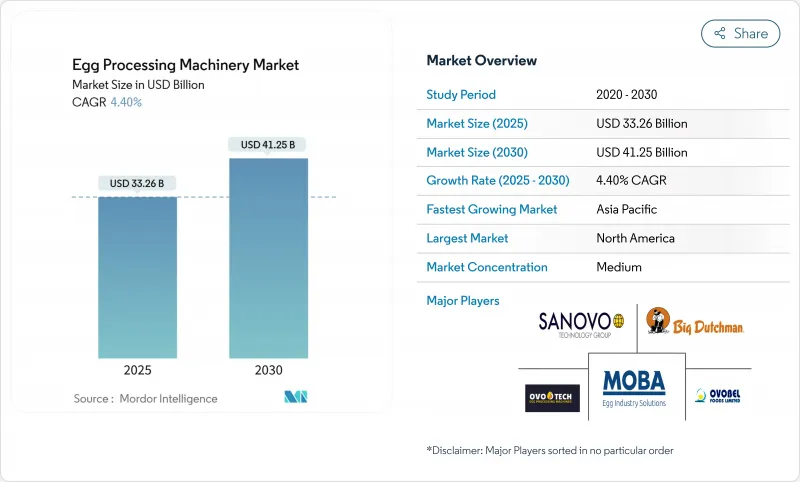

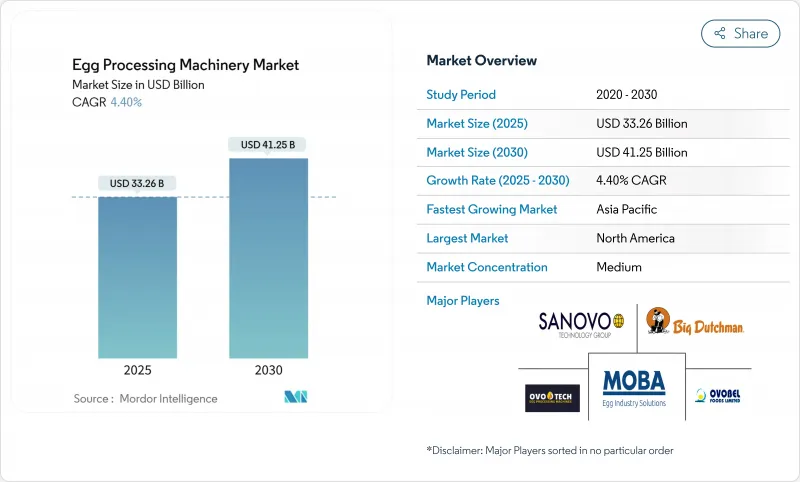

계란 가공 기계 시장은 2025년에 332억 6,000만 달러로 평가되었고, 2030년에는 412억 5,000만 달러에 이를 것으로 예측되며, CAGR 4.40%로 성장할 전망입니다.

이러한 성장은 자동화 기술의 발전, 엄격한 식품 안전 규정, 단백질 소비 패턴의 다양화 증가에 힘입어 이루어지고 있습니다. 미국과 유럽의 규제 변화는 지속적인 모니터링 시스템, 강력한 사이버 보안 조치, AI 기반 안전 기능을 갖춘 첨단 기계의 도입을 촉진하고 있으며, 이는 교체 주기 단축에도 기여하고 있습니다. 북미에서는 가산업체들이 고병원성 조류 인플루엔자 발생 등으로 인한 공급망 차질에 대응하기 위해 유연한 생산 라인에 대규모 투자를 진행 중입니다. 동시에 아시아태평양 지역 운영사들은 인구 증가와 식습관 변화로 인한 도시 시장의 급증하는 수요를 충족시키기 위해 스마트 기술을 신속히 도입하고 있습니다. 경쟁 환경은 최첨단 하드웨어와 고급 데이터 분석을 결합한 통합형 솔루션 중심으로 진화하고 있습니다. 이러한 솔루션은 가산업체가 수율, 에너지 효율성, 규정 준수 등 핵심 성과 지표를 실시간으로 모니터링할 수 있게 하여 운영 효율성을 높이고 비용을 절감하며 식품 안전 기준 준수를 보장합니다.

즉석 섭취 가능하고 장기 보관이 가능한 단백질 원료로의 소비자 선호도 변화는 전통적인 액상 계란 응용을 뛰어넘는 첨단 가공 기술에 대한 지속적인 수요를 촉진하고 있습니다. 2025년 Cal-Maine이 Echo Lake Foods를 2억 5,800만 달러에 인수한 사례는 높은 이익률을 제공하지만 첨단 및 특수 가공 기계가 필요한 부가가치 계란 제품의 전략적 중요성을 부각시킵니다. 이 추세는 제조업체들이 에그 바이트, 사전 조리 오믈렛, 단백질 강화 편의식품과 같은 혁신적 제품을 생산할 수 있는 시스템을 추구함에 따라 가공 기계의 교체 주기를 가속화하고 있습니다. 이러한 제품들은 정밀한 온도 제어와 강력한 오염 방지 조치를 요구하므로 첨단 기계가 필수적입니다. 특히 균질기와 분무 건조기 부문이 이 변화의 혜택을 크게 보고 있는데, 이러한 기술들은 편의식품 응용 분야에 필요한 질감 개선과 유통기한 연장을 달성하는 데 핵심적이기 때문입니다. 경쟁력을 유지하기 위해 기계 제조업체들은 이제 단일 생산 라인에서 다양한 제품 형식을 처리할 수 있는 시스템을 설계해야 합니다. 이 요구사항은 생산 시스템의 복잡성과 자본 집약도를 동시에 증가시켜 기존 단일 제품 기계 대비 더 높은 기준을 설정하고 있습니다. 진화하는 시장 역학은 다양하고 고품질의 편의식품에 대한 증가하는 수요를 충족시키기 위해 가공 기술의 혁신과 적응력이 필요함을 강조합니다.

규제 집행이 주기적 검사에서 지속적인 모니터링으로 진화하면서 기계 설계 사양과 운영 프로토콜에 중대한 영향을 미치고 있습니다. FDA의 개정된 계란 규제 프로그램 기준(ERPS)은 주-연방 협력의 강력한 프레임워크를 수립하여 더 빈번한 검사와 더 엄격한 데이터 보고 의무를 이끌고 있습니다. 이러한 변화는 최소한의 수동 개입으로 규정 준수를 보장하는 내장형 모니터링 시스템, 자동 세척 기술, 실시간 데이터 수집 기능을 갖춘 첨단 기계의 채택을 촉진하고 있습니다. 또한 미국 농무부(USDA)가 개발한 무선 주파수(RF) 살균 기술은 기존 57분 소요 공정에 비해 현저히 빠른 24분 만에 살모넬라균을 99.999% 감소시키는 성과를 보여주며, 규제 요건이 기술 발전을 가속화하는 방식을 입증하고 있습니다. 운영 효율성을 유지하면서 이러한 혁신적인 안전 기술을 원활하게 통합할 수 있는 공급업체는 경쟁 우위를 점할 수 있는 위치에 있습니다. 규제 준수 비용이 수익성에 점점 더 큰 영향을 미치는 시장에서, 이러한 발전은 시장 리더십 유지와 진화하는 안전 기준 충족에 핵심적 요소가 되고 있습니다.

기계 금융 분야의 기술 발전은 대형 가산업체에 점점 더 유리하게 작용하는 반면, 소규모 업체들은 현대화에 대한 도전 과제가 커지고 있습니다. 이러한 어려움은 금융 접근성이 여전히 제한적인 신흥 시장에서 특히 두드러집니다. 종합 설비 구축에 1,000만 달러를 초과하는 상당한 자본 투자가 필요한 완전 자동화 계란 가공 라인은 중소 업체들이 직면한 재정적 장벽을 부각시킵니다. 이러한 제약을 해결하기 위해 인도 정부는 2025년 식품 가공 분야 생산 연계 인센티브 제도(PLI) 하에 1억 4,400만 달러를 배정하며 정책 주도적 개입의 필요성을 시사했습니다. 자금 조달 격차는 기계 서비스형 모델(Equipment-as-a-Service) 및 점진적 도입이 가능한 모듈식 시스템과 같은 대체 솔루션의 기회로도 이어졌습니다. 그러나 이러한 접근 방식은 완전 통합 설비의 운영 효율성을 제공하기에는 종종 부족합니다. 결과적으로 자본이 제한된 가산업체들은 기계 업그레이드를 자주 지연시키며, 이는 규제 미준수 위험과 경쟁력 약화를 초래합니다. 시간이 지남에 따라 이러한 취약성은 확대되어 시장 점유율 하락과 시장 내 추가 세분화로 이어질 수 있습니다.

2024년 기준 계란 깨기 기계는 시장 점유율 29.97%를 차지하며 하류 가공 공정의 핵심 요소로서 입지를 공고히 했습니다. 이러한 우위는 껍질 달걀을 액체 형태로 전환하는 필수 기능에서 비롯되며, 이는 부가가치 가공 전 필수적인 단계입니다. 결과적으로 계란 깨기 기계는 산업 인프라의 근간을 이룹니다. 이 부문은 기계 마모와 엄격한 위생 설계 규정 준수로 인한 꾸준한 교체 수요의 혜택을 받고 있습니다. 제조업체들은 자동화된 껍질 분리 및 품질 검사 기능을 통합한 첨단 깨기 시스템을 개발하여 대응하고 있습니다. 이러한 혁신은 오염 위험을 최소화할 뿐만 아니라 수율 효율성을 향상시켜 일관된 성능을 보장합니다. 다른 기계 카테고리가 기술적 발전을 경험하는 가운데, 계란 깨기 기계의 지속적인 시장 주도권은 업계가 기계적 가공 솔루션에 의존하고 있음을 강조합니다.

균질기는 2030년까지 연평균 복합 성장률(CAGR) 6.49%로 가장 빠르게 성장하는 기계 카테고리로 자리매김하고 있습니다. 이러한 성장은 액상 계란 응용 분야에서 균일한 제품 일관성과 유통기한 연장에 대한 수요 증가에 힘입은 것입니다. 이 분야의 주목할 만한 혁신 사례로는 모바(Moba)의 캐비테이션 균질화 기술이 있으며, 이는 보다 부드러운 균질화 공정을 가능케 합니다. 이 기술은 기존 고압 시스템 대비 파스퇴라이저 가동 시간을 연장하고 운영 비용을 절감하여 상당한 효율 향상을 제공합니다. 이 분야의 급속한 성장은 균질화 품질이 특히 제빵 및 식품 서비스 응용 분야에서 최종 제품 성능을 결정하는 데 있어 핵심적인 역할을 한다는 업계의 인식을 반영합니다. 현대식 균질기는 이제 살균 시스템과 완벽하게 통합되어 열처리를 최적화하면서도 제품 무결성을 유지합니다. 이러한 기술 융합은 전반적인 공정 효율성을 향상시키고, 제품 품질 유지와 운영 효율성이 경쟁 우위 확보의 핵심인 현대식 계란 가공 라인에서 균질기를 필수 구성 요소로 자리매김하게 합니다.

2024년 액상 계란은 시장 점유율 46.45%라는 상당한 비중을 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 7.15%를 기록할 것으로 전망됩니다. 이러한 성장은 일관된 품질과 취급 용이성이 중요한 식품 서비스, 제빵, 산업용 응용 분야 전반에 걸친 액상 계란의 다용도성을 부각시킵니다. 이 세그먼트의 우위는 껍질 달걀 대비 단순화된 저장, 운송, 재고 관리 등 가산업체에 운영 효율성을 제공하면서도 다양한 최종 사용자 범주의 요구를 충족시키는 능력에서 비롯됩니다. 달걀 껍질 오염 제거를 위한 97.6% 대장균 불활성화율을 달성하는 공학화된 물 나노구조(EWNS)와 같은 기술 발전은 액상 계란의 안전성과 품질을 더욱 향상시키면서 자연적 보호 특성을 보존하고 있습니다. 또한 첨단 가공 시스템은 실시간 품질 모니터링과 자동 오염 감지 기능을 통합하여 일관된 제품 사양을 보장합니다. 이러한 시장 주도권은 예측 가능하고 효율적인 제조 공정을 가능케 하는 표준화된 원료에 대한 식품 산업의 선호도가 증가하고 있음을 반영합니다.

액상 계란은 가공상의 장점을 활용하여 편의식품, 단백질 보충제, 기능성 식품 원료 등 신흥 응용 분야로도 확장되고 있습니다. 미국 농무부(USDA)가 개발한 고주파 살균 기술은 기존 57분 소요 공정 대비 단 24분 만에 살모넬라균을 99.999% 감소시켜 안전성을 높이고 가공 시간을 단축함으로써 액상 계란 응용 분야의 새로운 기회를 열었습니다. 이 분야를 지원하는 기계 제조업체들은 지속적인 수요 증가를 경험하고 있지만, 특수 제형을 처리하고 연장된 유통기한 요건을 충족할 수 있는 시스템 개발에 대한 압박이 커지고 있습니다. 강력한 성장 궤도를 타고 있는 액상 계란은 지속적인 기술 혁신과 새로운 응용 분야로의 다각화에 힘입어 시장 확장을 지속할 것으로 예상됩니다.

2024년 북미는 선진화된 식품 가공 인프라와 지속적인 기계 현대화를 촉진하는 엄격한 규제 체계에 힘입어 31.23%의 시장 점유율을 차지할 것으로 예상됩니다. 이 지역은 광범위한 자동화 도입과 편의 식품에 대한 강한 선호도로 혜택을 받고 있습니다. 그러나 시장 성숙도는 신흥 지역에 비해 성장 잠재력을 제한합니다. 공급망 차질이 기회를 창출하는 대표적인 사례로, 고병원성 조류인플루엔자(HPAI) 발생으로 인한 부족 사태를 해결하기 위해 2025년 미국이 터키로부터 4억 2천만 개의 계란을 수입하기로 한 결정이 있습니다. 미국 계란 위원회(American Egg Board)에 따르면, 미국이 연간 75억 개 이상의 계란을 생산함에도 불구하고 터키는 여전히 미국이 계란을 수입하는 유일한 국가입니다. 이러한 상황은 다양한 품질 기준을 가진 다양한 공급처의 원료를 처리할 수 있는 적응형 가공 시스템에 대한 수요 증가를 부각시킵니다.

아시아태평양 지역은 2030년까지 연평균 복합 성장률(CAGR) 7.49%로 가장 빠르게 성장할 것으로 전망됩니다. 이 성장은 급속한 도시화, 단백질 소비 증가, 식품 가공 산업 현대화를 목표로 한 정부 주도 정책에 의해 주도됩니다. 2000년 4월부터 2024년 3월까지 125억 8천만 달러의 외국인 직접 투자(FDI)를 유치한 인도의 식품 가공 부문은 해당 지역의 투자 매력과 성장 잠재력을 보여주는 대표적인 사례입니다. 중국에서는 2025년 초 154건의 미국산 식품 수입 거부 사례와 같은 농업 무역 역학이 강력한 국내 가공 역량과 엄격한 품질 관리 시스템의 필요성을 강조하고 있습니다. 이 지역의 확장은 현지 선호도, 규제 요건 및 비용 효율성 요구를 충족하도록 기술을 적용할 수 있는 기계 공급업체에게 상당한 기회를 창출합니다.

유럽은 엄격한 규제 준수 및 지속가능성 요구사항에 힘입어 꾸준한 수요를 지속하고 있습니다. 반면 남미와 중동·아프리카는 인프라 부족과 제한된 자본 가용성으로 성장이 제약되긴 하지만 신흥 시장으로서의 기회를 제시합니다. 이러한 지역별 격차는 경제 발전 단계와 식품 가공 산업 성숙도의 차이를 반영합니다. 또한 기계 공급업체들이 지역별 맞춤형 전략을 수립하고 현지 시장 수요에 부응하는 금융 솔루션을 제공할 수 있는 기회를 부각시킵니다.

The egg processing equipment market, valued at USD 33.26 billion in 2025, is projected to reach USD 41.25 billion by 2030, growing at a CAGR of 4.40%.

This growth is fueled by advancements in automation technologies, stringent food-safety regulations, and the increasing diversification of protein consumption patterns. Regulatory changes in the United States and Europe are driving the adoption of advanced machinery equipped with continuous monitoring systems, robust cybersecurity measures, and AI-based safety features, which are also contributing to shorter replacement cycles. In North America, processors are heavily investing in flexible production lines to counteract supply-chain disruptions, such as those caused by Highly Pathogenic Avian Influenza outbreaks. Concurrently, operators in the Asia-Pacific region are rapidly integrating smart technologies to meet the surging demand in urban markets, driven by population growth and changing dietary preferences. The competitive landscape is evolving towards integrated, solution-oriented offerings that combine state-of-the-art hardware with advanced data analytics. These solutions empower processors to monitor key performance indicators, such as yields, energy efficiency, and regulatory compliance, in real time, thereby enhancing operational efficiency, reducing costs, and ensuring adherence to food safety standards.

Shifting consumer preferences toward ready-to-eat and shelf-stable protein sources are driving sustained demand for advanced processing technologies that surpass traditional liquid egg applications. The acquisition of Echo Lake Foods by Cal-Maine for USD 258 million in 2025 highlights the strategic importance of value-added egg products, which offer higher profit margins but require advanced and specialized processing equipment. This trend is accelerating the replacement cycles for processing equipment, as manufacturers seek systems capable of producing innovative products such as egg bites, pre-cooked omelets, and protein-enriched convenience foods. These products demand precise temperature control and robust contamination prevention measures, making advanced equipment essential. The homogenizer and spray dryer segments are particularly benefiting from this shift, as these technologies are critical for achieving the texture modifications and extended shelf life required by convenience food applications. To remain competitive, equipment manufacturers must now design systems that can handle multiple product formats on a single production line. This requirement is increasing both the complexity and capital intensity of production systems, setting a higher standard compared to traditional single-product equipment. The evolving market dynamics underscore the need for innovation and adaptability in processing technologies to meet the growing demand for diverse, high-quality convenience food products.

Regulatory enforcement is evolving from periodic inspections to continuous monitoring, creating a profound impact on equipment design specifications and operational protocols. The FDA's updated Egg Regulatory Program Standards (ERPS) establish robust frameworks for state-federal collaboration, leading to more frequent inspections and stricter data reporting mandates. This shift is driving the adoption of advanced equipment featuring embedded monitoring systems, automated cleaning technologies, and real-time data capture capabilities, which ensure compliance with minimal manual intervention. Additionally, the USDA's development of Radio Frequency (RF) pasteurization technology, which achieves a 99.999% reduction in Salmonella in just 24 minutes-significantly faster than the traditional 57-minute process-demonstrates how regulatory requirements are accelerating technological advancements. Suppliers that can seamlessly integrate these innovative safety technologies while maintaining operational efficiency are positioned to gain a competitive edge. In markets where regulatory compliance costs increasingly influence profitability, such advancements are becoming critical for sustaining market leadership and meeting evolving safety standards.

Technological advancements in equipment financing are increasingly benefiting large processors, while smaller operations face growing challenges to modernization. These challenges are particularly pronounced in emerging markets, where access to financing remains constrained. Fully automated egg processing lines, which require significant capital investment exceeding USD 10 million for comprehensive installations, highlight the financial barriers smaller players encounter. To address such constraints, the Indian government has allocated USD 144 million in 2025 under its Production Linked Incentive Scheme for food processing, signaling the need for policy-driven interventions. The financing gap has also opened opportunities for alternative solutions, such as equipment-as-a-service models and modular systems, which enable incremental deployment. However, these approaches often fall short in delivering the operational efficiency of fully integrated installations. Consequently, processors with limited capital frequently delay equipment upgrades, exposing themselves to heightened risks of regulatory non-compliance and competitive disadvantages. Over time, these vulnerabilities can escalate, leading to potential market share erosion and further segmentation within the market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, egg breakers captured a significant 29.97% share of the market, solidifying their role as the cornerstone of downstream processing operations. This dominance stems from the essential function of converting shell eggs into liquid form, a critical step before any value-added processing can take place. As a result, egg breakers are fundamental to the industry's infrastructure. The segment benefits from steady replacement demand, driven by equipment wear and compliance with stringent sanitary design regulations. Manufacturers have responded by developing advanced breaking systems that incorporate automated shell separation and quality inspection features. These innovations not only minimize contamination risks but also enhance yield efficiency, ensuring consistent performance. The sustained market leadership of egg breakers highlights the industry's reliance on mechanical processing solutions, even as other equipment categories experience technological advancements.

Homogenizers are positioned as the fastest-growing machine category, with a projected CAGR of 6.49% through 2030. This growth is propelled by increasing demand for uniform product consistency and extended shelf life in liquid egg applications. A notable example of innovation in this segment is Moba's cavitation homogenizing technology, which enables gentler homogenization processes. This technology extends pasteurizer run times and reduces operational costs compared to traditional high-pressure systems, offering significant efficiency gains. The rapid growth of this segment reflects the industry's recognition of the critical role homogenization quality plays in determining the performance of final products, particularly in bakery and food service applications. Modern homogenizers now integrate seamlessly with pasteurization systems, optimizing thermal treatments while preserving product integrity. This technological convergence enhances overall processing efficiency and positions homogenizers as indispensable components in contemporary egg processing lines, where maintaining product quality and operational efficiency is key to achieving a competitive advantage.

In 2024, liquid eggs captured a significant 46.45% share of the market, with a projected CAGR of 7.15% through 2030. This growth highlights their versatility across food services, bakeries, and industrial applications, where consistent quality and ease of handling are critical. The segment's dominance is driven by its ability to meet the needs of multiple end-user categories while offering processors operational efficiencies, such as simplified storage, transportation, and inventory management compared to shell eggs. Technological advancements, such as engineered water nanostructures (EWNS) achieving a 97.6% E. coli inactivation rate for eggshell decontamination, have further enhanced the safety and quality of liquid eggs while preserving their natural protective properties. Additionally, advanced processing systems now integrate real-time quality monitoring and automated contamination detection, ensuring consistent product specifications. This market leadership reflects the food industry's growing preference for standardized ingredients that enable predictable and efficient manufacturing processes.

Liquid eggs are also expanding into emerging applications, including convenience foods, protein supplements, and functional food ingredients, leveraging their processing advantages. The USDA's development of Radio Frequency pasteurization technology, which reduces Salmonella by 99.999% in just 24 minutes compared to the traditional 57-minute process, has opened new opportunities for liquid egg applications by improving safety and reducing processing time. Equipment manufacturers supporting this segment are experiencing sustained demand growth but face increasing pressure to develop systems capable of handling specialized formulations and meeting extended shelf-life requirements. With a strong growth trajectory, liquid eggs are expected to continue their market expansion, driven by ongoing technological innovations and diversification into new applications.

The Global Egg Processing Equipment Market Report Segments the Industry by Machine Type (Egg Breakers, Egg Separators, and More); End Product (Liquid Eggs, and More); Automation Level (Manual/Small-Scale Systems, and More); End User (Egg Product Manufacturers, Bakery and Confectionery Processors, and More); and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

In 2024, North America holds a 31.23% market share, supported by its advanced food processing infrastructure and stringent regulatory frameworks that drive continuous equipment modernization. The region benefits from widespread automation adoption and a strong preference for convenience foods. However, market maturity limits its growth potential compared to emerging regions. A notable example of supply chain disruptions creating opportunities is the U.S. decision to import 420 million eggs from Turkey in 2025 to address shortages caused by HPAI outbreaks. Turkey remains the only country from which the U.S. imports eggs, despite the U.S. producing over 7.5 billion eggs annually, as per the American Egg Board. This scenario highlights the increasing demand for adaptable processing systems capable of handling inputs from diverse sources with varying quality standards.

Asia-Pacific is positioned as the fastest-growing region, with a projected CAGR of 7.49% through 2030. This growth is driven by rapid urbanization, increasing protein consumption, and government-led initiatives aimed at modernizing food processing industries. India's food processing sector, which attracted USD 12.58 billion in FDI between April 2000 and March 2024, exemplifies the region's investment appeal and growth potential In China, agricultural trade dynamics, such as the rejection of 154 U.S. food shipments in early 2025, underscore the critical need for robust domestic processing capabilities and stringent quality control systems. The region's expansion creates significant opportunities for equipment suppliers who can adapt technologies to meet local preferences, regulatory requirements, and cost-efficiency demands.

Europe continues to exhibit steady demand, driven by strict regulatory compliance and sustainability mandates. In contrast, South America and the Middle East & Africa present emerging opportunities, albeit with growth constrained by infrastructure deficits and limited capital availability. These geographic disparities reflect varying stages of economic development and food processing industry maturity. They also highlight opportunities for equipment suppliers to implement region-specific strategies and offer financing solutions tailored to local market needs.