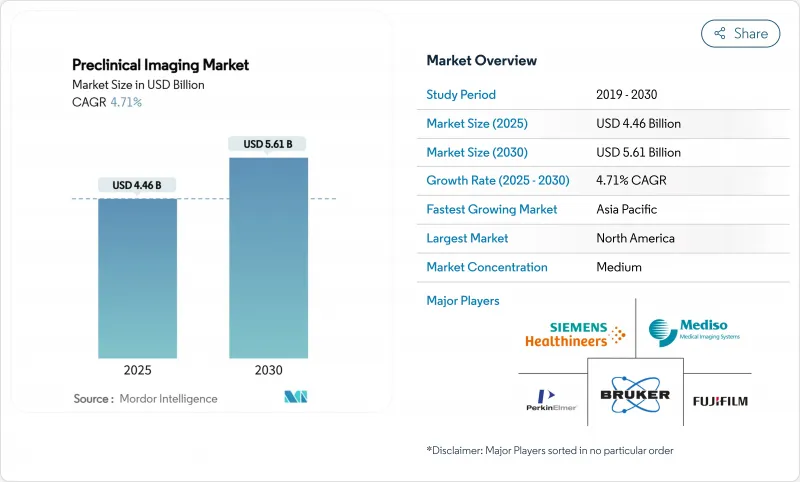

전임상 이미징 시장 규모는 2025년에 44억 6,000만 달러, 예측 기간 중(2025-2030년) CAGR은 4.71%를 나타내고, 2030년에는 56억 1,000만 달러에 달할 것으로 예측됩니다.

이 기세는 AI를 탑재한 멀티모달 시스템의 채택 증가, 지속적인 의약품 연구개발비, 이미지 인프라에 대한 꾸준한 공공 투자에 지지되고 있습니다. 광학 모달리티는 저비용과 실시간 시각화의 이점에서 계속 우위를 유지하고 있지만, 연구자들이 한 세션에서 더 풍부한 데이터 세트를 찾고 있기 때문에 하이브리드 플랫폼이 지지를 받고 있습니다. CRO(의약품 개발 업무 수탁기관)는 많은 의약품 개발 기업이 사내에 가지지 않는 최첨단 기기나 규제상의 노하우를 턴키로 이용할 수 있기 때문에 주목도가 높아지고 있습니다. 북미는 여전히 수요의 중심지이지만, 아시아의 급속한 인프라 정비가 그 차이를 줄이고 전임상 이미징 시장의 세계 공급망을 재구축하고 있습니다.

인공지능을 활용한 자동화상 취득과 크로스모달리티 해석에 의해 처리시간이 70%나 단축되어 과학자는 데이터 처리보다 해석에 전념할 수 있게 되었습니다. 이 기술은 동일한 동물 내에서 해부학, 기능 및 분자 판독을 동기화 할 수 있게하고 코호트 크기를 줄이면서 통계적 감지력을 향상시킵니다. 형광 현미경 검사와 3T-7T MRI의 조합은 심장과 신경 조직의 이온 이동에 대한 통찰력을 높이고 전임상 이미징 시장이 비침습적이고 종단적인 질병 진행 관찰을 향하고 있음을 보여줍니다. AI 파이프라인을 통합한 상용 플랫폼은 경험이 없는 실험실로의 도입도 간소화하고, 사용자층을 넓혀 전임상 이미징 시장에 새로운 수요를 주입하고 있습니다.

미국에서는 2024년까지 16개의 세포 및 유전자 치료제가 승인되었고, 그 파급 효과는 탐색과 독물학의 워크플로우에 침투했습니다. 스탠포드의 세포 및 유전자 치료 센터와 같은 아카데믹 허브는 리포터 유전자 이미징에 의해 이식 세포를 수개월간 추적하여 규제 당국이 요구하는 안전성과 지속성 데이터를 제공하는 방법을 보여줍니다. 이러한 요구는 고감도로 전신을 추적할 수 있는 멀티모달 스캐너의 지속적인 수주로 이어져 전임상 이미징 시장의 장기적인 성장을 뒷받침하고 있습니다.

하이브리드 스캐너는 MRI, PET, 광학 및 데이터 사이언스의 교차 교육이 필요하며 한 개인에게는 거의 얻을 수 없는 기술입니다. 유능한 직원이 월급이 높은 기지로 이동하면 연구소의 다운타임이 발생하고 생산 능력의 확대가 제한됩니다. 벤더는 클라우드 기반의 원격 조작 대시보드로 대응해 전문가의 지원을 시설 전체에 넓히고 있지만, 인재 부족은 계속되고 있어 아시아, 라틴아메리카, 아프리카의 일부에서는 신규 도입의 페이스가 억제되고 있습니다.

2024년 전임상 이미징 시장의 35.32%는 광학 시스템이 차지하고, 저렴한 가격, 직관적인 조작성, 루틴의 종양학이나 감염증 연구에 적합한 실시간 판독이 이점이 되고 있습니다. 이 부문의 설치 기반은 여전히 높은 처리량 스크리닝에 필수적이지만 CAGR은 신흥 대체 제품에 뒤처져 있습니다. PET/SPECT/CT나 PET/MR로 대표되는 하이브리드 시스템은 여러 번 마취를 하지 않고 멀티 파라메트릭한 지견을 얻으려는 연구자에 의해 2030년까지 연률 9.82%의 성장이 예측됩니다. MILABS VECTor와 같은 고급 장비는 최대 4μm의 기능 및 해부학 이미징을 통합하여 실험 설계의 자유도를 확대합니다. Revvity의 IVIS SpectrumCT 2는 광학 데이터에 CT 감쇠 보정을 추가하여 정량화 정확도를 높이고 하이브리드 플랫폼의 전임상 이미징 시장 규모를 끌어 올려 수렴 경향을 보여줍니다.

컴포넌트 비용 감소와 워크플로우 자동화는 하이브리드 채택을 더욱 가속화합니다. 아시아와 유럽의 연구 컨소시엄에서는 공유 장비를 조달할 때 멀티모달 기능을 요구하는 경향이 강해지고, 단일 모달리티 의존으로부터의 전략적 전환이 강조되고 있습니다. 이러한 선호도는 서비스 계약 및 소프트웨어 업그레이드에 대한 지속적인 수요로 이어져 전임상 이미징 시장 전반공급업체의 수익 스트림을 심화시키고 있습니다.

2024년 전임상 이미징 시장은 북미가 48.18%를 차지했습니다. SBIR과 같은 연방 보조금과 지속적인 벤처 캐피탈의 유입은 산학 협력의 치밀한 네트워크에 자금을 공급하고 있습니다. MD 앤더슨 암센터 등의 센터에서는 7T MRI와 트라이모달리티 PET/SPECT/CT 시스템을 도입하고 있으며, 이 지역의 기술적 우위성 유지에 대한 헌신을 뒷받침하고 있습니다. 광음향 토모그래피와 MRI를 통합한 워크플로우 등의 획기적인 기술이 미국의 연구소에서 태어나 종양의 특징을 보다 명확하게 하는 혈관과 대사의 동시 이미징을 가능하게 하고 있습니다.

아시아는 2030년까지 연평균 복합 성장률(CAGR)이 9.53%로 가장 빠르게 성장하는 지역입니다. 중국과 일본이 세련된 시설에 대한 투자 선진을 끊는 한편, 각국의 자금조달 방식이 조달 승인을 합리화하고 있습니다. 홍콩이공대학의 7T MRI와 고급 광음향 초음파의 설치는 이 지역의 급속한 능력 향상을 반영합니다. 시장 진출기업도 국내 CRO를 육성하고, 화상 처리 컴포넌트의 높은 수입 관세를 상쇄하는 보조금을 제공함으로써 전임상 화상 처리 시장에의 지역 진입을 확대하고 있습니다.

유럽은 관민 연계가 잘 작동하고 견조한 점유율을 유지하고 있습니다. 엄격한 동물 복지 규제는 동물의 수를 줄이는 비 침습적 접근법에 대한 수요를 가속화하고 윤리적, 과학적 우선 순위를 일치시킵니다. Discovery Park Ventures가 Vox Imaging Technology에 출자한 투자 차량은 MRI의 소형화에 새로운 자본을 투입하여 자국발의 혁신 파이프라인을 확보하고 있습니다. 벤더는 전임상과 임상에 걸친 소프트웨어 플랫폼의 조화를 중시하고 있습니다. 유나이티드 이미징의 트랜스레이셔널 아키텍처는 설치류에서 인간 시험까지 원활하게 데이터를 흘릴 수 있어 임상적으로 예측 가능한 이미지 워크플로우를 중시하는 유럽의 자세를 강화하고 있습니다.

The Preclinical Imaging Market size is estimated at USD 4.46 billion in 2025, and is expected to reach USD 5.61 billion by 2030, at a CAGR of 4.71% during the forecast period (2025-2030).

Momentum is anchored in rising adoption of AI-powered multimodal systems, sustained pharmaceutical R&D spending, and steady public investment in imaging infrastructure. Optical modalities continue to dominate because of their lower cost and real-time visualization advantages, yet hybrid platforms are gaining traction as researchers seek richer datasets in a single session. Contract research organizations (CROs) command growing attention, offering turnkey access to cutting-edge equipment and regulatory know-how that many drug developers lack in-house. North America remains the epicenter of demand, but Asia's rapid infrastructure build-out is closing the gap and reshaping global supply chains in the preclinical imaging market.

Automated image acquisition and cross-modality analysis powered by artificial intelligence now cut processing times by as much as 70%, freeing scientists to focus on interpretation rather than data wrangling. The technology enables synchronized anatomical, functional, and molecular readouts within the same animal, boosting statistical power while reducing cohort sizes. Fluorescence microscopy paired with 3T-7T MRI furthers insight into ionic shifts in cardiac and neurologic tissue, demonstrating the preclinical imaging market's push toward non-invasive, longitudinal observation of disease progression. Commercial platforms embedding AI pipelines also simplify onboarding for less-experienced laboratories, widening the user base and injecting fresh demand into the preclinical imaging market.

Sixteen U.S. approvals for cell and gene therapies through 2024 created ripple effects that permeate discovery and toxicology workflows. Academic hubs such as Stanford's Center for Cell and Gene Therapy illustrate how reporter gene imaging allows transplanted cells to be followed for months, providing safety and persistence data that regulators require. These needs translate to sustained orders for multimodal scanners capable of sensitive, whole-body tracking, reinforcing long-term growth in the preclinical imaging market.

Hybrid scanners demand cross-training in MRI, PET, optics, and data science, skills rarely found in a single individual. Laboratory downtime arises when qualified staff migrate to higher-paying hubs, constraining capacity expansion. Vendors respond with cloud-based remote operation dashboards that stretch expert support across facilities, yet talent shortages persist, tempering the pace of new installations in parts of Asia, Latin America, and Africa.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Optical systems retained 35.32% of the preclinical imaging market in 2024, benefiting from affordability, intuitive operation, and real-time readouts that suit routine oncology and infectious-disease studies. The segment's installed base remains pivotal for high-throughput screening, yet its CAGR lags emerging alternatives. Hybrid systems, notably PET/SPECT/CT and PET/MR, are forecast to grow 9.82% annually through 2030 as investigators seek multi-parametric insights without multiple anesthetic events. Advanced devices such as the MILABS VECTor integrate functional and anatomical imaging down to 4 µm, expanding experimental design latitude. Revvity's IVIS SpectrumCT 2 exemplifies the convergence trend by adding CT attenuation correction to optical data, thereby enhancing quantification accuracy and boosting the preclinical imaging market size for hybrid platforms.

Falling component costs and improved workflow automation further accelerate hybrid adoption. Research consortia in Asia and Europe increasingly mandate multimodal capabilities when procuring shared equipment, highlighting the strategic shift from single-modality reliance. These preferences feed recurring demand for service contracts and software upgrades, deepening vendor revenue streams across the preclinical imaging market.

The Preclinical Imaging Market Report is Segmented by Modality (Optical Imaging Systems, Nuclear Imaging Systems, Micro-MRI, Micro-CT, and More), Application (Oncology, Neurology, Cardiovascular Disorders, and More), End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 48.18% of the preclinical imaging market in 2024. Federal grants like SBIR and sustained venture capital inflows finance a dense network of academic-industry collaborations. Centers such as MD Anderson Cancer Center house 7 T MRI and tri-modality PET/SPECT/CT systems, underlining the region's commitment to maintaining technological edge. Breakthroughs such as integrated photoacoustic tomography-MRI workflows have emerged from U.S. labs, enabling concurrent vascular and metabolic imaging that refines tumor characterization.

Asia is the fastest-growing region with a 9.53% CAGR through 2030. China and Japan spearhead investment in sophisticated facilities, while national funding schemes streamline procurement approvals. Hong Kong Polytechnic University's installation of 7 T MRI and advanced photoacoustic ultrasound reflects the region's rapid capability build-up. Governments also nurture domestic CROs, offering subsidies that offset high import tariffs on imaging components, expanding regional participation in the preclinical imaging market.

Europe maintains robust share through well-coordinated public-private partnerships. Stringent animal welfare regulations accelerate demand for non-invasive modalities that reduce animal numbers, aligning ethical and scientific priorities. Investment vehicles like Discovery Park Ventures' stake in Vox Imaging Technology channel fresh capital into MRI miniaturization, ensuring a pipeline of home-grown innovation. Vendors emphasize harmonized software platforms across preclinical and clinical lines: United Imaging's translational architecture lets data flow seamlessly from rodent to human studies, reinforcing Europe's focus on clinically predictive imaging workflows.