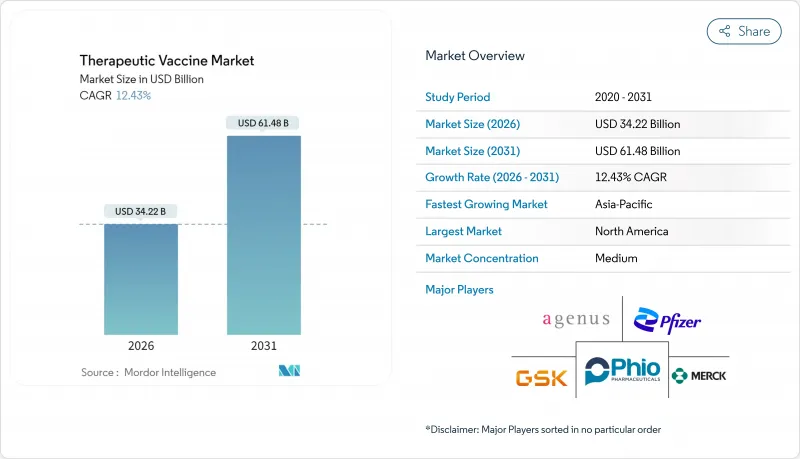

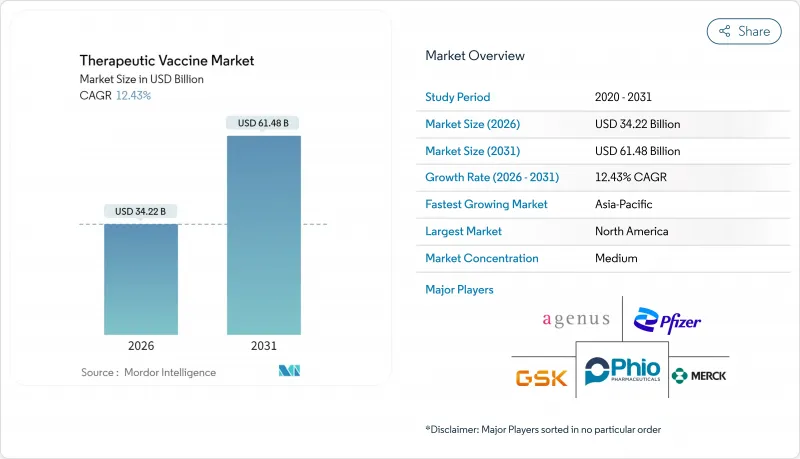

치료용 백신 시장 규모는 2026년 342억 2,000만 달러로 추정되고, 2025년 304억 4,000만 달러에서 성장했으며, 2031년에는 614억 8,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 연평균 성장률(CAGR)은 12.43%로 성장이 전망됩니다.

예방 접종에서 특히 암이나 만성 바이러스 감염증과 같은 활동성 질환에 대처하는 치료 중심의 면역요법 플랫폼으로의 이행에 수요가 확대되고 있습니다. 획기적인 mRNA 승인과 AI 지원에 의한 새로운 항원 발견 기술이 결합되어 개발 사이클의 단축 및 임상 정밀도의 향상이 실현되어 투자자의 신뢰를 강화함과 동시에 규제 당국에 의한 신속 승인 프로세스의 공식화를 촉진하고 있습니다. 팬데믹 기간에 증강된 제조 능력은 신규 파이프라인의 신속한 스케일업을 지원하고 있습니다. 또한 Project NextGen과 같은 정부 프로그램은 초기 단계의 위험을 줄이는 비희박화 자본을 제공합니다. 연구개발, 임상제조, 콜드체인 유통을 통합하는 기업은 경쟁 우위성을 낳아 여러 적응증에 걸친 모듈화된 맞춤형 치료법의 신속한 도입이 가능해집니다.

세계의 고령화에 의해 암 발생률이 높아지는 한편, 병원체의 진화에 의해 바이러스성 및 세균성 질환의 부담이 지속되고 있습니다. 치료용 백신은 노출 예방이 아닌 기존 질환과의 싸움을 향해 면역계를 훈련함으로써 이러한 미충족 요구에 대응합니다. 종양학, 만성 B형 간염, 재발성 성기 헤르페스는 지속적인 반응으로 평생 약물 요법을 완화시키는 고 수요 대상 영역입니다. 공중 보건 당국은 치료 요법을 만성 질환 치료제로 대체하는 비용 효율적인 단일 또는 제한 코스 옵션으로 자리매김하고 치유 가능성을 평가하는 상환 체계를 추진하고 있습니다. 그 결과, 선진국과 중소득국 경제권 모두에서 치료용 백신 시장은 지속적인 확대를 계속하고 있습니다.

미국은 차세대 플랫폼(예방을 넘은 치료 응용을 포함)에 50억 달러를 충당하는 '프로젝트 넥스트젠'을 시작했습니다. BARDA의 마일스톤형 보조금은 팬데믹 대응과 만성 질환 치료 모두에 대응 가능한 듀얼 유스 기술을 우선하여 GMP 시설의 정비 가속과 양산화 위험을 저감하고 있습니다. EU의 호라이즌 프레임워크에도 비슷한 조치를 취하고 있으며, CEPI는 다자간 승인 기간을 단축하는 임상시험의 국제표준화를 조정하고 있습니다. 민간 투자자들이 기존에 피해 온 초기 단계의 자금을 공적 자금이 공급함으로써, 치료용 백신 시장은 경기 후퇴에 대한 내성을 강화하고 있습니다.

치료용 백신은 결정적인 데이터를 얻을 때까지 수년 단위의 많은 투자를 필요로 합니다. 생물학적 제조에서는 승인 전에 1억 달러 규모의 자금을 투입하는 경우가 많아 초기 단계 기업의 재무 상황을 압박합니다. 면역학적 변동성은 후기 단계에서의 실패율이 저분자 의약품을 상회하고, 평가 모델을 복잡화시켜, 신중한 신디케이트를 촉진하고 있습니다. 그 결과 일부 파이프라인이 정체되어 치료용 백신 시장에서 예측 성장의 일부를 상쇄하고 있습니다.

암 백신은 2025년에 129억 8,000만 달러 시장 규모를 달성했고, 치료용 백신 시장 전체의 42.63%를 차지했으며, 암 영역이 상업적 보급의 기반임을 뒷받침했습니다. 본 부문은 검증된 항원, 견고한 바이오마커 기반, 고가치 적응증에 연동된 상환제도의 혜택을 받고 있습니다. 체크포인트 억제제와의 병용요법은 반응의 지속성을 높여 암 영역이 치료용 백신 시장 전체에 주는 공헌을 확고하게 하고 있습니다. 감염증 치료용 백신은 72억 2,000만 달러로 규모는 작은 것, 만성 B형 간염이나 헤르페스 후보 백신의 진전에 의해 13.06%의 연평균 복합 성장률(CAGR)로 확대하고 있습니다. 자가면역질환 및 신경질환 카테고리는 아직 발전 도상하면서 파이프라인의 다양화에 있어서 매우 중요하며, 제조 및 규제면에서 공통 학습 곡선을 살리려는 플랫폼 개발자의 관심을 모으고 있습니다. 전반적으로 다양한 제품 포트폴리오는 위험을 완화하고 치료용 백신 산업에서 장기적인 성장 지속에 기여합니다.

2차적인 효과로서 기존 치료가 증상 관리에만 머무르는 다발성 경화증 등의 질환을 대상으로 한 역전 효과나 내성 유도형 백신에 대한 벤처 자금의 재분배가 진행되고 있습니다. 타우 단백질과 α-시누클레인 백신을 포함한 신경질환 프로젝트는 중기 임상시험 단계로 진행되고 있으며, 면역요법이 단백질 응집성 질환에 대처할 수 있다는 확신을 강화하고 있습니다. 이러한 시너지 효과는 투자자의 관심을 지속하고 과학의 용도를 가속화하며 2020년대 말까지 비암 영역에서의 수익 비율을 증가시킵니다.

2025년에는 동종이식형 백신이 197억 달러(치료용 백신 시장 규모의 64.72%에 상당)를 창출했습니다. 이는 유통을 단순화하는 표준화된 기성품 형식 때문입니다. 그 규모의 경제성은 1회 투여당 비용 절감과 로트 릴리스 시간의 단축을 실현하고, 대규모의 공적 입찰에 있어서 매력적입니다. 한편, 자기유래 접근법은 시퀀싱 및 제조 자동화로 리드타임이 단축되기 때문에 2031년까지 13.01%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 환자 특이적 네오 항원은 특히 고형 종양에서 정확도를 향상시키고 객관적 연주 효율을 높이는 것으로 프리미엄 가격을 정당화합니다. 하이브리드 구조 등장 : 공유되는 지질 나노입자 코어와 개별화된 mRNA 삽입부를 결합하여 확장성 및 개별화의 균형을 실현합니다. AI 알고리즘에 의한 에피토프 선택의 추가 정교화에 따라, 홈메이드 방법 및 '반개별화' 포맷은 치료용 백신 시장에서 점유율을 확대할 것으로 예측됩니다.

플랫폼 수렴은 운영상의 민첩성을 촉진합니다. 시설에서는 현재 동일한 클린룸 내에서 플라스미드 DNA, mRNA, 단백질 서브유닛의 제조를 전환할 수 있는 멀티모달 설비를 도입하고 있습니다. 이 유연성은 유휴 설비를 줄이고 린 생산 방식의 경제성을 지원합니다. 파이프라인이 적응증 특화형으로 이동하는 가운데, 이러한 특성은 필수가 될 것입니다.

북미는 2025년 세계 수익의 41.12%를 차지했으며, FDA의 획기적인 지정, 집중적인 벤처 캐피탈 자금, 신속한 대상 등록 네트워크의 강점을 배경으로 했습니다. 프로젝트 넥스트젠 및 BARDA 조성금은 보스턴에서 샌디에고에 이르는 학산 연계 허브를 지지하고, 한편 머크의 10억 달러 규모의 더럼 공장 확장이나 화이자의 4억 6,500만 달러를 투입한 카라마주 공장의 업그레이드 등에 의해 충전 및 포장 공정의 잉여 생산 능력이 탄생했습니다. 상환 프레임워크는 조기 도입을 촉진하고 FDA 승인의 획기적인 제품에 대한 CMS의 전환 적용 규칙이 그 좋은 예입니다.

유럽에서는 대규모 관민 컨소시엄 및 호라이즌 유럽 조성금이 트랜스레이셔널 리서치를 주도하고 있습니다. 유럽 의약품청(EMA)의 PRIME 및 조건부 승인 프로그램은 독일과 프랑스의 가치를 기반으로 한 가격 책정 파일럿 사업과 협력하여 높은 필요성 적응증의 조기 시장 진입을 가능하게 합니다. 할레에 건설된 와커사의 1억 유로 규모 mRNA 센터 등의 시설이 유럽 대륙공급 안정성을 강화하고 있습니다. 그러나 각 국가의 지불자 협상이 끊어지기 때문에 균일한 접근이 지연될 수 있으며, 북미에 비해 도입 속도가 둔화되고 있습니다.

아시아태평양은 2031년까지 13.22%라는 가장 빠른 CAGR로 추이할 전망이며, 중국의 규제 근대화와 제조 비용 우위성이 그 기반이 되고 있습니다. 현지 바이오텍 기업은 특허 링크 제도를 활용하여 구미 기업과의 공동 개발을 진행함과 동시에 싱가포르와 한국에 신설된 CDMO 캠퍼스가 세계 고객에게 공급합니다. 일본에서는 고령화와 암 치료의 고액 상환이 단가를 밀어 올려 수량 성장의 둔화를 상쇄합니다. 지역 정부에 의한 콜드체인 정비에 대한 자금 투입은 국내 및 수출 시장 양쪽 공급 능력을 확대해, 치료용 백신 시장에 있어서 아시아태평양의 영향력 증강에 기여합니다.

The therapeutic vaccines market size in 2026 is estimated at USD 34.22 billion, growing from 2025 value of USD 30.44 billion with 2031 projections showing USD 61.48 billion, growing at 12.43% CAGR over 2026-2031.

Demand expands as companies shift from preventive inoculation toward treatment-focused immunotherapy platforms that tackle active disease, particularly cancer and chronic viral infections. Breakthrough mRNA approvals, together with AI-assisted neo-antigen discovery, shorten development cycles and improve clinical precision, bolstering investor confidence and prompting regulators to formalize expedited pathways. Manufacturing capacity added during the pandemic now underpins rapid scale-up for new pipelines, while government programs such as Project NextGen supply non-dilutive capital that reduces early-stage risk. Competitive advantage accrues to firms that integrate R&D, clinical manufacturing, and cold-chain distribution, allowing faster launch of modular, personalized regimens across multiple indications .

Global aging drives higher cancer incidence, while evolving pathogens sustain viral and bacterial disease burdens. Therapeutic vaccines address these unmet needs by training the immune system to combat existing illness rather than preventing exposure. Oncology, chronic hepatitis B, and recurrent genital herpes comprise high-volume targets where durable responses lessen lifelong drug therapy . Public health authorities view therapeutic regimens as budget-friendly once-or-limited-course alternatives to chronic medication, encouraging reimbursement frameworks that reward curative potential. The result is sustained expansion of the therapeutic vaccines market across both developed and middle-income economies.

The United States launched Project NextGen with USD 5 billion earmarked for next-generation platforms, including therapeutic applications beyond prevention. BARDA's milestone-based awards prioritize dual-use technologies able to pivot between pandemic response and chronic-disease therapy, accelerating GMP build-outs and de-risking scale-up. Similar instruments appear in the EU Horizon framework, while CEPI coordinates global clinical-trial standardization that shortens multi-country approvals. Public money now supplies early-stage capital that private investors historically avoided, fortifying the therapeutic vaccines market against downturns.

Therapeutic vaccines require multi-year, multimillion-dollar investments before pivotal data emerge. Biological manufacturing often commits USD 100 million ahead of approval, straining balance sheets of early-stage firms. Immunological variability raises late-phase attrition rates above those for small molecules, complicating valuation models and prompting cautious syndicates. Consequently, some pipelines slow, offsetting a portion of forecast growth within the therapeutic vaccines market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cancer vaccines delivered USD 12.98 billion in 2025, equal to 42.63% of therapeutic vaccines market size, affirming oncology as the anchor of commercial adoption. The segment benefits from validated antigens, robust biomarker infrastructure, and reimbursement aligned to high-value indications. Combination regimens with checkpoint inhibitors enhance response durability, cementing cancer's contribution to the broader therapeutic vaccines market. Infectious-disease therapeutics, although smaller at USD 7.22 billion, expand at 13.06% CAGR as chronic hepatitis B and herpes candidates advance. Autoimmune and neurological categories remain nascent yet critical for pipeline diversity, attracting platform developers eager to leverage shared manufacturing and regulatory learning curves. Overall, diversified product baskets reduce portfolio risk and help sustain long-term expansion within the therapeutic vaccines industry.

A second-order effect is the reallocation of venture dollars toward inverse and tolerance-inducing vaccines, targeting diseases such as multiple sclerosis where existing therapies only manage symptoms. Neurological projects-including tau and alpha-synuclein vaccines-progress through mid-stage trials, reinforcing confidence that immunotherapy can address protein-aggregation disorders. Together these dynamics sustain investor appetite, accelerate science translation, and increase the proportion of revenues derived from non-oncology indications by the end of the decade.

Allogeneic constructs generated USD 19.7 billion in 2025, equivalent to 64.72% of therapeutic vaccines market size, owing to standardized, off-the-shelf formats that simplify distribution. Their economies of scale produce lower per-dose cost and faster lot release, attractive for large public tenders. Autologous approaches, however, record a 13.01% CAGR through 2031 as sequencing and manufacturing automation shrink lead times. Patient-specific neo-antigens improve precision, particularly in solid tumors, yielding higher objective-response rates that justify premium pricing. Hybrid architectures emerge: shared lipid-nanoparticle cores paired with individualized mRNA inserts, thereby balancing scalability and personalization. As AI algorithms further refine epitope selection, autologous and "semi-personalized" formats are expected to raise their share of the therapeutic vaccines market.

Platform convergence also fosters operational agility. Facilities now host multi-modal suites able to switch between plasmid DNA, mRNA, and protein subunit runs within the same cleanroom footprint. This flexibility reduces idle capacity and supports lean manufacturing economics, traits that will be essential as pipelines become increasingly indication-specific.

The Therapeutic Vaccine Market is Segmented by Products (Autoimmune Disease Vaccines, Cancer Vaccines, and More), Technology (Allogeneic Vaccines and Autologous Vaccines), Age Group (Adults and More), Distribution Channel (Public and Private) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market and Forecasts are Provided in Terms of Value (USD).

North America contributed 41.12% of global revenue in 2025 on the strength of FDA breakthrough designations, concentrated VC funding, and rapid enrollment networks. Project NextGen and BARDA grants sustain academic-industry hubs from Boston to San Diego, while expansions such as Merck's USD 1 billion Durham plant and Pfizer's USD 465 million Kalamazoo upgrade create surplus fill-finish capacity. Reimbursement frameworks encourage early adoption, exemplified by CMS transitional-coverage rules for FDA-cleared breakthrough products.

Europe follows with substantial public-private consortia and Horizon Europe grants guiding translational research. EMA's PRIME and Conditional Approval programs align with value-based pricing pilots in Germany and France, enabling earlier market entry for high-need indications. Facilities such as WACKER's EUR 100 million mRNA center in Halle bolster continental supply security. However, fragmented national payer negotiations can delay uniform access, tempering uptake relative to North America.

Asia-Pacific posts the fastest 13.22% CAGR through 2031, anchored by China's regulatory modernization and manufacturing-cost advantage. Local biotechs leverage patent linkage to co-develop with Western firms, while new CDMO campuses in Singapore and South Korea supply global clients. Japan's aging demographic and premium reimbursement for oncology care lift unit prices, offsetting slower volume growth. Regional governments also fund cold-chain upgrades, broadening capacity for both domestic and export markets and reinforcing Asia-Pacific's rising influence in the therapeutic vaccines market.