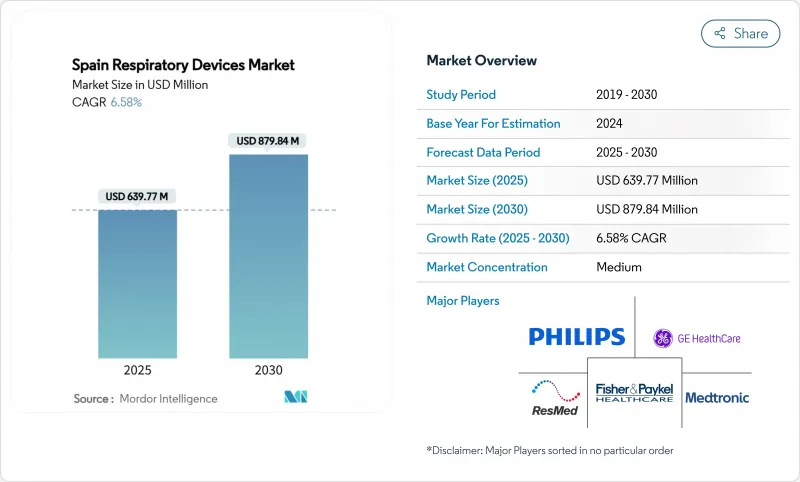

스페인의 호흡기 시장 규모는 2025년에 6억 3,977만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 6.58%를 나타낼 것으로 예측되며 2030년에 8억 7,984만 달러로 성장할 전망입니다.

견고한 공공 의료 보장, 가정 기반 치료의 급속한 확대, 치료 장비의 지속적인 혁신이 이러한 성장 궤도를 뒷받침합니다. 가속화된 인구 고령화는 인공호흡기와 산소 시스템에 대한 수요를 증가시키는 한편, 만성 폐쇄성 폐질환(COPD) 및 수면 무호흡증의 증가하는 부담은 잠재적 환자 풀을 확대합니다. 현지 제조 및 디지털 헬스 도입을 촉진하는 정부 인센티브는 수익 성장을 더욱 지원합니다. 동시에 강화된 규제 비용, 인력 부족, 강화된 환경 규제는 단기적 성장 동력을 약화시키지만 기존 공급업체의 규모의 경제를 촉진합니다.

COPD는 스페인 성인의 11.8%에게 영향을 미치며 호흡기 질환으로 인한 병원 퇴원 건수를 35.9% 증가시켰습니다. 이러한 추세는 인공호흡기, 분무기, 폐활량계의 장기적 판매를 강화합니다. 수면 무호흡증은 치매 위험이 높은 고령자의 거의 절반에 영향을 미치지만 여전히 진단이 크게 부족한 상태로, 양압 호흡기 및 가정용 수면 검사 키트에 대한 새로운 성장 여지를 창출하고 있습니다. 100% 민감도를 가진 결핵 PCR 키트의 발전은 공중보건 실험실에서 휴대용 진단 시스템에 대한 수요를 확대합니다. 이러한 역학적 변화들은 종합적으로 기기 교체 주기를 연장하고 스페인의 호흡기 시장을 급성 치료 환경을 훨씬 넘어 확장시킵니다.

90세 이상 인구 집단은 2013년부터 2023년까지 58.29% 증가하여 60만 8,321명에 달했습니다. 142.35%의 고령화 지수는 가정용으로 맞춤화된 비침습적 인공호흡기, 산소 농축기, 기도 청소 장치에 대한 수요 증가를 부각시킵니다. 2039년까지 1인 가구가 전체 가구의 33.5%를 차지할 것으로 예상됨에 따라, 제조사들은 노년층이 독립성을 유지할 수 있도록 직관적인 인터페이스와 원격 모니터링 기능을 우선시하고 있습니다. 이미 83%의 의료기관이 비침습적 인공호흡기 전용실을 운영 중이며, 이는 노화 관련 질환에 대한 지속적인 구매 수요를 시사합니다. 이러한 인구학적 현실은 스페인 호흡기 시장에 구조적 성장을 내재화하고 있습니다.

최근 공공 보건 지출에도 불구하고 병원들은 엄격한 예산 상한선 아래 운영되어 프리미엄 인공호흡기와 AI 기반 모니터의 조달 주기가 길어지고 있습니다. 지역 당국은 입증된 중급 제품을 선호하는 ‘질 조정 생명 연한당 비용(QALY)’ 기준을 적용합니다. 카나리아 제도가 의료 기기에 대한 IGIC 세율을 0%로 인하한 결정은 어떻게 표적 재정 정책이 접근성 제약을 완화할 수 있는지 보여줍니다. 전국적 부가가치세 감면이 없는 상황에서 가격 민감도는 스페인 호흡기 시장의 즉각적 성장을 계속 제한할 것이다.

치료용 기기는 2024년 매출의 56.54%를 차지했으며, 이는 지속적 기도 압력 시스템, 인공호흡기 및 산소 농축기에 대한 임상적 선호도를 반영합니다. KPAP과 같은 양압 호흡기 혁신은 수면 무호흡증 환자의 편안함과 치료 순응도를 향상시켜 마스크 및 튜브의 반복 구매를 유도합니다. 국가 회복 계획 하에 자금을 지원받는 인공호흡기 개발 프로그램은 가격 장벽을 낮추어 시장 침투를 더욱 확대합니다. 분무기는 만성 폐쇄성 폐질환(COPD) 관리에 여전히 중요하며, 휴대용 산소 시스템은 증가하는 재택 치료 수요를 지원합니다. 스페인 치료용 호흡기 시장 규모는 고령화 관련 동반 질환 증가와 함께 성장할 것으로 전망됩니다.

진단 및 모니터링 기기는 시장 규모는 작지만 7.65%의 가장 빠른 연평균 성장률(CAGR)을 기록하고 있습니다. 원격의료 확대 속에서 연결형 폐활량계, 웨어러블 카프노그래프, 가정용 수면 검사기 등이 인기를 얻고 있습니다. 호흡기 질환의 조기 진단은 입원률을 낮춰 선별 검사 도구에 대한 정책적 지원을 강화합니다. 그 결과 진단 플랫폼이 스페인 호흡기 기기 시장에서 점유율을 높여가고 있습니다.

The Spain Respiratory Devices Market size is estimated at USD 639.77 million in 2025, and is expected to reach USD 879.84 million by 2030, at a CAGR of 6.58% during the forecast period (2025-2030).

Robust public health coverage, the rapid expansion of home-based care, and continuous innovation in therapeutic equipment underpin this trajectory. Accelerated population ageing intensifies demand for ventilators and oxygen systems, while a growing burden of chronic obstructive pulmonary disease (COPD) and sleep apnea broadens the addressable patient pool. Government incentives that promote local manufacturing and digital health adoption further support revenue growth. At the same time, heightened regulatory costs, workforce shortages, and stricter environmental rules temper short-term momentum yet encourage scale advantages for established suppliers.

COPD affects 11.8% of Spanish adults and drove a 35.9% rise in hospital discharges for respiratory diseases, a pattern that strengthens long-term sales of ventilators, nebulizers, and spirometers. Sleep apnea remains widely underdiagnosed despite affecting nearly half of older adults at elevated dementia risk, creating fresh headroom for positive airway pressure devices and home sleep testing kits. Advances in tuberculosis PCR kits with 100% sensitivity expand demand for portable diagnostic systems in public health laboratories. Together, these epidemiological shifts lengthen device replacement cycles and enlarge the Spain respiratory devices market far beyond acute care settings.

The cohort aged 90 years or older swelled 58.29% from 2013 to 2023, reaching 608,321 citizens. An ageing index of 142.35% highlights growing demand for non-invasive ventilation, oxygen concentrators, and airway clearance devices tailored to home use. With single-person households forecast to account for 33.5% of all households by 2039, manufacturers prioritise intuitive interfaces and remote monitoring features that let older adults remain independent. Hospitals already maintain dedicated non-invasive ventilation units in 83% of facilities, signalling sustained procurement for ageing-related disorders. These demographic realities embed structural growth in the Spain respiratory devices market.

Hospitals operate under strict budget ceilings even after recent public-health outlays, causing extended procurement cycles for premium ventilators and AI-enabled monitors. Regional authorities lean on cost-per-quality-adjusted-life-year thresholds that favour proven mid-range products. The Canary Islands' decision to reduce its IGIC tax on medical devices to zero illustrates how targeted fiscal levers can mitigate affordability constraints. In the absence of nationwide VAT relief, price sensitivity will continue to cap immediate growth in the Spain respiratory devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Therapeutic devices accounted for 56.54% of 2024 revenue, reflecting a clinical preference for continuous airway pressure systems, ventilators, and oxygen concentrators. Positive airway pressure innovations such as KPAP enhance comfort and adherence among sleep apnea patients, locking in recurring mask and tubing sales. Ventilator development programs funded under national recovery schemes lower price barriers, further widening penetration. Nebulizers remain critical for COPD management, while portable oxygen systems support growing homecare demand. The Spain respiratory devices market size for therapeutic equipment is projected to rise in tandem with ageing-linked comorbidities.

Diagnostic and monitoring devices hold a smaller base but record the fastest 7.65% CAGR. Connected spirometers, wearable capnographs, and home sleep tests gain popularity amid wider telehealth rollouts. Early diagnosis of respiratory disease lowers hospital admissions, strengthening policy support for screening tools. As a result, diagnostic platforms capture a rising share of the Spain respiratory devices market.

The Spain Respiratory Devices Market Report is Segmented by Product Type (Diagnostic & Monitoring Devices, Therapeutic Devices, Disposables), Indication (COPD, Asthma, Sleep Apnea, Cystic Fibrosis, Tuberculosis, Other Respiratory Disorders), End User (Hospitals and Clinics, Homecare Settings, Ambulatory Surgical Centers, Long-Term Care Facilities), and Geography (Spain). The Market Forecasts are Provided in Terms of Value (USD).