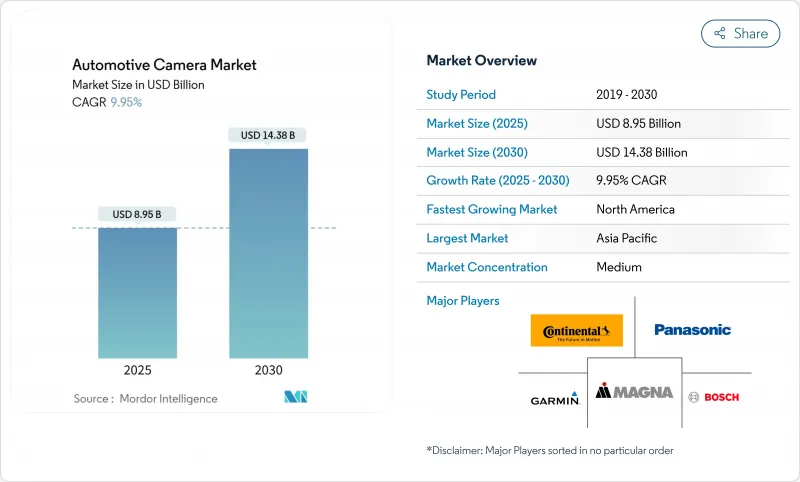

2025년 자동차용 카메라 시장 규모는 89억 5,000만 달러, 2030년에는 143억 8,000만 달러에 이를 것으로 예상되며, 2025-2030년의 CAGR은 9.95%를 나타낼 전망입니다.

법규제 강화, 자동차 자동화, CMOS센서 비용 저하 등이 상반되어 대수와 ASP 양쪽이 상승해 자동차용 카메라 시장 규모를 2자리 성장으로 밀어 올리고 있습니다. 유럽 연합(EU), 미국, 중국에서는 안전 규제가 강화되어 자동 긴급 브레이크, 인텔리전트 스피드 어시스트, 드라이버 모니터링 등의 카메라 대응 기능이 요구되고 있으며, 카메라는 최신 차량 설계에서 양보할 수 없는 핵심이 되고 있습니다. 자동차 제조업체는 또한 멀티카메라 어레이를 레벨 2 자율성에 대한 가장 저렴한 비용의 길로 간주하고 있으며, 중가격대 모델에서 전체 플랫폼에 대한 채택을 가속화하고 있습니다. 동시에 열기술과 근적외선 기술은 야간이나 악천후 시나리오까지 성능 범위를 넓혀 프리미엄 업그레이드 기회를 넓히고 있습니다. 마지막으로, 2024년을 통해 그리고 2025년까지 예상되는 웨이퍼 비용 디플레이션은 재료비를 줄이고 OEM은 스티커 가격을 늘리지 않고 차량에 더 많은 카메라를 탑재할 수 있습니다.

안전 규정의 수렴으로 OEM은 모든 신차 플랫폼에 멀티 카메라 스위트를 통합해야합니다. EU의 일반 안전 규칙 II는 2024년 7월에 발효되었으며 차선 유지, 지능형 스피드 어시스트, 긴급 브레이크용 전방 카메라 탑재를 의무화하고 있습니다. 중국의 2024년 NCAP에서는 드라이버 모니터링의 정밀도를 채점하게 되어 사실상 적외선 캐빈 카메라의 탑재가 의무화되었습니다. 미국에서는 2024년에 최종 결정된 NHTSA 규칙에 따라 시속 90마일까지 보행자 감지 기능이 있는 자동 긴급 브레이크가 의무화되어 어둠 속에서도 시인 가능한 적외선 센서가 명확하게 요구되고 있습니다. 따라서 자동차 제조업체는 세 가지 규제를 동시에 충족하는 카메라 아키텍처를 요구하고 있으며 세계 설계 사이클을 가속화하고 있습니다. 확장 가능한 기준 설계를 갖춘 공급업체는 대량 생산 플랫폼에서 새로운 RFQ를 획득했습니다. 이와 같이 규제의 조정에 의해 안전카메라는 차별화 요인이라기 보다 오히려 기본적인 상품이 되고 있어 자동차용 카메라 시장 전체의 출하대수를 밀어 올리고 있습니다.

레벨 2의 운전 기능은 프리미엄 명차에서 대중용 C 부문 차로 이행하고 있습니다. Mobileye의 SuperVision 플랫폼은 현재 폭스바겐의 MQB 모델에 탑재되어 있으며 서라운드 감지 및 고해상도 도로 참조용으로 최대 11대의 카메라를 사용하고 있습니다. 소니는 2027년도까지 각 차량에 현재 8대에서 12대의 카메라가 탑재될 것으로 예측했습니다. AI 온센서 기능은 실시간 비전 알고리즘을 에지 실리콘에서 실행하여 시스템 대기 시간과 배선 복잡성을 줄입니다. 자동화가 진행되면 더 많은 카메라에 투자할 수 있으며 비용 효과적인 루프를 닫을 수 있습니다. 순 효과로는 대수 증가와 함께 카메라 ASP가 상승해 2030년까지 자동차용 카메라 시장의 CAGR을 2.1포인트 상승시킵니다.

종합적인 ADAS 스택에는 현재 8-12대의 카메라가 필요하지만 단가는 해상도에 따라 20-500달러에 이릅니다. 가치 지향 명판의 경우 카메라는 차량 재료 비용의 최대 3%를 소비하고 이익을 압박할 수 있습니다. 2025년에 포드가 후면 카메라 소프트웨어의 문제를 이유로 107만 5,000대를 리콜한 것은 복잡성이 증가하면 보증을 받을 수 없게 된다는 것을 부각하고 있습니다. Tier 1 공급업체는 통합 비전 ECU와 단일 케이블 아키텍처를 지원하지만, 가까운 미래의 비용 역풍은 자동차용 카메라 시장의 CAGR을 1.8포인트 낮춥니다.

자동차용 카메라 시장 규모는 2024년 60억 달러로 세계 매출의 67.23%에 해당했습니다. 소형상용차 시장 규모는 현재 작지만 2030년까지 연평균 복합 성장률(CAGR)은 11.51%로 확대해 전체 성장을 웃돌 전망입니다. 함대 소유자는 보험 비용을 줄이고 충돌을 억제하며 텔레매틱스 기반 드라이버 스코어링을 지원하기 위해 카메라를 채택합니다. 볼보 트럭은 카메라 모니터 시스템이 기존 미러를 대체할 경우 연료를 2% 절약할 수 있다고 보고합니다. 따라서 자동차용 카메라 시장에서는 ROI를 정량화할 수 있는 물류기업으로부터의 조달이 증가하고 있습니다.

승용차는 대규모 생산과 소비자의 안전 팩에 대한 지불 의향으로 주도권을 유지합니다. ADAS의 보급률은 2025년에 소형차의 신차로 90%를 넘어, 안정된 설치 베이스가 확보됩니다. 대형 트럭에서 카메라 채택은 EU의 GSR II 사각 검출 규칙과 같은 규제의 고비와 일치합니다. Stoneridge의 MirrorEye 시스템이 Freightliner Cascadia 대형 트럭에 탑재되어 8대의 카메라에 의한 중복성이 입증되었습니다. 비용 절감 모듈과 입증된 차량 절약 효과의 융합으로 상용 부문 전체에서 자동차용 카메라 시장은 2자리 성장을 유지하고 있습니다.

뷰잉 카메라는 2024년 57.33%의 매출 점유율을 유지하며 리버스, 서라운드, 미러 교환 기능을 중심으로 자동차용 카메라 시장 점유율을 지원했습니다. 그러나 OEM이 디스플레이보다 지각을 우선하기 때문에 센싱 스테레오 유닛의 CAGR은 13.44%를 나타낼 전망입니다. 스바루의 차세대 EyeSight는 온세미 Hyperlux AR0823AT 센서를 활용하여 지금까지는 라이더 셋업에 한정된 차선 중앙 정밀도를 제공합니다. 심도 지각 스테레오 리그는 현재 일본에서 자율주행 시스템(ADS) 레벨 3까지 검증되고 있으며, 보다 광범위한 보급을 뒷받침하고 있습니다. 센싱 카메라가 합리적인 가격의 트림으로 이동함에 따라, 지각 하위 부문 내의 자동차용 카메라 시장 규모는 기존의 뷰잉 카테고리와의 차이를 줄일 것으로 보입니다.

기존의 뷰잉 시스템은 보다 높은 HDR과 노면 얼룩 속에서도 선명함을 유지하는 디스플레이 코팅에 의해 진화합니다. 자동차 제조업체는 4대의 카메라 사이에 프레임 정밀도의 동기화를 요구하는 버드아이 계산 모자이크를 통합하고 있으며 공급업체는 스큐가 적은 이미저를 제공하도록 요구되고 있습니다. 포사이트의 스테레오 알고리즘 번들은 0.05 럭스 이하로 물체 검출을 실현하고 센싱 카메라를 라이더를 대체하는 비용 효율적인 것으로 자리잡고 있습니다. 전반적으로 이미지 기반 지각의 이점과 BOM 하락은 자동차용 카메라 시장의 인텔리전스 엔드로 성장하는 축입니다.

자동차용 카메라 시장 보고서는 차량 유형(승용차, 소형 상용차 등), 유형(시야(서라운드/리어/프론트/인테리어) 등), 기술(디지털(CMOS) 등), 용도(주차 보조 등), 판매 채널(OEM-설치형 등), 지역별로 분류하고 있습니다. 시장 규모와 예측은 위의 모든 부문에 대해 금액(달러) 기준으로 제공됩니다.

2024년 자동차용 카메라 시장은 아시아태평양이 40.32%의 점유율을 차지했으며, 중국의 생산 규모와 일본의 반도체 리더십에 밀려왔습니다. 소니는 2026년도까지 차량용 이미저의 세계 점유율을 대폭 확대하는 것을 목표로 하고 있으며, 지역공급망 경쟁력을 강화하고 있습니다. 베이징의 스마트카 로드맵은 레벨 2 시스템을 보조하고 이코노미 EV에서도 멀티 카메라 패키지를 표준으로 합니다. 한국의 OEM은 모든 신형 SUV에 선진적인 서라운드 뷰를 탑재하고 있으며 센서와 렌즈의 현지 생산에 지지를 받고 있습니다. 이러한 정책과 산업의 두께는 자동차용 카메라 시장에서 APAC의 지위를 확실히 하고 있습니다.

북미는 2024년에 26.22%의 점유율을 차지했는데 이는 하이엔드의 안전기능을 요구하는 소비자 요구와 NHTSA의 의무화가 일치했기 때문입니다. 미국에서는 2029년까지 자동 긴급 브레이크를 의무화하는 규칙이 제정되어 검증 비용을 긴 사이클에 분산시키기 위해 카메라의 조기 도입이 장려되고 있습니다. 캐나다의 각 주는 대시 캠에 차량 보험 리베이트를 제공하여 복고풍 수영장을 확장하고 있습니다. 실리콘 밸리 칩 기업은 국내 OEM 시장 출시 기간을 단축하는 에지 AI 기준 설계를 제공합니다. 이러한 요인으로 인해 이 지역의 자동차용 카메라 시장은 견조한 확대 기조를 유지하고 있습니다.

유럽은 23.29%의 점유율을 획득했으며, GSR II 하에서 종합적인 카메라 기반 안전성을 최초로 법제화한 것이 그 원동력이 되고 있습니다. 독일의 고급 브랜드는 유로 NCAP에서 5 별을 얻기 위해 최대 10 대의 카메라를 탑재하고 있습니다. EV 제조업체가 드래그 컷 효과가 있는 가상 미러를 채용하는 중, EU권의 e미러 인가는 새로운 바람을 가져옵니다. 그러나 GDPR(EU 개인정보보호규정)은 엄격한 데이터 처리 규칙을 부과하므로 보다 광범위한 분석이 제한되어 APAC에 비해 성장이 약간 둔화되고 있습니다.

중동 및 아프리카는 걸프 협력 회의 국가에서 안전 장비의 의무화와 도시화 확대로 2024년 매출의 6.76%를 차지했습니다. 사우디아라비아에서는 자동차용 스플릿 뷰 카메라 에코시스템이 대두해 국내 조립의 의욕을 뒷받침하고 있습니다. 남미의 점유율은 5%에 그쳤지만, 브라질은 2026년 유엔 ECE의 백 카메라 표준에 맞출 계획으로 수년의 업그레이드 사이클을 설정하고 있습니다. 전반적으로 규제 타이밍이 다르기 때문에 자동차용 카메라 시장은 지리적으로 분산되어 있습니다.

The automotive camera market size is valued at USD 8.95 billion in 2025 and is forecast to reach USD 14.38 billion by 2030, advancing at a 9.95% CAGR during 2025-2030.

A synchronized wave of regulatory mandates, rising vehicle automation, and falling CMOS sensor costs is lifting both unit volumes and ASPs, pushing the automotive camera market size toward double-digit growth. Tightened safety rules in the European Union, the United States, and China now require camera-enabled functions such as automated emergency braking, intelligent speed assistance, and driver monitoring, making cameras a non-negotiable core of modern vehicle design. Automakers also view multi-camera arrays as the lowest-cost path to Level 2+ autonomy, which is accelerating platform-wide adoption across mid-priced models. At the same time, thermal and near-infrared technologies are broadening the performance envelope into night and bad-weather scenarios, opening premium upgrade opportunities. Finally, wafer cost deflation throughout 2024 and expected through 2025 is shrinking the bill-of-materials, letting OEMs fit more cameras per vehicle without inflating sticker prices.

A convergence of safety regulations is forcing OEMs to integrate multi-camera suites in every new vehicle platform. The European Union's General Safety Regulation II, effective July 2024, compels forward-facing cameras for lane keeping, intelligent speed assistance, and emergency braking. China's 2024 NCAP now scores driver-monitoring accuracy, effectively requiring infrared cabin cameras. In the United States, the NHTSA rule finalized in 2024 obliges automatic emergency braking with pedestrian detection up to 90 mph, creating a clear pull for thermal sensors that can see in darkness. Automakers, therefore, seek camera architectures that meet all three regimes simultaneously, accelerating global design cycles. Suppliers equipped with scalable reference designs are winning new RFQs from volume platforms. Regulatory alignment is thus turning safety cameras into a baseline commodity rather than a differentiator, lifting overall shipment volumes across the automotive camera market.

Level 2+ driving functions are shifting from premium nameplates to mass-market C-segment vehicles. Mobileye's SuperVision platform now powers Volkswagen's MQB models, using up to 11 cameras for surround sensing and high-definition road referencing. Sony forecasts each vehicle will embed 12 cameras by fiscal 2027, up from 8 today. AI-on-sensor capabilities let real-time vision algorithms run on edge silicon, trimming system latency and wiring complexity. In turn, higher automation creates a payback for more cameras, closing the cost-benefit loop. The net effect is an upward shift in camera ASPs alongside ballooning unit counts, underpinning an incremental 2.1-percentage-point lift in the automotive camera market CAGR through 2030.

Comprehensive ADAS stacks now need 8-12 cameras, yet unit prices range from USD 20 to USD 500, depending on resolution. For value-oriented nameplates, cameras can consume up to 3% of vehicle material cost, squeezing margins. Ford's 2025 recall of 1.075 million vehicles over rear camera software faults underscores the warranty exposure linked with added complexity. Tier 1 suppliers are responding with consolidated vision ECUs and single-cable architectures, but near-term cost headwinds still trim 1.8 percentage points from the automotive camera market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The automotive camera market size for passenger vehicles stood at USD 6 billion in 2024, equal to 67.23% of global revenue. Light commercial vehicles, while smaller today, are expanding at an 11.51% CAGR through 2030, outpacing overall growth. Fleet owners embrace cameras to trim insurance costs, curb collisions, and support telematics-based driver scoring. Volvo Trucks reports fuel savings of 2% when camera monitor systems replace traditional mirrors. The automotive camera market, therefore, sees rising procurement from logistics firms that can quantify ROI.

Passenger cars keep leadership because of scale production and consumer willingness to pay for safety packs. ADAS penetration exceeded 90% in new light-duty vehicles in 2025, ensuring a stable installed base. In heavy trucks, camera adoption aligns with regulatory milestones such as the EU's GSR II blind-spot detection rule. Stoneridge's MirrorEye system on Freightliner Cascadia heavy trucks has demonstrated 8-camera redundancy that may later cascade to consumer SUVs. The blend of cost-down modules and proven fleet savings sustains a double-digit rise in the automotive camera market across commercial segments.

Viewing cameras retained a 57.33% revenue share in 2024, anchoring the automotive camera market share around reversing, surround, and mirror replacement functions. Yet, sensing and stereo units are scaling at 13.44% CAGR as OEMs prioritize perception over display. Subaru's next-gen EyeSight leverages onsemi Hyperlux AR0823AT sensors to offer lane-centering precision previously limited to lidar setups. Depth-perception stereo rigs are now validated to Automated Driving Systems (ADS) Level 3 in Japan, driving broader uptake. As sensing cameras migrate into affordable trims, the automotive camera market size within perception sub-segments will narrow the gap against legacy viewing categories.

Traditional viewing systems evolve too, with higher HDR and de-spray coatings that maintain clarity in road grime. Automakers are integrating bird-eye computational mosaics that require frame-accurate synchronization across four cameras, pushing suppliers to deliver low-skew imagers. Foresight's stereo algorithm bundles deliver object detection at sub-0.05 lux, positioning sensing cameras as a cost-effective alternative to lidar. Overall, image-based perception advantages and falling BOMs are pivoting growth toward the intelligence end of the automotive camera market.

The Automotive Camera Market Report is Segmented by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and More), Type (Viewing (Surround/Rear/Front/Interior) and More), Technology (Digital (CMOS), and More), Application (Park Assist and More), Sales Channel (OEM-Installed and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) and for all the Above Segments.

Asia-Pacific dominated the automotive camera market with a 40.32% share in 2024, buoyed by China's production scale and Japan's semiconductor leadership. Sony targets a significant global share in automotive imagers by fiscal 2026, reinforcing regional supply-chain competitiveness. Beijing's smart-vehicle roadmap subsidizes Level 2+ systems, making multi-camera packages standard even in economy EVs. South Korea's OEMs embed advanced surround-view on every new SUV, underpinned by local sensor and lens fabrication. Such a policy and industrial depth secure APAC's anchor position in the automotive camera market.

North America held a 26.22% share in 2024 as consumer demand for high-end safety features dovetailed with NHTSA mandates. The U.S. rule obliging automatic emergency braking by 2029 incentivizes early camera adoption to spread validation costs over longer cycles. Canadian provinces offer fleet insurance rebates for dash-cams, expanding the retrofit pool. Silicon Valley chip firms provide edge-AI reference designs that reduce time-to-market for domestic OEMs. These factors keep the region's automotive camera market on a firm expansion track.

Europe captured 23.29% share, driven by being first to legislate comprehensive camera-based safety under GSR II. German luxury brands equip vehicles with up to 10 cameras to secure 5-Star Euro NCAP scores. The bloc's e-mirror approval delivers a fresh windfall as EV makers adopt drag-cutting virtual mirrors. However, GDPR imposes strict data processing rules that limit broader analytics, slightly moderating growth relative to APAC.

The Middle East and Africa region accounted for 6.76% of 2024 revenue, thanks to safety-equipment mandates in Gulf Cooperation Council states and expanding urbanization. Saudi Arabia's emerging automotive split-view camera ecosystem underpins domestic assembly ambitions. South America remained at 5% share, yet Brazil's 2026 plan to align with UN ECE rearview camera standards sets a multi-year upgrade cycle. Overall, differential regulation timing drives geographic dispersion within the automotive camera market.