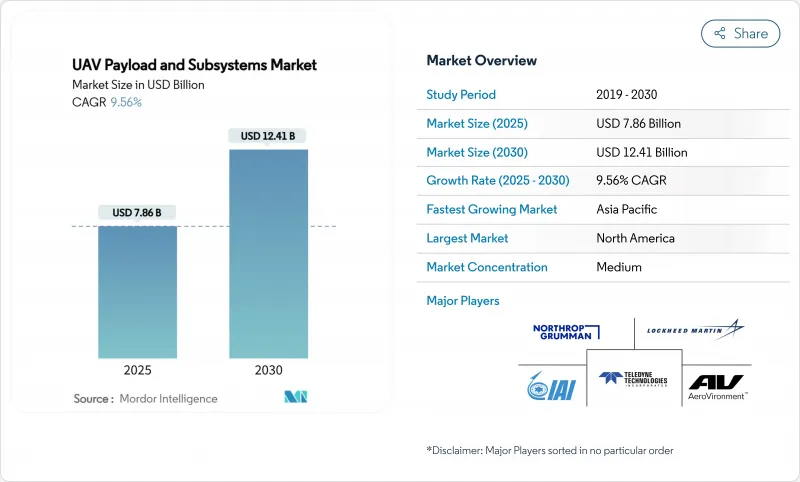

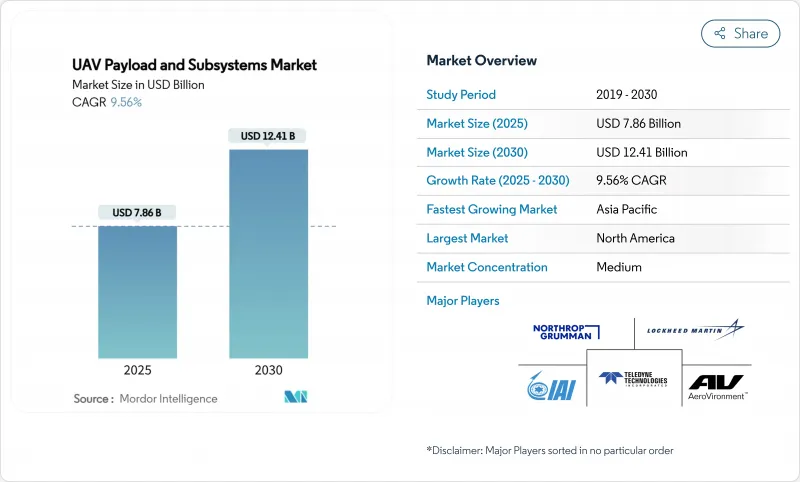

UAV 페이로드 및 서브시스템 시장은 2025년에 78억 6,000만 달러로 평가되었으며, 2030년에 124억 1,000만 달러에 이를 것으로 예측되며, CAGR 9.56%를 나타낼 전망입니다.

지속적인 군사 현대화 프로그램, 증가하는 국방 지출, 무인 플랫폼으로의 제도적 전환이 이러한 성장 궤도를 뒷받침하고 있습니다. 미국 국방부만 해도 2025 회계연도에 무인 차량 획득 및 연구개발(R&D)에 101억 달러를 배정하며 지속적인 연방 정부의 의지를 강조했습니다. 전자전(EW) 페이로드는 10.35%로 가장 빠른 부문 연평균 복합 성장률(CAGR)을 기록하는 반면, 전술용 무인항공기(UAV)는 여전히 물량 측면에서 선두를 유지하며 UAV 등급 세분화 시장의 27.85%를 차지하고 있습니다. 지역별로는 북미가 2024년 35.45% 점유율로 최대 시장을 유지하지만, 아시아태평양 지역이 9.75%의 최고 CAGR을 기록할 전망입니다. 이는 동아시아의 국방 지출이 2023년 4,110억 달러로 급증한 데 따른 것입니다. 내구성이 중요한 추진 및 전력 하위 시스템이 37.85%의 점유율을 차지하는 반면, 비행 제어 시스템은 GPS가 차단된 환경에서 자율성이 필수 요소가 되면서 11.23%의 CAGR을 기록하고 있습니다.

정보, 감시, 정찰(ISR) 예산 증가는 정보 우위가 현대 군사 계획 수립에 미치는 영향을 강조합니다. 2025 회계연도 미국 예산은 센서 융합과 실시간 처리를 결합한 무인 시스템에 101억 달러를 배정했습니다. 일본, 한국, 호주의 유사한 지출 동향은 신속한 데이터 순환이 킬 체인을 단축하고 승무원을 보호합니다는 공통된 인식을 확인시켜 줍니다. 조달 기관들은 이제 단일 통과 동안 원시 영상을 실행 가능한 정보로 변환할 수 있는 다중 스펙트럼 센서, 고대역폭 데이터 링크, 기내 분석 기술을 우선시합니다. 이러한 수요 급증으로 무인기 탑재체 및 하위 시스템 시장은 향후 10년간 지속적 두 자릿수 성장을 이룰 전망입니다.

엣지 컴퓨팅 칩셋은 클라우드 연결 없이도 드론이 위협을 식별하고 비행 경로를 조정할 수 있게 합니다. MIT 테스트에서 궤적 추적 오류를 50% 감소시켜, 전파 방해로 명령 링크가 차단될 때 기내 추론이 자율성을 향상시킨다는 점을 입증했습니다. 군 당국은 이제 진동, 온도 변화, 전자기 공격을 견디는 견고한 AI 하드웨어를 요구하여 GNSS 신호가 사라져도 임무 완수를 보장합니다. 이러한 프로세서는 또한 신속한 센서 융합을 가능하게 하여 운영자가 동일한 기체에 더 많은 탑재체 유형을 장착할 수 있게 합니다. 결과적으로 고급 GPU와 신경 가속기를 통합하는 항공 전자 장비 공급업체들은 주문량이 증가하고 있습니다.

ITAR, EAR, MTCR 규정은 제조사가 모든 부품과 고객을 심사하도록 의무화하여 수개월간 납품을 지연시킬 수 있는 서류 작업을 발생시킵니다. 기업들은 종종 고급 암호화, 사거리 또는 탑재량 옵션을 제거한 ‘수출 경량화’ 버전을 설계하여 규정 준수를 위해 성능을 희석시킵니다. 소규모 혁신 기업들은 법적 부담으로 고전하며, 사내 규정 준수 팀을 유지하는 주요 기업들에게 시장 점유율을 내주고 있습니다. 민간 항공 규제 기관은 국가 영공 비행 전 '시각적 회피 센서'와 '안전 장치 제어 시스템'을 의무화하며 추가 장벽을 세운다. 이러한 규제들은 첨단 하위 시스템의 글로벌 확산을 제한합니다.

2024년 UAV 페이로드 및 서브시스템 시장의 31.25%, 24억 6,000만 달러를 센서가 차지합니다. 그러나 전자전 구성은 스펙트럼 지배가 필수적이 됨에 따라 CAGR 10.35%로 다른 것을 능가합니다. 전자전용 UAV 페이로드 및 서브시스템 시장 규모는 레거시 기체에 뒷받침할 수 있는 모듈형 포드 아키텍처에 의해 2030년까지 두배로 될 것으로 예측되고 있습니다. 미국 해병대가 MQ-9 실증기에 T-SOAR 포드를 탑재한 것은 능동적 대 레이더 대책으로의 독트린의 전환을 강조하고 있습니다.

소형화된 활공탄약 및 체공형 탄두의 부양으로 무장 탑재체는 중간 단일자리 수 성장률을 기록합니다. 이미징 페이로드는 인공지능 기반 자동 표적 인식 알고리즘으로 운영자 업무 부담을 경감시켜 이점을 얻는다. 통신 및 데이터 링크는 RF 혼잡으로 어려움을 겪지만, 군집에서 탄력적인 메시 네트워크를 보장하는 L-밴드 및 S-밴드 중계기에 대한 수요는 지속됩니다. 화학 탐지, 사이버 정보 유출 키트 등 틈새 ‘기타’ 페이로드는 소규모이지만 전략적인 주문을 확보합니다.

추진 및 전력 시스템은 2024년 37.85% 점유율을 유지하며 주요 비용 요소 지위를 반영했습니다. 중유 엔진, 하이브리드 발전기, 고전압 배전 하네스가 조달을 주도합니다. 반면 자율성 요구로 인해 비행 제어 소프트웨어 및 하드웨어는 하위 시스템 중 최고인 연간 11.23% 성장할 전망입니다. 비행 제어 시스템과 연계된 무인기 탑재체 및 하위 시스템 시장 규모는 2025년 12억 달러에서 2030년 21억 달러로 증가할 전망입니다. 드레이퍼의 스트라토론치 탈론-A1용 유도 패키지는 첨단 제어 법칙이 초음속 비행 프로필을 어떻게 가능하게 하는지 보여줍니다.

항법 및 유도 모듈은 MEMS 관성 센서를 천체 및 지형 참조 업데이트와 결합해 GNSS 없이도 정밀도를 유지합니다. 허니웰의 소형 관성 항법 시스템은 센티미터 단위 정확도를 제공해 임무 범위를 확대합니다. 통신 하위 시스템은 방해 방지 모드를 갖춘 개방형 아키텍처 무선으로 전환 중입니다. 자동 발사 및 회수 장비는 도로나 함정 갑판에서의 분산 작전을 지원하기 위해 급속히 진화하고 있습니다.

북미의 성숙한 방위 생태계는 2024년 글로벌 매출의 35.45%를 차지했습니다. 해당 지역은 강력한 연구개발(R&D) 및 교육(E) 자금 지원, 산업-정부 공동 연구소, 명확한 획득 로드맵의 혜택을 받고 있습니다. 무인기 탑재체 및 하위 시스템 시장은 MQ-25, XQ-58, 협동 전투기 프로토타입과 같은 대량 생산 프로그램을 활용하여 안정적인 OEM 주문량을 확보하고 있습니다.

아시아태평양 지역은 9.75%라는 가장 가파른 연평균 성장률(CAGR)을 기록했습니다. 영토 갈등 고조로 중국, 인도, 일본, 한국에서 자체 개발 프로그램이 촉진되고 있습니다. 인도의 합작 공장은 중유 엔진과 복합재 날개를 생산하며, 싱가포르 국방연구청은 현지 중소기업과 AI 항법 칩을 공동 개발합니다. 정부 오프셋 정책은 현지 콘텐츠를 의무화하여 지역 내 공급업체 진출을 장려합니다.

유럽은 NATO 상호운용성 요구사항에 힘입어 가치 기준 3위를 차지합니다. 유로드론 MALE 프로젝트와 영국 및 이탈리아의 충성스러운 윙맨(Loyal Wingman) 프로젝트는 STANAG 표준 인증 센서 및 전자전(EW) 탑재체 수요를 견인합니다. 그러나 엄격한 수출 규정이 제3국 판매를 종종 저해합니다.

중동은 급속한 능력 확보와 연계된 불규칙하지만 상당한 수요를 보인다. 사우디아라비아와 UAE는 기술 이전 확보를 위해 현지화 최종 조립 라인에 투자하는 반면, 이스라엘의 부품 공급업체들은 레이더, EO-IR, 데이터링크 키트 수출을 지속하고 있습니다. 아프리카는 재정 제약으로 인해 초기 단계에 머물러 있으나, 국경 보안을 위해 저렴한 중국 및 터키산 전술 모델을 도입 중입니다.

The UAV payload and subsystems market is valued at USD 7.86 billion in 2025 and is forecasted to reach USD 12.41 billion by 2030, advancing at a 9.56% CAGR.

Ongoing military-modernization programs, higher defense outlays, and institutional shifts toward unmanned platforms anchor this growth trajectory. The US Department of Defense alone earmarked USD 10.1 billion for unmanned-vehicle acquisition and R&D in fiscal 2025, highlighting sustained federal commitment. Electronic-warfare (EW) payloads post the fastest segment CAGR at 10.35%, while tactical UAVs remain the volume leaders, capturing 27.85% of the UAV-class segmentation. Regionally, North America retains the largest position with a 35.45% share in 2024, but Asia-Pacific logs the highest 9.75% CAGR, propelled by East Asia's defense-spending jump to USD 411 billion in 2023. Endurance-critical propulsion and power subsystems command 37.85% share, whereas flight-control systems record an 11.23% CAGR as autonomy becomes essential in GPS-denied environments.

Rising intelligence, surveillance, and reconnaissance allocations underline how information dominance shapes modern force planning. The FY-2025 US budget dedicates USD 10.1 billion to unmanned systems that blend sensor fusion with real-time processing. Comparable spending moves in Japan, South Korea, and Australia confirm a shared belief that faster data cycles shorten the kill chain and protect crews. Procurement offices now prioritize multi-spectral sensors, high-bandwidth datalinks, and onboard analytics that can convert raw imagery into actionable cues during a single pass. This demand surge positions the UAV payload and subsystems market for sustained double-digit growth through the decade.

Edge-computing chipsets allow drones to identify threats and adjust flight paths without cloud connectivity. MIT testing cut trajectory-tracking error by 50%, proving that onboard inference improves autonomy when jamming blocks command links. Militaries now specify rugged AI hardware that endures vibration, temperature swings, and electromagnetic attack, ensuring mission completion even when GNSS signals vanish. These processors also enable rapid sensor fusion, letting operators push more payload types onto the same airframe. As a result, avionics suppliers that integrate advanced GPUs and neural accelerators see rising order volumes.

ITAR, EAR, and MTCR rules oblige manufacturers to vet every component and customer, creating paperwork that can delay deliveries by months. Firms often design "export-light" versions that drop advanced encryption, range, or payload options, diluting performance to stay compliant. Smaller innovators struggle with the legal overhead, ceding market share to primes that maintain in-house compliance teams. Civil aviation regulators add another layer, mandating see-and-avoid sensors and fail-safe controls before flights in national airspace. Together, these barriers restrict the global diffusion of cutting-edge subsystems.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sensors accounted for USD 2.46 billion and 31.25% of the UAV payload and subsystems market in 2024. Electronic-warfare configurations, however, will outpace all others at a 10.35% CAGR as spectrum dominance becomes indispensable. The UAV payload and subsystems market size for EW is forecast to double by 2030, helped by modular pod architectures that retrofit onto legacy airframes. US Marine Corps integration of T-SOAR pods on MQ-9 demonstrators underscores a doctrine shift toward active counter-radar measures.

Weaponized payloads log mid-single-digit growth, buoyed by miniaturized glide munitions and loitering warheads. Imaging payloads gain from AI-powered automatic-target-recognition algorithms, easing operator workload. Communications and datalinks struggle with RF congestion, yet demand persists for L-band and S-band relays that guarantee resilient mesh networks in swarms. Niche "other" payloads-chemical detection, cyber-exfiltration kits-capture small but strategic orders.

Propulsion and power retained a 37.85% share in 2024, reflecting their status as the primary cost element. Heavy-fuel engines, hybrid generators, and high-voltage distribution harnesses dominate procurement. Conversely, flight-control software and hardware will grow 11.23% annually, the highest among subsystems, as autonomy drives procurement. The UAV payload and subsystems market size tied to flight-control suites is projected at USD 2.1 billion by 2030, up from USD 1.2 billion in 2025. Draper's guidance package on Stratolaunch's Talon-A1 shows how advanced control laws enable hypersonic profiles.

Navigation and guidance modules blend MEMS inertial sensors with celestial and terrain-referenced updates to maintain precision without GNSS. Honeywell's Compact Inertial Navigation System delivers centimeter accuracy, widening mission envelopes. Communications subsystems pivot toward open-architecture radios with anti-jam modes. Automated launch-and-recovery gear is evolving rapidly to support dispersed operations from roads or naval decks.

The UAV Payload and Subsystems Market Report is Segmented by Payload Type (Sensors, Weaponry, and More), Subsystem Type (Propulsion and Power, and More), UAV Class (Nano and Micro UAVs, Mini UAVs, and More), End User (Military and Law Enforcement), Application (Combat and Strike, Logistics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America's mature defense ecosystem delivered 35.45% of global revenue in 2024. The region benefits from robust R&D and E funding, joint industry-government labs, and clear acquisition roadmaps. The UAV payload and subsystems market leverages volume programs such as MQ-25, XQ-58, and collaborative-combat-aircraft prototypes, ensuring stable OEM order books.

Asia-Pacific registers the steepest 9.75% CAGR. Rising territorial tensions spur indigenous development programs across China, India, Japan, and South Korea. Joint-venture factories in India produce heavy-fuel engines and composite wings, while Singapore's defense-research agency co-develops AI-navigation chips with local SMEs. Government offsets mandate local content, encouraging supplier footprints across the region.

Europe ranks third by value, sustained by NATO interoperability mandates. The Eurodrone MALE initiative and loyal-wingman projects in the United Kingdom and Italy anchor demand for sensor and EW payloads certified to STANAG standards. However, stringent export rules occasionally hamper third-country sales.

The Middle East shows lumpy yet significant demand tied to rapid capabilities acquisition. Saudi Arabia and the UAE invest in localized final-assembly lines to secure technology transfer, while Israel's component suppliers continue exporting radar, EO-IR, and datalink kits. Africa remains nascent and limited by fiscal constraints, but is adopting affordable Chinese and Turkish tactical models for border security.