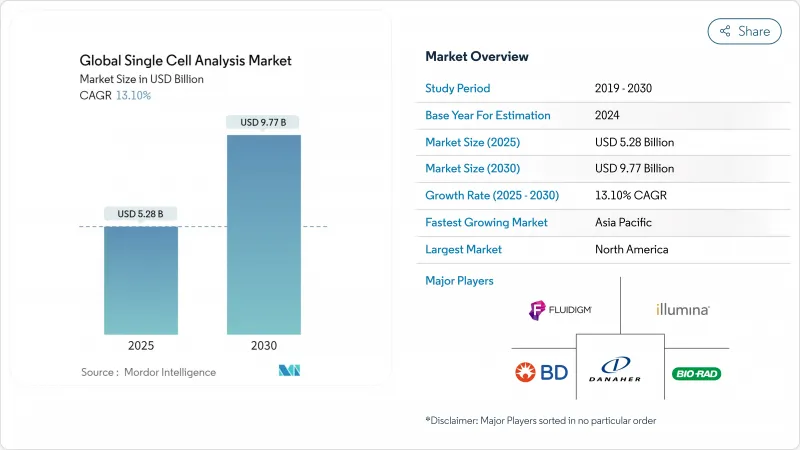

단일세포 분석 시장은 2025년 52억 8,000만 달러로 평가되었고, 2030년에 97억 7,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 13.10%를 나타낼 전망입니다.

정밀의학 프로그램 확대, 암 및 자가면역질환 부담 증가, 정부 및 벤처 캐피털의 적극적인 자금 지원이 두 자릿수 성장을 지속시키고 있습니다. 단일세포 멀티오믹스, AI 기반 생물정보학, 공간 전사체학 분야의 급속한 발전은 새로운 임상 및 연구 활용 사례를 창출하고 있으며, 반복적인 소모품 판매는 공급업체에게 예측 가능한 현금 흐름을 유지시켜 줍니다. 대형 장비 기업과 특화된 혁신 기업 간의 전략적 통합은 통합 워크플로우 도입을 가속화하고 있으며, 지역별 규제 프레임워크는 단일세포 판독값 기반 진단 검사를 수용하기 시작했습니다.

임상 프로그램은 대량 오믹스 접근법의 한계를 극복하기 위해 세포 이질성 해결에 단일세포 기술을 점점 더 의존하고 있습니다. 종양학 분야가 이러한 변화를 보여줍니다. 단일세포 RNA 시퀀싱은 내성 종양 클론을 식별하고 면역요법 선택을 정교화하여 반응 예측 정확도를 35% 향상시키고 있습니다. 주요 암 센터 전반에 걸쳐 일상적인 워크플로에의 통합이 증가함에 따라 단일세포 분석 시장은 지속적인 장기 수요를 확보하고 있습니다.

단일세포 해상도에서 게놈, 전사체, 단백체 분석을 결합하는 스타트업에 대한 벤처 투자는 2024년 500억 달러를 넘어섰다. 단일세포에서 DNA, RNA, 단백질 패널을 동시에 제공하는 플랫폼은 바이오마커 발견 및 환자 계층화 파이프라인을 가속화하여 단기 상업적 채택을 강화하고 있습니다.

고급 공간 오믹스 장비는 종종 50만 달러 이상이며, 연간 서비스 계약은 소유 비용의 10-15%를 추가합니다. 샘플당 500-2,000달러에 달하는 높은 소모품 가격은 특히 라틴 아메리카, 아프리카 및 동남아시아 일부 지역에서 자금력이 풍부한 센터 외부의 도입을 제한합니다.

소모품 부문은 실험실에서 일상적인 워크플로우에 필수적인 시약, 칩 및 분석 키트를 반복적으로 구매함에 따라 2024년 매출의 58.12%를 차지했습니다. 라이브러리 준비 시약에 대한 지속적인 수요는 예측 가능한 수익을 보장하고 장비 예산의 거시경제적 변동에 대한 민감도를 낮춥니다. 기기 판매는 규모는 작지만, 단일 실행으로 멀티오믹스 판독값을 결합하는 신제품 출시로 인해 14.50%의 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 고처리량 처리를 간소화하는 자동 액체 처리 및 로봇 공학 모듈도 자본 장비의 매력을 높이고 있습니다.

소모품 제조업체들은 시약과 소프트웨어 및 기술 지원을 결합한 통합 워크플로 번들로 전환하며 고객 락인을 강화하고 있습니다. 광범위한 포트폴리오를 보유한 기업들은 교차 판매 이점을 확보하는 반면, 틈새 시약 공급업체들은 종합 솔루션 제공을 위한 파트너십을 모색하고 있습니다. 공간 오믹스 및 DNA-RNA-단백질 복합 분석기가 시제품 단계에서 상용화 단계로 진입함에 따라 단일세포 분석 장비 시장 규모는 급속히 확대될 전망입니다.

유세포 분석기는 임상 면역학, 이식, 혈액암 연구실에서의 확고한 입지를 바탕으로 2024년 매출 점유율 34.45%를 유지했습니다. 지속적인 검출기 및 형광체 업그레이드로 40개 이상의 매개변수 패널이 가능해져 활용도가 높아지고 있습니다. 차세대 시퀀싱은 기가베이스당 비용 하락과 세포 바코딩 화학 기술이 고함량 전사체 프로파일링을 가능케 하면서 13.70%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 기술입니다. 단일세포 분석 시장에서는 PCR, 현미경 검사, 질량 분석법, 마이크로플루이딕스, RNA-FISH가 각자의 전문 영역을 차지하고 있습니다. 질량 분석 기반 단일세포 단백질체학은 전사체에서 단백질로의 간극을 메우고 있으며, 공간 전사체학은 이미징과 시퀀싱을 결합해 미세환경에 대한 인사이트을 제공합니다.

북미는 2024년 매출의 42.19%를 차지했으며, 이는 NIH 자금 지원, 밀집된 암 센터 네트워크, 그리고 Thermo Fisher Scientific, Illumina, 10x Genomics 등 글로벌 시장 선도 기업의 본사 소재지라는 점에 힘입었습니다. FDA가 실험실 개발 단일세포 진단법과 협력함으로써 규제 명확성이 증진되고 있습니다. 학계 의료 시스템과 산업 간의 지역적 협력이 전환 연구 파이프라인을 가속화하고 있습니다. 분자 진단에 대한 보험 적용이 확대됨에 따라 북미의 단일세포 분석 시장 규모는 지속적으로 성장할 것으로 예상됩니다.

아시아태평양 지역은 2030년까지 14.50%의 가장 빠른 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 중국의 정밀의학 추진, 일본의 공학적 강점, 인도의 확장 중인 바이오테크 산업이 수요를 뒷받침합니다. 국가 연구 보조금과 체외 검사(IVD)에 대한 유리한 승인 절차는 소모품 및 장비의 현지 생산을 촉진하고 있습니다. 지역 정부들은 데이터 관리 수요에 대응하기 위해 클라우드 인프라에도 투자 중입니다.

유럽은 독일, 영국, 프랑스가 주도하는 상당한 시장 점유율을 유지하고 있습니다. ‘호라이즌 유럽’ 보조금은 다기관 연구를 촉진하는 반면, 체외진단규정(IVDR)은 성능 입증 요건을 강화하여 제품 설계에 영향을 미치고 있습니다. 중동 및 남미 지역의 규모는 작지만 점진적인 채택은 의료 현대화 및 유전체 감시 프로그램의 확대를 반영합니다. 비용 장벽과 인력 부족 문제 해결 여부가 이들 신흥 지역의 도입 속도를 결정할 것입니다.

The single cell analysis market is valued at USD 5.28 billion in 2025 and is forecast to climb to USD 9.77 billion by 2030, registering a 13.10% CAGR over the period.

Expanding precision-medicine programs, a widening cancer and autoimmune disease burden, and active government and venture capital funding are sustaining double-digit growth. Rapid advances in single-cell multi-omics, AI-enabled bioinformatics, and spatial transcriptomics are opening new clinical and research use cases, while recurring consumables sales maintain predictable cash flows for suppliers. Strategic consolidation among large instrumentation firms and focused innovators is accelerating integrated workflow rollouts, and region-specific regulatory frameworks are beginning to accommodate diagnostic assays based on single-cell readouts.

Clinical programs increasingly rely on single-cell technologies to resolve cellular heterogeneity that limits bulk-omics approaches. Oncology illustrates the shift: single-cell RNA sequencing is identifying resistant tumor clones and refining immunotherapy selection, driving 35% gains in response-prediction accuracy . Growing integration into routine workflows across major cancer centers positions the single cell analysis market for sustained long-term demand.

Venture investment in startups that combine genomic, transcriptomic, and proteomic readouts at single-cell resolution surpassed USD 50 billion in 2024. Platforms delivering simultaneous DNA, RNA, and protein panels from a single cell are accelerating biomarker discovery and patient-stratification pipelines, reinforcing near-term commercial uptake.

Advanced spatial-omics instruments often list above USD 500,000, with annual service contracts adding 10-15% of ownership cost. High consumable prices, ranging USD 500-2,000 per sample, limit adoption outside well-funded centers, especially in Latin America, Africa, and parts of Southeast Asia .

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The consumables segment accounted for 58.12% of 2024 revenue as laboratories repeatedly purchase reagents, chips, and assay kits essential for routine workflows. Continuous demand for library-prep reagents anchors predictable income and lowers sensitivity to macroeconomic swings in instrumentation budgets. Instrument sales, although a smaller base, are projected to grow 14.50% CAGR owing to launches that combine multi-omic readouts in single runs. Automated liquid-handling and robotics modules that streamline high-throughput processing are also raising capital-equipment appeal.

Consumable manufacturers are pivoting toward integrated workflow bundles that pair reagents with software and technical support, deepening customer lock-in. Broad-portfolio firms capture cross-selling advantages, whereas niche reagent suppliers seek partnerships for full-solution offerings. The single cell analysis market size for instruments is set to expand rapidly as spatial-omics and combined DNA-RNA-protein analyzers move from prototype to commercial release.

Flow cytometry retained 34.45% revenue share in 2024 on the strength of established adoption in clinical immunology, transplantation, and blood-cancer labs. Continuous detector and fluorophore upgrades permit 40-plus-parameter panels, bolstering utility. Next-generation sequencing is the fastest-growing technique, forecast at 13.70% CAGR, as falling per-gigabase costs and cell-barcoding chemistries unlock high-content transcriptomic profiling. The single cell analysis market sees PCR, microscopy, mass spectrometry, microfluidics, and RNA-FISH occupying specialized niches. Mass-spectrometry-based single-cell proteomics is bridging transcript-to-protein gaps, while spatial transcriptomics combines imaging with sequencing to add microenvironment insights.

The Single Cell Analysis Market Report Segments the Industry Into by Product (Consumables and Instruments), Technique (Flow Cytometry, and More), Cell Type (Human Cells and More), Workflow Step (Sample Preparation, and More), Application (Research Applications, Medical Applications), End User (Academic and Research Laboratories, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America contributed 42.19% revenue in 2024, supported by NIH funding, a dense network of cancer centers, and headquarters of global market leaders such as Thermo Fisher Scientific, Illumina, and 10x Genomics. FDA engagement with lab-developed single-cell diagnostics is fostering regulatory clarity. Regional collaborations between academic health systems and industry accelerate translational pipelines. The single cell analysis market size in North America is expected to keep expanding as reimbursements for molecular diagnostics broaden.

Asia-Pacific is forecast to post the fastest 14.50% CAGR through 2030. China's precision-medicine initiatives, Japan's engineering strengths, and India's expanding biotech sector underpin demand. National research grants and favorable approval pathways for in-vitro tests are catalyzing local production of consumables and instruments. Regional governments are also investing in cloud infrastructure to cope with data-management demands.

Europe maintains a sizeable share led by Germany, the United Kingdom, and France. Horizon Europe grants fuel multi-center research, while the In-Vitro Diagnostic Regulation tightens performance-evidence requirements, influencing product designs. Smaller but growing adoption in the Middle East and South America reflects increasing healthcare modernization and genome-surveillance programs. Addressing cost barriers and workforce gaps will determine uptake pace across these emerging territories.