot to disposable catheters and surgical tools. Coating suppliers responded with cost-optimized hydrophilic finishes designed for one-time use, eliminating the sterilization burden of re-usable instruments. Ambulatory centers benefit through faster turnover and reduced cross-contamination risk, supporting volume growth in coated disposables.

Shortages of PTFE and spikes in silicone precursor costs in 2024 forced many coaters to renegotiate supply contracts, delay shipments and raise prices. Smaller providers lacking hedging capacity lost share to vertically integrated rivals. Although larger players absorbed shocks through inventory buffers, persistent energy-price swings keep input costs unpredictable.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Parylene coatings represented 29.66% of the medical coatings market in 2024. Their pin-hole-free conformal layers protect neural probes, pacemakers and microfluidic chips, underpinning long-term trust in critical implants. Demand remains stable in cardiology and neuromodulation, yet raw material scarcity and deposition cycle length put cost pressure on suppliers. Fluoropolymer solutions are experiencing a robust growth rate of 7.45% CAGR, driven by the demand for ultra-low friction in catheter procedures. Regulatory focus on PFAS limits heightens uncertainty, but healthcare exemptions expected for life-saving devices preserve outlook. Silicone-based chemistries retain relevance in flexible tubing and wound-care films due to elastomeric properties, while metal-ion and bioceramic coatings inhabit high-value niches for osseointegration.

The medical coatings market is witnessing formulation cross-pollination whereby parylene films gain hydrophilic top-coats and fluoropolymer layers adopt antimicrobial additives. Suppliers offering such hybrid stacks secure multi-year contracts with OEMs looking to shrink vendor lists. Advancements in atomic layer deposition allow angstrom-level control of titanium oxide nucleation on parylene, boosting barrier performance.

Antimicrobial layers accounted for 30.56% of the revenue share in 2024, driven by hospital mandates to curb biofilm formation. Silver-ion and antibiotic coatings demonstrate sustained pathogen-kill rates in joint replacements and central-line catheters, enhancing device safety. Hydrophilic/lubricious finishes are experiencing the fastest growth at a 7.87% CAGR, powered by neurovascular and peripheral interventions that require smooth navigation through tortuous anatomy.

Multi-effect formulations that merge antimicrobial and lubricious traits stand out, particularly for urinary catheters where infection and comfort both matter. Anti-thrombogenic chemistries play a significant role in applications such as cardiovascular grafts and ventricular assist devices. Drug-eluting options in the "Others" basket gain traction as controlled-release stents receive new approvals, yet cost remains a barrier to widespread uptake outside critical cardiovascular segments. OEMs now specify performance dashboards-coefficient of friction, log-reduction values, cytotoxicity scores-and expect coaters to meet targets across parameters, raising technical entry hurdles.

The Medical Coatings Market Report is Segmented by Chemistry (Silicone, Fluoropolymer, and More), Coating Function Type (Antimicrobial, Hydrophilic/Lubricious, and More), Deposition Technology (Chemical Vapor Deposition, Plasma Spray, and More), Application (Medical Device, Implants, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained the top spot with 34.44% of 2024 revenue, underpinned by robust reimbursement, rigorous FDA pathways and a concentration of multinational OEM headquarters. Hospital purchasing committees emphasize coatings that support infection-reduction metrics mandated by CMS, anchoring steady antimicrobial volumes. Canada's device export incentives and Mexico's contract-manufacturing clusters also stimulate regional growth.

Asia Pacific is the fastest mover at an 8.99% CAGR, driven by China's Made in China 2025 targets and rising procedure rates among aging populations. Domestic Chinese manufacturers integrate parylene and hydrophilic chemistries to close performance gaps with imported devices, while Japanese and South Korean firms pioneer sensor-integrated implants. India and ASEAN markets progress from basic silicone coatings toward advanced fluoropolymer friction-reduction as catheter labs proliferate.

Europe contributes a sizeable revenue pool but faces PFAS uncertainty that clouds fluoropolymer futures. Nonetheless, Germany's orthopedic clusters and Ireland's export-oriented device plants sustain investment in plasma and CVD lines. South America and the Middle East & Africa remain nascent yet promising; Brazil's tax incentives for implant factories and Saudi Arabia's Vision 2030 healthcare build-out elevate demand for coated orthopedic and cardiovascular products.