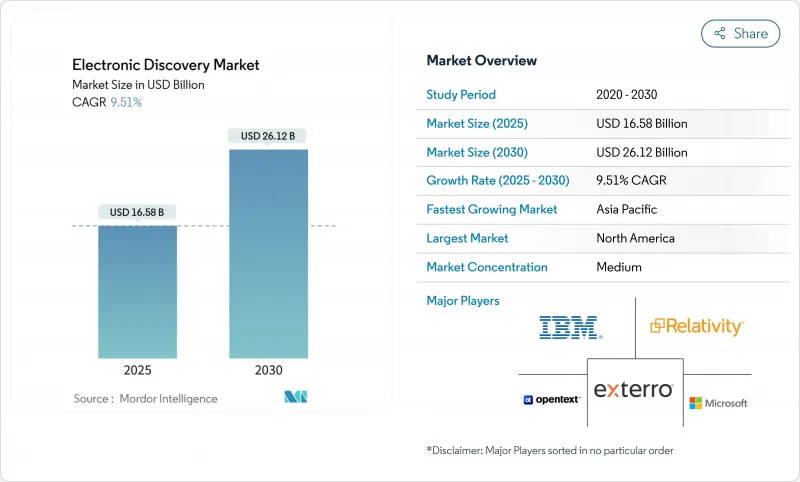

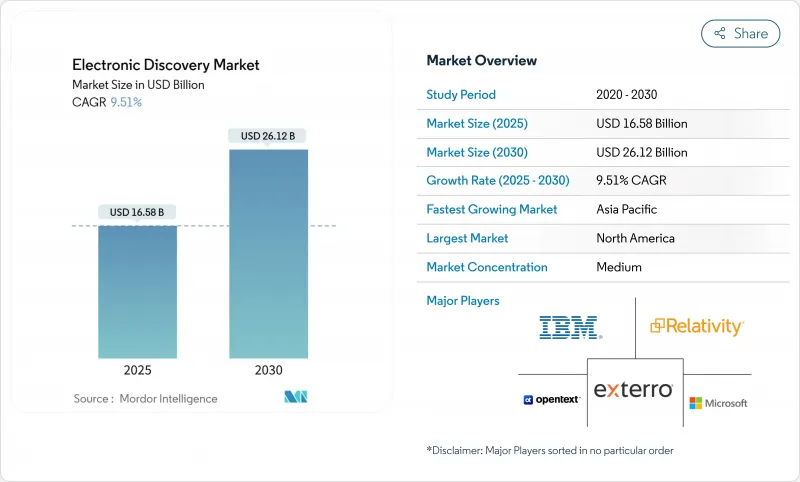

전자 증거개시 시장 규모는 2025년에 165억 8,000만 달러로 예측 기간 중 CAGR은 9.51%를 나타낼 전망이며, 2030년에는 261억 2,000만 달러에 달할 것으로 예상되고 있습니다.

법적 프로세스의 고급 디지털화, 다중 포맷 데이터의 급증, 규제의 복잡화로 인해 법무 부서는 증거 공개 워크플로의 현대화와 AI 대응 검토 도구의 채택을 강요하고 있습니다. 대기업은 급등하는 소송 비용의 헤지로 고급 분석을 검토하고 중소기업은 인프라 비용을 전액 부담하지 않고 동등한 기능을 이용하기 위해 관리 서비스 전문가에게 아웃소싱하고 있습니다. 클라우드 퍼스트 아키텍처로의 전환이 진행되고 있으며, 종량 과금제의 경제성과 하이브리드 워크에 있어서 협업 요구의 고조가 도입의 뒷받침을 하고 있습니다. 북미는 플랫폼의 혁신과 판례의 성숙도에 있어서 규모의 우위성을 유지하고 있지만, 아시아태평양이 2자리수의 성장을 이루고 있는 것은 현지의 시행 체제와 국경을 넘은 상거래가 융합해, 벤더에게 새로운 수익원을 창출하고 있는 것을 뒷받침하고 있습니다. 투명성이 높은 가격 설정, 간소화된 사용자 경험, 새로운 인증 기준에 대응하는 설명 가능한 AI 기능으로 기존 기업에 도전하는 클라우드 네이티브의 진입으로 경쟁의 치열성이 증가하고 있습니다.

일반 인공지능 및 대규모 언어 모델 도구를 통해 인간의 검토 시간을 최대 70%까지 줄였으며, 법률 사무소는 보다 가치 있는 광고주로 직원을 재배치할 수 있습니다. CS Disco의 세실리아 어시스턴트는 감사 추적을 저장하면서 대화형 애널리틱스가 반복적인 태깅을 억제하는 방법을 설명합니다. 미국 규칙 707의 개정안에서는 AI의 출력이 인정되기 전에 변호사는 정확성뿐만 아니라 신뢰성을 입증해야 합니다. 따라서 벤더는 설명 가능한 랭킹, 캘리브레이션 지표, CoC 로깅 등 투명성이 높은 모델 거버넌스 프레임워크에 투자해, 허용성을 손상시키지 않고 도입의 기세를 유지하려고 하고 있습니다. 이러한 보증 레이어가 성숙함에 따라 효율성과 변호성을 양립시키는 전자 증거개시 시장 진출 기업은 경쟁력을 확대할 것으로 보입니다.

Microsoft Teams만으로 연간 1조 페이지 이상을 처리하고 있으며 증거 공개 팀이 직면하고 있는 규모의 과제가 부각되고 있습니다. 하이브리드 작업 방식은 증거 저장소를 개인 기기 및 소비자 앱으로 확장하고 기업은 정보 거버넌스의 기본을 검토해야 합니다. 클라우드 네이티브 벤더는 Slack, Google Vault, Microsoft 365에서 직접 데이터를 끌어내는 API 구동 커넥터로 복잡성을 해결하고 법적 보류 및 수집 워크플로우를 자동화합니다. 그러나 새로운 데이터 파이프가 늘어날 때마다 프라이버시 침해 공격 대상이 확대되기 때문에 고객은 제로 지식 암호화와 지역별 데이터 레지던시 제어를 요구하고 있습니다. 따라서 전자 증거개시 시장은 단일 사용자 인터페이스 하에서 정책 구현, 협력 검색, AI를 활용한 엔티티 추출을 통합한 플랫폼에 끌려가고 있습니다.

GB당 15-30달러의 엔트리 레벨 처리 요금은 데이터 양 증가와 섞여 프로젝트 전체의 지출을 많은 중소기업의 예산을 초과하고 있습니다. 클라우드 라이선싱은 초기 투자 금액을 줄이는 것, 스토리지, 고급 분석, 검토 전문가 등 다운스트림 비용은 여전히 큽니다. KLDiscovery와 같은 부채를 가진 서비스 제공업체는 공급업체가 밸런스 시트를 보강하려고 하는 동안 마진 압력이 가격 설정을 통해 어떻게 파급되는지를 보여줍니다. 합리적인 가격의 자동화, 투명한 구독 티어, 커뮤니티 기반 교육 리소스는 시장 성장 억제요인을 둔화시킬 수 있지만, 시장의 이분화는 계속되고 있으며, 기업 고객은 풀 서비스 플랫폼에 끌려가고, 비용에 중점을 둔 사용자는 기본 키워드 검색을 기본으로 합니다.

2024년 전자 증거개시 시장 점유율은 매니지드 서비스가 46.30%를 차지하고 처리, 호스팅, AI 모델 튜닝 등 노동 집약적인 태스크 아웃소싱을 선호하는 기업의 의향을 반영했습니다. 공급자는 인프라와 인력을 중앙 집중화하여 규모의 경제를 실현하고 고객은 고정비를 변동비로 전환할 수 있습니다. 권고 및 배포 후 서비스는 CAGR 10.15%로 예측되며 멀티클라우드 난립을 억제하고 책임을 지고 AI를 통합하기 위한 거버넌스 로드맵이 필요한 조직을 매료하고 있습니다. 증거 공개 요청이 모바일 채팅, 클라우드 아카이브, 소셜 피드에 이르면서 기업은 단일 서비스 수준 계약을 통한 엔드 투 엔드 책임(법적 보류, 수집, 분석, 생성)에 중점을 두게 됩니다. 따라서 전자 증거개시 업계에서는 단편적인 작업 가격 설정보다 성과 기반 서비스 번들을 판매하는 공급업체가 평가되고 있습니다.

또한 Managed Specialists는 데이터 최소화 플레이북 및 특권 심사 모델과 같은 조사 촉진 기능을 통합합니다. 이러한 차별화 요인은 심사 사이클이 단축되고 증거 능력이 엄격하게 묻는 시대에 방어력이 강화됩니다. Exterro가 첸나이에 신설한 법의학 실험실로 대표되는 것처럼 고성장 지역에 진출하는 공급자는 현지 인력 풀을 활용하여 24시간 365일 지원을 확대하여 배달 비용을 절감하고 있습니다.

E 디스커버리 및 조기 케이스 평가 제품군은 2024년 매출 점유율 34%로 소프트웨어 카테고리를 선도했지만, AI 주도 검토 및 분석은 이 부문 내에서 가장 빠른 CAGR 10.40%를 나타낼 것으로 예측됩니다. 고객은 조달 기준을 원시 처리 능력에서 플랫폼이 얼마나 신속하게 캐스트 디얼 핫스팟, 감정 피벗 및 특권 이상을 표면화할 수 있는지에 대한 인사이트 벨로시티로 이동하고 있습니다. Relativity의 클라우드 채용률 75%로의 전환은 SaaS 전달이 기능 배포를 가속화하고 집중적인 머신러닝 워크로드의 컴퓨팅을 확장하는 방법을 보여줍니다. 반면, 법률 홀드 및 프로덕션을 전문으로 하는 포인트 솔루션 공급업체는 API 게이트웨이를 통합하여 보다 광범위한 케이스 관리 스택에 원활하게 통합함으로써 플랫폼이 통합되어도 틈새 관련성을 유지합니다.

AI 분석과 관련된 전자 증거개시 시장 규모는 설명 가능성 대시보드 및 바이어스 테스트 프로토콜에 의해 점점 보호되고 있습니다. 구매자는 구성 가능한 신뢰성 임계값과 법정에서 프레젠테이션을 지원하는 내러티브 요약을 찾고 있습니다. 투명성이 뛰어난 AI와 세분화된 비용 추적 도구를 패키징한 벤더는 리스크와 재무 관리의 양면에서 차별화를 도모해 예산 감독하에 있는 기업 고문에 어필하고 있습니다.

북미는 확립된 판례, 왕성한 소송, 서비스 제공업체의 밀집한 에코시스템을 강점으로 2024년 매출에 41.20% 공헌했습니다. 이 지역에 본사를 둔 시장 리더, 마이크로소프트, IBM, 오픈 텍스트, 레라티비티는 전 세계적으로 파급되는 제품 로드맵을 설정하고 있습니다. 그러나 클라우드 도입이 포화 상태에 가까워지고 법률 사무소가 AI 도입을 최종 결정함에 따라 성장이 완만해지고 있습니다. 공급자는 현재 예측 결과 모델링 및 자동화된 권한 스크리닝과 같은 부가가치 모듈을 강조하고 지갑 공유를 보호하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 11.40%를 나타낼 것으로 예측되며 기업 책임에 관한 법규제의 확대와 크로스보더 이슈 증가에 의해 뒷받침됩니다. 일본에서는 증거공시의 규정이 한정적이며 변호사와 의뢰인 간의 은닉 특권이 없기 때문에 현지 데이터 처리와 해외 애널리틱스 허브를 융합시킨 하이브리드 워크플로우에 대한 수요가 높아지고 있습니다. 호주, 인도, 싱가포르는 현지 정보 공개 규범을 세계 모범 사례와 일치시키는 규제의 조화를 주도하고 플랫폼 도입을 가속화하고 있습니다. APAC에서 성공을 거두는 공급업체는 사용자 인터페이스를 현지화하고 지역 데이터센터를 제공하며 국내 인시던트 응답 팀을 육성함으로써 주권에 대한 우려를 충족합니다.

유럽에서는 GDPR(EU 개인정보보호규정)에 의한 데이터 전송의 제약을 극복하면서 꾸준한 도입이 계속되고 있습니다. 지역 내 호스팅, 세분화된 동의 관리, 자동화된 PII 재편집을 제공하는 제공업체가 경쟁 입찰에 우선합니다. 영국의 규칙이 브레그지트 후에 괴리되었기 때문에 법역마다 보존과 삭제의 정책을 바꿀 수 있는 모듈식의 컴플라이언스 엔진이 요구되고 있습니다. 라틴아메리카와 중동 및 아프리카는 아직 발전도상이지만 미국 당국과의 규제협력이 활발해지고 있으며, 다국적기업은 강제조치가 실현되기 전에 정보공개 인프라를 사전 도입하는 경향이 있습니다.

The electronic discovery market size stood at USD 16.58 billion in 2025 and is projected to reach USD 26.12 billion in 2030, reflecting a 9.51% CAGR over the forecast period.

Heightened digitization of legal processes, the rapid rise in multi-format data, and mounting regulatory complexity are pushing legal departments to modernize discovery workflows and adopt AI-enabled review tools. Large enterprises view advanced analytics as a hedge against spiraling litigation costs, while small and mid-sized firms outsource to managed-service specialists to access comparable capabilities without bearing full infrastructure costs. Deployment preferences continue to swing toward cloud-first architectures, encouraged by pay-as-you-go economics and by heightened collaboration needs in hybrid work settings. North America retains scale advantages in platform innovation and case-law maturity, yet Asia-Pacific's double-digit expansion underscores how local enforcement regimes and cross-border commerce are converging to create fresh revenue pools for vendors. Competitive intensity is rising as cloud-native entrants challenge incumbents with transparent pricing, streamlined user experiences, and explainable AI features that address emerging admissibility standards.

Generative AI and large-language-model tooling now slash human review hours by up to 70%, enabling law firms to redeploy staff toward higher-value advocacy. CS Disco's Cecilia assistant illustrates how conversational analytics curtail repetitive tagging while preserving audit trails . Courts are concurrently tightening evidentiary standards: proposed U.S. Rule 707 amendments will oblige counsel to demonstrate reliability, not just accuracy, before AI outputs become admissible. Vendors are therefore investing in transparent model governance frameworks-explainable ranking, calibration metrics, and chain-of-custody logging-to sustain adoption momentum without jeopardizing admissibility. As these assurance layers mature, electronic discovery market participants that marry efficiency with defensibility will widen their competitive moat.

Microsoft Teams alone processes more than 1 trillion pages annually, underscoring the scale challenge facing discovery teams. Hybrid work patterns extend evidence repositories into personal devices and consumer apps, compelling enterprises to revisit information-governance baselines. Cloud-native vendors are countering complexity through API-driven connectors that pull data directly from Slack, Google Vault, and Microsoft 365, automating legal hold and collection workflows. Yet every new data pipe expands the attack surface for privacy breaches, so clients demand zero-knowledge encryption and region-specific data-residency controls. The electronic discovery market is therefore gravitating toward platforms that integrate policy enforcement, federated search, and AI-powered entity extraction under a single user interface.

Entry-level processing fees of USD 15-30 per GB intersect with rising data volumes, pushing overall project spend beyond many small-firm budgets. While cloud licensing reduces upfront capital outlay, downstream expenses-storage, advanced analytics, specialist review talent-remain material. Debt-laden service providers such as KLDiscovery illustrate how margin pressure can ripple through pricing as vendors seek to shore up balance sheets. Affordable automation, transparent subscription tiers, and community-based training resources could blunt the restraint, but market bifurcation persists, with enterprise clients gravitating to full-service platforms and cost-sensitive users defaulting to rudimentary keyword searches.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Managed services accounted for a 46.30% electronic discovery market share in 2024, reflecting corporate preference for outsourcing labor-intensive tasks such as processing, hosting, and AI model tuning. Providers achieve economies of scale by centralizing infrastructure and talent, letting clients convert fixed costs into variable spend. Advisory and post-implementation services, forecast at a 10.15% CAGR, attract organizations that need governance roadmaps to tame multicloud sprawl and to embed AI responsibly. As discovery requests span mobile chat, cloud archives, and social feeds, enterprises value end-to-end accountability-legal hold, collection, analytics, and production-under a single service-level agreement. The electronic discovery industry therefore rewards vendors that market outcome-based service bundles over piecemeal task pricing.

Managed specialists also integrate investigation accelerators such as data-minimization playbooks and privilege-screening models. These differentiators shorten review cycles and bolster defensibility in an era of stricter admissibility scrutiny. Providers expanding into high-growth geographies, exemplified by Exterro's new forensics lab in Chennai, leverage local talent pools to scale 24/7 support and lower delivery costs.

E-discovery and early case-assessment suites led the software category with 34% revenue share in 2024, yet AI-driven review and analytics is projected to rise at 10.40% CAGR, the fastest within the segment. Customers are shifting procurement criteria from raw processing horsepower toward insight velocity-how quickly a platform can surface custodial hot spots, sentiment pivots, or privilege anomalies. Relativity's move to a 75% cloud adoption ratio illustrates how SaaS delivery accelerates feature rollout and scales compute for intensive machine-learning workloads. Meanwhile, point-solution vendors that specialize in legal hold or production are embedding API gateways to integrate seamlessly into broader case-management stacks, preserving niche relevance even as platforms consolidate.

The electronic discovery market size attached to AI analytics is increasingly defended by explainability dashboards and bias-testing protocols. Buyers demand configurable confidence thresholds and narrative summaries that support courtroom presentation. Vendors that package transparent AI with granular cost-tracking tools differentiate on both risk and financial stewardship, appealing to corporate counsel under budget oversight.

The Electronic Discovery Market Report is Segmented by Service (Professional Services, Managed Services, Advisory & Post-Implementation Services), Software (E-Discovery and Early Case Assessment, Legal Hold and Preservation, and More), Deployment (SaaS/Cloud, On-Premise, Hosted/Hybrid), End User (Government and Public Sector, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 41.20% revenue in 2024 on the strength of established case law, prolific litigation, and a dense ecosystem of service providers. Market leaders headquartered in the region-Microsoft, IBM, OpenText, and Relativity-set product roadmaps that ripple globally. Growth, however, is moderating as cloud adoption approaches saturation and law firms finalize AI rollouts. Providers now emphasize value-add modules such as predictive outcome modeling and automated privilege screening to defend wallet share.

Asia-Pacific is forecast to grow at 11.40% CAGR through 2030, buoyed by expanding corporate-liability statutes and increasing cross-border deal activity. Japan's limited discovery provisions and absence of attorney-client privilege create demand for hybrid workflows that blend local data processing with offshore analytics hubs. Australia, India, and Singapore spearhead regulatory harmonization that aligns local disclosure norms with global best practices, accelerating platform uptake. Vendors succeeding in APAC localize user interfaces, offer regional data centers, and cultivate in-country incident-response teams to satisfy sovereignty concerns.

Europe continues steady adoption while navigating GDPR-driven constraints on data transfer. Providers offering in-region hosting, fine-grained consent management, and automated PII redaction earn preference in competitive bids. Post-Brexit divergence in UK rules demands modular compliance engines capable of toggling retention and deletion policies per jurisdiction. Latin America and Middle East and Africa remain nascent, yet rising regulatory cooperation with U.S. agencies is tipping multinational corporations to pre-deploy discovery infrastructure before enforcement actions materialize.