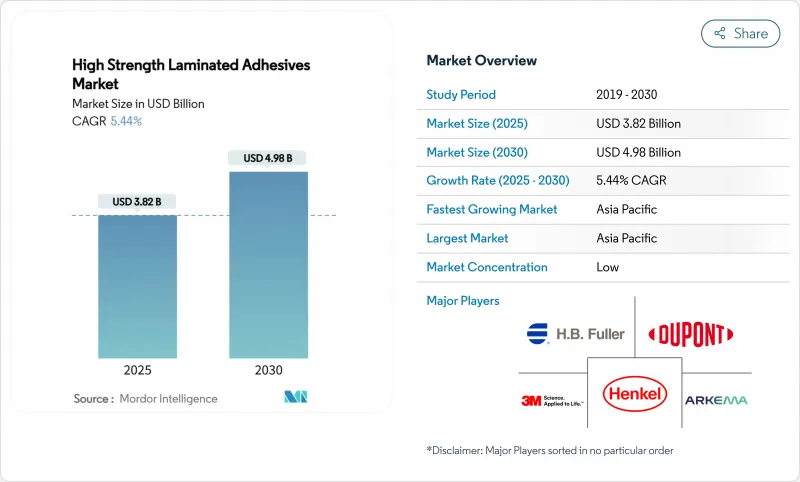

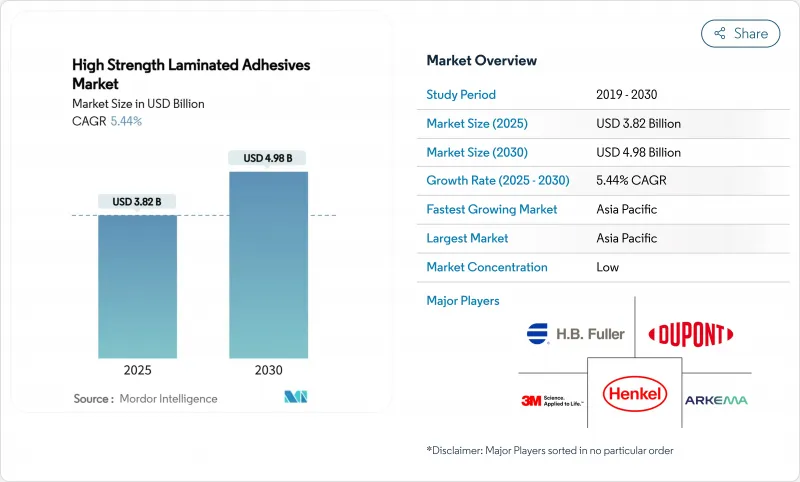

고강도 라미네이트 접착제 시장 규모는 2025년에 38억 2,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.44%를 나타낼 것으로 예측되며 2030년에 49억 8,000만 달러에 이를 것으로 예측됩니다.

환경 규제가 강화되고 있음에도 불구하고, 탄탄한 연포장 수요, 가속화되는 자동차 경량화 및 급속한 전자제품 소형화로 시장 성장세는 확고히 유지되고 있습니다. 생산업체들은 저휘발성 유기화합물(VOC) 화학물질 도입, 바이오 기반 원료 개발 및 아시아태평양 지역 생산 현지화를 서두르며 증가하는 다운스트림 생산량을 확보하려 하고 있습니다. 다우(Dow)의 연포장용 라미네이팅 접착제 사업부 매각과 같은 전략적 매각 사례는 원자재 가격 변동성이 마진을 압박하는 가운데 고부가가치 틈새 시장을 중심으로 산업이 효율화되고 있음을 보여줍니다. UV 경화형 및 수성 시스템으로의 기술 전환이 가속화되고 있지만, 용매 기반 제품이 여전히 핵심 고성능 라미네이션 시장을 주도하며 시장이 전환기에 있음을 시사합니다. 1차 공급업체 간 통합은 변환업체 및 자동차 공장 인근에 공급망을 구축한 지역 전문업체들의 장기적 존재로 인해 완화되고 있습니다.

브랜드 소유주들의 두께 감소(down-gauging) 및 소비자 편의성 추구로 연포장재 사용량은 지속적으로 증가하고 있습니다. 해당 부문은 2028년까지 3,416억 달러 규모로 성장할 전망이며, 고성능 접착 시스템에 의존하는 다층 라미네이트 생산량을 끌어올릴 것입니다. 유럽 그린딜(European Green Deal)에 따라 의무화된 단일 소재 파우치 및 재활용 가능 차단 필름은 폐쇄형 재활용과 호환되는 접착제를 요구하여 제품 제형 개발사들에게 프리미엄 틈새 시장을 열어주고 있습니다. 전자상거래가 시급성을 더하고 있으며, 팩사이즈(Packsize)와 헨켈(Henkel)은 에코팍스(Eco-Pax) 바이오 기반 핫멜트 솔루션을 사용했을 때 3억 4천만 개의 배송 상자에서 온실가스 배출량을 32% 감축했다고 보고했습니다. 식품 접촉 안전성, 낮은 이주성 및 탈잉크 분리 성능을 인증할 수 있는 공급업체들은 라미네이팅 접착제 시장에서 가격 경쟁력을 확보합니다.

현대 자동차는 20년 전 30피트에 불과했던 접착제 사용량이 평균 400피트 이상으로 증가하며, 리벳과 용접에서 접착 라인으로의 구조적 전환을 보여줍니다. 혼합 소재 차체(화이트 바디), 배터리 팩 캡슐화, 소음 감쇠 라미네이트는 모두 전단 강도와 열순환 내구성에 대한 기술적 기준을 높입니다. 멕시코 자동차 산업은 국가 GDP의 6%를 차지하며 13% 생산 증가를 목표로 하고 있어 북미 공급망 내 지역 수요를 확대하고 있습니다. OEM 업체들이 분해 용이성과 수명 종료 후 재활용을 우선시함에 따라 열가소성 폴리우레탄 제형의 점유율이 증가하고 있습니다.

원자재 가격 변동성은 적층 접착제 제조업체에 지속적인 압박 요인으로 작용하고 있으며, BASF는 2025년 4월부터 1,4-부탄디올 및 N-메틸피롤리돈을 포함한 주요 폴리우레탄 전구체에 대해 파운드당 0.08-0.10달러의 가격 인상을 시행할 예정입니다. 복합재 제조업체의 79%가 수지 부족을 호소하며, 이로 인해 제형 개발사들은 예측 불가능한 납기 기간에 노출되고 있습니다. 석유 의존도는 폴리우레탄 원료가 원유 가격 변동에 묶여 있게 하는 반면, 바이오 기반 원료는 규모가 제한적입니다. 공급업체들은 분기별 가격 조항과 이중 공급 전략으로 대응하고 있지만, 불확실성은 여전히 라미네이팅 접착제 시장의 마진 확대를 저해하고 있습니다.

폴리우레탄(PU)은 2024년 글로벌 매출의 43.18%를 차지하며, 고탄성 파우치 라미네이션과 내구성 있는 자동차 내장재에서의 다용도성을 입증했습니다. 이 부문는 2030년까지 연평균 6.41%의 성장률을 기록할 것으로 예상되며, 변환업체들이 이질적 기질 간 강력한 접착력을 선호함에 따라 라미네이션 접착제 시장에서의 선두 위치를 유지할 전망입니다. 이소시아네이트에 대한 규제 압박으로 인해 유해성 표시를 줄이면서도 접착 강도를 유지하는 비이소시아네이트 폴리우레탄(PU) 및 바이오 기반 폴리올 공정으로의 전환이 가속화되고 있습니다.

리그닌, 대두, 피마자 유래 전구체를 활용한 바이오 함량이 증가하며 부분적으로 재생 가능한 폴리우레탄 사슬이 가능해지고 있습니다. 연구 결과 기존 등급과 동등한 가수분해 저항성을 유지하는 비이소시아네이트 폴리우레탄(NIPU) 합성에 성공한 사례가 확인되었습니다. 아크릴계 시스템은 광학 투명도와 고속 생산이 핵심인 자외선(UV) 경화형 전자 부품 적층 분야에서 점유율을 확대하고 있습니다. 에폭시는 극한의 화학적 안정성이 요구되는 항공우주 및 풍력 블레이드 직물 분야의 틈새 시장을 계속해서 차지하고 있으나, 상대적 시장 점유율은 여전히 미미한 수준입니다. 전반적으로 폴리우레탄 분야의 혁신은 적층 접착제 시장을 저탄소이면서도 고성능 솔루션으로 나아가게 하고 있습니다.

아시아태평양 지역은 2024년 글로벌 수요의 44.18%를 차지했으며, 화학 클러스터 투자와 1인당 포장 제품 소비 증가에 힘입어 2030년까지 연평균 6.04%의 성장률을 보일 것으로 예상됩니다. 중국의 변환기 업체와 인도의 신규 록타이트 공장을 포함한 지역 거대 기업들은 다국적 기업을 위해 공급을 현지화하고 리드 타임을 단축하며 통화 위험을 줄입니다.

북미는 자동차 경량화와 식품 접촉 안전 기준이 혁신을 주도하는 고부가가치 시장으로 남아 있습니다. 루브리졸의 노스캐롤라이나주 2,000만 달러 규모 아크릴 에멀젼 확장 프로젝트는 특수 등급 제품에 대한 지속적인 생산 능력 강화를 보여줍니다.

유럽의 엄격한 배출 규제는 기술 전환을 촉진하고 재활용 가능 라미네이션을 우선시하는 생산자 책임 제도를 확대하여 지역 제형사들을 저모노머 폴리우레탄 및 수성 레시피로 몰아넣고 있습니다. 라틴 아메리카와 중동은 낮은 기반에서 출발하지만 산업화 프로젝트와 소비자 지출 증가와 연계된 신흥 수요 거점을 제시합니다. 지역별 분할 분석은 라미네이팅 접착제 시장에서의 성공에 있어 다운스트림 포장업체 및 자동차 제조업체와의 근접성이 여전히 결정적임을 보여줍니다.

The High Strength Laminated Adhesives Market size is estimated at USD 3.82 billion in 2025, and is expected to reach USD 4.98 billion by 2030, at a CAGR of 5.44% during the forecast period (2025-2030).

Robust flexible-packaging demand, accelerating automotive lightweighting and rapid electronics miniaturization keep the market firmly on a growth track despite tighter environmental rules. Producers are racing to introduce low-VOC chemistries, develop bio-based feedstocks and localize production in Asia-Pacific to capture rising downstream output. Strategic divestments, such as Dow's sale of its flexible-packaging laminating adhesives line, illustrate an industry streamlining around high-value niches while raw-material volatility pressures margins. Technology migration toward UV-curable and water-borne systems is gathering pace, yet solvent-based products still dominate critical high-performance laminations, highlighting a market in transition. Consolidation among tier-one players is tempered by a long tail of regional specialists that anchor supply close to converters and car plants.

Flexible packaging volumes keep rising as brand owners pursue down-gauging and consumer convenience. The sector is projected to hit USD 341.6 billion by 2028, lifting multilayer laminate output that relies on high-performance bonding systems . Mono-material pouches and recyclable barrier films mandated under the European Green Deal require adhesives compatible with closed-loop recycling, opening premium niches for product formulators. E-commerce adds urgency, with Packsize and Henkel reporting a 32% greenhouse-gas cut across 340 million shipper boxes when using Eco-Pax bio-based hot-melt solutions. Suppliers able to certify food-contact safety, low migration and de-inking debonding gain a pricing edge in the laminating adhesives market.

Modern vehicles average more than 400 linear feet of adhesive versus 30 feet two decades ago, underscoring the structural shift from rivets and welds to bonding lines . Mixed-material bodies in white, battery-pack encapsulation and noise-damping laminates all raise the technical bar for shear strength and thermal-cycling durability. Mexico's auto sector, contributing 6% to national GDP, is on track for 13% production growth, amplifying localized demand in North American supply corridors. Thermoplastic polyurethane formulations gain share as OEMs prioritize dismantlability and end-of-life recycling.

Raw material price volatility continues to pressure laminating adhesives manufacturers, with BASF implementing price increases of USD 0.08-0.10 per pound for key polyurethane precursors including 1,4-Butanediol and N-Methylpyrrolidone effective April 2025. Seventy-nine percent of composites fabricators cite resin shortages, exposing formulators to unpredictable lead times. Petroleum dependency keeps polyurethane inputs tethered to crude swings, while bio-based feedstocks face limited scale. Suppliers respond with quarterly pricing clauses and dual-sourcing strategies, yet the uncertainty still trims margin expansion in the laminating adhesives market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyurethane (PU) claimed 43.18% of global revenue in 2024, underscoring its versatility in high-flexibility pouch laminations and resilient automotive interior skins. The segment is projected to grow at a 6.41% CAGR through 2030, keeping its lead in the laminating adhesives market as converters favor robust adhesion across heterogeneous substrates. Regulatory pressure on diisocyanates accelerates migration to non-isocyanate polyurethane (PU) and bio-based polyol routes that curb hazard labeling without sacrificing bond strength.

Bio-content gains momentum with lignin-, soy-, and castor-derived precursors enabling partially renewable polyurethane chains. Research demonstrates successful Non-Isocyanate Polyurethane (NIPU) syntheses that retain hydrolysis resistance equal to incumbent grades. Acrylic systems pick up share in ultraviolet (UV)-curable electronics laminations where optical clarity and rapid line speed are paramount. Epoxies continue to serve niche aerospace and wind-blade fabrics demanding extreme chemical stability, yet their relative market slice stays modest. Overall, innovation in polyurethane keeps the laminating adhesives market moving toward lower-carbon yet high-performance solutions.

The High Strength Laminating Adhesives Market Report is Segmented by Resin Type (Polyurethane, Acrylic, Epoxy, Other Resin Types), Technology (Water-Borne, Solvent-Based, Hot-Melt, UV-Curable), Application (Packaging, Automotive, Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 44.18% of global demand in 2024 and is anticipated to expand at a 6.04% CAGR through 2030, fueled by chemical cluster investment and rising per-capita packaged-goods consumption. Regional heavyweights, including China's converters and India's new Loctite plant, localize supply, shorten lead times and cut currency risk for multinationals.

North America remains a high-value arena where automotive lightweighting and food-contact safety standards steer innovation. Lubrizol's USD 20 million acrylic-emulsion expansion in North Carolina illustrates continued capacity reinforcement for specialty grades.

Europe's stringent emission rules catalyze technology pivots and extend producer-responsibility schemes that prioritize recycle-ready laminations, pushing regional formulators into low-monomer polyurethane and water-borne recipes. Latin America and the Middle East present emergent demand nodes linked to industrialization projects and consumer spending catch-up, albeit from lower bases. The geography split shows that proximity to downstream packagers and automakers remains decisive for success in the laminating adhesives market.