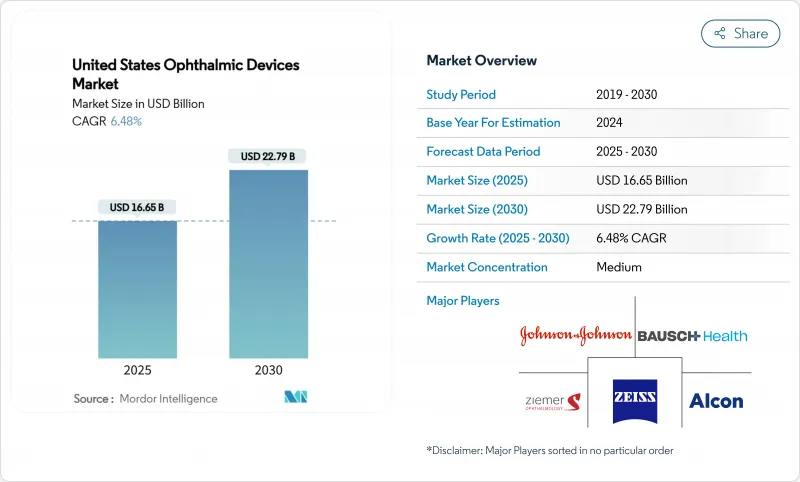

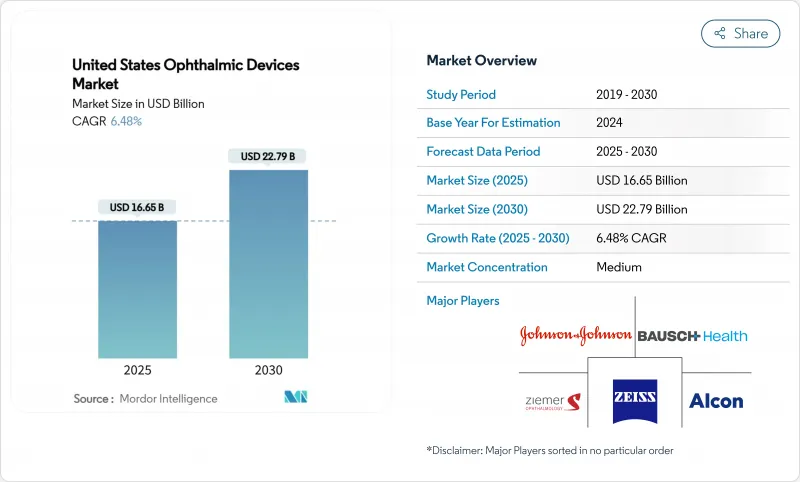

미국의 안과용 의료기기 시장 규모는 2025년에 166억 5,000만 달러로 평가되었고, 2030년에는 227억 달러에 이를 전망입니다.

65세 이상 성인층의 백내장 환자 증가, 보험 적용 범위 확대, 영상 소프트웨어의 지속적인 업그레이드가 이 꾸준한 성장세를 뒷받침하고 있습니다. 수술 기기는 현재 매출의 42.1%를 차지하는데, 이는 고마진 굴절 수술, 백내장 수술, 녹내장 수술을 가능하게 하여 대부분의 병원이 미룰 수 없는 시술이기 때문입니다. 외래 수술 센터는 가장 빠르게 성장하는 최종 사용자 채널로, 5.23%의 연평균 성장률(CAGR)을 기록하고 있습니다. 이는 보험사와 환자들이 동일한 결과를 더 낮은 비용으로 제공하는 입원 환경에서 외래 환경으로 이동하기 때문입니다. 한편, 프리미엄 인공수정체 붐과 자율적 AI 선별 도구의 급속한 도입은 구매 기준을 재편하고 있으며, 이로 인해 기기 제조사들은 수명 주기 차별화를 위해 하드웨어, 분석 도구, 클라우드 연결성을 묶어 제공하는 방향으로 나아가고 있습니다.

고령화 및 근시 인구 증가로 미국 안과 기기 시장의 진단 수요가 크게 증가하고 있습니다. 2050년까지 미국인 2명 중 1명이 근시가 될 것이라는 전망에 따라, 보험사들은 고도근시를 만성 질환으로 분류하는 방안을 검토하고 있습니다. 당뇨성 망막병증 환자 수는 2004년부터 2024년 사이 960만 명으로 두 배 증가했으나, 조기 검진으로 환자들이 더 빨리 치료를 받게 되면서 시력 위협 사건은 감소했습니다. 지역 클리닉에 설치된 자율적 안저 촬영 알고리즘이 이러한 진전의 핵심으로, 의뢰 지연을 줄이고 농촌 지역의 접근성을 확대하고 있습니다.

노안 교정 및 확장 초점 심도 렌즈는 안경 의존도 해소를 원하는 환자 수요에 부응하며 외과의사들의 선택을 받고 있습니다. 2022년 ESCRS 조사에 따르면 2016년 대비 노안 교정 인공수정체 사용률이 4% 증가한 반면, 이중초점 모델은 신형 광학 기술이 대비 감도를 개선함에 따라 2%로 하락했습니다. 2024년 9월 출시된 존슨앤드존슨의 TECNIS Odyssey 렌즈는 이미 14,000안 이상에 시술되었으며, 기존 다초점 임플란트 대비 저조도 대비를 두 배로 향상시켰습니다. 이러한 가속화된 교체 주기는 미국 안과 기기 시장을 주도하는데, 외과의들이 종종 정밀한 렌즈 위치 조정을 위해 보정된 업그레이드된 파코 콘솔과 프리미엄 렌즈를 함께 사용하기 때문입니다.

OCT, 각막 지형도, 자동 굴절 검사를 포함한 완전한 진단 기기 세트는 50만 달러 이상이 소요될 수 있어, 대규모 외래 수술 센터(ASC) 환자 유입이 부족한 독립 진료소의 예산을 압박합니다. 많은 주에서 전문 서비스 수수료가 정체된 상황에서, 이들 제공자들은 7년 이내에 감가상각될 수 있는 자본 투자를 주저합니다. 리스 및 사용량 기반 요금제는 위험을 완화하지만, 환자 수에 따라 수수료가 변동되어 후방 사무 업무 복잡성을 초래합니다. 결과적으로 미국 안과 기기 시장 성장은 고르지 못하며, 소규모 진료소는 AI 소프트웨어 업데이트가 투자 수익률을 정당화할 때까지 구매를 미루고 있습니다.

수술 시스템은 2024년 매출의 42.11%를 차지했으며, 높은 초기 비용과 반복적인 소모품 사용을 결합하여 미국 안과 기기 시장의 핵심으로 남아 있습니다. 이러한 강력한 성과는 프리미엄 인공수정체(IOL)의 지속적인 보급률 증가 덕분으로, 시술당 가치를 높이고 외과의들이 난시 교정 및 난시 보정을 위한 토릭 정렬에 최적화된 콘솔 구매를 유도합니다. 외래 수술 센터 네트워크 역시 소형 수술실에 적합한 모듈식 펨토초 플랫폼을 선호합니다. 외과의들이 노후화된 백내장 수술 기기를 교체하여 MIGS와 백내장 수술을 결합한 워크플로우를 지원할 때마다, 이러한 꾸준한 교체 주기는 미국 안과 기기 시장 규모에서 수술 부문 비중을 높입니다.

반면, 시력 관리 기기는 여전히 출하량 기준 63.21%(2024년 기준)로 점유율을 주도하지만, 가격 하락과 온라인 안경 할인으로 인해 가치 기여도는 제한됩니다. 콘택트렌즈 제조사들은 산소 투과성을 높여 착용 시간을 연장하고 이탈률을 낮추는 실리콘 하이드로겔 소재로 대응합니다. 사용자가 분기별로 렌즈를 재주문함에 따라 공급업체는 예측 가능한 현금 흐름을 확보하여 점진적 연구를 지원합니다. 이러한 선순환 구조는 미국 안과 기기 시장의 전체 수익 구조를 크게 바꾸지 않으면서도 해당 분야의 리더십을 유지합니다.

The United States ophthalmic devices market size is valued at USD 16.65 billion in 2025 and is forecast to reach USD 22.7 billion by 2030, advancing at a 6.48% CAGR over the period.

Rising cataract volumes among adults over 65 years, broader insurance coverage, and continuous upgrades in imaging software collectively underpin this steady expansion. Surgical devices currently command 42.1% of revenue because they enable high-margin refractive, cataract, and glaucoma procedures that few hospitals can defer. Ambulatory surgical centers are the fastest-growing end-user channel, registering a 5.23% CAGR as payers and patients migrate from inpatient to outpatient settings that deliver comparable outcomes at lower cost. Meanwhile, the premium intraocular-lens boom and the rapid adoption of autonomous AI screening tools are reshaping purchasing criteria, prompting device makers to bundle hardware, analytics, and cloud connectivity for lifecycle differentiation.

An aging and increasingly myopic population is materially lifting diagnostic volumes across the United States ophthalmic devices market. Projections indicate that one in two Americans will be myopic by 2050, encouraging payers to consider classifying high myopia as a chronic disease. The diabetic-retinopathy population doubled between 2004 and 2024 to 9.6 million, yet sight-threatening events declined because earlier screening now redirects patients to treatment sooner. Autonomous fundus-photography algorithms installed in community clinics are central to this progress, reducing referral delays and widening access in rural counties.

Surgeons have embraced presbyopia-correcting and extended-depth-of-focus lenses to meet patient demand for spectacle independence. The 2022 ESCRS survey showed a 4% rise in presbyopia-correcting IOL use since 2016, while bifocal models fell to 2% as newer optics improved contrast sensitivity. Johnson & Johnson's TECNIS Odyssey lens, launched in September 2024, already treats more than 14,000 eyes, delivering double the low-light contrast versus earlier multifocal implants. This accelerated turnover drives the United States ophthalmic devices market because surgeons often pair premium lenses with upgraded phaco consoles calibrated for precise lens positioning.

A full diagnostic bay comprising OCT, corneal topography, and automated refraction can cost more than USD 500,000, straining budgets at independent practices that lack large ASC volumes. With many states seeing flat professional-service fees, these providers hesitate to commit capital that may depreciate in under seven years. Leasing and pay-per-use models mitigate risk, yet present back-office complexity because fees fluctuate with patient load. Consequently, growth in the United States ophthalmic devices market is uneven, with small offices deferring purchases until AI software updates justify their return on investment.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Surgical systems generated 42.11% of revenue in 2024 and remain the anchor of the United States ophthalmic devices market because they combine high upfront prices and recurring consumables. The strong performance benefits from sustained premium-IOL penetration, which boosts per-procedure value and nudges surgeons to purchase consoles optimized for toric alignment and astigmatic correction. Networks of ambulatory surgical centers also favor modular femtosecond platforms that fit compact operating rooms. This steady replacement cycle lifts the surgical slice of United States ophthalmic devices market size whenever surgeons retire aging phaco units to support combined MIGS-and-cataract workflows.

Conversely, vision-care devices still dominate unit volumes, accounting for 63.21% of shipments in 2024, yet price erosion and online spectacles discounting limit their value contribution. Contact-lens makers respond with silicone-hydrogel materials that extend oxygen permeability, extending wear times and lowering dropout rates. As users reorder lenses quarterly, suppliers secure predictable cash flow that finances incremental research. The virtuous feedback loop sustains category leadership without materially altering the overall profit mix of the United States ophthalmic devices market.

The United States Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More. The Market Forecasts are Provided in Terms of Value (USD).