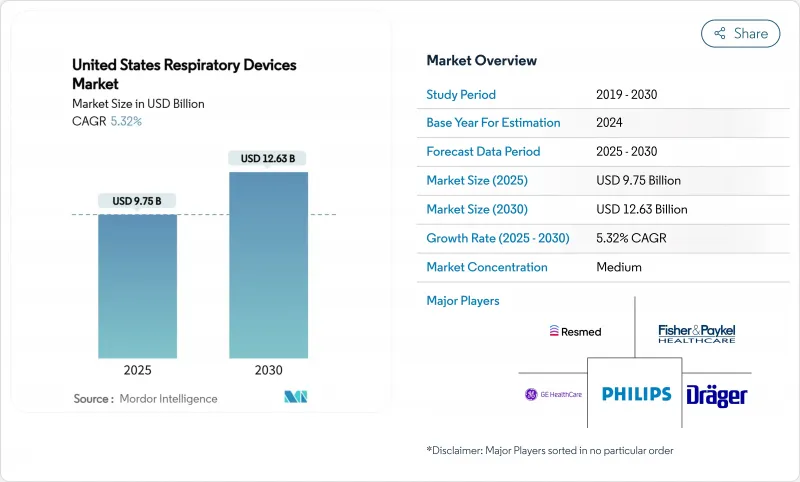

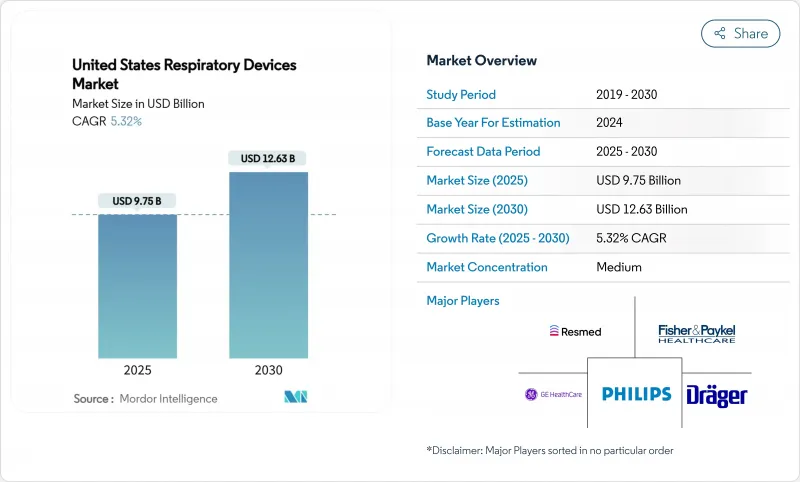

미국의 호흡 기기 시장 규모는 2025년에 97억 5,000만 달러로 추정되고 예측기간(2025-2030년)의 CAGR은 5.32%로, 2030년에는 126억 3,000만 달러에 달할 것으로 예상됩니다.

수요 증가는 만성 호흡기 질환의 유병률 상승, 집에서의 치료를 선호하는 고령화, 메디케어 메디케이드 서비스 센터(CMS)가 재택 산소 요법과 비침습적 환기에 대한 상환을 확대한 것에 수반됩니다. 특히 서부 제주에서는 산불의 시즌이 격화되고 공기청정호흡 기기 제품에 대한 소비자의 관심이 높아지는 반면 진단 도구에 내장된 인공지능(AI) 알고리즘은 치료까지의 시간을 단축하고 임상 정확성을 향상시키고 있습니다. 동시에 리콜 중심의 품질 모니터링을 통해 제조업체는 보다 안전한 소재와 보다 스마트한 센서에 대한 투자를 강요하고 환자의 안전에 대한 경쟁의 초점을 더욱 선명하게 하고 있습니다. 주요 브랜드가 디지털 건강 관련 신흥 기업을 인수하고 하드웨어, 소프트웨어 및 데이터 분석을 통합 케어 플랫폼에 통합함으로써 업계 재편이 완만하게 계속되고 있습니다.

COPD는 1,250만 명, 천식은 2,680만 명의 미국인이 병을 앓고 있는 것으로 진단되었으며, 유병률은 남동부와 중서부 카운티에서 봉우리에 이릅니다. 주 수준의 COPD 이환율은 하와이의 3%에서 웨스트 버지니아의 12%까지 다양하며 환경 노출과 건강 관리에 대한 접근 격차를 반영합니다. COPD의 사망률은 성인 10만명당 41-171명으로 치료상의 부담이 큰 것으로 밝혀졌습니다. 이러한 역학적 패턴은 분무기, 산소 농축기, 흡입 유량을 모니터링하여 악화를 예측할 수 있는 디지털 흡입기에 대한 수요를 부추기고 있습니다. 천식의 연간 직접 및 간접 비용은 800억 달러에 달하며 비용 효율적인 재택 호흡기 솔루션에 대한 지불자의 관심이 높아지고 있습니다.

2060년까지 미국인의 4분의 1 근처가 65세 이상이 되어, 재택 치료와 원격 환자 모니터링으로의 구조적인 변화가 촉진됩니다. 메디케어 수급자는 최근 COPD 관련 입원을 24만 건 이상 기록해 휴대형 산소 농축기나 재택 인공호흡 기기의 필요성을 높여가고 있습니다. 원격 환자 모니터링의 이용자는 이미 약 5,000만 명에 이르고 있으며, 진료 보상이 밸류 베이스 케어의 인센티브에 합치함에 따라, 10년 후까지는 배증할 것으로 예상되고 있습니다. Patient-Driven Groupings Model(환자 주도형 그룹화 모델)은 운영의 복잡성을 향상시키지만 연결된 호흡기 플랫폼을 사용하여 측정 가능한 결과 개선을 입증한 공급자에게는 보상이 부과됩니다. 장기 인공호흡 사례가 20년간 2배 이상으로 증가하고, 급성기 후 시설의 용량이 희박해, 재택 대응 인공호흡 장치에 대한 투자가 촉진됩니다.

미국의 대부분의 병원은 주요기기의 구입을 회계연도마다 할당하고 있기 때문에 임베디드의 결정이 12-18개월 늦게 늘어나고, 고급인공호흡 기기나 화상처리그레이드의 초음파 진단 장치의 구입이 늘어나고 있습니다. 2025년 의사 보수 개정에서는 지불액이 2.93% 삭감되기 때문에 특히 수출 자금이 부족한 지방 병원에서는 영업 이익이 압박됩니다. 가치 기반 상환은 자본 요구에 대해 명확한 임상 결과 증거를 요구하므로 장비 제조업체에게는 실제 데이터를 제공하는 장애물이 높아집니다. COPD의 연간 경제 손실은 500억 달러에 달하는 추세이지만 고급 진단제의 투자 회수 기간이 길기 때문에 특히 환자 수가 적은 경우 도입이 지연될 수 있습니다. 제조업체 각사는 리스나 사용 마다의 구독 모델을 제공해, 가격 쇼크를 완화하고 있지만, 대규모 의료 시스템 이외에서의 도입은 아직도 마을입니다.

2024년 미국의 호흡 기기 시장의 46.54%를 치료용 기기가 차지했고 만성 및 급성 증상에 대응하는 기도양압(PAP) 시스템과 재택인공호흡 기기가 그 중심이 되었습니다. 설치 기반은 이익률이 높은 소모품 수요를 만들어 내고, AI 주도의 어드히어런스 알고리즘은 치료 효과를 높입니다. 진단 및 모니터링 기기는 FDA가 인가한 가정용 스파이로미터와 AI청진 소프트웨어가 검사를 클리닉에서 거실로 이행시키기 때문에 2030년까지의 CAGR이 6.65%로 계속해서 가장 급성장하는 카테고리입니다. 일회용 제품은 마스크, 필터 및 호흡 회로를 정기적으로 교체해야 하므로 안정적인 성장을 유지하고 경상 수익을 보장합니다.

주요 성장의 변곡점은 COPD 치료에서 우수한 침착을 실현하는 진동 메쉬식 분무기에 기인하고 있으며, 주요 지불자가 처방으로의 통합을 촉진하고 있습니다. 휴대용 산소 농축기는 클라우드 연결을 통합하여 임상의가 원격으로 유량을 조정할 수 있게 하고, 가정 관리 동향과 일치합니다. 호흡 수와 수면 운동을 추적하는 진단용 스마트 패치는 수면 무호흡 증후군의 진단주기를 단축합니다. 이러한 요인이 결합되면서 미국의 호흡 기기 시장 규모에 새로운 가치가 더해지는 동시에 데이터 주도형 사용자 체험을 둘러싼 경쟁이 격화됩니다.

The United States Respiratory Devices Market size is estimated at USD 9.75 billion in 2025, and is expected to reach USD 12.63 billion by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

Demand growth follows rising chronic respiratory disease prevalence, an aging population that prefers treatment at home, and the Centers for Medicare & Medicaid Services (CMS) widening reimbursement for home oxygen therapy and non-invasive ventilation. Intensifying wildfire seasons, particularly in western states, elevate consumer interest in air-purifying respiratory products, while artificial-intelligence (AI) algorithms embedded in diagnostic tools speed time-to-care and improve clinical accuracy. Concurrently, recall-driven quality scrutiny compels manufacturers to invest in safer materials and smarter sensors, sharpening the competitive focus on patient safety. Moderate industry consolidation persists as leading brands acquire digital-health start-ups to integrate hardware, software, and data analytics into unified care platforms.

COPD affects 12.5 million diagnosed adults and asthma affects 26.8 million Americans, with prevalence peaking in southeastern and midwestern counties. State-level COPD rates vary from 3% in Hawaii to 12% in West Virginia, mirroring disparities in environmental exposures and healthcare access. COPD mortality spans 41-171 deaths per 100,000 adults, underscoring the ongoing therapeutic burden. These epidemiologic patterns fuel demand for nebulizers, oxygen concentrators, and digital inhalers capable of predicting exacerbations by monitoring inspiratory flow metrics. Annual direct and indirect asthma costs near USD 80 billion, intensifying payer interest in cost-effective home-based respiratory solutions.

Nearly one quarter of Americans will be 65 years or older by 2060, prompting a structural shift toward in-home therapy and remote patient monitoring. Medicare beneficiaries recorded over 240k COPD-related hospitalizations in recent times, amplifying the need for portable oxygen concentrators and home ventilators. Remote patient monitoring users already number about 50 million and are expected to double by the end of the decade as reimbursement aligns with value-based care incentives. The Patient-Driven Groupings Model increases operational complexity but rewards providers that demonstrate measurable outcome improvements using connected respiratory platforms. Long-term mechanical ventilation cases more than doubled over two decades, tightening capacity in post-acute facilities and driving investment in home-compatible ventilators.

Most U.S. hospitals allocate major equipment purchases once per fiscal year, extending replacement decisions 12-18 months and deferring acquisition of advanced ventilators and imaging-grade ultrasound devices. A 2.93% payment cut in the 2025 Physician Fee Schedule compresses operating margins, especially in rural facilities with thin cash reserves. Value-based reimbursement requires clear clinical-outcome evidence for capital requests, raising the bar for device makers to supply real-world data. Although COPD's annual economic toll nears USD 50 billion, the longer payback period for sophisticated diagnostics can slow adoption, particularly where patient volumes are modest. Manufacturers offer leasing and per-use subscription models to mitigate sticker shock, but uptake remains mixed outside large health systems.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Therapeutic devices commanded 46.54% of the 2024 United States respiratory devices market, anchored by positive airway pressure (PAP) systems and home ventilators that address both chronic and acute conditions. The installed base generates high-margin consumables demand, while AI-driven adherence algorithms elevate therapeutic efficacy. Diagnostic & monitoring devices remain the fastest-growing category at a 6.65% CAGR through 2030 as FDA-cleared home-use spirometers and AI auscultation software migrate testing from clinics to living rooms. Disposables retain steady uptake because masks, filters, and breathing circuits require periodic replacement, ensuring recurring revenue.

A key growth inflection stems from vibrating mesh nebulizers that deliver superior deposition in COPD therapy, prompting formulary inclusion by major payers. Portable oxygen concentrators integrate cloud connectivity, allowing clinicians to titrate flow remotely and aligning with home-care trends. Diagnostic smart patches that track respiratory rate and sleep motion shorten sleep-apnea diagnosis cycles. Combined, these factors add incremental value to the United States respiratory devices market size while intensifying competition around data-driven user experiences.

The United States Respiratory Devices Market Report is Segmented by Product Type (Diagnostic & Monitoring Devices, Therapeutic Devices, Disposables), Indication (COPD, Asthma, Sleep Apnea, Infectious Diseases, Other Respiratory Disorders), End User (Hospitals & Clinics, Home-Care Settings, and More), and Geography (Northeast, Midwest, Southeast, West, Southwest). The Market Forecasts are Provided in Terms of Value (USD).