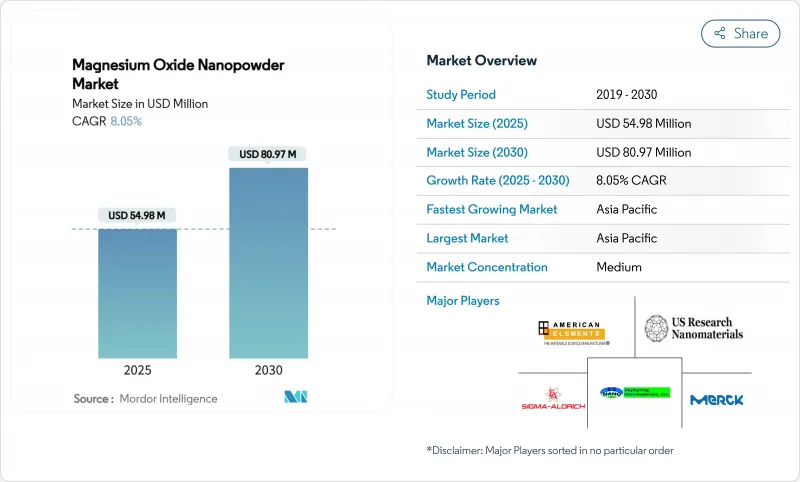

산화 마그네슘 나노파우더 시장 규모는 2025년에 5,498만 달러로 추정되고, 2030년에는 8,097만 달러에 이를 것으로 예상되며, 예측기간(2025-2030년)의 CAGR은 8.05%를 나타낼 전망입니다.

수익의 대부분은 여전히 기존의 내화물 수요에서 비롯되었지만, 그 기세는 연료 첨가제, 전기 절연, 난연성 고분자 화합물, 초기 고체 전지 프로토타입과 같은 고가치 용도로 분명히 변화하고 있습니다. 2024년 1차 마그네슘 생산량의 중국 점유율은 52%에 달했으며, 아시아 가공업자에게는 비용면에서 유리하게 되었지만, 세계의 바이어에게는 정책에 따른 변동에 노출되게 되었습니다. 경쟁적 위치는 첨단 복합재료와 전해질에 필요한 좁은 입도 분포와 기능화 표면을 실현하는 독자적인 합성 루트에 점점 의존하고 있습니다. 마지막으로, 북미와 EU는 인공 나노재료의 직장 노출 규제가 강화되어 컴플라이언스 비용이 상승하고 있지만, 인증된 품질 시스템을 가진 입증된 제조업체가 유리해지고 있습니다.

나노스케일 산화 마그네슘을 포함한 마그네시아-탄소 벽돌은 고밀도화를 나타내어 염기성 산소로나 전기 아크로에서의 공극률로 인한 파손을 줄입니다. 중국, 일본, 한국의 철강 제조업체는 팬, 탠디쉬, 연속 주조기의 라이닝에 나노 분말 등급을 표준화하여 급속한 열 사이클을 견딜 수 있도록하고 있습니다. 종합 철강 제조업체 간의 통합은 더 적은 구매자가 더 큰 구매력을 행사한다는 것을 의미하지만, 그들은 계획되지 않은 종료를 피하는 신뢰성에 대한 프리미엄을 지불합니다. 아시아태평양 전역에서 전기로의 생산 능력이 확대되는 가운데, 산화 마그네슘 나노파우더 시장 수요는 스크랩 기반의 철강 생산량 증가와 밀접한 상관관계를 유지하고 있습니다. 수직 통합 생산 및 내화물 배합에 대한 전문 지식을 가진 업계별 공급업체는 공동 R&D 계약을 중심으로 장기 계약을 획득할 수 있습니다.

산화 마그네슘 나노입자를 1wt% 첨가한 에폭시 시스템은 230°C에서 13의 유전율을 유지하고 열전도율은 미첨가 수지의 2배가 됩니다. 이러한 특성은 실리콘 카바이드 파워 모듈과 트랙션 인버터의 방열과 전기 저항률 사이의 만성적 절충을 해결합니다. 800V를 넘는 전기자동차의 드라이브 트레인 전압은 소형화된 폼 팩터와 함께 부분 방전 하에서도 화학적으로 불활성인 고온 절연 필러의 필요성을 높여주고 있습니다. 아시아태평양 케이블 제조업체는 공간 전하 축적을 억제하는 동결건조된 산화 마그네슘 폼을 채운 폴리에틸렌 화합물의 규모를 확대하고 있습니다. 풍력 터빈 인버터의 용량이 증가함에 따라 유럽의 전력 회사는 해상 변전소를위한 나노 입자 충진 포팅 화합물을 지정했습니다.

닛산 1,425kg의 생산이 가능한 졸-겔 플랜트는 4만 5,000달러를 넘는 자본 지출이 필요하며, 현재의 가격 구조에서는 투자 회수는 3년을 넘습니다. 에너지 집약적인 수열 공정과 탈탄산 공정은 EU와 미국의 특정 주에서 탄소 가격 설정에 대한 감도를 높입니다. 99.8wt%보다 엄격한 순도 규격은 시약과 여과 비용을 상승시키지만, 이것은 상품량 전체에서 상각할 수 없습니다. 아시아태평양 이외의 소규모 생산자는 규모의 불리에 직면하여 대규모 내화물 입찰 및 자동차 첨가제 공급 계약에 대한 입찰 능력이 제한됩니다.

2024년의 산화 마그네슘 나노파우더 시장 규모의 42.65%는 내화물이 차지했고 철강이나 알루미늄 용융 가공용의 마그네시아 카본 벽돌이나 탠디쉬 라이닝이 중심이 되었습니다. 전기 아크로의 기술 향상은 벽돌의 미세 구조를 치밀화하는 미립자 분포를 선호합니다. 스크랩 기반 철강이 아시아 전역에 깊숙이 침투하는 동안 에너지 효율적인 라이닝은 생산성에 있어 여전히 중요합니다. 시장의 리더십은 2030년까지 지속될 것으로 예상되지만, 새로운 용도가 확대됨에 따라 비율이 감소합니다.

연료 첨가제 카테고리는 2030년까지의 CAGR이 8.86%를 나타낼 전망인데, 이는 온로드 및 오프로드 플리트에서 미립자 물질과 NOx 배출을 줄이는 전례없는 규제 압력을 반영합니다. 나노입자 분산액은 분무화를 개선하고, 화염 온도의 균일성을 향상시키고, 엔진 하드웨어의 보증을 손상시키지 않으면서 그을음 전구체를 감소시킵니다. EU와 중국에서의 테스트 플릿 테스트는 2% 이상의 연비 향상을 보고했습니다. 이 부문은 작은 기준선에서 시작하지만, 성장 속도는 드롭 인 솔루션을 추구하는 자동차 관련 고객을 타겟팅하는 제조업체에 중점을 둡니다.

아시아태평양은 산화 마그네슘 나노파우더 시장의 2024년 수익의 52.18%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR) 8.76%를 나타낼 것으로 예측됩니다. 이 지역 수요를 지지하고 있는 것은 중국이지만, 일본 세라믹의 전문 지식과 한국의 반도체 에코시스템이 초고순도 등급에 더욱 견인력을 부여하고 있습니다. 에너지 전이 하드웨어를 목표로 한 정부의 자극 전략은 전기자동차의 열 관리 및 고체 배터리의 파일럿 라인에서 추가량을 촉진합니다.

북미는 규모는 작지만 기술적으로 풍부한 무대이며 항공우주, 방위, 첨단 파워 일렉트로닉스에서 하이스펙 파우더가 사용되고 있습니다. 미국은 국내 공급 안보 조치를 요구하고, 마그라티아와 같은 신흥 기업은 해수에서 탄소 중립 마그네슘 추출을 시험적으로 실시했습니다. 캐나다의 크리티컬 미네랄 전략에는 나노파우더 마감 라인의 자본 장애물을 낮추기 위한 보조금이 포함되어 있으며 이 지역을 수입국에서 특수 등급 수출국으로 재지정할 수 있습니다.

건축 기준법이 난연성 기준을 엄격히 하고 자동차 제조업체가 마그네슘을 많이 포함하는 전자 이동성 부품을 채택함에 따라 유럽은 안정적인 성장을 유지하고 있습니다. 독일은 자동차 산업과 화학 산업을 기반으로 소비를 이끌고 있지만 영국은 고온 단열재가 필요한 항공우주 및 방위 프로젝트를 개척하고 있습니다. EU의 서큘러 이코노미(순환형 경제) 규제는 할로겐 대체품보다 광물 기반의 난연성 필러를 장려하고 있으며, 산화 마그네슘 나노파우더 시장의 확대에 규제면에서의 추풍이 되고 있습니다. EU권의 에너지 전략 지령은 또한 MgO가 중요한 인터페이스 역할을 하는 고체 전지 컨소시엄에 자금을 유도하고 있습니다.

The Magnesium Oxide Nanopowder Market size is estimated at USD 54.98 Million in 2025, and is expected to reach USD 80.97 Million by 2030, at a CAGR of 8.05% during the forecast period (2025-2030).

Most revenue still flows from legacy refractory demand, yet momentum is clearly shifting toward high-value applications in fuel additives, electrical insulation, flame-retardant polymer compounds and early solid-state battery prototypes. Supply security is shaped by China's 52% share of primary magnesium production in 2024, which delivers cost advantages for Asian processors but exposes global buyers to policy-driven volatility. Competitive positioning increasingly depends on proprietary synthesis routes that deliver narrow particle-size distributions and functionalized surfaces needed in advanced composites and electrolytes. Finally, tightening workplace-exposure limits for engineered nanomaterials in North America and the EU are raising compliance costs, but they also favour established producers with certified quality systems.

Magnesia-carbon bricks incorporating nanoscale magnesium oxide show higher densification that lowers porosity-induced failure in basic oxygen and electric arc furnaces. Steelmakers in China, Japan and South Korea have standardised nanopowder grades in ladle, tundish and continuous-caster linings to withstand rapid thermal cycling. Consolidation among integrated steel producers means fewer buyers wield greater purchasing power, but they pay premiums for reliability that avoids unplanned shutdowns. As electric arc furnace capacity expands across Asia-Pacific, magnesium oxide nanopowder market demand remains closely correlated with rising scrap-based steel output. Suppliers with vertically integrated production and refractory formulation expertise can capture long-term contracts anchored in joint R&D agreements.

Epoxy systems loaded with 1 wt% magnesium oxide nanoparticles maintain a dielectric constant of 13 at 230 °C and double the thermal conductivity versus neat resin. These attributes solve the chronic trade-off between heat dissipation and electrical resistivity in silicon carbide power modules and traction inverters. Electric-vehicle drive-train voltages above 800 V, combined with miniaturised form factors, amplify the need for high-temperature insulation fillers that stay chemically inert under partial discharge. Asia-Pacific cable makers are scaling polyethylene compounds filled with freeze-dried magnesium oxide foams that suppress space-charge accumulation. As wind-turbine inverters grow in capacity, European utilities are also specifying nanoparticle-filled potting compounds for offshore substations.

Sol-gel plants capable of 1,425 kg day-1 output require capital spending above USD 45,000 and return on investment stretches beyond three years under today's price structure. Energy-intensive hydrothermal and calcination steps heighten sensitivity to carbon-pricing trajectories in the EU and selected US states. Purity specifications tighter than 99.8 wt% raise reagent and filtration costs that cannot be amortised across commodity volumes. Smaller producers outside Asia-Pacific face scale disadvantages, which limits their ability to bid for large refractory tenders or automotive additive supply contracts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Refractory materials generated 42.65% of the magnesium oxide nanopowder market size in 2024, anchored in magnesia-carbon bricks and tundish linings for steel and aluminium melt processing. Technical upgrades in electric arc furnaces favour finer particle distributions that densify brick microstructures. As scrap-based steel makes deeper inroads across Asia, energy-efficient linings remain critical for productivity. Market leadership is expected to persist through 2030, though its proportional share will slip as newer uses scale.

The fuel-additive category shows an 8.86% CAGR to 2030, reflecting unprecedented regulatory pressure to cut particulate and NOx emissions in both on-road and off-road fleets. Nanoparticle dispersions improve atomisation, raise flame temperature uniformity and reduce soot precursors without compromising engine hardware warranties. Pilot fleet tests in the EU and China report fuel-economy gains above 2%. Although the segment starts from a small baseline, its growth pace makes it a focal point for producers targeting automotive clients seeking drop-in solutions.

The Magnesium Oxide Nanopowder Market Report is Segmented by Application (Refractory Materials, Electric Insulation, Fuel Additive and More), Synthesis Method (Physical Method, Chemical Precipitation, and More), End-User Industry (Auto Metallurgy, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific owned 52.18% of 2024 revenue in the magnesium oxide nanopowder market and is forecast to advance at an 8.76% CAGR through 2030, underpinned by integrated supply chains, cost-advantaged feedstock and dense clusters of steel, electronics and battery manufacturers. China anchors regional demand, yet Japan's ceramics expertise and South Korea's semiconductor ecosystem provide incremental pull for ultra-high-purity grades. Government stimulus aimed at energy-transition hardware drives additional volume in electric-vehicle thermal management and solid-state battery pilot lines.

North America is a smaller but technologically rich arena in which aerospace, defence and advanced power electronics consume high-spec powders. The United States requisitioned domestic supply security measures, and start-ups such as Magrathea are piloting carbon-neutral magnesium extraction from seawater, which could de-risk feedstock procurement and reinforce local value chains by the late 2020s. Canada's critical-minerals strategy includes grants that lower capital hurdles for nanopowder finishing lines, potentially repositioning the region as an exporter of specialty grades rather than an importer.

Europe maintains steady growth as building codes tighten flame-retardancy thresholds and automakers adopt magnesium-rich e-mobility components. Germany leads consumption due to its automotive and chemical base, whereas the United Kingdom taps aerospace and defence projects requiring high-temperature insulation. EU circular-economy regulations encourage mineral-based fire-retardant fillers over halogenated alternatives, offering regulatory tailwinds for magnesium oxide nanopowder market expansion. The bloc's energy-strategy directives also channel funds into solid-state battery consortia where MgO plays a critical interface role.