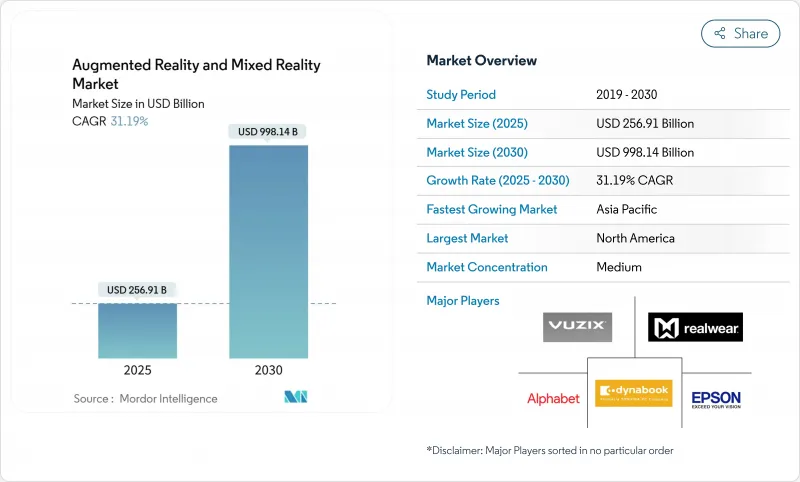

증강현실(Augmented Reality) 및 혼합현실(Mixed Reality) 시장 규모는 2025년에 2,569억 1,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 31.19%를 나타낼 것으로 예측되며 2030년에 9,981억 4,000만 달러에 달할 전망입니다.

5G 네트워크의 상용화, 지속되는 기업 디지털 전환 예산, 마이크로 OLED 및 웨이브가이드 디스플레이의 급속한 비용 하락으로 공간 컴퓨팅 시범 운영이 대규모 도입으로 전환되고 있습니다. 기업들은 측정 가능한 효율성 향상을 보고하고 있습니다. 예를 들어, 마스 펫케어는 RealWear HMT-1 웨어러블 기기를 Microsoft Teams와 연동한 후 코칭 출장 비용을 35% 절감했습니다. 메타가 리얼리티 랩스의 다년간 손실을 흡수하고, 애플이 비전 프로를 프리미엄 공간 컴퓨팅으로 포지셔닝하며, 삼성-구글-퀄컴 연합이 2025년 안드로이드 XR 출시를 위해 경쟁하면서 경쟁 구도가 격화되고 있습니다. 증강현실(AR) 및 혼합현실(MR) 시장은 이제 하드웨어 혁신, AI 지원 3D 콘텐츠 파이프라인, 반복 수익 모델을 촉진하는 관리형 서비스 성장의 교차점에 위치해 있습니다.

통신사들은 이제 20ms 미만의 지연 시간을 제공하여 클라우드 렌더링 시각화를 가능케 함으로써 헤드셋의 부하를 줄이고 배터리 수명을 연장합니다. 에지 오프로딩을 통해 경량 안경도 열 과부하 없이 풍부한 기능의 콘텐츠를 처리할 수 있습니다. 퀄컴의 분산 컴퓨팅 특허는 기기가 로컬과 원격 처리 간에 원활하게 전환하여 전력 요구를 네트워크 상태에 맞출 수 있게 합니다. 멀티플레이어 혼합현실 게임은 이제 플레이어당 최대 50Mbps를 요구하여 통신사들이 AR 전용 서비스 계층을 구축하도록 유도합니다. 원격 장비 재설정과 같은 시간 민감형 산업 작업은 거의 즉각적인 홀로그래픽 가이드의 혜택을 받아 네트워크 공급업체에게 새로운 기업 계약 기회를 열어줍니다.

스마트폰 AR은 진입 장벽을 낮추며, 포켓몬 GO의 누적 매출 80억 달러 돌파가 이를 입증합니다. 소매업체들은 가상 착용 서비스를 활용합니다. 세포라의 얼굴 인식 기반 ‘버추얼 아티스트'는 장바구니 전환율을 높이고 반품률을 낮춥니다. 이케아의 '플레이스’ 앱은 실제 공간에서 가구 배치 적합성을 확인시켜 크기 관련 반품을 줄입니다. 구글은 AR 뷰티 체험 서비스를 모바일 브라우저로 확대해 50개 이상 브랜드의 상호작용률을 10% 향상시켰습니다. 모바일 채널은 사용자의 친숙도를 키워 이후 헤드셋 채택으로 이어지며, 증강현실 및 혼합현실 시장의 스마트폰에서 웨어러블로의 전환 과정을 강화합니다.

고가 정책은 대량 배포를 제한합니다. 애플 비전 프로의 가격표는 3,000달러를 넘어 기업들이 시범 운영 단계별 도입을 강요받게 합니다. 소니는 플레이스테이션 VR2 가격을 인하했으나 과잉 재고로 인한 비용 민감도가 부각되며 생산을 중단했습니다. HTC는 ROI 분석을 통해 999달러 Vive Focus Vision 구매를 정당화할 수 있는 틈새 기업 사용자를 겨냥합니다. 메타의 리얼리티 랩스 누적 손실은 기술적 야망과 합리적 소비자 SKU를 결합하는 데 어려움을 시사합니다. 업체들은 광학 및 SoC 분야의 규모의 경제에 집중해 시장 진입 장벽을 넘어 더 넓은 시장으로 진출하려 합니다.

2024년 하드웨어 부문은 프리미엄 헤드셋과 광학 부품의 자본 집약적 특성으로 매출의 61%를 유지했습니다. 금전적 측면에서 증강현실 및 혼합현실 하드웨어 시장 규모는 1,560억 달러에 근접했으며, 이는 Vision Pro, Quest Pro, HoloLens에 대한 기업의 지속적인 지출을 반영합니다. 한편 서비스 부문은 32.5%의 최고 연평균 성장률(CAGR)을 기록하며 구독 기반 지원, 콘텐츠 제작, 기기 관리 서비스로의 전환을 강조했습니다.

관리형 서비스의 성장은 클라우드 소프트웨어의 성장 궤적을 반영합니다. ArborXR은 다중 브랜드 VR을 아우르는 플릿 관리 구독 서비스를 제공하여 대규모 배포 시 IT 복잡성을 줄입니다. 시스템 통합업체들은 콘텐츠 라이브러리, 분석 도구, 긴급 문제 해결 서비스를 예측 가능한 운영 비용(OPEX)으로 묶어 제공함으로써 비용 논의의 초점을 하드웨어 지출에서 총 솔루션 투자 회수(TROP)로 전환합니다. 마이크로 OLED 비용이 하락함에 따라 하드웨어 매출은 비례적으로 감소할 수 있으나, 서비스 부문은 복합적으로 성장하여 증강현실 및 혼합현실 시장을 반복적 수익 구조로 유지할 것입니다.

2024년 독립형 HMD는 지출의 48%를 차지했으며, 이는 증강현실 및 혼합현실 기기 시장 규모의 거의 절반에 해당합니다. 그러나 스마트 글래스는 웨이브가이드 소형화로 제품이 일상적인 안경 수준의 무게로 발전함에 따라 연평균 33%의 성장률을 보일 것으로 전망됩니다. Meta Orion과 같은 업계 프로토타입은 70도 시야각을 제공하면서도 85g 미만 목표를 달성하여 하루 종일 착용 가능성의 전환점이 되고 있습니다.

삼성-구글의 프로젝트 무한(Project Moohan)은 투명 디스플레이와 제미니 AI를 결합해 완전한 몰입형 경험보다는 헤드업 정보 표시(HUD)에 중점을 둡니다. 소비자는 사회적 환경에서 가벼운 폼 팩터를 선호하는 반면, 기업은 안전 헬멧 통합 및 시야선 작업 흐름을 위해 안경형 기기를 선호합니다. 공급망이 안정화됨에 따라 시장 구성은 안경형 기기로 전환될 것이며, 이는 증강현실 및 혼합현실 시장 전반에 걸쳐 개발자 우선순위와 마케팅 전략을 재편할 것입니다.

증강현실 및 혼합현실 시장 보고서는 컴포넌트별(하드웨어, 소프트웨어, 서비스), 디바이스 유형별(독립형 헤드마운트 디스플레이 (HMD), 테더/콘솔 링크형 HMD, 기타), 최종 사용자 산업별(게임 및 엔터테인먼트, 헬스케어, 교육 및 트레이닝, 소매 및 전자상거래, 기타), 용도별(원격 협업 및 지원)

북미는 플랫폼 소프트웨어 및 벤처 캐피털의 대부분을 계속 공급하고 있습니다. 초기 기업 도입 사례는 물류, 현장 서비스, 의료 분야에서 투자 수익률(ROI)을 입증하여 거시적 불확실성에도 불구하고 반복 주문을 확보했습니다. 수출 통제 및 지적 재산권 보호에 대한 규제 명확성은 해외 기업들이 실리콘밸리와 시애틀에 연구개발(R&D) 센터를 설립하도록 유도합니다. 그러나 초기 도입 기업들이 성숙 단계에 접어들고 조달이 교체 주기로 전환되면서 단위 성장률은 둔화되었습니다.

아시아태평양 지역의 확장 속도는 글로벌 평균을 상회합니다. 혁신 친화적 산업 정책과 집중된 디스플레이 제조 역량이 신제품 광학 장치의 시장 출시 기간을 단축합니다. 한국과 일본의 통신사들은 5G 기반 XR 구독 서비스를 통해 수익을 창출하며 소비자 인지도 제고에 기여합니다. 스타트업들은 시범 운영 비용의 최대 50%를 지원하는 정부 보조금을 활용해 기업 대상 개념 검증(PoC)을 가속화합니다. 중산층 소비자의 가처분 소득 증가로 AR 쇼핑 및 게임 채택률이 더욱 상승합니다.

유럽은 기회와 신중함 사이에서 균형을 맞추고 있습니다. 산업 기업들은 기존 자동화 아키텍처 내에서 예측 유지보수를 위해 AR을 활용하는 한편, 의료 시스템은 원격 수술 시각화 시범 운영을 진행 중입니다. 그러나 GDPR에 따른 동의 절차는 개발 부담을 가중시킨다. '프라이버시 바이 디자인(Privacy-by-Design)'을 입증한 기업들은 신뢰를 얻어 철도, 에너지, 국방 분야 입찰에서 승리합니다. 디지털 유럽 프로그램(Digital Europe Programme)의 보조금은 향후 10년간 분열을 줄이기 위한 국경 간 표준 조정을 목표로 합니다.

The Augmented Reality And Mixed Reality Market size is estimated at USD 256.91 billion in 2025, and is expected to reach USD 998.14 billion by 2030, at a CAGR of 31.19% during the forecast period (2025-2030).

Commercial deployment of 5G networks, sustained enterprise digital-transformation budgets, and rapid cost erosion in micro-OLED and waveguide displays are converting spatial-computing pilots into scaled roll-outs. Enterprises report measurable efficiency gains; for example, Mars Petcare cut coaching travel costs by 35% after pairing RealWear HMT-1 wearables with Microsoft Teams. Competitive momentum intensifies as Meta absorbs multi-year Reality Labs losses, Apple positions Vision Pro for premium spatial-computing, and a Samsung-Google-Qualcomm alliance races to a 2025 Android XR launch. The augmented reality and mixed reality market now sits at the intersection of hardware innovation, AI-assisted 3D content pipelines, and managed-services growth that encourages recurring-revenue models.

Telcos now deliver sub-20 ms latency, enabling cloud-rendered visuals that lighten headsets and prolong battery life. Edge offloading lets lightweight glasses handle feature-rich content without thermal overload. Qualcomm's distributed compute patents allow devices to switch seamlessly between local and remote processing, matching power needs to network conditions. Multiplayer mixed-reality games now require up to 50 Mbps per player, pushing operators toward AR-specific service tiers. Time-sensitive industrial tasks such as remote equipment resets benefit from near-instant holographic guidance, unlocking new enterprise contracts for network providers.

Smartphone AR lowers entry barriers, evidenced by Pokemon GO surpassing USD 8 billion lifetime revenue. Retailers leverage virtual try-ons; Sephora's facial-recognition-enabled Virtual Artist drives higher cart conversion while lowering return rates. IKEA's Place app lets buyers assess furniture fit in actual rooms, reducing size-related returns. Google broadened AR beauty try-ons to mobile browsers, lifting interaction rates for 50+ brands by 10%. The mobile channel nurtures user familiarity that later transitions to headset adoption, reinforcing the augmented reality and mixed reality market's funnel from phones to wearables.

Premium pricing restricts volume deployment. Apple Vision Pro's tag surpasses USD 3,000, forcing firms to stage adoption in pilot waves. Sony trimmed PlayStation VR2 prices yet paused production after excess inventory underscored sensitivity to cost. HTC targets niche enterprise users willing to justify USD 999 Vive Focus Vision through ROI analytics. Meta's cumulative Reality Labs losses signal the struggle to pair technological ambition with affordable consumer SKUs. Vendors focus on scale economies in optics and SoCs to cross critical pricing thresholds that unlock wider addressable markets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware retained 61% of revenue in 2024 as premium headsets and optics remain capital-heavy. In monetary terms, the augmented reality and mixed reality market size for hardware approached USD 156 billion, reflecting continued enterprise spending on Vision Pro, Quest Pro, and HoloLens. Meanwhile, services posted the highest 32.5% CAGR, underlining migration to subscription-oriented support, content-authoring, and device-management offerings.

Growth in managed services mirrors cloud-software trajectories. ArborXR offers fleet-management subscriptions across multi-brand VR, reducing IT complexity for large roll-outs. System integrators bundle content libraries, analytics, and on-call troubleshooting into predictable OPEX, shifting cost discussions from hardware outlay to total-solution payback. As micro-OLED costs fall, hardware revenue may dilute proportionally, yet services will compound, keeping the augmented reality and mixed reality market on a recurring-revenue footing.

Stand-alone HMDs commanded 48% of spend in 2024, equivalent to nearly half of the augmented reality and mixed reality market size for devices. However, smart glasses are forecast at a 33% CAGR as waveguide miniaturization moves products toward everyday eyewear weight. Industry prototypes such as Meta Orion deliver 70-degree FOV while meeting under-85-gram targets, a tipping point for day-long wearability.

Samsung-Google's Project Moohan blends transparent displays with Gemini AI, focusing on heads-up information rather than full-occlusion immersion. Consumers gravitate to lighter form factors in social settings, while enterprises favor glasses for safety-helmet integration and line-of-sight workflows. As supply chains stabilize, the mix will pivot toward glasses, reshaping developer priorities and marketing narratives across the augmented reality and mixed reality market.

The Augmented Reality and Mixed Reality Market Report is Segmented by Component (Hardware, Software, and Services), Device Type (Stand-Alone Head-Mounted Display [HMD], Tethered/Console-linked HMD, and More), End-User Industry (Gaming and Entertainment, Healthcare, Education and Training, Retail and E-Commerce, and More), Application (Remote Collaboration and Assistance, Design and Visualization, and More), and Geography.

North America continues to supply the bulk of platform software and venture capital. Early enterprise roll-outs confirmed ROI in logistics, field service, and healthcare, anchoring repeat orders despite macro uncertainty. Regulatory clarity on export controls and IP safeguards attracts overseas firms to form R&D centers in Silicon Valley and Seattle. Yet unit growth has slowed as first-wave adopters mature and procurement moves into replacement cycles.

Asia Pacific's expansion outpaces the global average. Pro-innovation industrial policies and concentrated display manufacturing compress time-to-market for new optics. Telcos in South Korea and Japan monetize 5G-based XR subscriptions, fueling consumer awareness. Start-ups enjoy government grants that cover up to 50% of pilot costs, accelerating enterprise proof-of-concepts. Rising disposable income among middle-class consumers further elevates AR shopping and gaming uptake.

Europe balances opportunity with caution. Industrial companies leverage AR for predictive maintenance within established automation architectures, while healthcare systems pilot remote-surgery visualization. However, GDPR-driven consent workflows add development overhead. Firms that demonstrate privacy-by-design earn trust and win tenders across rail, energy, and defense. Subsidies from the Digital Europe Programme target cross-border standards alignment, aiming to lower fragmentation over the coming decade.