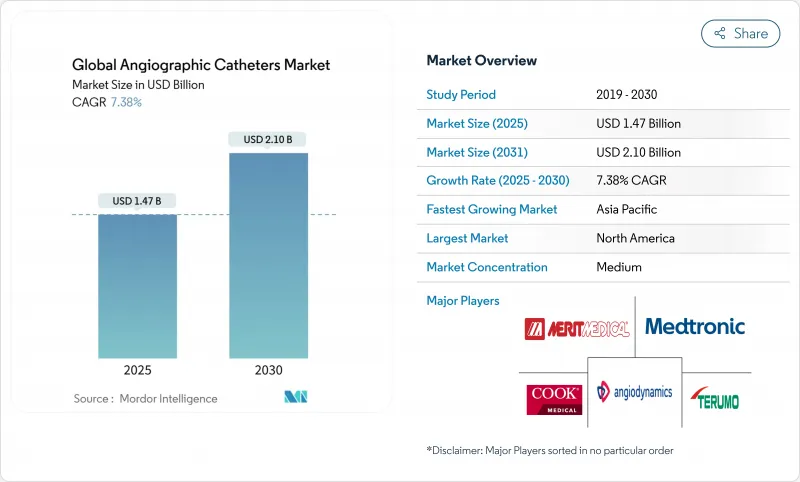

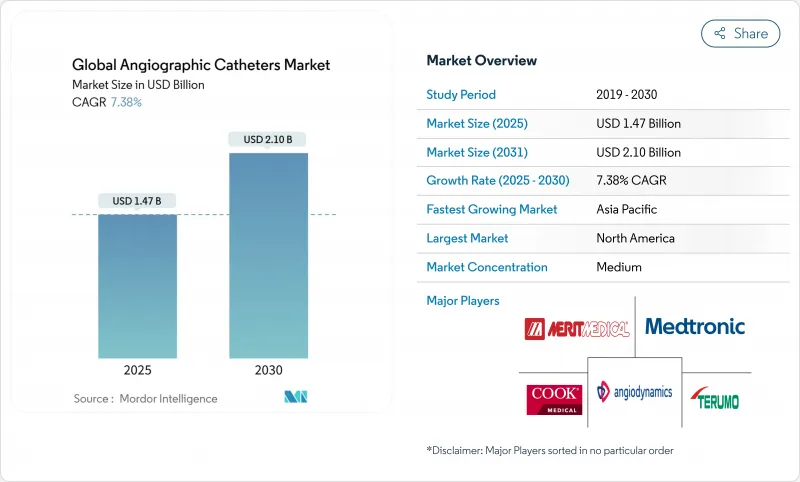

혈관조영 카테터 시장은 2025년에 14억 7,000만 달러로 추정되고, 2030년에는 21억 달러에 이를 것으로 예측되며, CAGR 7.38%로 성장이 전망됩니다.

이 성장은 심혈관 질환(CVD) 유병률 증가, 급속한 장비 혁신, 경피적 절차에 대한 외래로의 지속적인 전환을 반영합니다. 복잡한 병존질환을 안고 있는 고령화 사회가 안정된 시술 건수를 견인하는 한편, 진료 보수 개혁이 병원이나 외래 시설에, 재원 일수를 단축해 총 비용을 삭감하는 저침습 솔루션의 채용을 촉구하고 있습니다. 재료 과학의 혁신, 특히 나일론과 Pebax의 블렌드는 토크 제어와 견고성을 향상시켜 작은 액세스 포인트에서 복잡한 인터벤션을 가능하게 합니다. 보스턴 사이언티픽에 의한 실크로드 메디컬 인수 및 텔레플렉스에 의한 BIOTRONIK의 혈관 부문 인수와 같은 전략적 인수는 규모와 기술적 폭이 여전히 결정적인 경쟁력을 가지고 있음을 보여줍니다. 반대로, 혈관 내 이미징의 사용 확대는 순수한 혈관 조영 가이드 하에서의 혈관 조영을 감소시키기 시작했으며, 기본 카테터에 장기적인 사용량 감소의 역풍이 되었습니다.

허혈성 심장질환은 2024년에도 CVD에 의한 사망의 주요인으로 계속되었으며, 2,050만 명의 생명을 빼앗아 치료의 초점은 조기 진단과 저침습 치료로 옮겨가고 있습니다. 신흥국은 도시화와 함께 식생활 및 생활 습관의 위험 요인이 수렴함에 따라 가장 급격한 상승을 경험합니다. 따라서 특히 정부가 카테터 치료 설비에 투자하는 경우, 이와 연동하여 치료 건수가 증가합니다. 프라이빗 에퀴티 그룹은 이 수요를 지속적인 것으로 간주하여 2021-2023년 342개 시설로 구성된 41개의 순환기과 진료소를 인수하여 안정적인 도입의 흐름을 획득하는 지역 네트워크를 구축했습니다. 이러한 추세는 혈관조영 카테터 시장의 건전한 성장을 지원합니다.

고령자는 다지 협착, 석회화 병변, 허약의 비율이 높고, 각각 혈관의 안전성과 누르기 용이성의 밸런스를 취하는 특수한 카테터 플랫폼이 필요합니다. 혈관 경화는 기구의 내비게이션을 복잡하게 하기 때문에 제조업체는 샤프트의 경도 기울기와 팁의 유연성을 개선하도록 촉구하고 있습니다. 저침습 접근은 회복 시간의 단축으로 이어지며, 이는 여러 합병증을 가진 노인 환자를 관리하는 의사에게 중요한 성과입니다. 세계의 심장외과 벤치마크에 따르면, 중저소득국에서는 인구 10만 명당 61.6건의 카테터에 의한 심장수술 또는 수술적 심장수술이 언메트 니즈가 되어 평균 수명이 연장됨에 따라 카테터 확장의 여지가 커지고 있습니다.

기기 가격, 시설 사용료, 급성기 후의 케어 등이 함께, 혈관 조영은 일상적인 병원 수술 중에서 가장 비용이 많이 드는 것의 하나가 되고 있어, 현금 지불이나 공적 자금에 의한 시스템에서는 이 현실은 더욱 커집니다. 1,560억 달러의 미국 장비 시장은 복잡한 상환 채널을 조종하는 것이 제조업체에게 여전히 자원 집약적임을 보여줍니다. 비용 효과 연구는 경계 병변에 대한 약리학적 또는 예방적 선택을 지지하는 경향이 강해지고, 지불자가 임계값을 엄격하게 하면 카테터 사용률이 저하될 수 있습니다. 사전 승인을 의무화하는 이용 관리 프로그램은 현재 미국의 대부분의 보험 회사에 걸쳐 있으며, 긴급하지 않은 사례를 연장하는 관리 지연이 발생하고 있습니다.

관상동맥 부문은 2024년 혈관조영 카테터 시장 점유율의 49.91%를 차지했으며, 여전히 공급업체 수익의 기반이 되었습니다. 프로토콜이 성숙하고 있음에도 불구하고, 재료와 코팅의 개량이 진행되고 있기 때문에 수요는 안정되고 있으며, 관상동맥용 혈관조영 카테터 시장 규모는 안정적인 CAGR 7% 이상으로 병행 확대될 것으로 예측되고 있습니다. 대조적으로, 신경혈관 카테터는 기계적 혈전 제거술이 대혈관 뇌졸중의 최전선이 됨에 따라 CAGR 8.14%를 나타낼 전망입니다. 슈퍼 추적 가능한 원위 접근 카테터와 SOFIA Flow 88과 같은 흡입 플랫폼은 혈전 회수의 성공률을 최적화하고 신경혈관의 보급률을 밀어 올리고 있습니다.

혈관 내 인터벤션과 말초 인터벤션은 혈관 내 결석 파쇄 카테터와 같은 장치가 심하게 석회화된 병변을 치료하는 상당한 중간층을 형성합니다. 기타 카테고리-신제신경, 구조적 심장, 하이브리드 플랫폼-는 소규모이지만 여전히 이익을 얻고 있습니다. 메드트로닉의 Symplicity Spyral은 2025년에 잠정적인 패스스루 상태를 획득하여 보험 상환의 증액이 가능하게 되어, 고혈압 치료가 혈관조영 카테터 시장에 확실히 자리매김하게 되었습니다.

병원은 2024년 매출의 65.34%를 차지했는데, 이는 주로 외과 수술 백업과 ICU 치료가 필요한 복잡하고 긴급한 사례를 관리하기 때문입니다. 병원으로 인한 혈관조영 카테터 시장 규모는 여전히 상승하는 것으로 보이지만 그 속도는 ASC보다 느립니다. 외래센터는 낭비 없는 인원 배치 모델과 전용 룸을 활용하여 턴어라운드의 단축과 환자 처리량의 향상을 실현하고 있습니다. 성장세는 강내 장비 마진을 얻기 위해 원내에 ASC를 설립하는 심장병 그룹의 사모 주식에 의한 통합에 의해 더욱 강화됩니다.

전문 클리닉과 오피스 기반 랩(OBL)은 진단 혈관 조영술과 간단한 인터벤션을 위한 틈새 시장을 차지하며 이웃 병원과 스탭 공유에 의존합니다. 이러한 시설의 매력은 시설 사용료의 저렴함과 지역사회에 가깝지만 자본 요건이 확대 속도를 제한하고 있습니다. 이동식 카테터 실험실 유닛과 하이브리드 OR은 서비스가 잘 되지 않는 지역과 수술과 인터벤션의 복합 사례에 유연한 솔루션을 제공하여 이러한 상황을 청소합니다.

북미는 2024년 매출액의 42.71%를 차지했으며, 광범위한 보험 적용, 국가의 임상 지침, 높은 절차 밀도에 의해 지원됩니다. 획기적인 장비에 대한 과도적인 패스스루 결제는 투자 회수 사이클을 단축하고 병원이 재고를 업그레이드하는 동기를 부여합니다. 미국은 전 세계 의료기기 매출의 40%를 차지하고 있으며 재료 및 코팅 표준에 큰 영향력을 미치고 있습니다. 순환기과 진료소의 통합이 가속화되고, ASC 개척이 도시뿐만 아니라, 충분한 서비스를 받지 않은 지방에서도 행해지게 되어, 혈관조영 카테터 시장의 수량 성장이 유지되고 있습니다.

아시아태평양의 CAGR은 8.95%로 가장 높습니다. 중국에서는 장비 심사가 합리화되어 2023년에는 혁신적으로 분류되는 61건을 포함한 1만2,213건의 신규 등록이 승인되어 시장 투입까지의 시간이 대폭 단축되었습니다. Healthy China 2030 하에서 정부의 밀어남과 CVD 발생률의 상승이 이중 수요와 정책 추풍을 창출하고 있습니다. 일본과 한국은 수출 지향 제조업을 통해 공헌하고 인도는 2025년 마케팅 코드를 통해 윤리적 프로모션 기준을 인상하고 다국적 브랜드에 명확한 컴플라이언스 지침을 제공합니다.

유럽은 꾸준하지만 성장은 완만합니다. 의료기기 규제는 시장 진입을 중앙 집중화하고 독일 OPS 코딩 업데이트는 새로운 기술에 대한 상환의 무결성을 보장합니다. 프랑스의 2025년 애드온 지불 정책은 우위가 입증되면 특수 카테터에 대한 액세스를 확대합니다. 영국은 브렉시트 후에도 대륙의 임상 증거 파일을 많이 인식하고 중복 임상시험을 제한하는 명확하면서도 조화로운 패스웨이를 유지하고 있습니다.

중동 및 아프리카와 남미는 전체적으로 1자리대의 고성장을 전망할 수 있지만 구조적인 장애물에 직면하고 있습니다. 북아프리카에서 허혈성 심장 질환은 주요 DALY 증가 요인 중 하나이지만 공공 자금 부족과 두뇌 유출은 카테터 실험실의 확대를 방해합니다. 관민 파트너십과 기본 등급 카테터의 지역 제조에 기회가 있습니다. 라틴아메리카에서는 브라질이 3차 병원 하이브리드 심장센터를 통해 도입 선진을 끊고 아르헨티나와 콜롬비아는 환율 변동 위험이 있는 것, 상환 리스트를 꾸준히 갱신하고 있습니다.

The angiographic catheter market was valued at USD 1.47 billion in 2025 and is forecast to reach USD 2.10 billion by 2030, advancing at a 7.38% CAGR.

This growth reflects rising cardiovascular disease (CVD) prevalence, rapid device innovation, and the continued migration of percutaneous procedures to outpatient settings. An aging population with complex comorbidities drives steady procedural volume, while reimbursement reforms encourage hospitals and ambulatory sites to adopt minimally invasive solutions that shorten stays and lower overall costs. Material science breakthroughs-particularly Nylon & Pebax blends-improve torque control and kink resistance, enabling complex interventions through smaller access points. Strategic acquisitions such as Boston Scientific's purchase of Silk Road Medical and Teleflex's buyout of BIOTRONIK's vascular unit signal that scale and technological breadth remain decisive competitive levers. Conversely, expanding use of intravascular imaging is beginning to reduce purely angiography-guided runs, creating a long-term usage headwind for basic catheters.

Ischemic heart disease remained the leading cause of CVD deaths in 2024, claiming 20.5 million lives and shifting therapeutic focus toward earlier diagnosis and less-invasive care . Emerging economies experience the steepest climb as dietary and lifestyle risk factors converge with urbanization. Procedural volumes therefore rise in tandem, especially where governments invest in catheterization capacity. Private-equity groups viewed this demand as durable, acquiring 41 cardiology practices comprising 342 sites between 2021 and 2023 to build regional networks that capture steady referral streams. These trends collectively sustain healthy growth in the angiographic catheter market.

Older adults present higher rates of multivessel stenosis, calcified lesions, and frailty, each necessitating specialized catheter platforms that balance pushability with vessel safety. Vascular stiffening complicates device navigation, prompting manufacturers to refine shaft stiffness gradients and tip flexibility. Minimally invasive access translates to shorter recovery times-an outcome prized by physicians managing elderly patients with multiple comorbidities. Global cardiac surgery benchmarking suggests an unmet need of 61.6 catheter-based or surgical cardiac procedures per 100,000 population in low- and middle-income countries, implying vast room for catheter expansion as life expectancy rises .

Device prices, facility fees, and post-acute care combine to make angiography among the costliest routine hospital procedures, a reality magnified in cash-pay and publicly funded systems. The USD 156 billion U.S. device market demonstrates that navigating complex reimbursement channels remains resource-intensive for manufacturers . Cost-effectiveness studies increasingly favor pharmacologic or preventive options for borderline lesions, potentially dampening catheter usage when payers tighten thresholds. Utilization-management programs that mandate prior authorization now span most U.S. insurers, adding administrative lag that can defer non-urgent cases.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The coronary segment accounted for 49.91% of the angiographic catheter market share in 2024 and remains the bedrock of vendor revenue. Despite mature protocols, ongoing material and coating enhancements keep demand steady, with the angiographic catheter market size for coronary work projected to rise in parallel with stable 7%-plus CAGR. Neurovascular catheters, by contrast, show an 8.14% CAGR as mechanical thrombectomy becomes front-line for large-vessel stroke. Ultra-trackable distal access catheters and aspiration platforms such as SOFIA Flow 88 optimize clot retrieval success rates, pushing neurovascular penetration higher.

Endovascular and peripheral interventions form a sizable mid-tier, where devices like intravascular lithotripsy catheters treat heavily calcified lesions. The "Others" category-renal denervation, structural heart, and hybrid platforms-remains small yet lucrative. Medtronic's Symplicity Spyral won transitional pass-through status in 2025, unlocking incremental reimbursement and placing hypertension therapy firmly within the angiographic catheter market.

Hospitals retained 65.34% of 2024 revenue, largely because they manage complex and emergent cases requiring surgical back-up or ICU care. The angiographic catheter market size attributable to hospitals should still climb but at a slower rate than ASCs. Outpatient centers enjoy lean staffing models and dedicated rooms, translating to shorter turnaround and improved patient throughput. Growth momentum is further reinforced by private-equity consolidation of cardiology groups that establish in-house ASCs to capture downstream device margins.

Specialty clinics and office-based labs occupy a niche for diagnostic angiography and simple interventions, relying on shared staff with nearby hospitals. Their appeal lies in lower facility fees and community proximity, though capital requirements limit expansion pace. Mobile cath-lab units and hybrid ORs round out the landscape, offering flexible solutions for underserved regions or combined surgical-interventional cases.

The Angiographic Catheter Market Report is Segmented by Application (Coronary, Endovascular/Peripheral, and More), End-User (Hospitals, Ambulatory Surgical Centrs and More), Material (Polyurethane, Polyvinyl Chloride, and More), Coating Type (Hydrophilic, Non-Coated), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 42.71% revenue in 2024, underpinned by broad insurance coverage, national clinical guidelines, and high procedural density. Transitional pass-through payments for break-through devices shorten payback cycles, incentivizing hospitals to upgrade inventories. The U.S. alone holds 40% of global device sales and exerts outsized influence on material and coating standards. Consolidation among cardiology practices has accelerated, bringing ASC development to both urban and underserved rural counties, thereby preserving volume growth in the angiographic catheter market.

Asia-Pacific logs the highest CAGR at 8.95%. China streamlined device reviews, approving 12,213 new registrations in 2023, including 61 classified as innovative, which sharply cuts time-to-market. Government push under Healthy China 2030 and rising CVD incidence create dual demand and policy tailwinds. Japan and South Korea contribute through export-oriented manufacturing, while India's 2025 marketing code elevates ethical promotion standards, giving multinational brands clearer compliance guidance.

Europe offers steady but slower gains. The Medical Device Regulation unifies market entry, and Germany's updated OPS coding ensures reimbursement alignment for novel procedures. France's 2025 add-on payment policy widens access to specialty catheters once superiority is proven. Post-Brexit, the UK maintains a distinct yet harmonized pathway that still recognizes much of the Continental clinical evidence file, limiting duplicative trials.

The Middle East & Africa and South America collectively present high-single-digit growth potential but face structural hurdles. In North Africa, ischemic heart disease ranks among leading DALY drivers, yet public funding gaps and brain drain hinder cath-lab expansion. Opportunities lie in public-private partnerships and regional manufacturing of base-grade catheters. In Latin America, Brazil spearheads adoption through hybrid cardiac centers in tertiary hospitals, while Argentina and Colombia steadily update reimbursement lists, albeit with currency volatility risks.