영국의 치과용 장비 시장 규모는 2024년에 4억 7,210만 달러로 평가되었고, 2030년에는 6억 1,497만 달러로 확대될 것으로 예측되며, 2025-2030년의 CAGR은 4.58%를 나타낼 전망입니다.

디지털 워크플로우, 슈퍼공제 자본공제(Super-Deduction Capital Allowance) 같은 정책적 인센티브, 고령 환자 중심의 인구 구조 변화가 투자 우선순위를 재정의하면서 수요가 가속화되고 있습니다. 잉글랜드가 시장을 주도하지만, 스코틀랜드는 맞춤형 인력 육성 정책을 통해 성장 동력을 확보 중입니다. 치과 소모품이 여전히 매출의 주축이지만, CAD/CAM, 3D 프린팅, AI 기반 영상 기술의 급속한 도입으로 장비 부문이 전체 성장률을 앞지르고 있습니다. 독립 치과 진료소가 기업 그룹으로부터 소유권 점유율을 되찾으며 구매 패턴과 공급망 관계를 재편하고 있습니다. 한편, NHS 치과 회복 계획은 인력 부족으로 서비스 역량이 제한되고 장비 업그레이드가 지연되는 상황에서도 디지털 도입을 촉진하고 있습니다.

2050년까지 65세 이상 인구가 전국 인구의 25%를 차지할 것으로 예상되며, 이는 내구성과 생체 적합성을 갖춘 보철 및 임플란트 솔루션에 대한 장기적 수요를 촉진할 것입니다. 치과 병원들은 티타늄 코어와 이산화 지르코늄 세라믹을 결합한 지르코니아 하이브리드 임플란트로 전환 중이며, 이는 염증 반응을 줄이고 티타늄 과민증을 해결합니다. 실험실 연구에 따르면, 이러한 하이브리드 임플란트는 순수 티타늄 대비 인간 치수 줄기세포의 세포 부착 및 골형성 분화 능력을 향상시킵니다. 이에 따라 조달 담당자들은 첨단 세라믹 및 복합 임플란트 라인의 일관된 품질을 보장할 수 있는 공급업체를 우선적으로 선정하고 있습니다. 이 촉진요인의 영향력은 노인 치과 인프라가 가장 발달한 잉글랜드와 스코틀랜드에서 가장 강하며, 이는 예측 기간 동안 영국 치과용 장비 시장의 꾸준한 성장을 뒷받침할 것입니다.

NHS 치과 회복 계획은 치료량 증가에 대한 재정적 인센티브를 도입하고 2031년까지 교육 인원을 40% 확대함으로써, 진료소가 처리량 목표를 달성하기 위해 워크플로우를 디지털화하도록 유도하고 있습니다. 설문조사에 따르면 99.3%의 의료진이 디지털의 이점을 인식하고 있지만, 자본 비용이 여전히 주요 도입 장벽으로 남아 있습니다. 특히 그룹 진료소는 진료 시간 단축과 개혁에 포함된 예방 치료 KPI 달성을 위해 구강 내 스캐너와 진료실 밀링 장비 도입을 확대하고 있습니다. 잉글랜드에만 적용되는 정책이지만, 공급업체들이 UKCA 인증 스캐너에 대한 국경 간 주문을 보고함에 따라 웨일즈로의 확산 효과가 나타나고 있습니다. 이 촉진요인은 디지털 장비의 시장 평균을 상회하는 성장을 지속시키고 영국 치과용 장비 시장 내 입지를 공고히 합니다.

5,500명의 치과 전문가 부족이 공식적으로 확인되며, 특히 해안 지역 및 취약 지역에서 ‘치과 사막화’ 현상이 확대되고 있습니다. 95%의 진료소가 간호사와 보조 인력 채용에 어려움을 겪고 있습니다. 진료 의자 수 감소로 인해 소유주들이 활용률을 의심하며 첨단 영상 장비 및 내부 밀링 장비에 대한 자본 지출을 꺼리고 있습니다. 어소시에이트들은 더 높은 보수를 위해 개인 병원으로 이동하고 있어 NHS 처리량을 더욱 억제하고 있습니다. 확대된 교육 과정 졸업생이 배출되기 전까지 인력 부족은 첨단 기술 도입 속도를 저해하여 영국 치과용 장비 시장의 기본 CAGR에서 약 1.4% 포인트를 감소시킬 것으로 예상됩니다.

영국의 치과용 장비 시장의 장비 부문은 2030년까지 5.23%의 CAGR 전망을 기록하며, 2024년 소모품이 주도하는 61.23%의 매출 기반을 넘어설 것으로 예상됩니다. 진료실에서는 턴어라운드 시간을 단축하고 아웃소싱 비용을 절감하는 전략적 투자 수단으로 진료실 내 CAD/CAM 및 실험실 등급 3D 프린터를 꼽고 있습니다. CAD/CAM 블록 및 소모품 시장은 설치 기반과 함께 확장되며, 반복 수익을 창출하는 독점적 공급망에 클리닉을 묶어두고 있습니다.

구강 내 스캐너는 이제 일상적인 검사에 널리 보급되어 STL 데이터를 클라우드 설계 포털에 직접 공급합니다. 한편, 우수한 재료 효율성과 설계 자유도로 인해 복잡한 수복 작업이 밀링에서 적층 방식으로 전환되고 있습니다. DEXIS Ti2와 같은 AI 기반 센서는 이미징에 머신러닝 분석을 적용하여 독립형 하드웨어가 아닌 진단 플랫폼의 역할을 예고합니다. 이러한 추세는 장비의 가치 점유율을 강화하고 영국 치과용 장비 시장 전반에 디지털 의존성을 심화시키고 있습니다.

영국의 치과용 장비 시장 보고서는 산업을 제품 유형(일반 및 진단 장비, 치과 소모품, 기타 치과용 장비), 치료 분야(교정, 근관 치료, 치주 치료, 보철 치료), 최종 사용자(병원, 치과 클리닉, 기타 최종 사용자)별로 세분화합니다. 5년간의 과거 데이터와 향후 5년간의 예측이 포함됩니다.

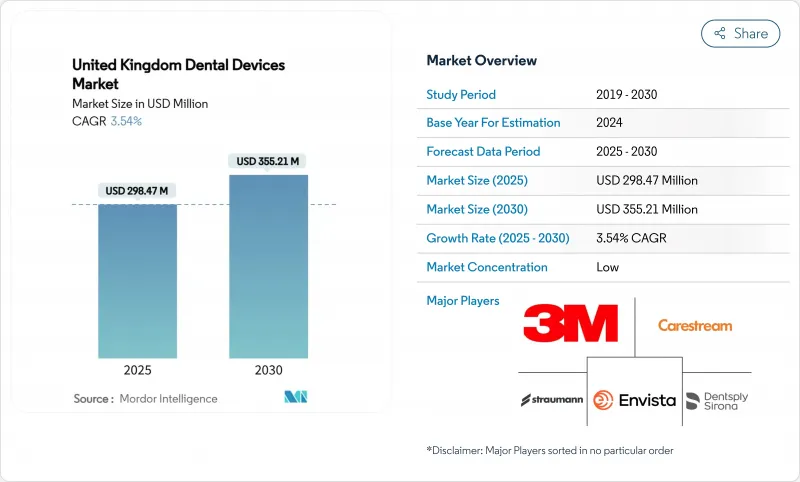

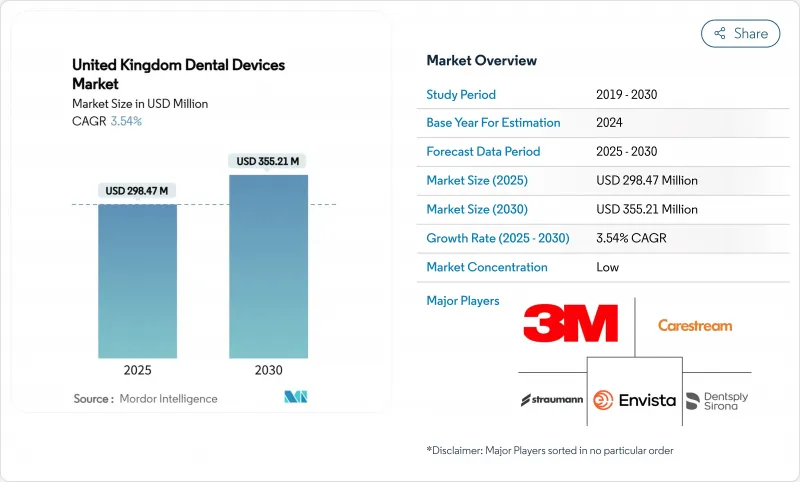

The United Kingdom dental devices market size is USD 472.10 million in 2024 and is forecast to expand to USD 614.97 million in 2030, reflecting a 4.58% CAGR over 2025-2030.

Demand is accelerating as digital workflows, policy incentives such as the Super-Deduction Capital Allowance, and a demographic tilt toward older patients redefine investment priorities. England anchors the market, but Scotland is gaining momentum through targeted workforce initiatives. Dental consumables remain the revenue backbone, yet the equipment category is outpacing overall growth due to the rapid uptake of CAD/CAM, 3-D printing, and AI-enabled imaging. Independent practices are regaining ownership share from corporate groups, reshaping purchasing patterns and supply-chain relationships. Meanwhile, the NHS Dental Recovery Plan is catalyzing digital adoption even as workforce shortages restrain service capacity and delay equipment upgrades.

Adults aged >=65 will represent 25% of the national population by 2050, pushing long-term demand for durable, biocompatible prosthodontic and implant solutions. Clinics are shifting toward zirconia-hybrid implants that blend titanium cores with zirconium-dioxide ceramic, reducing inflammatory response and addressing titanium hypersensitivity. Laboratory studies show these hybrids improve cell adhesion and osteogenic differentiation in human dental pulp stem cells compared with pure titanium. As a result, procurement teams are prioritizing suppliers able to guarantee consistent quality of advanced ceramic and composite implant lines. The driver's influence is strongest in England and Scotland where geriatric dental infrastructure is most developed, and it underpins steady growth for the United Kingdom dental devices market through the forecast horizon.

The NHS Dental Recovery Plan introduces financial incentives that reward higher treatment volumes and allocates a 40% lift in training places by 2031, prompting clinics to digitize workflows to meet throughput targets. Surveys show 99.3% of practitioners recognize digital benefits, yet capital costs remain the chief adoption barrier. Group practices in particular are scaling intraoral scanners and chairside milling to cut appointment times and align with preventive-care KPIs embedded in the reform. Although limited to England, the policy's spillover into Wales is visible as suppliers report cross-border orders for UKCA-compliant scanners. This driver sustains above-market growth for digital equipment and cements its role in the United Kingdom dental devices market.

A documented gap of 5,500 dental professionals is widening "dental deserts," particularly in coastal and deprived regions, with 95% of practices struggling to hire nurses and associates. Reduced chair capacity discourages capital outlays for advanced imaging and in-house milling, as owners question utilization rates. Associates are shifting toward private practice for higher remuneration, further throttling NHS throughput. Until expanded training cohorts graduate, staffing scarcity will dampen the pace of high-tech adoption, subtracting an estimated 1.4 percentage points from the base CAGR of the United Kingdom dental devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The equipment slice of the United Kingdom dental devices market recorded a 5.23% CAGR outlook to 2030, outstripping the consumables-dominated 61.23% revenue base in 2024. Practices cite chairside CAD/CAM and lab-grade 3-D printers as strategic investments that compress turnaround times and cut outsourcing fees. The CAD/CAM blocks and consumables niche is expanding in tandem with installed bases, locking clinics into proprietary supply chains that generate recurring revenue.

Intraoral scanners now permeate routine examinations, feeding STL data directly into cloud design portals. Meanwhile, three-dimensional printing is shifting complex restoration work from milling to additive, due to superior material efficiency and design freedom. AI-enabled sensors such as DEXIS Ti2 layer machine-learning analytics onto imaging, foreshadowing a diagnostic platform play rather than stand-alone hardware. These trends reinforce the value share of equipment and embed digital dependence throughout the United Kingdom dental devices market.

The UK Dental Devices Market Report Segments the Industry Into by Product Type (General and Diagnostics Equipment, Dental Consumables, Other Dental Devices), by Treatment (Orthodontic, Endodontic, Periodontic, Prosthodontic), by End User (Hospitals, Dental Clinics, Other End Users). Five Years of Historical Data and Five-Year Forecasts are Included.