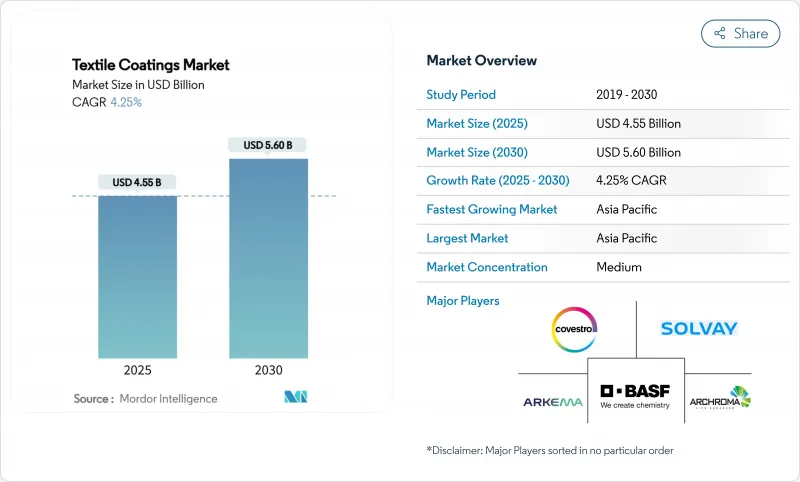

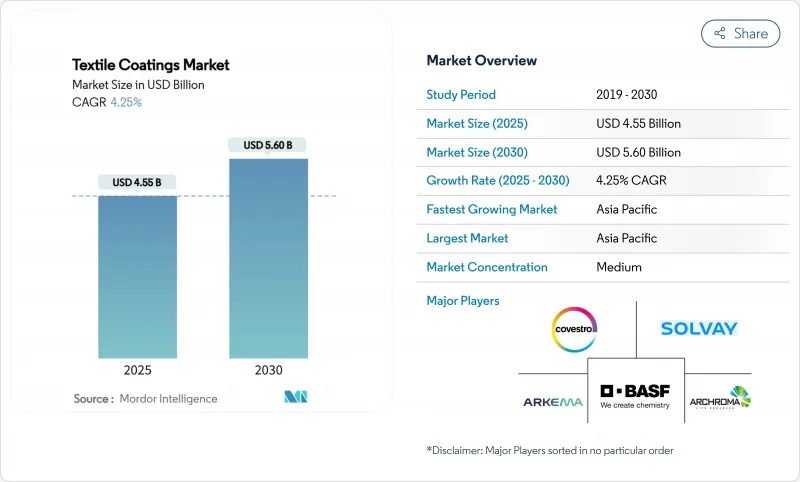

섬유 코팅 시장 규모는 2025년에 45억 5,000만 달러로 평가되었고 예측 기간 중(2025-2030년)의 CAGR은 4.25%를 나타낼 것으로 예측되며 2030년에 56억 달러에 이를 전망입니다.

수성 및 무용매 폴리머 시스템으로의 가속화된 전환이 이 변화의 핵심에 자리 잡고 있습니다. 제조업체들은 내구성이나 미적 요소를 저해하지 않으면서도 낮은 VOC(휘발성 유기화합물) 프로파일을 추구하기 때문입니다. 아시아태평양 지역은 비용 경쟁력 우위를 유지하며 신규 생산 능력의 대부분을 흡수하는 반면, 북미와 유럽은 글로벌 제형 선택에 영향을 미치는 고성능 화학 기술과 규제 프레임워크를 주도하고 있습니다. 의료, 자동차, 인프라 부문은 항균성, 내후성, 난연성 특성을 중심으로 성능 기준을 재정의하며, 공급업체들이 기존 PFAS 화학물질에서 벗어나 다각화하도록 촉구하고 있습니다. 실리콘 기반 에멀젼, 플라즈마 표면 처리, 디지털 도포 라인에 대한 투자는 양적 규모보다 특수 성능과 마진 회복력을 선택하려는 경쟁적 시장 환경을 보여줍니다. 이러한 배경 속에서 섬유 코팅 시장은 2030년까지 기술 로드맵을 형성하는 비용, 규정 준수, 맞춤화 압박 사이의 균형을 계속 유지하고 있습니다.

세계의 규제 기관들은 성능 및 안전 기준을 강화하며, 제조업체들이 NFPA 1971-2018과 같은 최신 규정을 충족시키면서 PFAS를 제거한 난연성, 내화학성, 방습성 솔루션을 개발하도록 촉구하고 있습니다. 밀리켄(Milliken)은 기존 내구성 기준을 뛰어넘는 비 PFAS 대체재를 선보이며 경쟁사들 간의 혁신 경쟁을 자극하고 시험실 투자를 가속화했습니다. 유럽 공급업체들은 그린딜 목표에 부합하기 위해 생물 기반 화학 물질로 초점을 확장하고 있으며, 수요는 소방복에서 산업용 작업복으로 확대되어 섬유 코팅 시장 내에서 규정을 준수하는 화학 물질의 상업적 잠재력을 넓히고 있습니다.

전기차 및 자율주행차의 경량화 의제와 고급 실내 공간에 대한 기대는 마모 저항성, 열 관리, 항균성을 한 층으로 제공하는 코팅으로 이어집니다. 주류 미디어에서 보도된 기존 난연제에 대한 건강 우려는 더 안전한 대안으로의 재구성을 촉진하며, OEM의 지속가능성 목표와 엄격한 실내 공기질 기준을 모두 충족하는 플랫폼으로 조달을 유도하고 있습니다. 아시아 변환업체들은 비용 및 규모 이점을 활용해 실내 장식용 의류 계약을 수주하며, 아시아태평양 지역의 섬유 코팅 시장 수요 및 공급 중심지 역할을 강화하고 있습니다.

폴리비닐 알코올, 면, 석유 유래 합성섬유는 반복적인 가격 변동을 보이며, 현물 시장에 크게 노출된 코팅업체들의 계획 주기를 왜곡하고 마진을 잠식합니다. 2025년 초 폴리비닐 알코올 가격은 하락했으나, 석유 변동성으로 합성섬유 비용은 10-15% 상승하여 혼합된 원자재 비용 상황을 초래했습니다. 이는 신중한 재고 관리와 장기 공급 계약을 강요합니다. 이러한 변동성은 섬유 코팅 시장에서 단기 수익 불확실성을 야기합니다.

열가소성 폴리머는 비용 효율성, 기계적 강도 및 재활용 가능성의 균형을 반영하여 2024년 섬유 코팅 시장 점유율의 51.23%를 차지하며 부문를 지배합니다. 수요는 내마모성과 치수 안정성이 필수적인 자동차 시트, 보호복, 유연 건설용 막에 집중됩니다. 최종 사용자는 강화되는 VOC 제한에 부합하는 수성 및 무용매 코팅 화학물질과의 호환성으로 열가소성 수지를 선호합니다. 경량 전기차 내장재 및 모듈식 인프라 프로젝트는 물량 요구를 더욱 증가시킵니다. 이러한 복합적 요인으로 열가소성 수지는 주요 소비 지역 전반에 걸쳐 고성능 코팅용 선호 기판으로 자리매김합니다.

열가소성 폴리머는 2030년까지 6.34%의 가장 빠른 연평균 복합 성장률(CAGR)을 기록할 전망으로, 섬유 코팅 시장 규모에서 규모와 성장 동력 양면에서 이중 리더십을 공고히 할 것입니다. 천연 섬유, 셀룰로오스 기반 섬유, 열경화성 섬유 등 경쟁 소재들은 열가소성 플라스틱의 가공 속도, 내열성, 재활용성 우위를 따라잡지 못해 성장세가 뒤처지고 있습니다. 공중합체 혼합물과 표면 처리 기술의 점진적 혁신은 환경 규정 준수를 저해하지 않으면서 성능 한계를 지속적으로 높이고 있습니다. 하류 브랜드들이 순환 경제 약속을 확대함에 따라, 코팅된 열가소성 직물을 재용해 및 재가공할 수 있다는 전망은 장기적 매력을 강화합니다. 결과적으로 신규 코팅 라인에 대한 자본 지출은 해당 부문의 지속적인 확장을 위한 생산 능력 확보를 위해 열가소성 친화적 설비 구성을 점점 더 목표로 삼고 있습니다.

2024년 직물 기판은 45.18%의 텍스타일 코팅 시장 점유율을 달성했으며, 6.01%의 연평균 성장률(CAGR)을 동반한 이 우위는 본질적인 인장 강도, 치수 안정성 및 우수한 코팅 고정력을 반영합니다. 구조적 무결성을 타협할 수 없는 자동차, 건축 및 안전 분야는 장기적 성능을 위해 직물 구조를 선호합니다. 부직포 기술 발전은 코팅 침투성과 기능적 균일성을 개선하는 공학적 다공성 덕분에 의료용 일회용품 및 여과 매체 분야에서 점차 주목받기 시작했습니다.

편직 직물은 신축성과 드레이프성이 요구되는 틈새 시장을 차지하고 있으나, 접착력과 형태 유지력의 한계로 인해 대규모 기술적 응용 분야로의 진출은 제한적입니다. 직물의 안정성과 편직물의 편안함을 결합한 하이브리드 다층 직물이 스포츠 및 의료용 보조기 분야에서 등장하며, 기판 혁신이 텍스타일 코팅 시장 내 차별화를 위한 핵심 동력임을 시사합니다.

아시아태평양 지역은 2024년 글로벌 매출의 53.12%를 차지하며, 섬유 코팅 시장 전반에 걸친 가격 형성 및 공급 배분에 대한 영향력을 공고히 했습니다. 중국은 2024년 섬유 및 의류 수출액 3,010억 달러 중 1,420억 달러가 섬유에서 비롯되었으며, 이는 베트남, 인도, 방글라데시로 다각화 움직임 속에서도 여전히 보유한 생산 역량의 깊이를 보여줍니다. 인도의 생산 연계 인센티브 프로그램(PLI) 및 PM MITRA 산업단지 같은 정책 도구는 2030년까지 국내 생산 가치를 3,500억 달러로 끌어올리는 것을 목표로 하며, 국내 제형 개발사들이 수성 화학 기술을 조기에 도입하고 신규 생산 능력에 이를 통합하도록 장려하고 있습니다. 방글라데시와 베트남은 경쟁력 있는 노동 비용과 무역 협정을 통해 입지를 공고히 하고 있으나, 특정 품목에 대한 미국의 관세 부과로 인해 조달 전략이 재편되고 현지 공급업체들이 기능적 차별화를 더욱 강화할 수 있습니다.

북미는 기술 중심 지역으로 남아, 규제 열기를 PFAS 무첨가 및 저휘발성 유기화합물(VOC) 시스템의 상업적 기회로 전환하고 있습니다. 캘리포니아와 뉴욕은 2025년 1월부터 세계에서 가장 엄격한 섬유 화학물질 금지 조치를 시행하며, 이미 규정 준수 제품군 공급 역량을 갖춘 기업들의 선점 우위를 촉진하고 있습니다. 루브리졸의 개스토니아 아크릴 에멀젼 생산 시설 2천만 달러 규모 확장은 가정용 섬유 및 자동차 내장재용 고성능 기능성 직물 수요 집적을 지원하며, 해당 지역의 부가가치 틈새 시장 지향성을 강화합니다. 캐나다의 미국 자동차 생산 연계성은 국경 간 수요를 유지하지만, 원자재 가격 변동 주기에 대한 노출로 조달 전략의 지속적인 재조정 필요성이 발생합니다.

유럽은 지속가능 화학 및 첨단 가공 분야에서 선도적 위치를 유지합니다. 독일, 프랑스, 북유럽 혁신 기업들은 수성 폴리우레탄 및 바이오 폴리머 기술의 한계를 넓히면서 물과 에너지 투입량을 획기적으로 절감하는 플라즈마 및 디지털 적용 라인에 투자하고 있습니다. 프로이덴베르크의 헤이텍스 자산 1억 유로 인수와 같은 거래는 기술 섬유 포트폴리오를 확장하며 지속적인 통합을 예고합니다. EU 순환경제 법안은 재활용 코팅 및 폐쇄형 인프라에 대한 관심을 촉진하여 섬유 코팅 시장을 지역 기후 목표의 수혜자이자 촉진자로 자리매김하게 합니다.

The Textile Coatings Market size is estimated at USD 4.55 billion in 2025, and is expected to reach USD 5.60 billion by 2030, at a CAGR of 4.25% during the forecast period (2025-2030).

Accelerated migration toward waterborne and solvent-free polymer systems sits at the center of this shift, as manufacturers seek lower VOC profiles without compromising durability or aesthetics. Asia-Pacific retains cost-leadership advantages and absorbs a majority of new capacity, while North America and Europe propel high-performance chemistry and regulatory frameworks that influence global formulation choices. Medical, automotive, and infrastructure segments are reframing performance benchmarks around antimicrobial, weather-resistant, and flame-retardant properties, prompting suppliers to diversify away from legacy PFAS chemistries. Investments in silicone-based emulsions, plasma surface treatment, and digital application lines reveal a competitive field willing to trade volume for specialty performance and margin resilience. Against this backdrop, the textile coatings market continues to balance cost, compliance, and customization pressures that collectively shape technology road maps through 2030.

Global regulators are tightening performance and safety benchmarks, prompting manufacturers to develop flame-resistant, chemical-resistant, and moisture-barrier solutions that eliminate PFAS while meeting updated norms such as NFPA 1971-2018. Milliken introduced non-PFAS alternatives that surpass earlier durability thresholds, stimulating competitive innovation and accelerating test-lab investments among rivals. European suppliers extend the focus to bio-based chemistries to align with Green Deal ambitions, and demand extends from firefighting ensembles to industrial workwear, broadening commercial potential for compliant chemistries within the textile coatings market.

Lightweighting agendas and premium cabin expectations in electric and autonomous vehicles translate into coatings that deliver abrasion resistance, thermal management, and antimicrobial properties all in one layer. Health concerns about legacy flame retardants reported in mainstream media spur reformulations toward safer alternatives, steering procurement toward platforms that satisfy both OEM sustainability goals and stringent interior-air-quality metrics. Asian converters leverage cost and scale advantages to win upholstery contracts, reinforcing Asia-Pacific's role as demand and supply nucleus for the textile coatings market.

Polyvinyl alcohol, cotton, and oil-derived synthetics exhibit recurrent price swings that distort planning cycles and erode margins among coaters heavily exposed to spot markets. Polyvinyl alcohol price declines in early 2025, yet synthetic fiber costs climbed 10-15% on oil volatility, producing a mixed input-cost picture that forces cautious inventory management and long-term supply contracts. Such volatility introduces near-term earnings uncertainty in the textile coatings market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Thermoplastic polymers dominate the segment with 51.23% of textile coatings market share in 2024, reflecting their balance of cost efficiency, mechanical strength, and recyclability. Demand concentrates in automotive upholstery, protective apparel, and flexible construction membranes where abrasion resistance and dimensional stability are mandatory. End-users favor thermoplastics for compatibility with waterborne and solvent-free coating chemistries that align with tightening VOC limits. Lightweight electric-vehicle interiors and modular infrastructure projects further elevate volume requirements. These combined drivers anchor thermoplastics as the preferred substrate for high-performance coatings across major consumption regions.

Thermoplastic polymers will also deliver the fastest 6.34% CAGR through 2030, underscoring their dual leadership in both scale and momentum within the textile coatings market size. Competitive materials such as natural, cellulose-based, and thermoset fibers trail in growth because they struggle to match the processing speed, thermal tolerance, and recyclability advantages of thermoplastics. Incremental innovations in copolymer blends and surface treatments continue to raise the performance ceiling without sacrificing environmental compliance. As downstream brands expand circular-economy commitments, the prospect of re-melting and re-processing coated thermoplastic fabric reinforces long-term attractiveness. Consequently, capital expenditure in new coating lines increasingly targets thermoplastic-friendly configurations to secure capacity for the segment's sustained expansion.

Woven substrates achieved 45.18% textile coatings market share in 2024 and pair that dominance with a 6.01% CAGR, reflective of their inherent tensile strength, dimensional stability, and superior coating anchorage. Automotive, architectural, and safety segments, which cannot compromise on structural integrity, prefer woven constructions for long-term performance. Non-woven advancements begin gaining traction in medical disposables and filtration media, aided by engineered porosity that improves coating penetration and functional uniformity.

Knitted fabrics occupy niches demanding stretch and drape, yet adhesion and shape-retention limits constrain penetration in large technical applications. Hybrid multilayer fabrics combining woven stability with knitted comfort emerge in sports and medical braces, indicating that substrate innovation remains a critical lever for differentiation within the textile coatings market.

The Textile Coatings Market Report Segments the Industry by Polymer Type (Thermoplastics, Thermosets, and More), Fabric Type (Woven, Knitted, Non Woven), Functionality (Waterproof and Breathable, Flame Retardant, and More) Application (Clothing, Transportation, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 53.12% of global revenue in 2024, cementing its influence on price formation and supply allocation across the textile coatings market. China shipped USD 301 billion in textiles and garments in 2024, of which USD 142 billion stemmed from textiles, underscoring capacity depth even amid diversification moves toward Vietnam, India, and Bangladesh. Indian policy tools such as the Production Linked Incentive program and PM MITRA parks seek to elevate national production value to USD 350 billion by 2030, encouraging domestic formulators to embrace water-based chemistries early and embed them in new capacity. Bangladesh and Vietnam cement footholds via competitive labor costs and trade agreements, but the imposition of US tariffs on certain categories could reorder sourcing strategies and push local suppliers toward greater functional differentiation.

North America remains a technology-centric region, channeling regulatory fervor into commercial opportunities for PFAS-free, low-VOC systems. California and New York enact some of the world's most stringent textile chemical bans effective January 2025, prompting early-mover advantage for firms already equipped to supply compliant portfolios . Lubrizol's USD 20 million acrylic-emulsion expansion in Gastonia supports demand clusters in home textiles and technical performance fabrics for automotive interiors, reinforcing the region's tilt toward value-added niches. Canada's integration with US vehicle production sustains cross-border demand, though exposure to raw-material price cycles forces constant recalibration of sourcing strategies.

Europe sustains leadership in sustainable chemistry and advanced processing. German, French, and Nordic innovators push waterborne polyurethane and bio-polymer frontiers while investing in plasma and digital-application lines that dramatically cut water and energy inputs. Acquisitions such as Freudenberg's EUR 100 million takeover of Heytex assets expand technical-textile portfolios and signal ongoing consolidation. EU circular-economy legislation accelerates interest in recyclable coatings and closed-loop infrastructures, positioning the textile coatings market as both beneficiary and enabler of regional climate objectives.