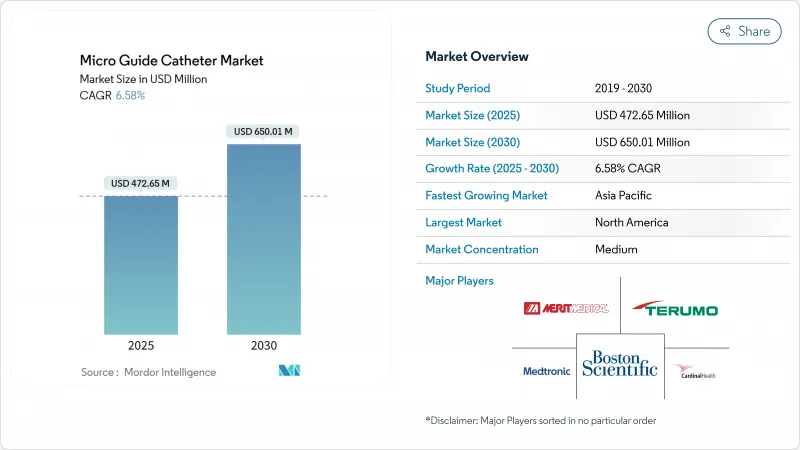

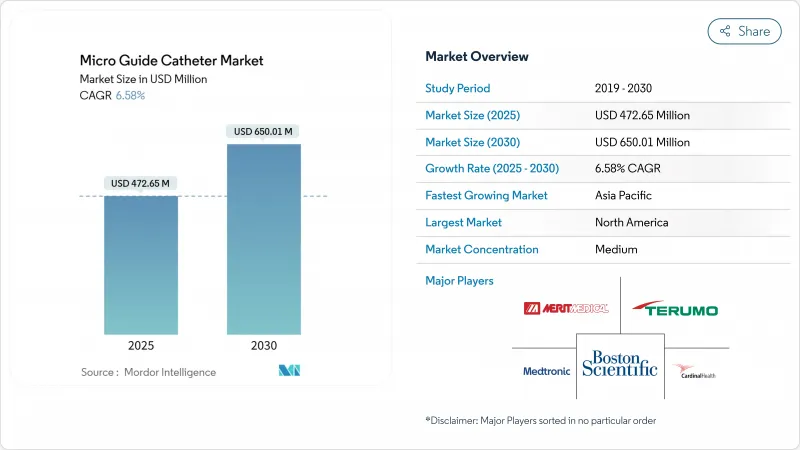

마이크로 가이드 카테터 시장 규모는 2025년에 4억 7,265만 달러로 평가되었고, 2030년에 6억 5,001만 달러에 이를 것으로 예측되며, CAGR은 6.58%를 나타낼 전망입니다.

수요가 증가하는 이유는 고령 인구가 더 많은 중재적 시술을 필요로 하고, 기기 설계에 조종성과 압력 감지 기능이 통합되었으며, 정책 입안자들이 일상적인 혈관성형술과 단순 신경혈관 시술을 입원 환자용 수술실에서 비용 절감형 외래 환경으로 계속 전환하고 있기 때문입니다. 심혈관 질환은 현재 미국 성인 1억 2,790만 명에게 영향을 미치며, 병원으로 하여금 중증 석회화 병변을 통과할 수 있는 이중 루멘 및 잠금식 디자인에 의존하는 만성 완전폐색(CTO) 프로그램을 확대하도록 촉진하고 있습니다. 신경 분야에서는 기계적 혈전제거술 지침이 말단 부위로의 신속한 접근을 권장하며, 컴퓨터 지원 성형 알고리즘이 96%의 첫 시술 성공률을 제공하여 시술 시간과 형광투시 검사를 줄입니다. 보스턴 사이언티픽의 실크로드 메디컬 인수(12억 6,000만 달러)와 같은 OEM 간 통합은 연구개발 규모 확대와 폴리머 공급 안정화를 가져왔으나, 지속적인 PTFE 부족과 수지 공장 가동 중단으로 부품 확보가 어려워지고 있습니다.

심혈관 질환은 미국에 연간 4,223억 달러의 직접 비용을 부과하며, 생활습관 위험 요인과 고령화 인구 구조가 맞물리면서 계속 증가하고 있습니다. 동일한 패턴이 아시아태평양 지역에서도 나타나고 있으며, 홍콩은 치료에 46억 달러, 싱가포르는 81억 달러를 지출하여 정부가 중재적 치료 프로그램을 보조하도록 촉구하고 있습니다. 뇌졸중 발생률 증가로 더 많은 신경과 전문의가 카테터 기술을 습득하고 있으며, 다학제적 뇌졸중 팀은 마이크로 가이드 카테터의 토크 반응성과 팁 유연성에 의존하는 혈전제거술을 사상 최대 규모로 시행하고 있습니다. 이러한 요소들이 결합되어 마이크로 가이드 카테터 시장의 장기적 수요를 유지하고 있습니다.

임상계는 고위험 노인 환자에게 TAVR(경피적 대동맥판막 치환술)과 같은 덜 침습적인 해결책을 선호합니다. 소형 고리에서 자가팽창형 판막은 복합 종료점 9.4%를 기록한 반면 풍선팽창형 플랫폼은 10.6%를 나타냈습니다. 증가하는 구조적 심장 질환 사례는 폐쇄 장치 위치를 최적화하기 위해 정밀한 압력 피드백이 가능한 미세 카테터가 필요합니다. 컴퓨터 유도 성형 소프트웨어는 첫 시술 실패율을 34%에서 4%로 낮추며, 형광 투시 검사 시간을 단축하고 시술자의 피로를 줄입니다. 동일한 디지털 도구는 접근 속도가 신경학적 기능을 좌우하는 뇌졸중 시스템에도 적용되어, 마이크로 가이드 카테터 시장 성장에 의미 있는 호재로 작용합니다.

퇴직하는 심장 전문의 2명당 신규 진입자는 단 1명에 불과하여, 많은 병원에서 시술실 처리량이 제한되고 있습니다. 보상금이 정체된 반면 사례 복잡성은 증가하면서 번아웃 비율이 급증했습니다. 경력 초반 의사들은 예측 사망률이 높은 사례를 처리해야 하므로 학습 곡선을 단축하고 자신감을 높여주는 직관적인 카테터의 필요성이 더욱 부각됩니다. 농촌 지역이 가장 큰 부족을 겪고 있으며, 병원들은 환자를 수백 마일 떨어진 곳으로 이송하여 치료를 지연시키고 의료 서비스가 부족한 지역의 마이크로 가이드 카테터 시장 기기 수요를 압박합니다.

오버더와이어(OTW) 구성은 2024년 매출의 65.35%를 차지했으며, 의료진은 장시간 풍선 팽창 및 스텐트 삽입 시 점진적 지원 기능을 계속 선호하고 있습니다. 이 카테고리는 확고한 임상적 친숙도로 CTO 프로토콜의 중심을 유지하고 있으나, 특히 비외상성 원위 접근을 중시하는 신경혈관 분야에서 유동 디렉티드 시스템이 연평균 7.57% 성장률로 점유율을 확대하고 있습니다. 보스턴 사이언티픽의 레니게이드 HI-FLO는 경쟁사 대비 36.8% 낮은 힘과 7% 높은 유량을 기록하며 설계 개선을 입증했습니다. 조종 가능한 샤프트는 와이어 교체를 줄여 실험실에서 형광 투시 및 조영제 사용을 절감하는 데 기여합니다.

혁신은 와이어 또는 마이크로코일 동시 전달을 용이하게 하는 이중 루멘 및 삼중 루멘 형태로 집중되고 있습니다. 고어의 삼중 루멘 설계는 최대 4개의 와이어를 처리하여 천공형 이식편 삽입을 단순화합니다. 압력 감지 루멘은 통합 생리학적 평가를 약속하지만, 분획 유량 예비량 정확도에서 전용 와이어보다 0.03 단위 뒤처지는 보정 한계로 인해 여전히 틈새 시장입니다. 수지 공급업체의 생산 능력 안정화에 따라 제조사들은 조종성, 모듈성, 저프로파일 원위 샤프트를 차세대 라인에 통합하여 마이크로 가이드 카테터 시장이 다목적 하이브리드로의 전환을 지속하도록 할 계획입니다.

북미는 포괄적인 보험 적용 범위, 높은 실험실 밀도, 정밀 내비게이션 기능의 빠른 도입을 바탕으로 2024년 매출의 42.81%를 차지합니다. 미국 의료진은 연간 50만 건 이상의 PCI 시술을 수행하며, 이 중 29%는 마이크로카테터 통과율을 높이는 CTO(완전 폐쇄) 기술을 포함합니다. 캐나다는 허브 앤 스포크 방식을 채택하여 지역 병원이 복잡한 환자를 학술 센터로 이송함으로써 전국적인 기기 회전율을 높입니다. 압력 감지 카테터에 대한 환급은 여전히 유리하며, CMS는 외래 환자 청구서에 기록될 경우 사용당 추가로 989달러를 지급합니다.

아시아태평양 지역은 2030년까지 연평균 8.45%의 성장률을 보일 것으로 예상되며, 마이크로 가이드 카테터 시장의 점진적 성장을 주도할 핵심 지역이 될 것입니다. 중국은 매년 250개 이상의 카테터실(Cath Lab)을 신설하며, 물량 기반 조달 입찰 제도로 인해 국내 기업들은 상품 가격 상한선을 피하기 위해 조종 가능한 말단 팁과 같은 차별화된 틈새 시장으로 진출하고 있습니다. 일본은 고령화 사회와 보편적 의료 보장 제도를 바탕으로 다음으로 성장할 전망이며, 신개념 신경 혈전 제거 도구에 대한 중립적 보상 정책이 조기 도입을 가속화하고 있습니다. 베트남과 같은 동남아시아 경제권은 의료기기 성장률이 두 자릿수를 기록하고 있으나, 정교한 마이크로 가이드 카테터는 수입에 의존하고 있습니다. 2021년부터 2024년 사이 현지 임상시험 참여는 65% 증가하여 국내 등록 절차를 가속화했습니다.

유럽은 독일, 프랑스, 영국을 중심으로 안정적인 중단위 성장률을 보입니다. EU 의료기기 규정(MDR)은 승인 주기를 연장하지만 인식된 안전성을 높여 의료진의 신뢰를 뒷받침합니다. 라틴아메리카의 분산된 지불자 구조는 물량 증가를 제한하지만, 브라질의 5,900만 달러 규모 혈관 기기 시장은 민간 병원을 겨냥한 프리미엄 카테터의 발판을 마련합니다. 사우디아라비아 같은 중동 허브는 ‘비전 2030’ 계획 하에 심장 전문 센터에 투자하며, 영상 장비와 일회용 제품을 묶어 구매하는 조달 계약을 창출하고 있습니다.

The micro guide catheters market size reached USD 472.65 million in 2025 and is projected to climb to USD 650.01 million by 2030, advancing at a 6.58% CAGR.

Demand is rising because aging populations need more interventional procedures, device designs now integrate steerability and pressure-sensing, and policy makers continue to shift routine angioplasty and simple neurovascular work from inpatient suites to cost-saving ambulatory settings. Cardiovascular disease now affects 127.9 million U.S. adults, spurring hospitals to expand chronic total occlusion (CTO) programs that rely on dual-lumen and locking designs able to cross heavily calcified lesions. On the neuro side, mechanical thrombectomy guidelines recommend faster access to distal territories, and computer-assisted shaping algorithms deliver 96% first-trial success, reducing procedure time and fluoroscopy. Consolidation among OEMs, such as Boston Scientific's USD 1.26 billion purchase of Silk Road Medical, adds scale for R&D and secures polymer supply, yet persistent PTFE shortages and resin plant outages hinder component availability.

Cardiovascular disease imposes USD 422.3 billion in direct costs annually on the United States and continues to rise as lifestyle risk factors intersect with aging demographics. The same pattern is unfolding across Asia-Pacific, where Hong Kong spends USD 4.6 billion and Singapore USD 8.1 billion on treatment, prompting governments to subsidize interventional programs. Increasing stroke incidence means more neurologists are training in catheter skills, and multi-disciplinary stroke teams now perform a record number of thrombectomies that depend on micro guide catheter torque response and tip flexibility. Together, these factors sustain long-run demand in the micro guide catheters market.

The clinical community favors less invasive solutions such as TAVR for high-risk elderly patients; self-expanding valves posted a 9.4% combined endpoint versus 10.6% for balloon-expandable platforms in small annuli. Higher volumes of structural heart cases require microcatheters with precise pressure feedback to optimize closure device positioning. Computer-guided shaping software lowers first-pass failure from 34% to 4%, trimming fluoroscopy seconds and operator fatigue. The same digital tools inform stroke systems, where speed of access dictates neurological function, thus creating a meaningful tail-wind for micro guide catheters market growth.

Only one new cardiologist enters the workforce for every two that retire, limiting lab throughput in many hospitals . Burnout rates have escalated because reimbursement stagnates while case complexity rises. Early-career physicians contend with higher predicted mortality caseloads, reinforcing the need for intuitive catheters that shorten learning curves and improve confidence. Rural regions feel the shortfall most; hospitals ship patients hundreds of miles, delaying treatment and compressing demand for micro guide catheters market devices in underserved areas.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Over-the-wire configurations held 65.35% of revenue in 2024 as operators continue to favor their incremental support during prolonged balloon inflations and stent delivery. This category's entrenched clinical familiarity keeps it at the center of CTO protocols, yet flow-directed systems are picking up pace at a 7.57% CAGR, particularly in neurovascular circles that value atraumatic distal access. Boston Scientific's Renegade HI-FLO exemplifies design gains, posting 36.8% lower force and 7% higher flow than peers . Steerable shafts reduce wire exchanges, helping labs trim fluoroscopy and contrast.

Innovation converges on dual-lumen and tri-lumen form factors that facilitate simultaneous wire or microcoil delivery. Gore's tri-lumen design handles up to four wires, simplifying fenestrated graft placement. Pressure-sensing lumens promise integrated physiological assessment but remain niche due to calibration limits that trail dedicated wires by 0.03 units in fractional-flow reserve accuracy. As resin suppliers stabilize capacity, manufacturers aim to merge steerability, modularity, and low-profile distal shafts into next-gen lines, ensuring the micro guide catheters market continues its shift toward versatile hybrids.

The Micro Guide Catheters Market Report is Segmented by Product Type (Over-The-Wire Micro Guide Catheters, Flow-Directed Micro Guide Catheters), Application (Cardiovascular, Neurovascular, Others), End User (Hospitals & Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America anchors 42.81% of 2024 revenue on the strength of comprehensive insurance coverage, high lab density, and rapid adoption of precision navigation features. U.S. operators perform more than 500,000 PCI cases annually, with 29% involving CTO techniques that elevate microcatheter pull-through rates. Canada adopts a hub-and-spoke approach where community hospitals send complex patients to academic centers, increasing national device turnover. Reimbursement for pressure-sensing catheters remains favorable, with CMS paying an extra USD 989 per use when documented in outpatient claims.

Asia-Pacific, projected at an 8.45% CAGR through 2030, will be the swing territory for incremental gains in the micro guide catheters market. China opens more than 250 cath labs each year, and its volume-based-procurement tenders push domestic firms toward differentiated niches like steerable distal tips to escape commodity price ceilings. Japan advances next as an aging society with universal coverage; its neutral reimbursement for novel neuro thrombectomy tools accelerates early adoption. Southeast Asian economies such as Vietnam log double-digit medical device growth rates, though they rely on imports for sophisticated micro guide catheters. Local clinical trial participation increased 65% between 2021 and 2024, enabling faster in-country registrations.

Europe presents stable mid-single-digit expansion fueled by Germany, France, and the UK. The EU Medical Device Regulation (MDR) lengthens approval cycles but raises perceived safety, supporting clinician confidence. Latin America's fragmented payer mix tempers volume, yet Brazil's USD 59 million vascular device market sets a foothold for premium catheters targeting private hospitals. Middle East hubs like Saudi Arabia invest in cardiac centers of excellence within Vision 2030, creating procurement contracts that often bundle imaging hardware with disposables.