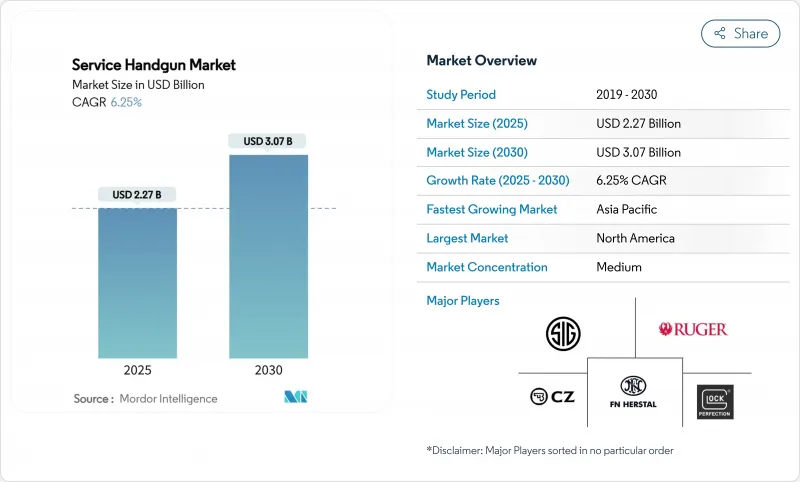

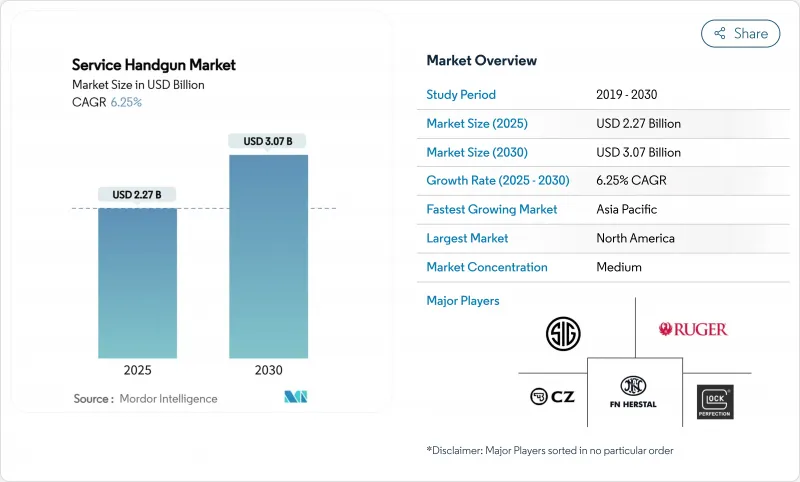

군용 권총 시장 규모는 2025년에 22억 7,000만 달러로 평가되었고, 2030년에 30억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 6.25%를 나타낼 전망입니다.

국방 현대화, 법 집행 기관의 군수품 동시 업등급, 그리고 더블 액션 권총을 스트라이커 발사식 플랫폼으로 빠르게 대체하는 추세가 성숙 및 신흥 조달 프로그램 전반에 걸쳐 수요를 지속적으로 유지하고 있습니다. 모듈식 광학장비 장착 가능 설계가 이제 사양 목록을 지배하며, 무기 전체 교체 없이도 신속한 기술 갱신이 가능해졌습니다. 지역별 추세는 고르지 않습니다: 북미가 가장 큰 설치 기반을 유지하고 있지만, 아시아태평양 지역은 자국 내 제조가 확대되고 전략적 비축이 시급해지면서 가장 빠른 성장을 보이고 있습니다. 탄약부터 총기까지 수직 통합된 그룹이 주도하는 통합 활동과 니트로셀룰로오스 같은 핵심 소재의 공급망 취약성은 가치 사슬 전반에 걸쳐 협상력을 재편하고 있습니다.

국방 기관들은 점진적 개량을 넘어 상호운용성, 액세서리 레일 호환성, 센서 통합을 확보하기 위해 완전한 권총 교체 방식을 선호하고 있습니다. 독일은 특수부대 장비를 표준화하기 위해 밀폐형 발광체 광학장치와 개선된 방아쇠를 장착한 발터 P14 권총 3,200정과 P14K 권총 3,300정을 주문했습니다. 호주의 '프로젝트 랜드 300'은 단일 아키텍처 하에 레드닷 사이트, 전술 조명, 비살상 훈련 모듈을 장착한 SIG P320 기반 F9 시스템을 도입했습니다. 이러한 프로그램들은 기존 군용 권총이 미래 성능 업등급를 수용할 수 없음을 강조하며, 군용 권총 시장을 뒷받침하는 연속적인 조달 주기를 촉진하고 있습니다.

경찰 기관들은 일관된 방아쇠 당김, 간편한 유지보수, 광학장비 호환성을 우선시합니다. 펜실베이니아 주 경찰은 직접 가공된 Aimpoint ACRO 호환성과 인체공학적 개선을 이유로 Walther PDP를 선택했습니다. 하트퍼드 경찰은 .40구경 Glock 22/23 Gen4에서 9mm Glock 17/19 Gen5로 전환하며 향상된 종단 성능, 낮은 반동, 저렴한 탄약을 근거로 제시했습니다. 특정 스트라이커 방식 모델과 관련된 개별적인 안전 문제에도 불구하고, 전반적인 추세는 여전히 스트라이커 메커니즘을 선호하며, 이는 서비스 권총 시장 전반의 성장을 강화하고 있습니다.

ITAR에서 EAR 감독으로의 전환은 변경되지 않은 제품 라인에 대해서도 완전한 규정 준수 개편을 요구합니다. 산업안보국(BIS)의 확대된 감사 인력은 집행 위험을 높이며, 대부분의 권총 수출은 여전히 허가가 필요해 리드 타임을 연장합니다. 복잡한 이중용도 기술 규정은 관료적 마찰을 가중시켜 소규모 생산자를 위축시키며, 성숙한 규정 준수 인프라를 보유한 기업 중심으로 군용 권총 시장을 우연히 통합하는 문턱을 설정합니다.

권총은 2024년 매출의 88.67%를 차지하며, 리볼버 대비 더 큰 탄창 용량과 빠른 재장전 속도로 무장 전문가들의 기본 보조 무기 지위를 공고히 했습니다. 리볼버는 11.33%에 그쳤으나, 특수 부대가 여전히 민감한 작전에서 기계적 단순성과 회수 불가능한 탄피 장점을 높이 평가함에 따라 전체 서비스용 권총 시장 성장률(6.98% CAGR)을 상회할 전망입니다. 역사적으로 공유된 안정성은 플랫폼 전환보다 혁신이 조달을 주도함을 보여줍니다. 군용 권총 시장은 교체 가능한 백스트랩, 모듈식 프레임, 광학장치 장착부를 제공하는 권총 제조사에 계속해서 보상을 주는 반면, 리볼버 공급업체들은 훈련 및 은밀한 시나리오에서 틈새 역할을 개척하고 있습니다.

비록 리볼버가 제한된 상황에서 전술적 부활을 보이고 있지만, 권총은 제도적 선호도를 유지하고 있습니다. 호주의 브라우닝 하이파워 계열 교체와 같은 대규모 조달 프로그램은 기존 플랫폼의 13발 대비 17발 탄창의 필요성을 언급했습니다. 최신 스트라이커 방식 권총이 향상된 인체공학과 액세서리 레일을 제공함에 따라 대체품과의 격차는 더욱 벌어지고 있습니다. 그럼에도 현대적 금속 공학과 개선된 더블 액션 방아쇠로 대응하는 리볼버 제조사들은 하위 부문의 수익성을 유지하며 다양한 군용 권총 시장을 지속할 것으로 보입니다.

스트라이커 방식 권총은 2024년 매출의 72.56%를 차지했으며, 7.01%의 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 이는 서비스용 권총 시장에서 점유율 1위 디자인이 동시에 가장 빠르게 성장하는 드문 사례다. 매 발사마다 일관된 방아쇠 당김은 훈련을 단순화하며, 부품 수가 적어 자원 제약이 있는 부서의 유지보수 비용을 절감합니다. 15.22% 점유율을 기록한 싱글 액션 권총은 정밀 사격에 중점을 둔 팀을 대상으로 하며, 12.22% 점유율을 차지한 더블 액션 시스템은 일부 기관이 구형 재고를 아직 교체하지 않았기 때문에 주로 유지되고 있습니다.

스트라이커 발사 방식의 부상은 조달 문서에 낙하 안전 의무와 현장 측정 기준이 명시되면서 가속화되고 있으며, 이는 기존 설계가 이미 초과 달성한 수준입니다. 따라서 서비스 핸드건 시장은 자기강화적 순환을 경험합니다: 기관들이 스트라이커 발사 플랫폼으로 전환하면, 애프터마켓 홀스터 및 광학 장비 생태계가 해당 플랫폼에 집중되고, 신규 입찰은 더 잘 지원되는 구성으로 기울어진다. 더블 액션 플랫폼은 제한된 역할에서 지속되겠지만, 자본 투자는 스트라이커 개발 로드맵 쪽으로 기울어질 전망입니다.

북미는 기관 현대화 예산과 지역 경찰 장비 업등급를 지원하는 연방 보조금 덕분에 2024년 매출의 40.10%를 유지했습니다. 미국 관세국경보호청(CBP)의 차세대 GLOCK 9mm 권총 도입은 훈련 기관, 무기 관리관, 애프터마켓 공급업체 전반에 파급되는 조달 프로그램을 반영합니다. 캐나다의 SIG P320 권총 1,940만 캐나다 달러(1,422만 달러) 규모 주문은 지역 간 상호운용성 목표를 강조합니다. 이 지역의 연평균 성장률(CAGR) 5.8%는 글로벌 성장세에 미치지 못하지만, 성숙한 조달 체계는 군용 권총 시장 전반에 걸쳐 꾸준한 기본 수요를 창출하고 있습니다.

아시아태평양 지역은 자립 정책과 위협 인식이 자금 조달을 가속화하며 가장 빠른 8.21% CAGR을 달성할 전망입니다. 호주의 F9 도입은 가상 훈련 모듈을 포함하며, 인도의 ‘메이크 인 인디아’ 정책은 외국 주요 기업들을 현지 합작 투자로 유인하고 있습니다. “아스미(Asmi)”와 같은 자국산 기관단총 프로그램은 정부가 국내 생산 역량을 전략적 자산으로 인식함을 시사합니다. 이러한 요소들이 결합되어 해당 지역은 군용 권총 시장의 성장 동력이자 잠재적 제조 허브로 부상하고 있습니다.

유럽은 NATO 표준화 및 다국간 입찰에 힘입어 2024년 28.45% 점유율로 마감했습니다. 독일의 P13 경쟁과 덴마크의 SIG P320 채택은 대량 구매 할인을 극대화하는 엄격하지만 공동 조달 방식을 보여줍니다. 중동 및 아프리카(15.20%)는 대규모 국방 예산과 카라칼 같은 국내 제조사가 만나는 기회 중심지로 남아 있으며, 카라칼은 인도네시아 및 인도와의 생산 제휴를 통해 수출 비중을 두 배로 늘렸다. 공급망 주권화 추세로 인해 소규모 국가들조차 현지 조립을 추진하며, 이 지역은 서비스용 권총 시장 전반에 걸쳐 다각화된 수익원을 모색하는 글로벌 OEM 기업들에게 매력적인 시장으로 남아 있습니다.

The service handgun market size is estimated at USD 2.27 billion in 2025, and is expected to reach USD 3.07 billion by 2030, reflecting a CAGR of 6.25% during the forecast period.

Strong defense modernization, synchronized law-enforcement fleet upgrades, and the rapid displacement of double-action pistols by striker-fired platforms continue to sustain demand across mature and emerging procurement programs. Modular optics-ready designs now dominate specification lists, enabling fast technology refresh without entire weapon replacement. Regional momentum is uneven: North America retains the largest installed base, yet Asia-Pacific exhibits the quickest expansion as Indigenous manufacturing ramps up and strategic stockpiling gains urgency. Consolidation activity led by vertically-integrated ammunition-to-firearm groups and supply-chain fragilities in critical materials such as nitrocellulose reshape bargaining power along the value chain.

Defense agencies have moved beyond incremental overhauls, favoring complete sidearm replacement to secure interoperability, accessory rail compatibility, and sensor integration. Germany ordered 3,200 Walther P14 and 3,300 P14K pistols with enclosed-emitter optics and enhanced triggers that standardize special-forces equipment. Australia's Project Land 300 fielded the SIG P320-based F9 system with red-dot sights, tactical lights, and non-lethal training mods under a single architecture. These programs underscore that legacy service pistols cannot absorb future capability inserts, prompting contiguous procurement cycles that underpin the service handgun market.

Police agencies prioritize consistent trigger pull, straightforward maintenance, and optics readiness. Pennsylvania State Police chose the Walther PDP, citing direct-milled Aimpoint ACRO compatibility and ergonomic improvements. Hartford Police transitioned from .40 caliber Glock 22/23 Gen4 to 9 mm Glock 17/19 Gen5, referencing improved terminal performance, lower recoil, and cheaper ammunition. Notwithstanding isolated safety concerns tied to specific striker-fired models, the broader trajectory still favors striker mechanisms, reinforcing growth across the service handgun market.

Shifting from ITAR to EAR oversight requires a full compliance overhaul even for unchanged product lines. The Bureau of Industry and Security's larger audit force heightens enforcement risk, and most handgun exports still need licenses, extending lead times. Complex dual-use technology rules add bureaucratic friction that deters smaller producers, setting thresholds that inadvertently consolidate the service handgun market around firms with mature compliance infrastructure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pistols delivered 88.67% of 2024 revenue, cementing their status as the default sidearm for armed professionals thanks to greater magazine capacity and faster reloads than revolvers. Revolvers secured only 11.33% yet will outpace overall service handgun market growth at a 6.98% CAGR because specialized units still value their mechanical simplicity and non-recoverable brass advantages in sensitive operations. Historically, shared stability shows that innovation drives procurement rather than platform switching. The service handgun market continues to reward pistol makers that offer interchangeable backstraps, modular frames, and optics cuts, whereas revolver suppliers carve niche roles in training and covert scenarios.

Although revolvers are making a tactical comeback in limited contexts, pistols retain institutional preference. Large procurement programs like Australia's replacement of Browning Hi-Power variants cited the need for 17-round magazines versus the legacy platform's 13-round capacity. As newer striker-fired pistols furnish enhanced ergonomics and accessory rails, they further distance themselves from alternatives. Nevertheless, revolver makers responding with modern metallurgy and improved double-action triggers will likely keep the sub-segment profitable, sustaining a diverse service handgun market.

Striker-fired pistols captured 72.56% 2024 revenue and are forecasted to notch a 7.01% CAGR, a rare instance where the top-share design is also the fastest grower within the service handgun market. Consistent trigger pull across every shot simplifies training, and fewer parts cut maintenance costs for resource-constrained departments. Single-action pistols at 15.22% share cater to precision-oriented teams, while double-action systems with 12.22% share endure mainly because some agencies have yet to refresh legacy inventories.

The striker-fired rise intensifies as procurement documents embed drop-safety mandates and field-gauge standards that current designs already exceed. The service handgun market, therefore, sees a self-reinforcing loop: agencies switch to striker-fired platforms, aftermarket holster and optic ecosystems concentrate there, and fresh bids lean toward the better-supported configuration. Double-action platforms will persist in limited roles, but capital investment tilts toward striker development roadmaps.

The Service Handgun Market Report is Segmented by Type (Revolvers and Pistols), Operation Mechanism (Single-Action, Double-Action, and Striker-Fired), Caliber (9 Mm, . 40 S&W, . 45 ACP, and Other Calibers), Material (Stainless Steel, Polymer Frame, and Aluminum Alloy), End-User (Military, Law Enforcement, and Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 40.10% 2024 revenue thanks to agency modernization budgets and federal grants that support local police upgrades. US Customs and Border Protection's switch to new-generation GLOCK 9 mm pistols reflects procurement programs that ripple across training academies, armorers, and aftermarket suppliers. Canada's CAD 19.4 million (USD 14.22 million) order for SIG P320 pistols underscores regional interoperability aims. Although the region's 5.8% CAGR trails global momentum, its mature acquisition frameworks continue to generate steady baseline demand across the service handgun market.

Asia-Pacific will achieve the fastest 8.21% CAGR as self-reliance policies and threat perceptions accelerate funding. Australia's F9 adoption embeds virtual training modules, while India's "Make in India" doctrine lures foreign primes into local joint ventures. Indigenous machine-pistol programs such as "Asmi" signal that governments see in-country capacity as strategic. These factors combine to make the region the growth engine and potential manufacturing hub of the service handgun market.

Europe closed 2024 with a 28.45% share, powered by NATO harmonization and multi-nation tenders. Germany's P13 competition and Denmark's SIG P320 adoption illustrate rigorous but collective procurement that maximizes volume discounts. The Middle East and Africa, holding 15.20%, remain opportunity centers where large defense budgets converge with domestic manufacturers like Caracal, which doubled export ratios by forging Indonesian and Indian production tie-ups. Supply-chain sovereignty themes mean that even smaller states pursue localized assembly, keeping the region attractive to global OEMs seeking diversified revenue streams across the service handgun market.