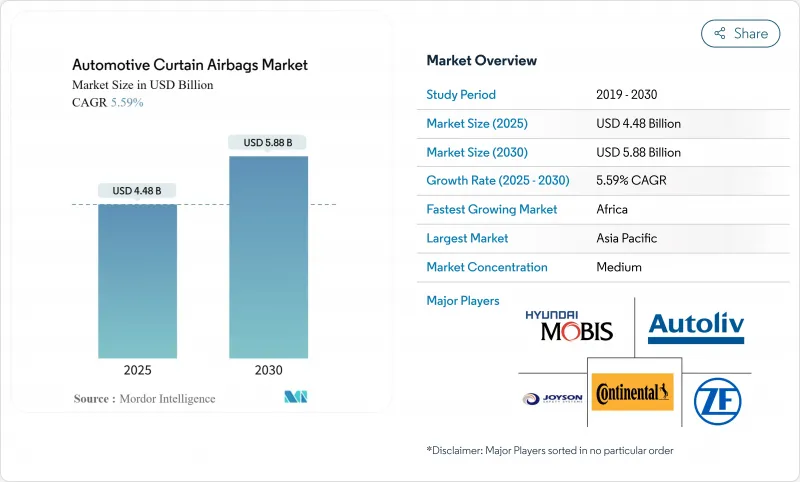

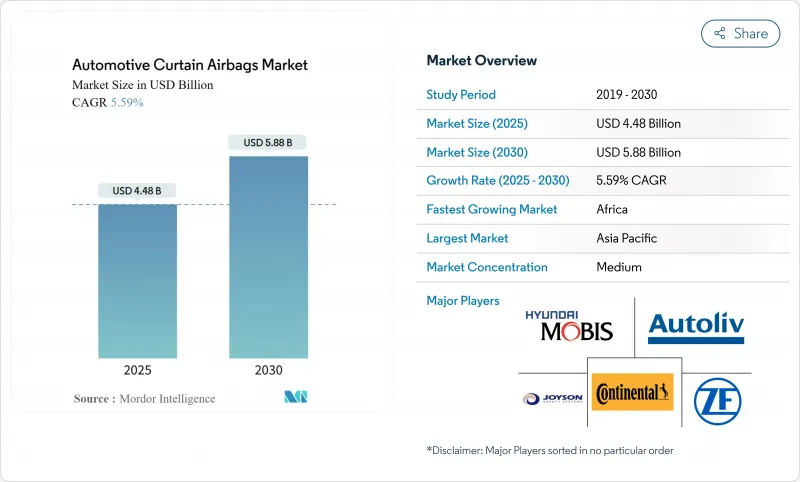

자동차 커튼 에어백 시장 규모는 2025년에 44억 8,000만 달러, 2030년에는 58억 8,000만 달러에 이를 것으로 예상되며, CAGR은 5.59%를 나타낼 전망입니다.

이 기세는 엄격한 세계적인 측면 충돌 규제, 스포츠 다목적 차량(SUV)의 출하 붐, 전기자동차(EV)의 스케이트보드 플랫폼이 만들어내는 패키징의 자유도의 수렴을 반영하고 있습니다. FMVSS 214, 유로 NCAP 퍼사이드 프로토콜 및 GTR 14에 대한 적합성 의무화로 모든 대량 판매 차량 제조업체는 선진국 시장과 신흥국 시장 모두에서 루프레일 커튼을 통합해야 하며 표준 장착률이 가속화되고 있습니다. 인도, 브라질, 아세안 지역의 5성 충돌 점수에 대한 소비자의 요구는 OEM의 전체 길이 커튼에 집중을 강화하고 동양 방-인드라마 태국의 나일론-6,6 제직 공장과 같은 합작 사업은 지금까지 생산을 억제하고 있던 직물의 희박을 완화합니다. 롤오버 지향 SUV 라인과 광범위한 크로스오버 포트폴리오가 자동차 커튼 에어백 시장의 세계 전개에서 유일하게 가장 큰 흡수 채널이 되었습니다.

세계기술규칙 14호는 시장 전체에서 머리 부상 기준을 일치시키고 OEM은 수출 트림뿐만 아니라 모든 플랫폼에서 커튼 에어백을 지정하도록 강제하고 있습니다. 호주의 새로운 측면 충돌 규제에서 커튼의 전개가 의무화되면 탑승자의 사망률이 30% 감소했습니다. 이전에 NHTSA는 사이드 에어백의 의무화에 의해 연간 311명의 생명이 구출될 것으로 예측했지만, 이 목표는 현재 실증적인 충돌 데이터베이스의 검토에 의해 검증되고 있습니다. 인도에서는 6 에어백이 의무화되고 브라질 NCAP에서는 별평가와 루프레일 커튼이 연결되어 있기 때문에 공급업체는 사이드 커튼 옵션 장비의 지위를 없애는 규제 체인에서 이익을 얻고 있습니다. 그 결과, 직물, 인플레이터, 이니시에이터의 수량 확약은 수년 앞까지 고정되어, 경기 후퇴기에서도 생산 능력을 확보할 수 있습니다.

SUV는 가장 빠르게 성장하는 경차 카테고리이며, 이 동향은 1대당 커튼 수를 직접 증가시킵니다. 포드 길이 15피트의 5열 시트 에어백은 스트레치 밴과 3열 시트 크로스오버 탑승자를 보호하는 데 필요한 엔지니어링의 도약을 가리킵니다. 미국 도로 안전 보험 협회의 데이터는 머리 보호 커튼이 전개될 때 운전자의 사망률이 37% 감소한 것을 뒷받침합니다. 중국 국내 SUV 붐과 인도 해치백에서 컴팩트 SUV로의 전환은 커튼 수량이 수년에 걸쳐 증가하는 것을 보장하고, 이 드라이버를 세계 수요 곡선에 더욱 정착시킵니다.

NHTSA가 2024년 크라이슬러와 닷지 세단 29만 8,700대를 리콜한 것은 사이드 에어백의 팽창식 커튼 파열의 위험에 의한 것으로, 유산탄에 의한 부상에 대한 사회적 불안이 재연되었습니다. 법적 해결은 공급업체의 보험료를 매달아 OEM은 검증 프로토콜을 늘려 비용 증가와 모델 출시 지연을 초래했습니다. BMW, 기아자동차, 도요타는 2024-2025년에 비슷한 커튼 관련 리콜에 직면해 자동차 커튼 에어백 업계에 대한 투자자들의 경계감을 강화했습니다.

헤드 전용 커튼은 2024년 자동차 커튼 에어백 시장 점유율의 51.25%를 차지했습니다. 규제기관은 계속해서 머리 부상 기준을 중시하고 지속적인 수요를 확보하고 있습니다. 머리와 몸통을 하나의 모듈로 커버하는 콤보 커튼은 2030년까지의 CAGR이 8.31%가 되어, 보다 심플한 부품 점수를 요구하는 프리미엄 3열 시트 SUV로 점유율을 확대하고 있습니다.

제조업체 각 회사는 6초간의 팽창을 유지하기 위해 직조 밀도와 벤트 홀의 형상을 개선하여 다중 롤 사고의 2차 충돌로부터 탑승자를 보호합니다. 오토 리브의 최신 3 열 시트는 2.5m 및 35ms로 전개됩니다. 중국의 MPV 플랫폼이 라이드 헤일링 서비스를 지원하기 위해 성장함에 따라 슈퍼 롱 커튼은 자동차 커튼 에어백 시장에 다음 채택의 파도를 약속합니다.

SUV는 2024년 자동차 커튼 에어백 시장 규모의 44.36%를 차지했고, CAGR은 9.12%를 나타낼 전망입니다. SUV는 무게 중심이 높기 때문에 횡전의 위험이 높고 루프레일의 커버 범위를 넓혀야 합니다. B부문와 C부문의 크로스오버는 중국, 인도, 미국에서 호조로 팔리고 있으며, 공급업체는 파노라믹 선루프 프레임을 클리어하는 얇은 모듈의 개발을 추진하고 있습니다.

세단은 점차 줄어들고 있지만 일본과 한국의 지역적 선호도는 컴팩트한 4문에 대한 안정적인 커튼 수요를 유지하고 있습니다. 포드의 상용 밴 커튼은 배치 타이밍을 손상시키지 않고 5열 좌석을 커버하는 복잡성을 보여줍니다. EV의 SUV는 새로운 기술적 변수를 가져옵니다. 바닥 배터리는 사이드 실을 딱딱하게 만들고 침입 입력을 위쪽으로 전달하기 때문에 커튼은 부서진 유리와의 머리 접촉을 방지하기 위해 오랫동안 부풀어 오르지 않으면 안됩니다.

아시아태평양은 2024년 매출 점유율 46.18%로 자동차 커튼 에어백 시장을 선도했으며, 이는 중국의 대규모 생산 거점과 인도의 6기통 에어백의 규제 강화를 견인했습니다. 길리기차나 멀티 등 국내 OEM은 수출 목표를 달성하기 위해 1만 달러 이하의 해치에도 전체 길이의 커튼을 내장하고 있습니다. 하이브리드 인플레이터를 세계에 공급하고 있는 다이셀에서는 일본의 화공기술의 전문지식이 추진제화학의 획기적인 획기를 뒷받침하고 있습니다. 한국은 ADAS 알고리즘과 패시브 시스템을 조합해 프리미엄 전기차(EV) 라인업 전체의 배치 타이밍을 세련시키고 있습니다.

북미는 FMVSS 214를 준수하고 호조로운 SUV 판매를 통해 여전히 중요한 위치를 차지하고 있습니다. 미국에서는 레벨 4 자율주행시험으로 저온 하이브리드 인플레이터를 추진해 공급자에게 극한 기후 솔루션의 실증장을 제공. 멕시코의 조립 공장이 국경을 넘은 모델에 동일한 커튼 사양을 채용해, 티아원의 투어링을 합리화. 캐나다는 지역 부품 구성 규칙에 따라 모듈의 서브어셈블리를 지원하며 자동차 부문에 부가가치를 부여합니다.

유럽은 지속가능성과 기술 통합에 중점을 둡니다. 독일에서는 프리미엄 EV의 확대가 고급 벤트 홀 미터를 추진하고, 프랑스와 이탈리아는 긴급 액세스를 돕기 위해 충돌 후 신속한 수축을 허용하는 기계 스티치를 장려합니다. 아프리카는 낮은 수준에서 시작되었지만 2030년까지 연평균 복합 성장률(CAGR)이 6.18%로 가장 급성장하는 지역입니다. 남아프리카의 CKD 공장은 EU의 수출 호모로게이션에 따른 듀얼 스테이지 커튼을 통합. 케냐와 나이지리아가 중고차 수입 규제를 개시해, 풀 세이프티 스위트를 번들한 신차 판매를 촉구합니다. GCC국가가 UN R135를 채용하고, 미·일 SUV 수입에 세관검사에서 머리보호 커튼의 장착을 의무화합니다.

The Automotive curtain airbags market size stands at USD 4.48 billion in 2025 and is projected to reach USD 5.88 billion by 2030, registering a 5.59% CAGR.

This momentum reflects the convergence of stringent global side-impact legislation, the boom in sport-utility vehicle (SUV) deliveries, and the packaging freedom created by electric-vehicle (EV) skateboard platforms . Mandatory compliance with FMVSS 214, Euro NCAP far-side protocols, and GTR 14 forces every volume carmaker to embed roof-rail curtains in both developed and emerging markets, accelerating standard fitment rates. Consumer demand for five-star crash scores across India, Brazil, and the ASEAN bloc intensifies OEM focus on full-length curtains, while joint ventures such as Toyobo-Indorama's nylon-6,6 weaving plant in Thailand mitigate fabric tightness that previously throttled production. Rollover-oriented SUV lines and expansive crossover portfolios thus become the single largest absorption channel for Automotive curtain airbags market deployments worldwide.

Global Technical Regulation 14 aligns head-injury criteria across markets and forces OEMs to specify curtain airbags on every platform, not just export trims. Australia's new side-impact rule lowered occupant fatalities by 30% once curtain deployment became compulsory. Earlier, NHTSA projected its side-airbag mandate would save 311 lives per year-a target now verified through empirical crash-database reviews. With India moving toward mandatory six-airbag legislation and Brazil's NCAP tying star ratings to roof-rail curtains, suppliers benefit from a regulatory cascade that eliminates optional-equipment status for side curtains. Consequently, volume commitments for fabric, inflators, and initiators stay locked years in advance, safeguarding capacity utilization even in cyclical downturns.

SUV deliveries represent the fastest-growing light-vehicle category, a trend that directly lifts per-vehicle curtain count. Ford's 15-ft-long, five-row airbag points to the engineering leap required to safeguard occupants in stretched vans and three-row crossovers. Insurance Institute for Highway Safety data corroborate a 37% drop in driver deaths when head-protecting curtains deploy. China's domestic SUV boom and India's migration from hatchbacks to compact SUVs assure a multi-year uplift in curtain volumes, further embedding this driver in global demand curves.

NHTSA's 2024 recall of 298,700 Chrysler and Dodge sedans for Side Airbag Inflatable Curtain rupture risk revived public anxiety around shrapnel injuries. Legal settlements inflate supplier insurance premiums, while OEMs lengthen validation protocols, adding cost and delaying model launches. BMW, Kia, and Toyota faced similar curtain-related recalls in 2024-2025, reinforcing investor caution in the Automotive curtain airbags industry.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Head-only curtains secured 51.25% of the Automotive curtain airbags market share in 2024, supported by a proven 31% fatality reduction in side-impact crashes. Regulatory agencies continue to weigh head-injury criteria heavily, ensuring perennial demand. Combo curtains, which merge head and torso coverage in a single module, log an 8.31% CAGR through 2030 and gain traction in premium three-row SUVs seeking simpler bill-of-material counts.

Manufacturers refine weaving density and vent-hole geometry to sustain six-second inflation, protecting occupants against secondary hits in multi-roll incidents. Autoliv's latest three-row design spans 2.5 m and deploys in 35 ms, illustrating how suppliers address cabin length growth. As Chinese MPV platforms stretch to court ride-hailing services, ultra-long curtains promise the next adoption wave for the Automotive curtain airbags market.

SUVs accounted for 44.36% of the Automotive curtain airbags market size in 2024 and are on pace for a 9.12% CAGR. Their high center of gravity increases rollover exposure, necessitating extended roof-rail coverage. Crossovers in the B- and C-segments sell briskly in China, India, and the United States, pushing suppliers to develop low-profile modules that clear panoramic-sunroof frames.

Sedans decline gradually, yet regional tastes in Japan and South Korea maintain steady curtain demand for compact four-doors. Pickup trucks and MPVs create lucrative niches; Ford's commercial van curtain illustrates the complexity of spanning five seating rows without compromising deployment timing. EV SUVs bring new engineering variables: floor batteries stiffen side sills, transferring intrusion force upward, so curtains must remain inflated longer to prevent head contact with shattered glass.

The Global Automotive Curtain Airbags Market is Segmented by Curtain Airbag Type (Torso Curtain Airbags, Head Curtain Airbags and More), Vehicle Type (Hatchback, Sedan, Sports Utility Vehicles, and More), End User (OEM and Aftermarket), Inflator Technology (Pyrotechnic, Stored Gas, and More), Sales Channel (Traditional Dealerships and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific leads the Automotive curtain airbags market with 46.18% revenue share in 2024, driven by China's large production base and India's regulatory push for six airbags. Domestic OEMs such as Geely and Maruti embed full-length curtains even in sub-USD 10,000 hatches to meet export targets. Japan's pyrotechnic expertise propels propellant chemistry breakthroughs at Daicel, which supplies hybrid inflators worldwide. South Korea pairs ADAS algorithms with passive systems to refine deployment timing across premium electric vehicle (EV) lineups.

North America remains pivotal through FMVSS 214 compliance and strong SUV sales. United States Level-4 autonomy pilots promote low-temperature hybrid inflators, giving suppliers a proving ground for extreme-climate solutions. Mexico's assembly plants adopt identical curtain specifications for cross-border models, streamlining tier-one tooling. Canada supports module sub-assembly under regional parts-content rules, adding value to its auto sector.

Europe emphasizes sustainability and technology integration. Germany's premium EV expansion drives advanced vent-hole metering, while France and Italy encourage mechanical stitching that enables rapid post-crash deflation to aid emergency access. Africa, while starting from a lower base, is the fastest-growing region with a 6.18% CAGR through 2030. South African CKD plants integrate dual-stage curtains aligned with EU export homologation. Kenya and Nigeria launch used-vehicle import restrictions, compelling new-car sales that bundle full safety suites. GCC states adopt UN R135, obliging Japanese and US SUV imports to include head-protecting curtains at customs inspection.