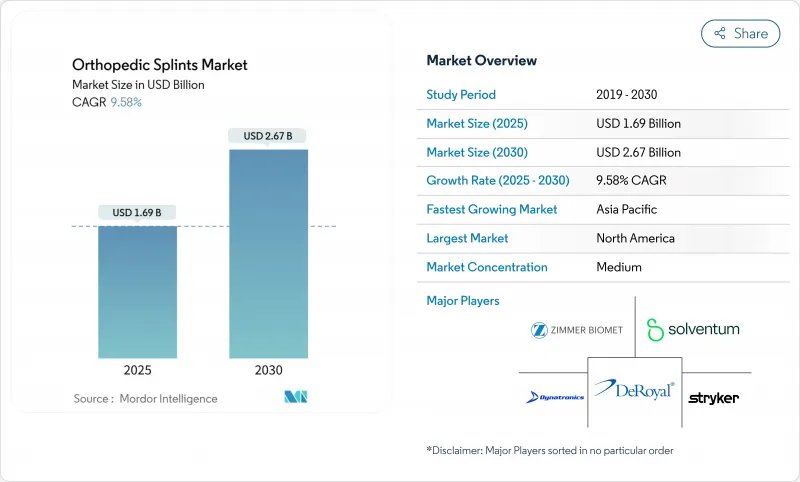

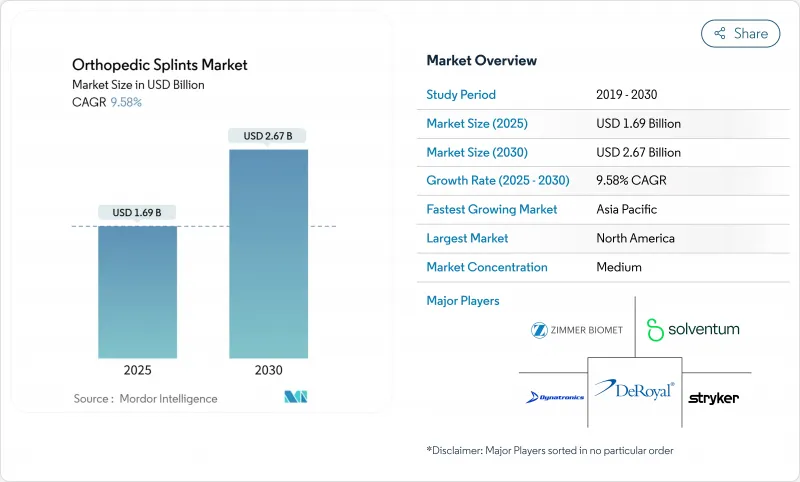

정형외과용 부목 시장 규모는 2025년에 16억 9,000만 달러로 평가되었고, 2030년에 26억 7,000만 달러에 이를 것으로 예상되며, 이 기간의 CAGR은 9.58%를 나타낼 전망입니다.

인구 고령화, 스포츠 참여 증가, 외래 진료 중심의 치료 환경 전환으로 수요가 확대되고 있습니다. 석고에서 경량 복합재 및 3D 프린팅 형태로의 전환을 비롯한 재료 기술 발전은 적용 시간을 단축하고 환자 편의성을 개선하여 의료진의 빠른 도입을 촉진합니다. 규제 기관은 임상적으로 검증된 혁신을 장려하는 수명주기 기반 심사 방식을 시범 운영 중이며, 보험급여 체계는 의료진이 비용 효율적이고 결과 중심의 제품을 선호하도록 유도합니다. 이러한 역학 관계가 결합되어 가격 책정이 절제되고 지속적인 제품 갱신 주기가 촉진되며, 이는 정형외과용 부목 시장의 성장 동력을 유지합니다.

전 세계 골관절염 환자는 2021년 6억 700만 명에 달했으며 여전히 증가 추세에 있어, 부목은 관절 안정화를 위한 일차적 비수술적 해결책으로 자리매김하고 있습니다. 요통만 해도 2029년까지 2억 5300만 건의 신규 환자가 발생할 것으로 예상되어 비용 효율적인 고정 장치의 필요성이 더욱 부각되고 있습니다. 직업 관련 연구에 따르면 사무직 근로자의 88.8%가 경추 통증을, 83.8%가 요통을 경험하는 것으로 나타나 만성적 수요가 광범위함을 보여줍니다. 부목은 특히 수술을 지연하거나 피하려는 환자에게 통증을 완화하고 관절의 추가 악화를 제한합니다. 보험사들이 침습적 시술 승인 전 보존적 치료를 강조함에 따라 정형외과용 부목 시장은 꾸준한 시술량을 확보하고 있습니다.

연령 표준화 골관절염 유병률이 크게 증가했습니다. 골밀도 감소와 함께 골절 취약성이 높아지며, 특히 척추나 고관절 안정화가 필요한 폐경 후 여성에서 두드러집니다. 의료진은 수술실 노출이 적합하지 않은 노인 환자의 이동성 보존을 위해 부목을 점점 더 선호합니다. 장기화된 치료 기간과 반복적인 장치 교체 필요성은 공급업체에 예측 가능한 수익원을 제공합니다. 선진국에서는 보편적 의료보험 적용으로 일관된 장치 비용 보상이 보장되어, 정형외과용 부목 시장이 노인 근골격계 치료의 핵심 축으로 자리매김하고 있습니다.

사회경제적 격차로 인해 많은 염좌와 미세 골절이 정형외과 진료소에 도달하지 못합니다. 보험 적용이 부족한 집단은 응급실을 과도하게 이용하거나 아예 치료를 포기하여 장치 사용량을 직접적으로 감소시킵니다. 농촌 병원들은 인력 부족에 직면해 있으며, 정형외과 전문의를 고용한 곳은 30%에 불과해 최종 치료가 지연되고 가끔은 자가 치료로 수요가 전환되기도 합니다. 신흥 경제국에서는 전통적인 뼈 맞추기 치료에 대한 의존으로 소아 환자의 28%가 진료를 늦게 받게 되며, 이는 실현되지 않은 시장 잠재력을 나타냅니다. 이러한 격차는 보다 광범위한 의료 접근성 개선 정책이 정형외과용 부목 시장의 새로운 수요를 창출할 수 있음을 보여줍니다.

2024년 정형외과용 부목 시장에서 유리섬유 부목은 45.42%의 점유율을 기록했으며, 이는 저렴한 비용, 광범위한 임상적 친숙도, 확립된 보험 적용 경로에 기인합니다. 의료진은 예측 가능한 강성과 빠른 경화 특성으로 인해 유리섬유 부목을 선호하며, 외상 치료실에서 주로 사용됩니다. 그러나 연평균 10.34% 성장률을 보이는 3D 프린팅 맞춤형 부목이 경쟁 구도를 재편하고 있습니다. 무작위 대조 시험 결과, 부피가 큰 폴리머 제품 대신 적층 제조 디자인을 사용할 경우 통증 감소, 만족도 향상, 욕창 발생률 감소가 확인되었습니다. 병원 내 프린터를 도입한 기관들은 외부 발주 시 다일이 소요되던 제작 기간을 당일 맞춤 제작으로 단축하여 환자 처리량을 높이고 재고 위험을 줄였습니다.

3D 프린팅의 성장은 스캐닝 장치, 설계 소프트웨어, 소모성 필라멘트 등 부속 시장으로 파급되어 조기에 전환한 공급업체들에게 새로운 수익 사슬을 창출하고 있습니다. 프린팅된 프레임워크와 전통적인 랩 재료를 혼합한 하이브리드 제품은 가격에 민감한 구매자를 대상으로 하면서도 맞춤형 혜택을 유지합니다. 석고 캐스트는 감소 추세이지만 기술 예산이 여전히 부족한 열악한 환경에서는 여전히 입지를 유지하고 있습니다. 전반적으로 다양한 제품 포트폴리오는 제조사가 중증도와 가격대별로 시장을 세분화할 수 있게 하여 정형외과용 부목 시장 전반에 걸쳐 지속적인 가치 창출을 지원합니다.

2024년 정형외과용 부목 시장에서 유리섬유는 44.43%를 차지했으나, 열가소성 플라스틱이 2030년까지 연평균 10.22% 성장률로 가장 빠르게 확장 중입니다. 중간 온도에서 재성형이 가능한 열가소성 시트는 진료진이 추적 관찰 시 정렬을 미세 조정할 수 있게 하여 재수술률을 낮춥니다. 통기성과 방수 특성 또한 환자 순응도 향상으로 이어지며, 이는 소아 및 스포츠 환자군에서 핵심 촉진요인입니다. 규제 기관은 이제 친환경 의료를 장려하여 의료 제공자들이 미세 플라스틱 잔류물 없이 분해되는 생분해성 폴리머 대안을 모색하도록 촉진하고 있습니다.

탄소섬유 복합재는 발목-발 고정용으로 인장 강도 대비 무게 효율성을 인정받아 전용 보험 적용 코드가 부여되는 프리미엄 등급을 차지합니다. 단가는 일반 유리섬유보다 훨씬 높으나, 엘리트 운동선수 및 수술 후 환자에게는 프리미엄 비용이 정당화됩니다. 파리 석고는 성형성과 초저비용이 구매 기준인 저자원 시장에서 여전히 사용됩니다. 지속가능성 의제가 강화됨에 따라 재활용 가능한 수지 기술에 투자하는 공급업체들은 정형외과용 부목 시장에서 초기 브랜드 우위를 점할 수 있을 것입니다.

북미는 선진적인 외상 치료 인프라, 높은 선택적 수술률, 소재 및 제조 혁신의 조기 도입 덕분에 2024년 정형외과용 부목 시장의 41.44% 점유율을 차지했습니다. 공급업체 통합으로 구매력이 향상되면서 공급업체들은 디지털화된 재고 추적 및 현장 교육과 같은 부가가치 서비스를 패키지로 제공하게 되었습니다. 정형외과 기기 대상 '제품 전체 수명 주기 자문 프로그램(TPLAC)'과 같은 규제 시범 사업은 혁신 주기 단축을 목표로 하지만, 동시에 제조업체에 시판 후 안전성 데이터 제출을 요구하여 규정 준수 비용을 증가시킵니다.

아시아태평양 지역은 2030년까지 연평균 복합 성장률(CAGR) 10.59%로 가장 빠른 확장 통로를 형성할 전망입니다. 도시화, 보험 적용 범위 확대, 가처분 소득 증가는 근골격계 손상 치료율 증가로 이어집니다. 중국, 인도, 한국 정부는 현재 국내 적층 제조 라인을 보조금 지원하여 수입 의존도를 낮추고 지역별 인체 측정 데이터에 맞춤화된 제품 변종을 육성하고 있습니다. 대규모 환자 풀은 생산량 확대를 신속히 가능케 하여 현지 합작 투자에 대한 공급업체의 관심을 강화합니다. 스포츠 참여 증가와 교통사고 관련 골절은 정형외과용 부목 시장의 잠재적 수요 기반을 더욱 확대합니다.

유럽은 고령화 인구와 의료비 보장을 위한 보편적 의료 시스템에 힘입어 완만한 성장을 유지하고 있습니다. 환경 관리 지침으로 인해 병원들은 재활용 가능하거나 생분해성 소재에 대한 조달 목표를 설정해야 하며, 이는 공급업체의 친환경 소재 개발 투자를 촉진합니다. 중동 및 아프리카 시장은 작은 기반에서 확장 중이며, 걸프 국가들은 외국인 근로자와 국내 인구 모두를 위해 고급 의료기기를 수입하고 있습니다. 남미는 브라질과 아르헨티나에서 공공-민간 의료 협력으로 의료기기 접근성과 의료진 교육이 개선되며 성장 동력을 보이고 있습니다. 이러한 지리적 폭은 단일 지역 경기 침체로부터 정형외과용 부목 시장을 보호하고 지속적인 글로벌 매출을 뒷받침합니다.

The orthopedic splints market size reached USD 1.69 billion in 2025 and is forecast to climb to USD 2.67 billion by 2030, reflecting a solid 9.58% CAGR over the period.

Demand expands as populations age, sports participation rises, and care delivery shifts toward outpatient settings. Material advances, notably the move from plaster to lighter composites and 3-D printed forms, shorten application times and improve patient comfort, encouraging faster provider uptake. Regulatory agencies now pilot lifecycle-based review pathways that reward clinically validated innovation while reimbursement schedules push providers to favor cost-efficient, outcomes-oriented products. Together, these dynamics keep pricing disciplined and stimulate continual product refresh cycles, sustaining momentum in the orthopedic splints market.

Global osteoarthritis cases hit 607 million in 2021 and are still climbing, making splints a first-line, non-surgical solution for joint stabilization. Low back pain alone could reach 253 million incident cases by 2029, reinforcing the need for cost-effective immobilization devices. Occupational studies note cervical pain in 88.8% of office workers and lower-back pain in 83.8%, underscoring widespread, chronic demand . Splints mitigate pain and limit further joint deterioration, especially for patients seeking to delay or avoid surgery. As payers emphasize conservative management before approving invasive procedures, the orthopedic splints market gains steady procedural volume.

Age-standardized osteoarthritis prevalence rose significantly . Fracture susceptibility grows alongside reductions in bone density, particularly among post-menopausal women, who often require vertebral or hip stabilization. Providers increasingly opt for splints to preserve mobility in elderly patients not suited for operating room exposure. Longer treatment timelines and repeat device replacement needs add a predictable revenue stream for suppliers. In wealthier nations, universal coverage ensures consistent device reimbursement, cementing the orthopedic splints market as a pillar of geriatric musculoskeletal care.

Socioeconomic disparities mean many sprains and hairline fractures never reach orthopedic clinics. Under-insured groups disproportionately use emergency departments or forego care altogether, cutting directly into unit volumes. Rural hospitals face staffing shortages; only 30% employ orthopedic surgeons, delaying definitive treatment and occasionally shifting demand toward home remedies. In emerging economies, reliance on traditional bone setters leads to delayed presentations in 28% of pediatric cases, representing unrealized market potential. The gap illustrates how broader health-access initiatives could unlock new volumes for the orthopedic splints market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fiberglass splints held 45.42% of the orthopedic splints market in 2024, anchored by their low cost, broad clinical familiarity, and established reimbursement pathways. Providers value fiberglass for predictable rigidity and quick setting, making it a go-to in trauma bays. Yet 3-D printed custom splints, expanding at 10.34% CAGR, are redrawing competitive boundaries. Randomized trials document lower pain, improved satisfaction, and fewer pressure sores when additive-manufactured designs replace bulkier polymers. Hospitals experimenting with in-house printers reduce turnaround from multi-day outsource cycles to same-day fittings, raising patient throughput while trimming inventory risk.

Growth in 3-D printing ripples through accessory markets such as scanning devices, design software, and consumable filaments, creating new revenue chains for suppliers that pivot early. Hybrid items mixing printed frameworks with traditional wrap materials cater to price-sensitive buyers yet preserve customization benefits. Plaster casts, although declining, retain a foothold in austere settings where technology budgets remain tight. Overall, diversified offerings allow manufacturers to segment by acuity and price point, supporting sustained value capture across the orthopedic splints market.

Fiberglass accounted for 44.43% of the orthopedic splints market in 2024, but thermoplastics are expanding fastest at 10.22% CAGR through 2030. Remoldable at moderate heat, thermoplastic sheets let clinicians fine-tune alignment during follow-up visits, curbing revision rates. Breathability and waterproof attributes also translate into higher patient compliance, a key driver in pediatric and sports cohorts. Regulatory bodies now encourage greener healthcare, prompting providers to explore biodegradable polymer alternatives that degrade without micro-plastic residue.

Carbon-fiber composites occupy the premium tier, validated by dedicated reimbursement codes that recognize their tensile strength-to-weight advantage for ankle-foot immobilization. Unit prices exceed mainstream fiberglass by a wide margin, yet elite athletes and postoperative cases justify the premium. Plaster of Paris persists where moldability and ultra-low cost dominate buying criteria, particularly in low-resource markets. As sustainability agendas intensify, suppliers investing in recyclable resin technologies may seize an early branding advantage in the orthopedic splints market.

The Orthopedic Splints Market is Segmented by Product (Fiberglass Splints, Plaster Splints, and More), Material (Fiberglass, Plaster of Paris, and More), Application (Lower Extremity [Hip, Knee, and More], Upper Extremity, and Spinal), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market and Forecasts are Provided in Terms of Value (USD).

North America commanded 41.44% share of the orthopedic splints market in 2024 thanks to advanced trauma infrastructure, high elective procedure rates, and early adoption of material and manufacturing innovation. Provider consolidation has improved purchasing power, prompting suppliers to bundle value-added services such as digitized inventory tracking and in-service training. Regulatory pilots like the Total Product Life Cycle Advisory Program for orthopedic devices aim to shorten innovation cycles but simultaneously push manufacturers to supply post-market safety data, raising compliance costs.

Asia-Pacific represents the fastest expansion corridor with a 10.59% CAGR projected to 2030. Urbanization, expanding insurance coverage, and increasing disposable income translate into higher musculoskeletal injury treatment rates. Governments in China, India, and South Korea now subsidize domestic additive-manufacturing lines, lessening import dependence and fostering region-specific product variants tailored to local anthropometry. Large patient pools allow quick scaling of production volumes, reinforcing supplier interest in localized joint ventures. Rising sports participation and traffic-related fractures further enlarge the addressable base for the orthopedic splints market.

Europe maintains moderate growth underpinned by aging demographics and universal health systems that guarantee device reimbursement. Environmental stewardship directives compel hospitals to set procurement targets for recyclable or biodegradable materials, stimulating supplier investment in green formulations. Middle East and Africa markets expand from a small base, with gulf states importing premium devices for expatriate workforces and domestic populations alike. South America shows momentum in Brazil and Argentina, where public-private healthcare partnerships improve device availability and clinician training. Collectively, geographical breadth cushions the orthopedic splints market against single-region downturns and underwrites sustained global revenues.