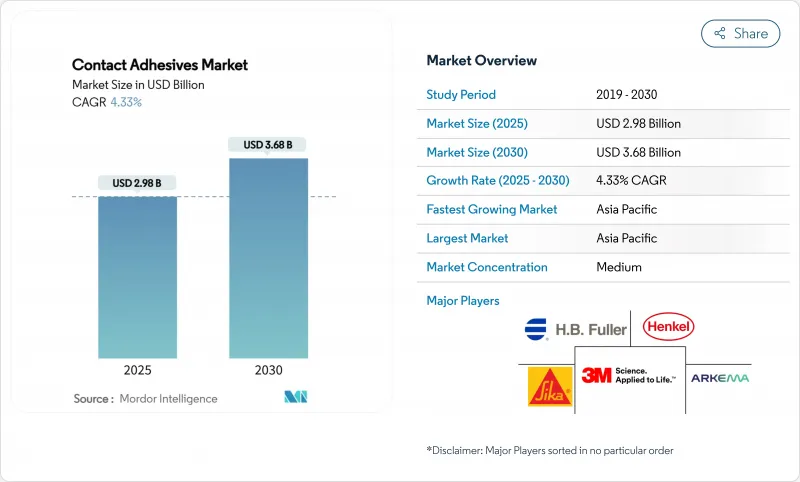

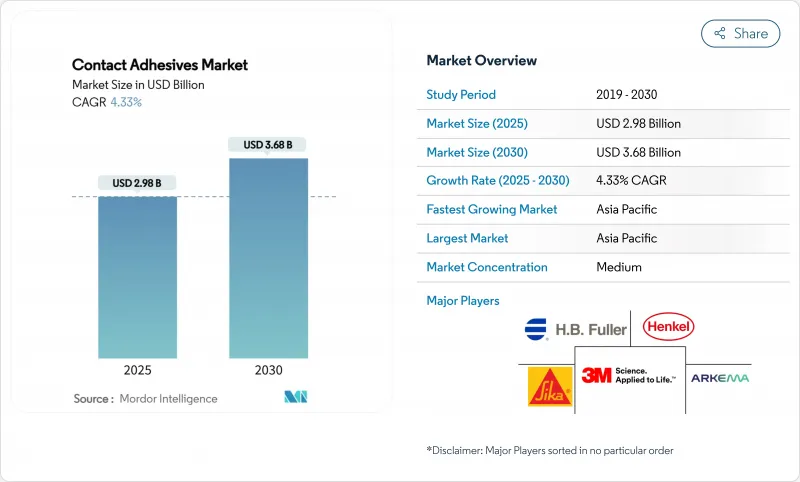

2025년 접촉형 접착제 시장 규모는 29억 8,000만 달러로 추정되고, 2030년에는 36억 8,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 4.33%를 나타낼 전망입니다.

이 성장경로는 전기자동차 배터리팩과 신재생에너지·유지보수의 새로운 수요에 뒷받침된 핵심사업의 성숙을 보여줍니다. 신발 조립, 모듈식 가구, 현장 건설 등의 즉각적인 접착 용도는 순간적인 택과 재위치 저항성이 여전히 중요한 전통 분야에 접촉형 접착제 시장을 확고하게 뿌리내리고 있습니다. 한편, 휘발성 유기화합물(VOC) 배출량 감축을 요구하는 규제압력은 수성처방으로의 변화를 가속시키고 있으며, 접착성능을 손상시키지 않고 기술 혁신의 여지가 확산되고 있습니다. 특히 아시아태평양에서는 클로로프렌 단량체의 부족과 원재료의 변동이 정기적으로 제조업체를 덮치는 중 공급망의 회복력이 가격의 안정을 지지하고 있습니다. 마지막으로 아시아 신발 공장에서 자동화와 풍력 터빈 블레이드의 수리 작업이 증가함에 따라 특수 등급 프리미엄 가격을 허용하는 백스페이스 기회가 탄생했습니다.

캘리포니아의 VOC 규제 강화와 캐나다의 2024년 국가 규제 강화에 따라 규제 기세가 제제 전략을 재구성했습니다. 현재, 단일 조리법으로 여러 관할 구역에 해당하는 무용제 등급의 대규모 생산이 경제적으로 유리합니다. 미국에서 제안된 N-메틸피롤리돈의 소비자용 접착제에 대한 45% 농도 규제는 용제의 팔레트를 더욱 좁히고 완전히 수성화하는 연구개발을 추진하고 있습니다. 3M Fastbond 1049와 같은 제품의 상시는 접촉형 접착제 시장이 용매 캐리어 없이 성능 벤치마크를 충족할 수 있음을 보여줍니다. 그 결과 공급업체는 오픈 타임과 그린 강도에서 배합이 동등해짐에 따라 적합 등급 가격 프리미엄이 증가하고 비용에 민감한 아시아 공장에서 더 널리 채택될 것으로 기대하고 있습니다.

도시의 고밀도화와 하이브리드 작업 공간은 기계식 패스너보다 접착제 기반 조립을 선호하는 모듈식 구조 기술에 박차를 가하고 있습니다. 접착제 솔루션은 무게를 줄이고 미관을 향상시키고 설치 시간을 단축하기 위해 아시아태평양 주택 및 상업시설 건설주기의 속도에 부합합니다. 마무리된 패널이나 경량 복합재를 사용하는 프로젝트에서는 초기 택이 높고 클램프 없이 수직 장착이 가능한 접촉형 접착제를 지정하는 경우가 많습니다. 모듈화 동향은 재사용 및 재활용을 위해 접착된 부품을 깨끗하게 제거할 수 있기 때문에 순환성을 향상시킵니다. 이러한 요인을 합치면 접촉형 접착제 시장의 단기 수요가 예상 0.8포인트 상승할 것으로 예상됩니다.

폴리머 등급 프로파일렌, 클로로프렌, 천연 고무의 가격은 공급 감소, 날씨 불순, 물류 병목 현상에 따라 크게 변동하고 있습니다. 소규모 생산자는 장기공급계약을 확보하기 위한 타코가 없기 때문에 가장 큰 타격을 받고 있습니다. 아시아에서는 에틸렌과 프로파일렌의 수익성이 여전히 침체되어 재투자가 억제되고 추가 비용 상승 위험이 높아지고 있습니다. 재고 완충액과 이중 조달은 부분적인 구제책이지만, 접촉형 접착제 시장의 새로운 설비 투자 결정은 불확실성 속에서 늦어지고 있습니다.

솔벤트 시스템은 2024년 접촉형 접착제 시장의 76.34%를 차지했으며, 타의 추종을 불허하는 오픈타임 유연성과 높은 초기 압정으로 인해 2024년에 접어들었습니다. 예를 들어, 양말 생산 라인은 조립 처리량을 높게 유지하는 빠른 횡령에 의존합니다. 그러나 수성 등급은 VOC 규제와 성능 차이를 줄이는 수지 유화의 진보로 CAGR 4.98%를 나타낼 전망입니다. 캘리포니아의 최신 소비자 제품 규정과 캐나다의 2024년 VOC 상한 규정은 무용제 솔루션을 위한 세계 표준화 노력을 가속화했습니다.

핫멜트나 반응성 수지는 내열성이나 즉시 경화가 비용을 웃도는 틈새 역할을 담당하고 있습니다. 3M과 같은 공급업체는 현재 박리 강도로 기존의 클로로프렌 제형에 필적하는 완전 무용제 라인을 홍보하고 있으며 기술의 수렴이 가능함을 증명하고 있습니다. 예측 기간 동안 수성 제형의 접촉형 접착제 시장 규모는 규제 지역의 꾸준한 대안을 반영하여 9억 6,000만 달러에 이를 것으로 예상됩니다.

본 보고서는 기술별(수계, 용제계, 기타), 폴리머별(폴리클로로프렌, 스티렌부타디엔 고무, 아크릴 공중합체, 기타), 최종사용자 산업별(내구 소비재 및 일렉트로닉스, 패키징, 자동차 및 운송, 가구·목공, 기타), 지역별(아시아태평양, 북미, 유럽, 기타)로 분류하여 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 접촉형 접착제 시장의 59.55%를 차지했고 CAGR은 5.05%가 될 것으로 예측됩니다. 이는 중국의 다양화된 제조거점과 인도 정부가 주도한 수입 대체의 추진 때문입니다. 베트남, 태국, 인도네시아는 운동화용 스마트 공장에 엄청난 투자를 하고 있으며 정밀하고 낮은 VOC 배합에 대한 지역 수요를 높이고 있습니다. 원재료는 정기적으로 변동하는 것, 수지 생산국에 가깝기 때문에 구미에의 수입에 비해 육양 비용은 유리하게 유지됩니다.

북미는 전기자동차 생산과 엄격한 환경기준에 힘입어 견조한 수요를 유지하고 있습니다. 자동차 제조업체는 미국 선진 청정 수송 프로그램의 크레딧을 확보하기 위해 수계 접착제를 지정하는 것이 늘어나고 있으며, 적합 등급의 북미에서의 보급률을 높이고 있습니다. 현지 공급업체는 강력한 지적재산권 포지션을 활용하여 가격 프리미엄을 획득했으며 판매량이 완만한 속도로 증가하는 가운데도 금리를 확대하고 있습니다.

유럽의 성숙 시장은 규제 측면에서의 리더십으로 주목받고 있습니다. REACH에 기초한 광범위한 PFAS와 포름알데히드의 규제는 개질 사이클의 가속화를 촉진하고 있습니다. 유럽은 또한 보수기를 맞은 풍력 터빈 블레이드의 대규모 설치 기지를 가지고 있으며, 특수한 접촉형 접착제가 안정적인 수요가 되고 있습니다.

남미와 중동 및 아프리카는 주택 건설 및 경공업과 관련된 프론티어 비즈니스 기회를 제공합니다. 환율 변동은 여전히 역풍이지만, 지역 정부는 접착제 컨버터를 유치할 수 있는 세제 우대 조치가 있는 공업 단지의 정비를 진행하고 있습니다.

The Contact Adhesives Market size is estimated at USD 2.98 billion in 2025, and is expected to reach USD 3.68 billion by 2030, at a CAGR of 4.33% during the forecast period (2025-2030).

This growth path shows a maturing core business now supported by new demand in electric-vehicle battery packs and renewable-energy maintenance. Immediate-bond applications such as footwear assembly, modular furniture, and on-site construction keep the contact adhesives market firmly rooted in traditional sectors where instant tack and repositioning resistance remain critical. Meanwhile, regulatory pressure to lower volatile-organic-compound (VOC) emissions is accelerating the shift toward waterborne formulations, opening room for innovation without compromising bonding performance. Supply-chain resilience, especially in Asia-Pacific, underpins price stability even as chloroprene monomer shortages and raw-material volatility periodically challenge manufacturers. Finally, automation in Asian footwear plants and rising repair work on wind-turbine blades are creating white-space opportunities that allow premium pricing for specialized grades.

Regulatory momentum is reshaping formulation strategies as tougher VOC caps in California and Canada's 2024 national limits push manufacturers toward waterborne products. The economics now favor the scale production of solvent-free grades that meet multiple jurisdictions with a single recipe. Proposed United States restrictions on N-Methylpyrrolidone at 45% concentration for consumer adhesives narrow the solvent palette further, driving research and development toward completely water-based chemistries. Product launches such as 3M Fastbond 1049 show that the contact adhesives market can meet performance benchmarks without solvent carriers. As a result, suppliers anticipate incremental price premiums for compliant grades and broader uptake in cost-sensitive Asian factories as formulations reach parity on open time and green strength.

Urban densification and hybrid workspaces are fueling modular construction techniques that favour adhesive-based assembly over mechanical fasteners. Adhesive solutions trim weight, enhance aesthetics, and cut installation time, aligning with Asia-Pacific's fast-track residential and commercial build cycles. Projects that rely on pre-finished panels and lightweight composites often specify contact adhesives for their high initial tack, enabling vertical mounting without clamping. The modular trend also improves circularity because glued components can be removed cleanly for reuse or recycling. Together, these factors lift short-term demand in the contact adhesives market by an estimated 0.8 percentage points.

Polymer-grade propylene, chloroprene, and natural rubber prices have swung sharply on supply cuts, weather events, and logistics bottlenecks. Small producers are hit hardest because they lack leverage to secure long-term supply contracts. Ethylene and propylene profitability remains weak in Asia, discouraging reinvestment and heightening the risk of further cost spikes. Inventory buffers and dual sourcing offer partial relief but capex decisions for new contact adhesives market capacity are delayed amid uncertainty.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solvent-borne systems retained 76.34% of the contact adhesives market in 2024, thanks to unmatched open-time flexibility and high initial tack. Footwear production lines, for instance, rely on rapid grab that keeps assembly throughput high. Yet waterborne grades are growing at a 4.98% CAGR due to VOC rules and advancements in resin emulsification that narrow the performance gap. California's latest consumer-products rule and Canada's 2024 VOC cap accelerate global standardization efforts toward solvent-free solutions.

Hot-melt and reactive chemistries play niche roles where temperature resistance or instant set outweigh cost. Suppliers such as 3M now advertise entirely solvent-free lines that equal older chloroprene formulations in peel strength, proving technology convergence is feasible. Over the forecast period, the contact adhesives market size for water-borne formulations is expected to reach USD 960 million, reflecting steady substitution in regulated regions.

The Contact Adhesives Report is Segmented by Technology (Water-Borne, Solvent-Borne, Others), Polymer (Polychloroprene, Styrene-Butadiene Rubber, Acrylic Copolymers, and More), End-User Industry (Consumer Durables and Electronics, Packaging, Automotive and Transportation, Furniture and Woodworking, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 59.55% of the contact adhesives market in 2024 and is projected to post a 5.05% CAGR, driven by China's diversified manufacturing base and India's government-led push for import substitution. Vietnam, Thailand, and Indonesia invest heavily in smart factories for athletic shoes, pushing regional demand for precise, low-VOC formulations. Despite periodic raw-material volatility, proximity to resin producers keeps landed costs favorable compared with imports into Europe or North America.

North America maintains a robust demand anchored in electric-vehicle production and stringent environmental standards. Automakers increasingly specify waterborne adhesives to secure credits under the United States Advanced Clean Transportation program, raising North American uptake for compliant grades. Regional suppliers leverage strong intellectual-property positions to command price premiums, boosting margins even as sales volumes grow at a moderate pace.

Europe's mature market is notable for regulatory leadership. Broad PFAS and formaldehyde restrictions under REACH prompt accelerated reformulation cycles. Europe also hosts a large installed base of wind-turbine blades now entering their repair life phase, placing specialized contact adhesives in steady demand.

South America and the Middle East, and Africa offer frontier opportunities tied to residential construction and light manufacturing. Currency volatility remains a headwind, yet regional governments are rolling out industrial parks with tax incentives that could attract adhesive converters.