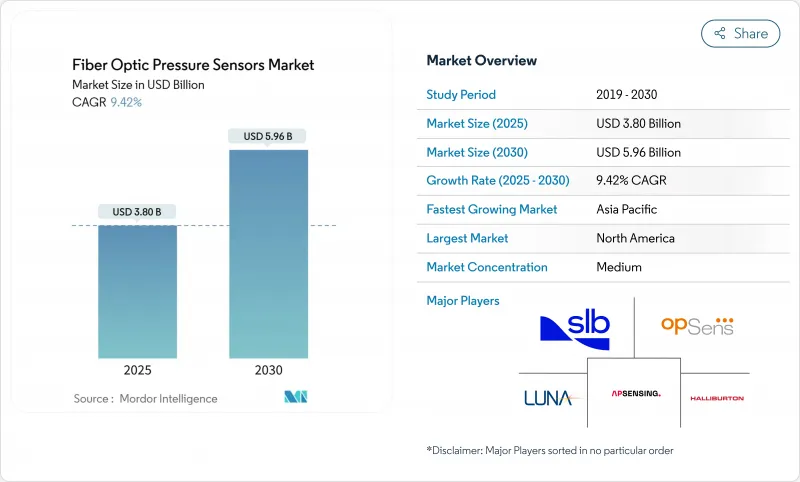

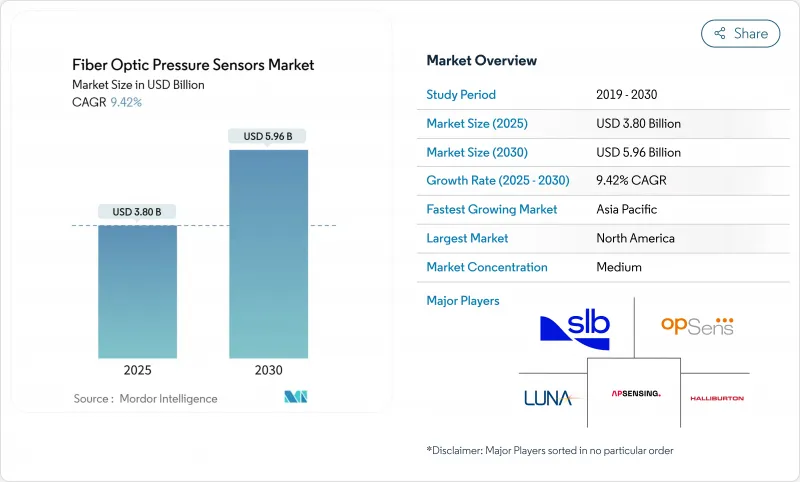

광섬유 압력 센서 시장 규모는 2025년에 38억 달러로 평가되고, 2030년에는 59억 6,000만 달러로 상승하며 CAGR 9.42%를 나타낼 것으로 예측됩니다.

수요가 견조한 것은 이 기술이 갱내유정이나 전기자동차의 배터리팩 등 가혹한 환경에서의 실시간 감시에 적합하기 때문입니다. 패브리 페로·마이크로 캐비티의 소형화가 진행되어, 2020년 이후, 인텔로게이션의 단가가 60% 저하한 것으로, 산업 오토메이션, 헬스 케어, 모빌리티등에서의 채용이 퍼지고 있습니다. 다중화의 진전은 파이버 브래그 그레이팅(FBG)의 보급을 밀어 올리고 스마트 공장이나 임베디드 디바이스에 있어서 엣지 분석의 통합은 새로운 성장 노선을 부각시키고 있습니다. 피에조 저항 센서에 비해 2-3배의 비용 프리미엄이 있는 것, 총소유 비용(Total Cost of Ownership)의 우위성이 높아지고, 노동력의 스킬 업, 커넥터 표준화 이니셔티브가 계속 채용 장벽을 완화하고 있습니다.

양산 리소그래피를 통해 풀 스케일의 정밀도를 -0.01% 유지하면서 캐비티 치수를 10µm 이하로 할 수 있게 되었습니다. 이러한 비약적인 진보로 공간에 제약이 있는 의료기기에서 2kPa라는 낮은 압력 검출이 가능해져 기존의 폴리머 센서보다 80% 감도가 향상되었습니다. 소형 캐비티는 실리콘 포토닉스의 공정 흐름에 따른 웨이퍼 레벨의 통합으로 응답 시간을 단축하고 단가를 낮춥니다. 소형 센서는 현재 구조적 무결성을 손상시키지 않고 카테터 기반 심혈관 모니터링, 고속 항공우주 액추에이션 피드백 및 임베디드 배터리 셀 진단을 지원합니다. 생산량이 증가함에 따라 광섬유 압력 센서 시장의 유선 및 무선 분야는 채널당 가격을 낮추면서 더 높은 성능의 혜택을 누릴 수 있습니다.

실리콘 포토닉스의 통합으로 2020년 이후 인텔로게이션 유닛의 가격이 약 60% 낮아졌으며 서브 나노미터의 파장 분해능이 일상적인 산업 예산에 도달하게 되었습니다. 저비용 유닛은 현재 2.5με 정밀도와 1초 이하의 응답 시간을 달성하여 다리, 터널 및 파이프라인에서 구조 안전성 모니터링의 채택을 가속화하고 있습니다. 중국이 11.3%의 점유율로 세계 전개를 선도하고 있어 대규모 스마트 공장 전개에 있어서 비용 경쟁력을 검증하고 있습니다. 에지 분석 펌웨어는 데이터 백홀의 필요성을 더욱 줄이고 원격 자산의 가치 제안을 강화하고 광섬유 압력 센서 시장의 전반적인 캡처를 뒷받침합니다.

특히, 예산의 상한이 엄격한 멀티 센서 산업 자동화 프로젝트에서는 2-3배의 단가 프리미엄이 지속되고 있습니다. 특수 인텔로게이션 하드웨어는 간단한 스트레인 게이지 컨디셔너에 비해 자본 비용을 증가시킵니다. 그러나 부식성이 있거나 고온의 장소에서 유지 보수를 절약하면 자산 수명주기에 걸쳐 초기 비용을 상쇄하고 점차 대체를 촉진합니다. 실리콘 포토닉스의 스케일 업은 2028년까지 대량 생산 라인의 차이가 거의 동등하게 축소되어 광섬유 압력 센서 시장의 이러한 억제요인이 완화될 것으로 예측됩니다.

유선 디바이스는 2024년 매출의 73%를 차지해 다운홀 컴플리션, 파이프라인 통로, 산업로 등 고신뢰성 자산에서의 역할을 굳혔습니다. 광섬유 압력 센서의 유선 단위 시장 규모는 정유소 업그레이드 및 LNG 터미널 확장으로 꾸준히 증가할 것으로 예측됩니다. 물리적 연결성은 무선 전파가 신뢰할 수 없는 환경에서 수 킬로미터의 광섬유에 걸쳐 신호 무결성을 보장합니다.

무선 노드는 CAGR 12%로 성장하고 케이블 배선이 무게, 복잡성 및 안전 위험을 증가시키는 설치에 대응합니다. 이식 가능한 의료기기, 배터리 셀 및 회전 기계는 비동기적으로 질문되는 배터리가없는 수동 태그를 활용합니다. 초저전력 광 인텔로게이터의 지속적인 비용 절감으로 초기 채용자 이외에도 대응 가능한 베이스가 넓어져 보다 광범위한 광섬유 압력 센서 시장 전체 수요를 끌어올리고 있다(3).

Fabry-Perot 센서는 서브밀리바의 분해능과 200℃에서의 견고성으로 인해 47%의 판매 점유율을 차지했습니다. 10µm 이하의 마이크로 캐비티 설계는 피하 주사 바늘과 좁은 지질학적 천공에 통합할 수 있어 광섬유 압력 센서 시장 점유율에서 리더십을 강화했습니다.

그러나 FBG 어레이는 CAGR 13.5%로 가장 빠르게 확대됩니다. 단일 섬유로 수백 개의 격자를 다중화하여 구조 상태 모니터링 및 장거리 파이프라인 프로젝트의 포인트당 비용을 절감합니다. 고속 복조기는 -1 pm의 안정성을 달성하여 지진에 강한 건물 모니터링 및 고층 빌딩의 풍하중 분석을 강화합니다. 인텔로게이션 비용이 낮아짐에 따라 FBG 채택은 Fabry Pelo의 우위를 완화하고 광섬유 압력 센서 시장의 어드레싱 가능한 총 수익을 확대합니다.

북미는 2024년 38%의 수익으로 리드, 셰일 플레이 전역의 엄격한 안전규범과 EV 배터리 플랜트의 확대에 지지를 받았습니다. 선진제조업에 대한 연방정부의 우대조치와 유전서비스 메이저의 존재가 신속한 프로토타이핑과 조기상용화를 촉진하고 있습니다. 항공우주프로그램도 비행 크리티컬 시스템에 광게이지를 채용하고 있어 광섬유 압력 센서 시장에서 이 지역의 혁신 우위성을 강화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 12.2%를 나타낼 전망입니다. 세계의 분산형 센싱 도입에 있어서 중국의 점유율 11.3%는 정부 주도의 스마트 팩토리 전개를 증명하고 있습니다. 일본의 정밀 자동차 대기업은 배터리 냉각 루프에 광 센서를 통합하고 인도의 정유소 확장은 고온 계측을 요구하고 있습니다. 실리콘 포토닉스의 지역 비용 우위는 질문 단위 출력을 가속화하고 국내에서의 가용성을 넓혀 광섬유 압력 센서 시장의 전반적인 성장을 자극합니다.

유럽은 자동차 제조, 석유화학처리, 해상풍력발전을 중심으로 안정된 성장을 기록하고 있습니다. 독일의 세계광 도입 점유율 9.4%는 산업 오토메이션의 오랜 리더십을 반영하고 있습니다. 영국의 해저 오퍼레이터는 북해의 수명 연장 프로젝트의 새로운 파도에 젖은 메이트 광 커넥터를 채용. 프랑스 항공우주 부문은 실시간 구조 진단에 광 어레이를 점점 선호하고 있으며 광섬유 압력 센서 시장 전체에 꾸준한 기세를 더하고 있습니다.

The fiber optic pressure sensors market size is valued at USD 3.8 billion in 2025 and is forecast to rise to USD 5.96 billion by 2030, advancing at a 9.42% CAGR.

Robust demand stems from the technology's suitability for real-time monitoring in harsh environments such as downhole oil wells and electric-vehicle battery packs. Ongoing miniaturization of Fabry-Perot micro-cavities and a 60% fall in interrogation-unit costs since 2020 have broadened adoption across industrial automation, healthcare, and mobility. Multiplexing gains have lifted Fiber Bragg Grating (FBG) uptake, while edge analytics integration in smart factories and implantable devices underscores new avenues of growth. Despite a 2-3 X cost premium over piezo-resistive sensors, rising total-cost-of-ownership advantages, workforce upskilling, and connector standardization initiatives continue to mitigate adoption barriers.

Mass-production lithography now delivers cavity dimensions below 10 µm while preserving +-0.01% full-scale accuracy. This leap enables pressure detection as low as 2 kPa in space-constrained medical devices, outperforming conventional polymer sensors by 80% sensitivity. Smaller cavities shorten response times and lower unit cost through wafer-level integration that follows silicon-photonics process flows. Miniature sensors now support catheter-based cardiovascular monitoring, high-speed aerospace actuation feedback, and embedded battery-cell diagnostics without compromising structural integrity. As production volumes climb, the wired and wireless segments of the fiber optic pressure sensors market both benefit from higher performance at reduced price per channel.

The integration of silicon photonics has trimmed interrogation-unit pricing by roughly 60% since 2020, placing sub-nanometer wavelength resolution within reach of routine industrial budgets. Low-cost units now achieve 2.5 µε accuracy and sub-1 s response time, accelerating structural-health-monitoring adoption in bridges, tunnels, and pipelines. China leads global deployments with 11.3% share, validating cost competitiveness in large-scale smart-factory rollouts. Edge-analytics firmware further reduces data-backhaul needs, strengthening the value proposition in remote assets and boosting overall uptake of the fiber optic pressure sensors market.

A 2-3 X unit-price premium persists, particularly in multi-sensor industrial automation projects where budget ceilings remain strict. Specialized interrogation hardware inflates capital cost compared to simple strain-gauge conditioners. Yet maintenance savings in corrosive or high-temperature sites offset initial spend over asset life cycles, encouraging gradual substitution. Silicon-photonics scale-up is expected to shrink the gap to near parity in high-volume lines by 2028, easing this restraint on the fiber optic pressure sensors market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Wired devices represented 73% of revenue in 2024, cementing their role in high-integrity assets such as downhole completions, pipeline corridors, and industrial furnaces. The fiber optic pressure sensors market size for wired units is projected to rise steadily alongside refinery upgrades and LNG terminal expansions. Physical connectivity guarantees signal integrity across kilometers of fiber in environments where wireless propagation is unreliable.

Wireless nodes, growing at a 12% CAGR, address installations where cabling adds weight, complexity, or safety risk. Implantable medical devices, battery cells, and rotating machinery capitalize on battery-free passive tags interrogated asynchronously. Continuous cost declines in ultra-low-power optical interrogators widen the addressable base beyond early adopters, lifting overall demand within the broader fiber optic pressure sensors market.[3]

Fabry-Perot sensors held 47% revenue share thanks to sub-milli-bar resolution and robustness at 200 °C. Their micro-cavity designs, now below 10 µm, allow integration in hypodermic needles and narrow geological perforations, reinforcing leadership within the fiber optic pressure sensors market share.

FBG arrays, however, will expand the fastest at 13.5% CAGR. A single fiber multiplexes hundreds of gratings, trimming per-point cost for structural-health-monitoring and long-haul pipeline projects. High-speed demodulators achieve +-1 pm stability, enhancing earthquake-resilient building surveillance and high-rise wind-load analysis. As interrogation costs fall, FBG uptake moderates Fabry-Perot dominance while enlarging total addressable revenue for the fiber optic pressure sensors market.

The Fiber Optic Pressure Sensors Market Report is Segmented by Type (Wired, Wireless), Technology (Fabry-Perot, Fiber Bragg Grating, and More), Application (Oil & Gas, Industrial Automation, Healthcare & Medical Devices, and More), Installation Environment (Down-hole/Sub-surface, Industrial Surface Plants, In-vivo/Biomedical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led with 38% revenue in 2024, supported by rigorous safety codes across shale plays and expanding EV battery plants. Federal incentives for advanced manufacturing and the presence of oilfield service majors foster rapid prototyping and early commercial launches. Aerospace programs also adopt optical gauges for flight-critical systems, reinforcing the region's innovation edge within the fiber optic pressure sensors market.

Asia-Pacific posts the strongest 12.2% CAGR to 2030. China's 11.3% share of global distributed sensing deployments evidences government-driven smart-factory rollouts. Japan's precision automotive giants integrate optical sensors in battery cooling loops, while India's refinery expansions demand high-temperature gauging. Regional cost advantages in silicon photonics accelerate interrogation-unit output, broadening domestic availability and stimulating overall growth in the fiber optic pressure sensors market.

Europe records stable uptake anchored in automotive manufacturing, petrochemical processing, and offshore wind. Germany's 9.4% share of global optical deployments reflects long-standing leadership in industrial automation. United Kingdom subsea operators embrace wet-mate optical connectors for a new wave of North Sea life-extension projects. France's aerospace sector increasingly favors optical arrays for real-time structural diagnostics, adding to steady momentum across the fiber optic pressure sensors market.