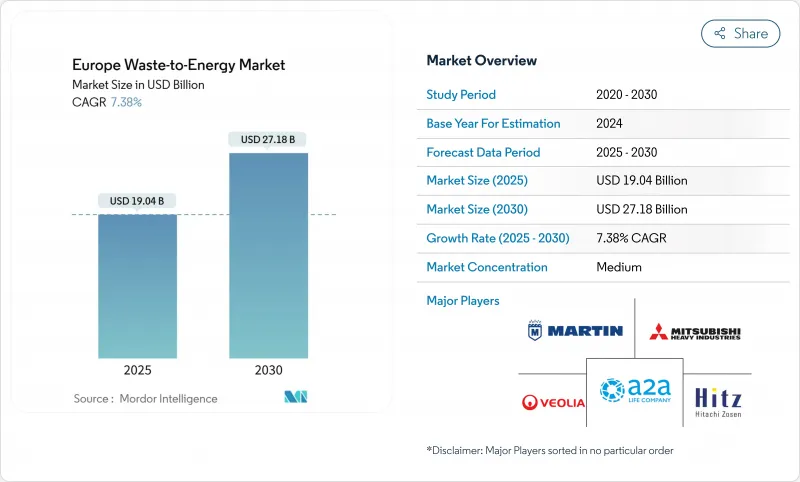

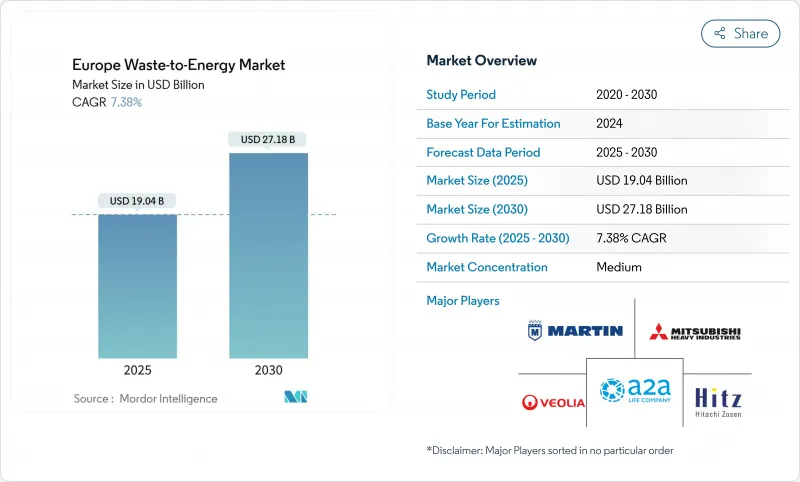

유럽의 폐기물 에너지화(WtE) 시장 규모는 2025년에 190억 4,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 7.38%로, 2030년에는 271억 8,000만 달러에 달할 것으로 예상됩니다.

EU의 폐기물 및 기후에 관한 지침의 정책적 무결성, 석탄 용량의 축소, 매립 게이트 요금의 상승으로 시설 이용률이 상승할 것으로 예상됩니다. EU의 탄소 국경 조정 메커니즘(CBAM)과 같은 탄소 연동 인센티브가 새로운 수익원을 창출하는 한편, 북유럽과 중·동유럽에서는 지역 난방의 건설이 진행되어 프로젝트의 융통성이 향상됩니다. 750t/d를 넘는 대규모 플랜트는 규모가 커질수록 분리 회수에 대응한 개수 비용이 낮아 EU 혁신 펀드에 대한 자본 접근이 용이해지기 때문에 기세가 증가하고 있습니다. 독일, 이탈리아, 폴란드, 북유럽, 영국에서는 도시 지역의 배출량에 대한 사회적 민감성과 도매 전력 가격의 연화가 성장을 억제하고 있기 때문에 신설 파이프라인이 좌절하지 않습니다. 그 결과, 유럽의 폐기물 에너지화(WtE) 시장은 매립지 전환을 추진하는 확고한 용량 공급자로서의 역할을 굳히고 있습니다.

이 지령은 2035년까지 지방자치단체의 매립처분량의 상한을 10%로 설정하여 회원국에 잔여폐기물의 흐름에 대한 열공급능력의 추가를 촉구하고 있습니다. 매립량은 2010년부터 2020년 사이에 27.5% 감소했지만, 14개국이 위반의 위험을 안고 있어 새로운 소각·혐기성 소화 플랜트의 조달을 가속시키고 있습니다. 폴란드와 루마니아는 턴키 시설에 자금을 제공하기 위해 EU의 결속 기금을 선호하고 마감일에 맞추기 위해 승인 창을 압축합니다. 에너지 회수는 폐기물 처리보다 상위에 위치하기 때문에 지자체는 프로젝트 수익을 향상시키는 높은 게이트 수수료를 정당화할 수 있습니다. 동유럽 당국은 폐기물 에너지화(WtE)을 매립지의 전환과 동계 피크시의 전력 부족에 대한 이중 해결책으로 생각하고 있으며, 유럽의 폐기물 에너지화(WtE) 시장 전체 수요를 뒷받침하고 있습니다.

CBAM은 2026년에 본격적으로 시동하여 폐기물 에너지화(WtE)가 화석 발전을 대체할 때 회피되는 배출량을 수익화합니다. 더 낮은 탄소 강도를 나타내는 시설은 산업계 구매자가 포기해야 하는 프리미엄 증서를 획득하고 공장 수익을 효과적으로 보조합니다. EU ETS의 가격이 80유로/tCO2를 상회하는 경향이 있기 때문에 증서는 신규 건설의 내부 수익률을 높입니다. 개발자는 탄소 계수를 검증하기 위해 고급 배기 가스 처리를 통합하기 시작했습니다. 탄소 배출량이 많은 전력을 수입하는 업체는 동등한 과세를 받기 때문에 이 구조는 간접적으로 국내 사업자를 보호하고 유럽의 폐기물 에너지화(WtE) 시장을 더욱 강화합니다.

환경보호단체는 기후 변화 대책에 관한 2024년 유럽인권재판소의 판결을 허가에 이의를 제기하고 승인 프로세스를 장기화시켰습니다. 암스테르담에서는 주민의 청원에 의해 발전소 계획이 중지되어 마드리드에서도 같은 반발에 직면하고 있습니다. 법적 불확실성은 대출자의 리스크 프리미엄을 높이고 개발자는 소각 전에 철저한 재활용 노력을 증명해야 합니다. 코펜하겐과 같은 공공 부문의 소유자는 사회적 수용성이 높지만 민간 회의에는 시민 감시위원회가 포함되는 경우가 많습니다. 이러한 역학은 밀집도시에서의 프로젝트 전개를 늦추고 유럽의 폐기물 에너지화(WtE) 시장에서 단기적인 용량 증가를 억제하고 있습니다.

화력발전 루트는 2024년 부문 수익의 60%를 창출했습니다. 가스화 및 열분해의 파일럿 플랜트는 현재 EU 혁신 펀드의 지원을 받고 있으며 포획 대응 설계를 정책이 선호하고 있음을 보여줍니다. 혐기성 소화가 2030년까지 35bcm라는 REPowerEU의 바이오메탄 목표에 부합하기 때문에 생물학적 클러스터는 CAGR 12.2%를 나타낼 전망입니다. 전처리 선별과 유기물의 소화, 쓰레기 고형 연료의 연소를 조합한 통합형 시설은 잔여 매립량을 삭감하고 순환형 사회의 지표를 높입니다. 생물학적 솔루션과 관련된 유럽의 폐기물 에너지화(WtE) 시장 규모는 2025년 54억 달러에서 2030년 82억 달러로 확대될 것으로 예상되며, 저탄소 가스에 대한 투자자의 의지를 뒷받침하고 있습니다.

히타치 조선 이노바, 마틴 GmbH, 밥콕 & 윌콕스 등의 화력 공급업체는 화격자 라인을 모듈화하고 옥시 연료 포착 포트를 통합하여 대응하고 있습니다. 프로젝트 스폰서는 현재 산업 배출 지령의 상한을 초과하는 배기 가스 처리를 설계하고 나중에 회수 통합의 리드 타임을 단축하고 있습니다. 생물기술 공급자는 소규모 지자체에 적합한 컨테이너형 소화조에 주력하여 대응 가능한 용적을 확대하고 있습니다. 공기 유량, 슬래그 처리, 소화조 체류 시간을 조정하는 디지털 제어로 가동률이 92% 가까이 향상되어 유럽의 폐기물 에너지화(WtE) 시장 전체의 수익 회복력이 강화됩니다.

도시고형폐기물(MSW)은 성숙한 수집물류와 최저처분량의 의무화로 2024년에는 처리량의 62%를 차지했습니다. 그러나 농가가 질산지령에 대응하기 위해 배뇨나 작물잔사를 수익화하고 있기 때문에 농업·농산업잔사는 매년 11.4% 증가하고 있습니다. 유럽의 폐기물 에너지화(WtE) 시장 규모는 이탈리아와 덴마크의 가스 그리드 인젝션 프리미엄에 의해 지원되며 2030년까지 67억 달러에 달할 가능성이 있습니다.

육류 가공의 장물과 치즈 유청은 투자 회수 기간을 12개월 미만으로 단축할 수 있는 고수율의 바이오가스 공급원으로, 협동조합 소유의 소화장치를 끌어들이고 있습니다. 하수 슬러지의 양은 도시 지역의 인구 증가와 폐수 규제의 강화에 따라 증가하고, 수도 사업체가 에너지 자급을 위해 슬러지 소각로를 설치하도록 촉구하고 있습니다. 포장재나 섬유제품 등의 상업 및 산업용 리사이클 원료는 발열량이 높지만 PVC나 금속을 제거하기 위한 프리소트 로봇이 필요합니다. 혼합투입전략은 발열량 변동을 균등화하고 연간 공급망을 확보함으로써 유럽의 폐기물 에너지화(WtE) 시장 전체에서 플랜트 이용률을 높입니다.

유럽의 폐기물 에너지화(WtE) 시장 보고서는 기술별(물리적, 열적, 생물학적), 폐기물 유형별(도시 고형 폐기물, 산업 폐기물, 농업·농산업 잔류물, 하수 슬러지 등), 에너지 출력별(전기, 열, 기타), 최종 사용자별(산업용 캡티브 플랜트, 운송 연료 유통업체 등), 국가별(독일, 영국, 이탈리아, 프랑스, 북유럽 국가 등)으로 분류됩니다.

The Europe Waste-to-Energy Market size is estimated at USD 19.04 billion in 2025, and is expected to reach USD 27.18 billion by 2030, at a CAGR of 7.38% during the forecast period (2025-2030).

Policy alignment across EU waste and climate directives, shrinking coal capacity, and rising landfill gate fees lift facility utilization rates. Carbon-linked incentives such as the EU Carbon Border Adjustment Mechanism (CBAM) create new revenue streams while district-heating build-outs in Nordic and Central-Eastern Europe improve project bankability. Large-scale plants above 750 tpd gain momentum because scale lowers capture-ready retrofit costs and eases EU Innovation Fund capital access. Public sensitivity toward urban emissions and wholesale power-price softness temper growth have not derailed newbuild pipelines in Germany, Italy, Poland, the Nordics, and the United Kingdom. As a result, the European waste-to-energy market is consolidating its role as a firm capacity provider that drives landfill diversion.

The Directive caps municipal landfills at 10% by 2035, pushing member states to add thermal capacity for residual waste streams. Landfilled volumes fell 27.5% between 2010-2020, yet 14 nations risk infringement, accelerating procurement for new incineration and anaerobic digestion plants . Poland and Romania prioritize EU cohesion funds to finance turnkey facilities, compressing approval windows to meet the deadline. Because energy recovery sits above disposal in the hierarchy, municipalities justify higher gate fees that improve project returns. Eastern European authorities see waste-to-energy as a twin answer to landfill diversion and winter-peak electricity deficits, underpinning demand across the European waste-to-energy market.

CBAM's full launch in 2026 monetizes avoided emissions when waste-to-energy electricity displaces fossil generation. Facilities demonstrating lower carbon intensity earn premium certificates that industrial buyers must surrender, effectively subsidizing plant revenues. With EU ETS prices trending above EUR 80/tCO2, certificates enhance internal rates of return for new builds. Developers have started embedding advanced flue-gas treatment to verify carbon factors. The mechanism indirectly shields domestic operators because importers of carbon-heavy electricity face equivalent levies, further strengthening the European waste-to-energy market.

Environmental groups leverage the 2024 European Court of Human Rights ruling on climate action to contest permits, lengthening approval processes. Amsterdam halted a planned plant after resident petitions, while Madrid faces similar pushback. Legal uncertainties raise lender risk premiums and oblige developers to prove exhaustive recycling efforts before incineration. Although public-sector owners such as Copenhagen record higher social acceptance, private concessions increasingly include citizen oversight boards. These dynamics slow project roll-outs in dense cities and curb near-term capacity additions within the European waste-to-energy market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Thermal routes generated 60% of segment revenue in 2024, driven by established grate combustion fleets spread across 19 EU members. Gasification and pyrolysis pilots now secure EU Innovation Fund support, indicating policy preference for capture-ready designs. The biological cluster grows at a 12.2% CAGR as anaerobic digestion aligns with the REPowerEU biomethane goal of 35 bcm by 2030. Integrated sites that marry front-end sorting with digestion for organics and combustion for refuse-derived fuel cut residual landfill volumes, boosting circularity metrics. The Europe waste-to-energy market size linked to biological solutions is projected to climb from USD 5.4 billion in 2025 to USD 8.2 billion in 2030, underscoring investor appetite for low-carbon gases.

Thermal suppliers such as Hitachi Zosen Inova, Martin GmbH, and Babcock & Wilcox respond by modularising grate lines and embedding oxy-fuel capture ports. Project sponsors now design flue-gas treatment to exceed Industrial Emissions Directive ceilings, shortening later capture integration lead times. Biological technology providers focus on containerized digesters suitable for small municipalities, broadening addressable volumes. Digital controls that adjust air flow, slag handling, and digester retention times raise availability by close to 92%, enhancing revenue resilience across the European waste-to-energy market.

Municipal solid waste (MSW) represented 62% throughput in 2024, thanks to mature collection logistics and minimum disposal mandates. However, agricultural and agro-industrial residues grow 11.4% annually as farmers monetise manure and crop residues to meet the nitrates directives. The European waste-to-energy market size attributable to agricultural feedstock could reach USD 6.7 billion by 2030, supported by gas-grid injection premiums in Italy and Denmark.

Meat-processing offal and cheese whey supply high-yield biogas streams that cut payback to under 12 months, attracting co-operative-owned digesters. Sewage sludge volumes climb with urban population growth and tighter wastewater rules, prompting water utilities to install sludge incinerators for energy self-sufficiency. Commercial and industrial recyclables such as packaging and textiles offer higher calorific value but demand pre-sort robotics to remove PVC and metals. Blended-feed strategies even out calorific swings and secure year-round supply chains, enhancing plant utilization across the European waste-to-energy market.

The Europe Waste-To-Energy Market Report is Segmented by Technology (Physical, Thermal, and Biological), Waste Type (Municipal Solid Waste, Industrial Waste, Agricultural and Agro-Industrial Residues, Sewage Sludge, and Others), Energy Output (Electricity, Heat, and More), End-User (Industrial Captive Plants, Transport Fuel Distributors, and More), and Country (Germany, United Kingdom, Italy, France, Nordic Countries, and More).