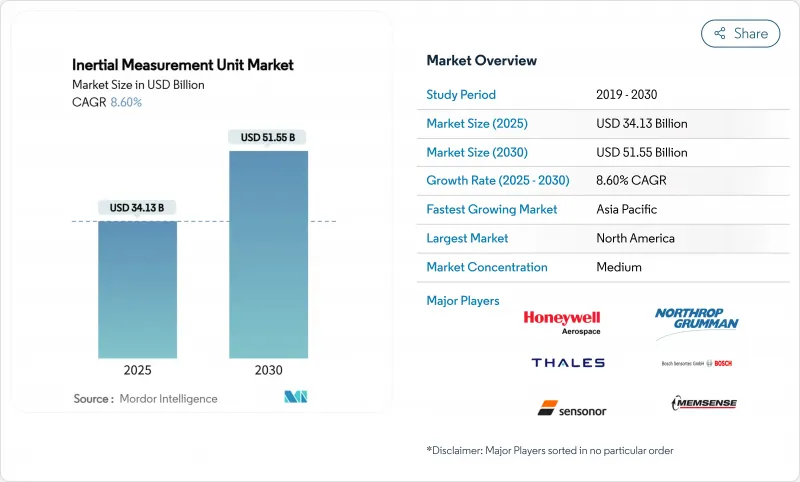

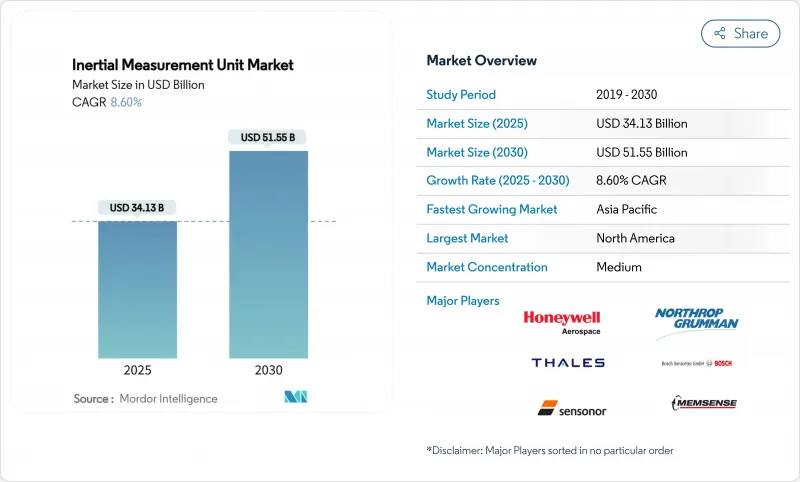

관성 측정 장치 시장 규모는 2025년에 341억 3,000만 달러로 평가되었고, CAGR은 8.60%를 나타낼것으로 예측되며, 2030년에 515억 5,000만 달러에 달할 전망입니다.

수요 증가는 하이브리드 양자-MEMS 센서 융합 기술에서 비롯되며, 이는 방위산업, 항공우주 및 자율 플랫폼 분야의 정밀 항법 방식을 재편하고 있습니다. 보잉은 2024년 양자 IMU 비행 시험에서 GPS에 의존하지 않는 항법 오차를 수십 킬로미터에서 수십 미터로 줄임으로써 이러한 변화를 입증했습니다. 고조되는 지정학적 위험, 무인 시스템의 확산, 양자 광학 기술의 성숙도는 관성 측정 장치 시장의 단기 성장 전망을 모두 강화하고 있습니다. 소비자 수요 역시 강력하다. 중국은 2025년 1분기 스마트 글래스 49만 4,000대를 출하하며 전년 동기 대비 116.1% 증가했고, 이는 정확도와 배터리 수명을 균형 있게 제공하는 저비용 6축 센서에 대한 기록적인 수요를 시사합니다. 해상, 광업, LNG 운영사들은 서브도(sub-degree) 동적 위치 정밀도 허용 오차를 충족하기 위해 전술 등급 MEMS IMU를 추가하며 관성 측정 장치 시장의 잠재적 고객 기반을 확대하고 있습니다.

현재 중동 여러 전역에서 저비용 드론이 기존 방공 체계보다 수적으로 우세하다. 노르딕 에어 디펜스의 크뢰거 100 요격기는 단순화된 IMU 전용 비행 컴퓨터를 탑재해 시속 270km에 달하며, 군집 대응 시 단위 비용을 절감합니다. 미 해병대는 민첩한 IMU와 소프트웨어 정의 방출기를 결합해 드론 전자 장비를 무력화하는 에피루스 마이크로웨이브 시스템을 선정했습니다. 이러한 움직임은 고가의 레이더나 광학 유도 방식 대신 관성 코어를 중심으로 한 모듈식 소프트웨어 중심 무기로의 조달 전환을 시사합니다. 확장 가능한 IMU 모듈과 개방형 API를 제공하는 공급업체들은 군이 대량 배치형 대(對)무인기 교리로 전환함에 따라 수혜를 볼 전망입니다.

유럽 LNG 운송사들은 더 긴 항구 대기열과 거친 대서양 파도에 직면하고 있습니다. 부르봉 선박은 이제 광섬유 자이로스코프 기반의 엑사일 옥탄스 AHRS를 탑재해 크레인 작업 중 롤, 피치, 헤브 안정성을 유지합니다. MEMS 설계는 개조 작업에서 링 레이저 자이로스코프를 대체하고 있는데, 이는 1도 미만 정확도를 유지하면서도 구매 가격을 절반으로 낮추기 때문입니다. 어드밴스드 네비게이션의 하이드러스 AUV는 해저 조사 비용을 75% 절감하고 팀 기반 잠수 임무의 필요성을 제거했습니다. 이러한 비용 절감 효과는 함대 전체 센서 업등급를 촉진하여 상업 선박 전반에 걸쳐 관성 측정 장치 시장을 확대하고 있습니다.

인증 위험으로 항공기 제조사들은 보수적인 태도를 유지합니다. 보잉은 양자 IMU를 4시간 동안 비행 시험했으나, 양산 적용 전 다년간의 자격 인증을 완료해야 합니다. 화성 탐사선에 탑재된 허니웰의 초소형 IMU는 항공우주 구매자들이 수십 년간 입증된 신뢰성을 가진 검증된 설계를 선호함을 보여줍니다. 긴 검증 기간은 기존 공급업체를 고착시키고 단가 하락을 늦춰 상업 항공 분야의 관성 측정 장치 시장 성장률을 둔화시킵니다.

자이로스코프는 2024년 관성 측정 장치 시장 매출의 40%를 차지했으며, 현재 위치 추정 정확도의 기초를 이루고 있습니다. 절대값은 더 작지만, 증강 현실 개발자들이 모든 헤드셋에 디지털 나침반을 내장함에 따라 자력계는 10.9%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 가속도계는 진동 및 ADAS(첨단 운전자 보조 시스템) 역할에서 꾸준한 물량을 유지하고 있습니다. 관성 측정 장치 시장은 이제 단일 패키지 센서 융합으로 기울고 있습니다. STMicroelectronics의 LSM6DSV16X는 제스처를 인식하는 머신러닝 코어를 추가하면서 대기 전력을 낮춰 배터리 수명을 연장합니다. 온칩 분석 기능을 제공하는 부품 공급업체들은 상품화 압박에도 불구하고 프리미엄 가격을 책정할 수 있습니다.

신규 패키지는 보안 엔클레이브 마이크로컨트롤러 내부에 자이로, 가속도계, 자력계 데이터를 결합합니다. 통합 타이밍은 센서 간 지연 시간을 제거하고 스푸핑 신호에 대한 시스템 내성을 강화합니다. 설계 팀이 이러한 모듈을 채택함에 따라, 부품 목록(BOM) 단순화가 원자재 비용을 제치고 주요 선택 요인으로 부상합니다. 이러한 전환은 출하량 증가에도 불구하고 관성 측정 장치 시장의 안정적인 가격 형성을 뒷받침합니다.

상용 등급 장치는 스마트폰 및 자동차 ADAS 시장의 규모 덕분에 2024년 관성 측정 장치 시장 규모의 35%를 차지했습니다. 우주 등급 출하량은 규모는 작지만 저궤도(LEO) 위성군 확산에 힘입어 연평균 12.4% 성장할 전망입니다. 노스롭 그루먼의 LR-450은 링 레이저 방식 대비 크기와 무게, 전력을 절반으로 줄이면서 궤도상 7천만 시간 이상 무고장 운용 기록을 보유한 밀리-HRG 자이로스코프를 사용합니다. 이러한 신뢰성은 동일한 위성 수백 대를 발사해야 하는 위성군 운영사들의 관심을 끌고 있습니다.

상업용 MEMS 정밀도가 향상되면서 등급 경계가 모호해지고 있습니다. 자동차 부품 공급업체들은 이제 전술 등급 수준의 편차 안정성을 요구하는 반면, 드론 제조사들은 방사선 내성을 위해 우주용 부품을 조달합니다. 소비자용에서 방위산업용으로 생산량을 전환할 수 있는 유연한 생산 라인을 확보한 업체들은 시장 침체기에도 회복탄력성을 유지하며 관성 측정 장치 시장 내 점유율을 강화하고 있습니다.

2024년 북미는 관성 측정 장치 시장 매출의 38%를 차지했습니다. 미국 국방 예산은 해군 연구소(Naval Research Laboratory)의 양자 간섭계 연구를 지원하여 드리프트 없이 항법 실행 시간을 연장하고 있습니다. 보잉의 양자 IMU 비행은 상업 항공 사용 사례를 검증했으며, 현지 OEM 업체들이 유럽 경쟁사보다 앞서 나가도록 합니다. 2024년 수출 통제 개혁으로 호주, 캐나다, 영국으로의 이전이 용이해져 북미 공급업체들이 동맹국 항공우주 프로그램에 특혜 접근권을 확보했습니다.

아시아태평양 지역은 2030년까지 가장 강력한 11.8% CAGR을 기록할 전망입니다. 중국 스마트 글라스 제조사들은 국내 보조금에 힘입어 분기마다 수천만 개의 6축 MEMS 센서를 주문하고 있습니다. 호주의 원격 광산은 광학 IMU 트럭의 실전 테스트베드 역할을 하며, 지역 대학들이 항법 스타트업 창업을 촉진하고 있습니다. 인도, 일본, 한국의 신생 우주 발사 기업들은 ITAR(국제무기거래규정) 적용 대상이 아닌 우주 등급 부품을 찾으며, 비용 민감 임무에서 미국 기존 업체들에 도전하는 자국 공급망을 육성 중입니다.

유럽은 해양, 에너지, 고정밀 위성 탑재체 분야에서 전략적 틈새 시장을 유지하고 있습니다. ESA 제네시스 위성은 센티미터 단위 해수면 모니터링을 위해 냉원자 IMU를 활용할 예정입니다. 엑사일(Exail)은 광섬유 자이로 동적 위치 제어 시스템 업등급 계약을 부르봉 선박과 체결하며, 거친 해상 환경용 센서 패키징 분야의 지역적 전문성을 입증했습니다. 허니웰이 2024년 시비타나비(Civitanavi)를 2억 유로에 인수함으로써 유럽 내 생산 기반을 확고히 구축, 대서양 횡단 무역 마찰 속에서도 항공기 프로그램의 연속성을 보장하게 되었습니다.

The inertial measurement unit market size stood at USD 34.13 billion in 2025 and is forecast to reach USD 51.55 billion by 2030, reflecting an 8.60% CAGR.

Demand gains stem from hybrid quantum-MEMS sensor fusion, which is reshaping precision navigation for defines, aerospace, and autonomous platforms. Boeing validated this shift when its 2024 flight test of a quantum IMU cut unaided-GPS navigation error from tens of kilometres to tens of meters. Escalating geopolitical risk, the spread of unmanned systems, and the maturity of quantum photonics all reinforce the near-term growth outlook for the inertial measurement unit market. Consumer pull is equally strong. China shipped 494,000 smart-glass units in Q1 2025, up 116.1% year over year, signalling record demand for low-cost six-axis sensors that balance accuracy and battery life. Maritime, mining, and LNG operators are adding tactical-grade MEMS IMUs to meet sub-degree dynamic-positioning tolerances, widening the addressable base for the inertial measurement unit market.

Low-cost drones now outnumber legacy air defenses across several Middle East theatres. Nordic Air Defence's Kreuger 100 interceptor relies on a simplified IMU-only flight computer, reaches 270 km/h, and cuts unit costs for swarm engagements. The U.S. Marine Corps selected Epirus microwave systems that couple agile IMUs with software-defined emitters to disable drone electronics. These moves signal a procurement pivot toward modular, software-centric weapons built around inertial cores rather than expensive radar or optical guidance. Suppliers that offer scalable IMU modules and open APIs stand to gain as militaries transition to volume-deployment counter-UAS doctrine.

European LNG shippers face tighter port queues and harsher Atlantic swells. Bourbon vessels now carry Exail Octans AHRS, based on fiber-optic gyros, to maintain roll, pitch, and heave integrity during crane operations. MEMS designs are also displacing ring-laser gyros on retrofit jobs because they slash purchase price by half while meeting sub-degree accuracy. Advanced Navigation's Hydrus AUV lowered subsea survey costs 75% and removed the need for team-based diving missions. Such savings encourage fleet-wide sensor upgrades, expanding the inertial measurement unit market across commercial shipping.

Certification risk makes air-framers conservative. Boeing flight-tested quantum IMUs for four hours but must still complete multi-year qualification before line-fit adoption. Honeywell's miniature IMU that flew on Mars probes underscores how aerospace buyers favour proven designs that demonstrate multi-decade reliability. Lengthy validation locks in incumbent vendors and slows unit-price erosion, tempering the inertial measurement unit market growth rate in commercial aviation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Gyroscopes contributed 40% of inertial measurement unit market revenue in 2024 and remain foundational for dead-reckoning accuracy. Magnetometers, though smaller in absolute value, compound at 10.9% CAGR as augmented-reality developers embed digital compasses inside every headset. Accelerometers maintain consistent volume in vibration and ADAS roles. The inertial measurement unit market now leans toward single-package sensor fusion. STMicroelectronics' LSM6DSV16X adds a machine-learning core that recognizes gestures while lowering standby power to extend battery life. Component vendors that offer on-chip analytics can charge premiums despite commoditization pressure.

Emerging packages combine gyro, accelerometer, and magnetometer data inside secure enclave micro-controllers. Integrated timing eliminates inter-sensor latency and hardens systems against spoof signals. As design teams adopt these modules, bill-of-materials simplicity overtakes raw component cost as the main selection factor. That transition supports steady pricing in the inertial measurement unit market despite rising shipment volumes.

Commercial-grade devices captured 35% of inertial measurement unit market size in 2024 thanks to smartphone and auto-ADAS scale. Space-grade shipments, though smaller, are projected to climb 12.4% CAGR on the back of proliferated low-Earth-orbit (LEO) constellations. Northrop Grumman's LR-450 uses milli-HRG gyros that log more than 70 million fault-free hours in orbit while halving size, weight, and power over ring-laser counterparts. That reliability attracts constellation operators who must launch hundreds of identical satellites.

Grade boundaries blur as commercial MEMS precision improves. Automotive suppliers now request tactical-grade bias stability, while drone makers procure space-qualified parts for radiation robustness. Vendors that master flexible production lines able to pivot from consumer to defense volumes gain resilience during sector downturns, reinforcing their share within the inertial measurement unit market.

Inertial Measurement Unit Market Report is Segmented by Component (Gyroscopes, Accelerometers, and More), Grade (Marine, Navigation and More), Technology (MEMS, FOG, and More), End User (Aerospace & Defense, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 38% of inertial measurement unit market revenue in 2024. U.S. defense budgets fund quantum interferometer research at the Naval Research Laboratory, extending navigation run-time without drift. Boeing's quantum-IMU flight validated commercial-aviation use cases and keeps local OEMs ahead of European rivals. Export-control reforms in 2024 eased transfers to Australia, Canada, and the United Kingdom, giving North American vendors privileged access to allied aerospace programs.

Asia-Pacific posts the strongest 11.8% CAGR through 2030. Chinese smart-glass makers, buoyed by domestic subsidies, order tens of millions of six-axis MEMS sensors each quarter. Australia's remote mines serve as live testbeds for photonic IMU trucks, encouraging regional universities to spin out navigation start-ups. New-space launch firms across India, Japan, and South Korea seek ITAR-free space-grade parts, fostering indigenous supply chains that challenge U.S. incumbents in cost-sensitive missions.

Europe retains strategic niches in marine, energy, and high-precision satellite payloads. The ESA GENESIS satellite will use cold-atom IMUs to underpin centimeter-level sea-level monitoring. Exail won Bourbon vessel contracts for fiber-optic gyro dynamic-positioning upgrades, reflecting regional expertise in harsh-sea sensor packaging. Honeywell's EUR 200 million purchase of Civitanavi in 2024 gives the firm a deep European production base, ensuring continuity for aircraft programs even amid trans-Atlantic trade frictions.