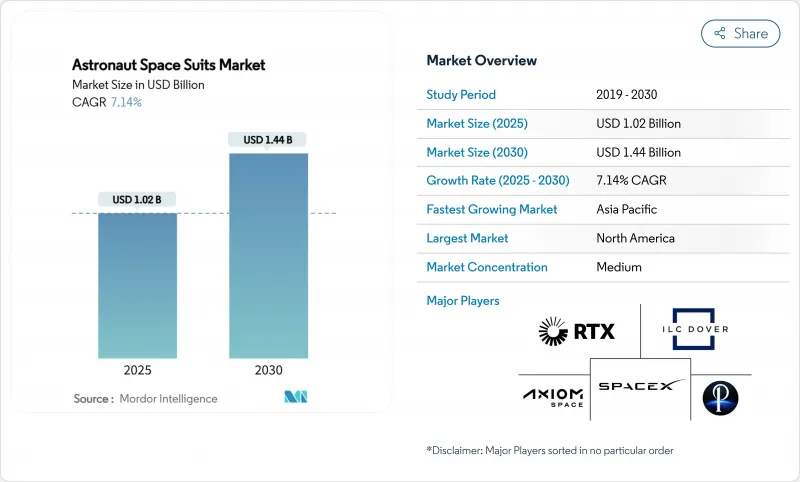

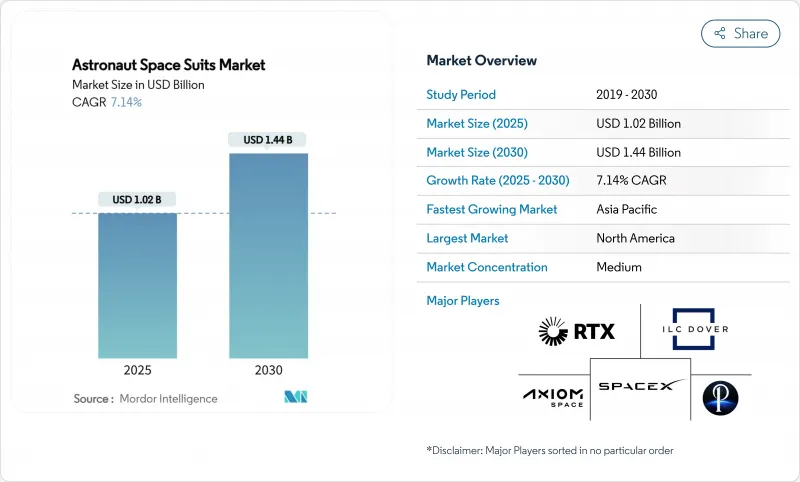

우주비행사 우주복 시장은 2025년에 10억 2,000만 달러로 평가되고, 2030년에는 14억 4,000만 달러에 이르며, CAGR 7.14%를 나타낼 것으로 예측됩니다.

이 확대는 상업 우주 여행, 민간 달 탐사 프로그램, 국가 탐사 이니셔티브가 차세대 생명 유지 시스템을 채택함에 따라 지금까지 정부 전용 고객 기반을 넘어서는 수요가 확대되고 있음을 반영합니다. 2024년 9월 폴라리스 돈 미션에서 SpaceX 최초의 상업선 외 활동에 의해 뒷받침된 바와 같이, 민간 자금을 통한 우주 수영으로의 전환은 민첩한 상업 개발자가 한때 NASA에 의해 정의된 성능 기준에 필적하게 되었습니다는 것을 뒷받침합니다. 북미는 아르테미스 조달을 통해 리드를 유지하고 있지만, 중국, 인도, 아랍 에미리트가 유인 우주 비행 예산을 늘리고 있기 때문에 아시아태평양이 가장 빠르게 성장하고 있습니다. 공급망의 회복력이 구조적인 원동력으로 부상하고 압력복 생산 능력을 확보하기 위해 Ingersoll Rand가 ILC Dover를 23억 2,500만 달러에 인수하는 등의 통합을 촉구하고 있습니다.

NASA의 Artemis 일정은 행성 표면용 정장 개발을 연구 개발의 최상위로 밀어 올렸습니다. 액시엄 스페이스의 AxEMU 프로토타입은 존슨 우주 센터에서 열진공 시험을 통과했으며, 달의 남극을 지배하는 -370°F 환경에서의 성능을 검증했습니다. 아르테미스 III를 2027년에 연기할 수 있는 지연은 먼지 경감층이나 소형화된 전력·냉각 서브시스템의 기술적 진보를 늦추지 않았습니다. 프라다는 고장력사와 인체공학에 근거한 패턴을 채용하는 것으로, 고급감과 미션의 안전성을 융합시킨, 분야 횡단적인 디자인의 도입을 실현하고 있습니다. 8시간의 선외 활동 능력, 보다 넓은 관절 가동역, 보다 경량인 휴대용 생명 유지 시스템은 우주비행사 우주복 시장의 각 계층에 영향을 주는 새로운 퍼포먼스 플로어를 설정했습니다.

2024년 6월 버진 갤럭틱의 12번째 서브 오비탈 비행은 반복 가능한 운영을 입증했고 2026년에 도착하는 델타 클래스 우주선을 예고했습니다. 블루 오리진의 2025년 4월 뉴셰퍼드 비행은 승객 모두가 여성인 것을 특징으로 하며, 승객의 편안함을 위해 어느 정도의 내구성을 교환하는 개인화된 IVA 의류로의 이동을 뒷받침했습니다. 이 분야에서는 2030년까지 500명 이상의 민간 우주비행사가 탄생할 것으로 예상되고 있으며, 제조업체 각사는 보다 대량으로 모듈화된 생산 라인을 목표로 하고 있습니다. SpaceX사의 폴라리스의 선외활동에서는 관광과 전문적인 미션의 표준을 교차함으로써 능력의 격차를 줄이고 우주비행사 우주복 시장의 대응 가능한 부분을 확대하고 있습니다.

콜린스 에어로스페이스사의 xEVAS로부터의 철수는 각 라이프 크리티컬한 개조의 재인증이 어떻게 상업적인 ROI의 역치를 넘어 지출과 리스크를 증대시키는지를 부각하고 있습니다. NASA의 유인 비행 규칙과 FAA의 상업 우주 비행 규칙의 이중 컴플라이언스는 개발주기를 늘리고 레거시 인증 인프라가있는 기업에게 유리합니다. 지적재산이 아니라 자본집약도가 우주비행사 우주복 시장에의 신규 진입을 막는 주요 장벽이 되고 있습니다.

IVA 슈트는 크루 드래곤, 스타라이너, 서유즈 우주선에서 거의 보편적인 역할에 힘입어 2024년 우주비행사 우주복 시장 점유율의 53.12%를 획득했습니다. 강화된 스타 라이너 IVA 의복은 2024년 ISS 투어에서 동체의 유연성을 향상시키고 이 부문의 우위를 강화했습니다. 행성 표면 정장의 우주비행사 우주복 시장 규모는 Artemis, Wangyu 프로그램, 상업 월면 관광 일정이 수렴함에 따라 CAGR 8.91%를 나타낼 것으로 예측됩니다. Axiom Space의 AxEMU 더스트 완화 스커트와 중국의 병렬 MPC 하이브리드 프로토타입은 햅틱 지침과 4G 음성 텔레메트리를 통합한 기동성 우선 설계를 보여줍니다. 예측 전반에 걸쳐 노후화된 EMU가 서비스 수명을 맞아 현재 안전 가이드라인을 충족하지 못할수록 EVA 교체 주기가 가속화됩니다.

행성 표면용 슈트는 기술의 프론티어가 됩니다. 기계적인 역압 패널은 캐빈의 압력을 희생하지 않고 부피를 줄이고, 그래핀이 들어간 직물이 햇빛의 변화로 인한 열 스파이크를 불러옵니다. 모듈식 허벅지 포트는 지질학 도구용 센서 포드를 수용하여 한 번의 출격당 과학적 처리량을 확장합니다. 아폴로 시대의 발목 제한은 트래버스 거리를 제한했습니다. 새로운 몸통 하부 베어링은 보폭을 32% 확대하여 월면 채굴 투자자들에게 매력적인 생산성 지표를 높였습니다. 그 결과, 이 하위 부문의 기술 혁신이 IVA 리프레시 프로그램에 연구개발 파급되어, 우주비행사 우주복 시장 전체가 강화됩니다.

정부기관은 NASA의 여러 해에 걸친 헌신과 중국의 국비 프로그램을 통해 2024년 우주비행사 우주복 시장 점유율의 62.35%를 유지했습니다. Artemis의 조달만으로 2032년까지의 서피스 슈트의 납품을 커버해, 1차 계약자의 볼륨을 지지하고 있습니다. 그러나 우주비행사 우주복 시장 규모는 민간 사업자에 기인하고 있으며, 버진 갤럭틱사, 블루 오리진사, 스페이스 X사가 비행 계획을 확대함에 따라 CAGR 8.24%를 나타낼 것으로 예측되고 있습니다. 폴라리스 돈의 선외 활동에 이어 민간 선외 활동 능력은 이제 ISS 운영에 필적하는 복잡성을 가지고 성능 차이는 축소되고 있습니다.

상업적 성장은 생산 경제성을 변화시킵니다. 표준화된 크기, 간소화된 폐쇄 시스템 및 퀵 스왑 글러브 모듈은 1개당 비용을 최대 25% 절감합니다. 유명인의 여객편에 관련된 상품화권은 공동 브랜드의 의복을 제공하는 제조업체에 2차적인 수입원을 만들어 냅니다. 미국 시장 경쟁법(Commercial Space Launch Competitiveness Act)에 따른 규제의 명확화로 인해 승객의 리스크 공개가 FAA 임계값을 충족하는 경우 사업자는 IVA 장비를 자체 인증할 수 있어 새로운 디자인 시장 출시 시간이 단축됩니다.

북미는 2024년 매출의 40.21%를 차지했으며 NASA의 지속적인 Artemis 기금과 SpaceX의 수직 통합형 제조에 지원되었습니다. 이 지역의 우주비행사 우주복 시장은 델라웨어, 텍사스, 플로리다에서 확립된 압력복 공급 라인에서 혜택을 누리고 있습니다. 미국 수출 규제 프레임워크은 국내 조달에 유리하지만 캐나다는 게이트웨이에 생명유지장치 생체공학을 제공하고 협력관계는 유지되고 있습니다. 2025년 의회 예산 상적은 선외활동 개수비를 2032년까지 연장하여 원청기업의 수량 예측을 가능하게 합니다.

아시아태평양의 CAGR은 8.83%로 가장 빠르며, 중국의 ISS급 스테이션과 월면 탐사의 두 가지 야망이 원동력이 되고 있습니다. 베어링 씰에서 PLSS 프로세서에 이르기까지 소블린 구성 요소를 강조하는 Wangyu 프로그램은 서쪽 ITAR 제약을 피하는 병렬 생태계를 구축합니다. 인도의 가간얀 모듈은 벵갈루루의 민간 기업과 제휴하여 2026년까지 IVA 환기 팩을 성숙시켜 지역 수출 가능성을 목표로 합니다. 한국과 일본은 JAXA의 쓰쿠바 콤플렉스에서 현존하는 우주복 테스트 베드를 활용해 태양계 궤도에 적합한 방사선 차폐 섬유의 공동 연구를 실시합니다.

유럽은 ESA의 Pextex 이니셔티브를 동원하여 달의 먼지를 시작하는 현무암 섬유 직물을 개발하는 등 지속적으로 견조합니다. 에어버스와 탈레스 알레니아 공간이 슈트포트 도킹 하드웨어를 제공하기 때문에 게이트웨이 조립이 시작되면 ESA에 귀속되는 우주비행사 우주복 시장 규모가 상승할 수 있습니다. 프랑스와 독일의 국가 우주 기관은 스파르탄 공간의 IVA 프로토타입에 공동 출자하여 대륙의 자주성을 높입니다. 폴란드와 체코 공화국의 동유럽 공급업체는 마이크로펌프 기술의 인큐베이션을 수행하고 주요 프라임이 통합되는 동안 밸류체인에서 발판을 확보합니다.

중동은 인공 위성에서 유인 우주 비행으로 축 발을 옮깁니다. UAE의 모하메드 빈 러시드 우주센터는 달의 레고리스를 본뜬 사막의 분진시험에서 훈련된 독자적인 설계를 주문하기 전에 러시아의 오랑 유닛을 개수하여 선외훈련을 실시합니다. 사우디아라비아는 NEOM 공업지대 내에 압력의류 공장을 병설하기 위한 자금을 확보하고, 세제우대조치로 구미의 파트너를 유치했습니다. 이러한 움직임은 우주비행사 우주복 시장을 다양화하고 단일 지역의 충격에 대한 헤지가됩니다.

The astronaut space suits market is valued at USD 1.02 billion in 2025 and is projected to reach USD 1.44 billion by 2030, advancing at a 7.14% CAGR.

This expansion reflects widening demand beyond the historical government-only customer base as commercial space tourism, private lunar programs, and national exploration initiatives adopt next-generation life-support systems. The transition toward privately funded spacewalks-underscored by SpaceX's first commercial EVA during the Polaris Dawn mission in September 2024-confirms that agile commercial developers now match performance standards once defined by NASA. North America preserves its lead through Artemis procurement, yet Asia-Pacific delivers the quickest growth as China, India, and the UAE elevate human-spaceflight budgets. Supply-chain resilience has emerged as a structural driver, prompting consolidation such as Ingersoll Rand's USD 2.325 billion purchase of ILC Dover to secure pressure-garment capacity.

NASA's Artemis schedule has moved planetary-surface suit development to the top of R&D agendas. Axiom Space's AxEMU prototype passed thermal-vacuum trials at Johnson Space Center, validating performance in -370°F environments that dominate the lunar south pole. Delays that may push Artemis III to 2027 have not slowed technical advances in dust-mitigation layers and miniaturized power-and-cooling subsystems. Prada's contribution of high-tensile yarns plus ergonomic patterning illustrates cross-sector design infusion that blends luxury with mission safety. Eight-hour EVA capability, wider joint articulation, and lighter portable life-support systems set new performance floors that influence every tier of the astronaut space suits market.

Virgin Galactic's 12th suborbital flight in June 2024 proved repeatable operations and previewed Delta-class vehicles arriving in 2026. Blue Origin's April 2025 New Shepard flight-featuring an all-female manifest-underscored the shift toward personalized IVA garments that trade some durability for passenger comfort. The sector anticipates more than 500 private astronauts by 2030, pushing manufacturers toward higher-volume, modular production lines. SpaceX's EVA work on Polaris bridges tourism and professional mission standards, narrowing the capability gap and enlarging the market's addressable portion of the astronaut space suits.

Collins Aerospace's exit from xEVAS highlights how re-certification of each life-critical modification multiplies expenditure and risk beyond commercial ROI thresholds. Dual compliance with NASA human-rating and FAA commercial-spaceflight rules lengthens development cycles, favoring firms with legacy certification infrastructures. Capital intensity, not intellectual property, has become the principal barrier to new entrants in the astronaut space suits market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

IVA suits captured 53.12% of the astronaut space suits market share in 2024, buoyed by their near-universal role aboard Crew Dragon, Starliner, and Soyuz vehicles. Enhanced Starliner IVA garments delivered improved torso flexibility during a 2024 ISS tour, reinforcing the segment's incumbency. The astronaut space suits market size for Planetary Surface Suits is projected to grow at an 8.91% CAGR as Artemis, the Wangyu program, and commercial lunar tourism schedules converge. Axiom Space's AxEMU dust-mitigation skirts and China's parallel MPC-hybrid prototypes exemplify mobility-first design, embedding haptic guidance and 4G voice telemetry. Across the forecast, EVA replacement cycles accelerate as aging EMUs approach end-of-life and fail to meet current safety guidelines.

Planetary surface suits represent the technology frontier. Mechanical counter-pressure panels cut bulk without sacrificing cabin pressure, while graphene-infused fabrics deflect thermal spikes from sun-shadow transitions. Modular thigh ports accept sensor pods for geology tools, expanding scientific throughput per sortie. Apollo-era ankle restrictions limited traverse distance; new lower-torso bearings enlarge step stride by 32%, raising productivity metrics attractive to lunar-mining investors. Consequently, innovation in this sub-segment sheds R&D spillovers into IVA refresh programs, reinforcing the broader astronaut space suits market.

Government agencies maintained 62.35% of the astronaut space suits market share in 2024, thanks to NASA's multi-year commitments and China's state-funded programs. Artemis procurement alone covers surface-suit deliveries through 2032, anchoring volumes for primary contractors. Yet, the astronaut space suits market size is attributable to commercial operators, and it is forecasted to expand at an 8.24% CAGR as Virgin Galactic, Blue Origin, and SpaceX scale flight cadence. Following the Polaris Dawn EVA, private EVA capability now rivals ISS operations in complexity, shrinking the performance gap.

Commercial growth alters production economics. Standardized sizing, simplified closure systems, and quick-swap glove modules cut per-unit costs by up to 25%. Merchandising rights around celebrity passenger flights create secondary revenue streams for manufacturers offering co-branded garments. Regulatory clarity under the US Commercial Space Launch Competitiveness Act allows operators to self-certify IVA equipment if passenger risk disclosures meet FAA thresholds, speeding time-to-market for new designs.

The Astronaut Space Suits Market Report is Segmented by Suit Type (IVA Suits, EVA Suits, Planetary Surface Suits), End User (Government Space Agencies, and More), Material Technology (Soft Suit, Hard Shell, Hybrid//Mechanical Counter-Pressure), Life Support Architecture (Backpack PLSS, Distributed-System PLSS, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 40.21% of 2024 revenue, anchored by NASA's sustained Artemis funding and SpaceX's vertically integrated manufacturing. The region's astronaut space suits market benefits from established pressure-garment supply lines in Delaware, Texas, and Florida. US export-control frameworks favor domestic sourcing, though Canada's contribution of life-support avionics to Gateway keeps cooperation intact. A renewed congressional budget top-up in 2025 extends EVA refurbishment spending to 2032, providing volume predictability for prime contractors.

Asia-Pacific posts the fastest 8.83% CAGR, powered by China's dual ISS-class station and lunar ambitions. The Wangyu program's emphasis on sovereign components-from bearing seals to PLSS processors-creates parallel ecosystems that bypass Western ITAR constraints. India's Gaganyaan module partners with private firms in Bengaluru to mature IVA ventilation packs by 2026, aiming for regional export potential. South Korea and Japan leverage extant spacesuit testbeds at JAXA's Tsukuba complex, collaborating on radiation-shielded textiles suitable for cislunar orbits.

Europe remains steady, mobilizing ESA's Pextex initiative to engineer basalt-fiber fabrics that repel lunar dust. The astronaut space suits market size attributable to ESA could rise once the Gateway assembly ramps, as Airbus and Thales Alenia Space provide suitport docking hardware. National space agencies in France and Germany co-finance Spartan Space's IVA prototype, enhancing the continent's autonomy. Eastern European suppliers in Poland and the Czech Republic incubate micro-pump technologies, securing a foothold in the value chain as bigger primes consolidate.

The Middle East pivots from satellite focus to human spaceflight. The UAE's Mohammed bin Rashid Space Centre pilots extravehicular training with refurbished Russian Orlan units before ordering indigenous designs trained on desert dust trials replicating lunar regolith. Saudi Arabia earmarked funding to co-locate a pressure-garment plant inside the NEOM industrial zone, courting Western partners with tax incentives. These moves diversify the astronaut space suits market and hedge against single-region shocks.