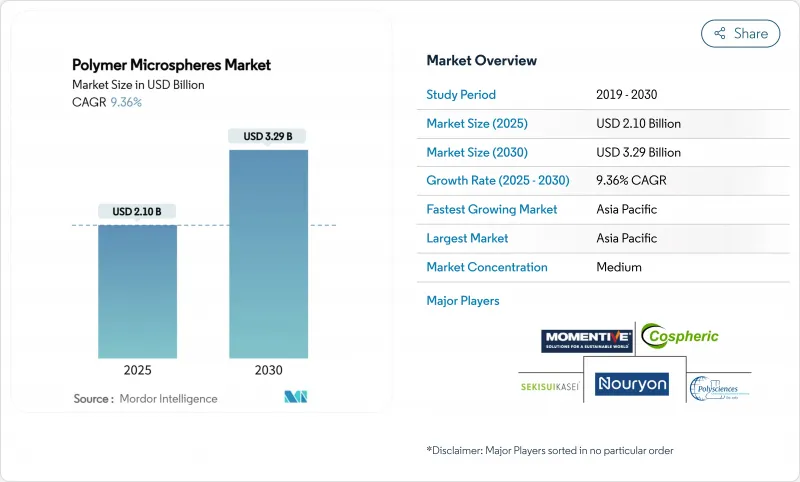

폴리머 마이크로스피어 시장 규모는 2025년에 21억 달러로 평가되었고 예측 기간(2025-2030년)의 CAGR은 9.36%를 나타낼 전망이며, 2030년에 32억 9,000만 달러에 이를 것으로 예측됩니다.

제약사들이 정밀 전달 시스템을 모색하고, 자동차 제조사들이 경량화 프로그램을 강화하며, 적층 제조 기업들이 복잡한 부품에 구형 원료를 채택함에 따라 수요가 가속화되고 있습니다. 폴리락틱-코-글리콜릭산(PLGA) 및 기타 생분해성 운반체를 활용한 제약 제형은 높은 생산 비용을 상쇄하는 가격 프리미엄을 가져온다. 자동차 제조사들은 부품 밀도를 낮추기 위해 중공 및 팽창성 등급을 사용하며, 이는 배출 및 전기화 목표 달성을 지원합니다. 전자제품 조립업체들은 첨단 패키징을 위해 열전도성 변형을 지정하는 반면, 3D 프린팅 서비스 업체들은 일관된 층 적층을 보장하는 좁은 입자 분말을 구매합니다. 공급 측면에서는 바이오 기반 혁신이 기존 생산자들의 위치를 재편하고 있지만, 변동성이 큰 스티렌 및 프로필렌 가격은 상류 통합이 없는 기업의 마진을 압박하고 있습니다.

PLGA 및 기타 생분해성 캐리어로 달성 가능한 정밀한 방출 프로파일은 제형 개발자들이 기존 정제에서 주사제 또는 이식형 미세구 시스템으로 전환하게 했습니다. 생물학적 제제를 캡슐화하는 능력은 안정성을 향상시켜 콜드체인 손실을 줄이고 치료 결과를 개선합니다. 마이크로유체 제조 기술은 이제 역사적인 배치 변동성을 극복하는 좁은 입자 크기 분포를 제공합니다. 미국 식품의약국(FDA)은 15개 이상의 PLGA 기반 제품을 승인하여 명확한 규제 선례를 마련했습니다. 맞춤형 의약품 프로그램은 조절 가능한 방출 동역학을 활용하여 개인별 약동학 프로파일에 맞춘 투여를 가능하게 합니다. 무균 미세구체 생산 능력을 이미 보유한 제약사는 높은 전환 비용을 구축하여 경쟁적 우위를 강화합니다.

유럽 규제 기관은 CO2 배출 강도 목표 달성을 위한 차량 전체 중량 감소를 요구하며, 이로 인해 중공 구체가 내장재, 범퍼 빔, 후드 하부 부품에 통합되는 폴리머 사용이 촉진됩니다. 밀도는 기계적 강성 손실 없이 25%까지 감소 가능하며, 이는 전기차 주행 거리 연장으로 이어집니다. 마이크로스피어로 가능해진 저압 성형은 사이클 타임 단축을 통해 공장 생산성을 향상시킵니다. 컴파운더와 함께 등급을 공동 개발하는 공급업체들은 다년간의 조달 계약을 확보합니다. 배터리 전기차 모델의 생산 비중이 증가함에 따라, 차체에서 제거되는 1kg당 OEM에 실질적인 비용 및 주행 거리 이점을 제공합니다.

유럽연합 규정은 씻어내는 화장품의 마이크로 플라스틱 함량을 0.01%로 제한하여, 페이셜 스크럽과 치약에 사용되는 기존 폴리스티렌 구형 입자를 사실상 금지합니다. 글로벌 브랜드들은 단일 준수 기준에 맞춰 제형을 통일함으로써 일회용 등급 제품의 주요 판매처를 상실하게 됩니다. 생분해성 대체재가 없는 공급업체들은 즉각적인 매출 감소를 경험합니다. 신제품 개발 주기도 규제 테스트에 자원을 전환하게 하여 인접 카테고리 출시를 지연시킵니다. 생분해성 대체재는 높은 마진을 제공하지만, 단기적 전환은 퍼스널케어에 크게 노출된 기업의 현금 흐름에 도전 과제를 제기합니다.

팽창성 등급은 2024년 매출의 52.76%를 차지했으며, 이는 자동차 및 건설용 복합재 분야에서 안정적인 사용에 기반합니다. 해당 분야에서는 제어된 팽창을 통해 강도를 저하시키지 않으면서 밀도를 낮출 수 있습니다. 생분해성 등급은 규모는 작지만, 규제 기관과 의약품 개발사들이 제어된 약물 방출을 위해 PLGA 및 폴리카프로락톤 매트릭스를 선호함에 따라 11.18%의 연평균 성장률(CAGR)로 가장 빠르게 성장할 것으로 전망됩니다. 아시아태평양 지역의 제형 개발사들은 역사적으로 경량 충전재용 팽창성 구에 집중해 왔으나, 현재는 미래 수요에 대비하기 위해 생분해성 생산 능력으로 다각화하고 있습니다.

제약회사는 후기 임상 프로그램용 생산 능력을 확보하는 장기 공급 계약을 체결하여 주문량을 안정화하고 있습니다. 반면 일반 확장성 제품은 특히 저비용 기반을 활용하는 중국 및 인도 내국 생산자들의 가격 경쟁이 심화되고 있습니다. 그 결과 2030년까지 폴리머 마이크로스피어 시장 매출 구성은 고마진 생분해성 부문으로 기울어질 전망입니다.

폴리머 마이크로스피어 시장 보고서는 유형(팽창성 마이크로스피어, 생분해성 마이크로스피어), 재료 구성(폴리스티렌(PS), 폴리메틸 메타크릴레이트(PMMA), 폴리에틸렌(PE) 등), 최종 사용자 산업(생명과학 및 제약, 화장품 및 퍼스널케어, 페인트 및 코팅 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

아시아태평양 지역은 2024년 글로벌 가치의 37.20%를 차지하며, 제약 제조, 반도체 조립 및 자동차 생산 분야의 우위를 반영합니다. 이 지역의 10.75% 예상 연평균 복합 성장률(CAGR)은 원료 비용 우위와 경량 충전재를 중시하는 전기차 조립 라인 확장에서 비롯됩니다. 인도는 국내 제약 생산량 증가와 현지 화장품 브랜드의 규격 준수 생분해성 대체재 채택으로 성장을 가속화합니다. 수출 지향적 공급업체들은 기존 물류망을 활용해 북미와 유럽으로 제품을 운송함으로써, 폴리머 마이크로스피어 시장의 주요 생산 거점으로서 아시아태평양 지역의 역할을 강화하고 있습니다.

이 지역의 10.75% 예상 연평균 복합 성장률(CAGR)은 원료 비용 우위와 경량 충전재를 중시하는 전기차 조립 라인 확장에서 비롯됩니다. 인도는 국내 제약 생산량 증가와 현지 화장품 브랜드의 규제 준수 가능한 분해성 대체재 채택으로 성장을 가속화하고 있습니다. 수출 중심 공급업체들은 기존 물류망을 활용해 북미와 유럽으로 제품을 운송하며, 아시아태평양 지역이 폴리머 마이크로스피어 시장의 주요 생산 거점으로서의 역할을 강화하고 있습니다.

북미는 약물 전달 시스템 혁신과 경량화 목표를 포함하는 엄격한 기업 평균 연비(CAFE) 규제로 인해 소비가 지속적으로 강세를 유지하고 있습니다. 계약 연구 기관(CRO)과 원천 장비 제조사(OEM)는 마이크로스피어 공급업체와 협력하여 고유한 성능 기준을 충족하는 독점 등급 제품을 개발하고 있습니다. 유럽은 REACH 규정에 따른 마이크로 플라스틱 제한을 시행하여 제형 개발자들이 생분해성 미세구체를 채택하도록 강제하고 있습니다. 이러한 입법적 추진은 퍼스널케어 및 도료 분야에서 제품 재구성을 가속화하고 있습니다. 남미, 중동 및 아프리카 지역은 산업 다각화가 진전되면서 중간 수준의 수요 증가를 경험하고 있으나, 현지 생산 능력 한계로 인해 공급은 수입에 의존하고 있습니다.

The Polymer Microspheres Market size is estimated at USD 2.10 billion in 2025, and is expected to reach USD 3.29 billion by 2030, at a CAGR of 9.36% during the forecast period (2025-2030).

Demand accelerates as drug developers seek precision delivery systems, automotive producers intensify lightweighting programs, and additive-manufacturing firms adopt spherical feedstocks for complex parts. Pharmaceutical formulations that exploit poly-lactic-co-glycolic acid (PLGA) and other biodegradable carriers bring price premiums that offset higher production costs. Automakers use hollow and expandable grades to cut part density, which supports emissions and electrification targets. Electronics assemblers specify thermally conductive variants for advanced packaging, while 3-D printing service bureaus purchase narrow-cut powders that ensure consistent layer deposition. On the supply side, bio-based innovations reposition incumbent producers, yet volatile styrene and propylene prices compress margins for firms without upstream integration.

Precise release profiles achievable with PLGA and other biodegradable carriers have shifted formulators away from traditional tablets toward injectable or implantable microsphere systems. The capability to encapsulate biologics improves stability, which reduces cold-chain losses and enhances therapeutic outcomes. Microfluidic manufacturing now delivers narrow particle-size distributions that overcome historic batch variability. The United States Food and Drug Administration has cleared more than 15 PLGA-based products, providing clear regulatory precedents. Personalized-medicine programs exploit tunable release kinetics, enabling dosing designed around individual pharmacokinetic profiles. Pharmaceutical companies that already own sterile microsphere capacity build high switching costs that reinforce competitive moats.

Regulators in Europe require fleetwide weight reductions that support CO2 intensity targets, encouraging polymers that integrate hollow spheres into interior trim, bumper beams, and under-hood parts. Density can fall by 25% with no loss in mechanical stiffness, a gain that extends electric vehicle driving range. Lower-pressure molding made possible by microspheres also trims cycle times, which improves plant productivity. Suppliers that co-develop grades with compounders lock in multiyear sourcing agreements. As battery-electric models account for a larger share of production, every kilogram removed from the body in white delivers tangible cost and range advantages for original equipment manufacturers.

European Union regulation limits microplastic content in rinse-off cosmetics to 0.01%, effectively banning conventional polystyrene spheres in facial scrubs and toothpastes. Global brands harmonize formulations to a single compliant standard, which removes a significant volume outlet for disposable grades. Suppliers that lack biodegradable alternatives see immediate revenue declines. New product development cycles also divert resources toward regulatory testing, slowing launches in adjacent categories. While bio-degradable replacements offer higher margins, the short-term shift challenges cash flows for firms heavily exposed to personal care.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Expandable grades captured 52.76% of 2024 revenue, underpinned by steady use in automotive and construction composites, where controlled expansion lowers density without sacrificing strength. Biodegradable grades, while smaller, are forecast to grow fastest at 11.18% CAGR as regulators and drug developers favor PLGA and polycaprolactone matrices for controlled drug release. Asia-Pacific formulators historically focused on expandable spheres for lightweight fillers, now diversifying into bio-degradable capacity to hedge future demand.

Pharmaceutical contractors lock in long-term supply agreements that secure capacity for late-stage clinical programs, stabilizing order books. By contrast, generic expandable products face intensifying price competition, especially from domestic producers in China and India that leverage low-cost bases. As a result, revenue mix across the polymer microspheres market tilts toward higher-margin biodegradable segments through 2030.

The Polymer Microspheres Market Report is Segmented by Type (Expandable Microspheres, and Biodegradable Microspheres), Material Composition (Polystyrene (PS), Polymethyl-Methacrylate (PMMA), Polyethylene (PE), and More), End-User Industry (Life Sciences and Pharmaceuticals, Cosmetics and Personal Care, Paints and Coatings, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific holds a 37.20% share of the 2024 global value, reflecting its dominance in pharmaceutical manufacturing, semiconductor assembly, and automotive production. The region's 10.75% forecast CAGR stems from cost advantages in feedstocks and expanding electric-vehicle assembly lines that value lightweight fillers. India amplifies growth as domestic pharmaceutical output rises, and local cosmetics brands adopt compliant, degradable alternatives. Export-oriented suppliers leverage established logistics to ship to North America and Europe, reinforcing Asia-Pacific's role as the primary production hub for the polymer microspheres market.

The region's 10.75% forecast CAGR stems from cost advantages in feedstocks and expanding electric-vehicle assembly lines that value lightweight fillers. India amplifies growth as domestic pharmaceutical output rises, and local cosmetics brands adopt compliant, degradable alternatives. Export-oriented suppliers leverage established logistics to ship to North America and Europe, reinforcing Asia-Pacific's role as the primary production hub for the polymer microspheres market.

North America maintains strong consumption through innovation in drug delivery and stringent corporate average fuel economy regulations that embed lightweighting targets. Contract research organizations and original equipment manufacturers collaborate with microsphere suppliers on proprietary grades that meet unique performance criteria. Europe enforces micro-plastic restrictions under REACH, compelling formulators to adopt biodegradable spheres. This legislative push drives rapid product reformulation across personal care and paints. South America and the Middle-East, and Africa experience moderate uptake as industrial diversification advances, but supply relies on imports due to limited local production capacity.