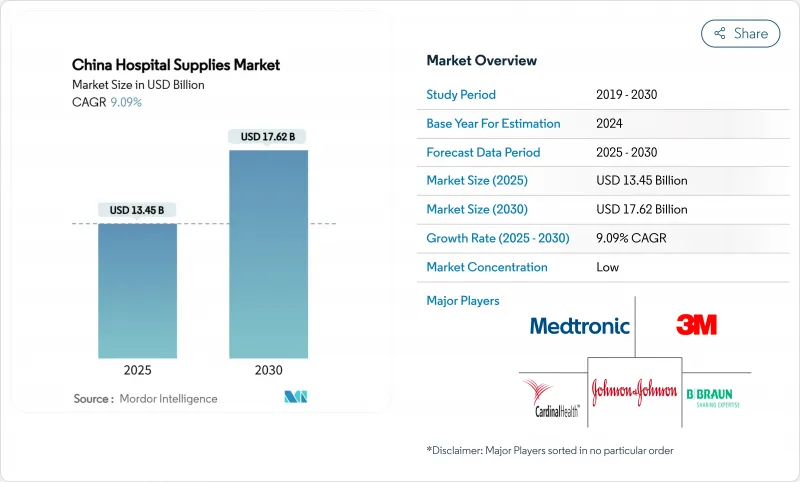

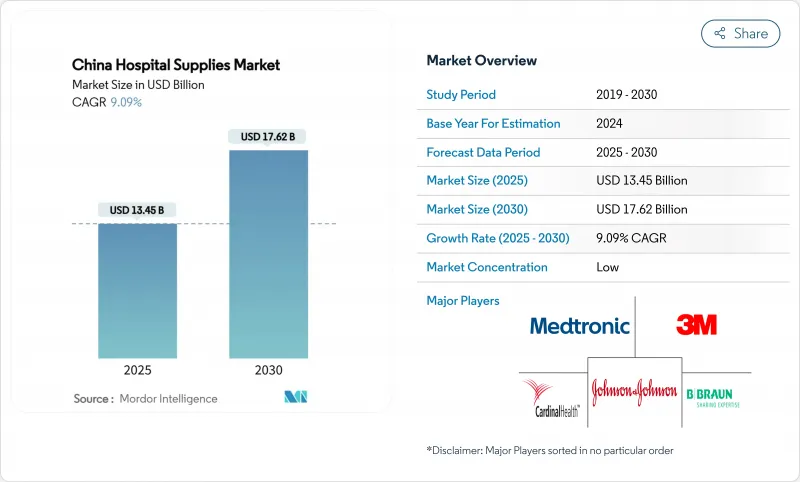

중국 병원 용품 시장 규모는 2025년에 134억 5,000만 달러, 예측기간(2025-2030년)의 CAGR은 9.09%를 나타내고, 2030년에는 176억 2,000만 달러에 달할 것으로 예측됩니다.

병원 인프라 확대, 감염제어 프로토콜 강화, 국내 업체를 선도하는 현지화 정책이 총체적으로 수요 패턴을 형성하고 있습니다. 일회용 제품은 감염 위험을 최소화하고 워크플로우를 간소화하기 위해 조달 목록의 상위 수준을 차지하고 있습니다. 중앙 집중식 구매 메커니즘은 수량의 예측 가능성을 높였지만 동시에 가격 경쟁을 격화시키고 공급업체에게 비용 효율성과 품질 보증의 균형을 유지하도록 촉구하고 있습니다. 이러한 요인은 규제 준수를 희생하지 않고 입찰가 한도를 충족시킬 수 있는 현지 기업에 경쟁 우위를 재분배하기 위해 수렴하고 있습니다.

중국에서는 2024년에 39,000개의 병원과 1,037만개의 병상이 보고되었으며, 이는 이 나라의 역사상 가장 광범위한 용량 확장을 보여줍니다. 제2, 제3의 도시에 있어서의 시설의 신설 및 개축에는 기본적인 소모품으로부터 고도의 진단 시스템까지, 종합적인 임상 재고가 필요합니다. 지역 의료 센터 프로그램과 관련된 정부 보조금은 병원 관리자에게 국가 입찰 목록에 따라 표준화된 고품질 장비를 얻도록 요청합니다. 병상 수 증가는 또한 주입 세트, 상처 드레싱, 카테터와 같은 환자 관리 용품의 안정적인 조달을 자극합니다. 신속한 납품과 경쟁 가격을 보장할 수 있는 현지 제조업체는 건설 프로젝트가 완료됨에 따라 증가하는 주문을 얻는 데 유리한 위치에 있습니다.

노인들은 이미 만성 질환 환자의 66.3%를 차지하고 있으며, 33.7%는 다질환 합병증을 경험했으며 급성기 병동에 지속적인 압력을 가하고 있습니다. 순환기과, 종양과, 투석과의 수술 건수가 증가하고, 수술용 드레이프로부터 이식형 기구에 이르기까지 소모품의 강하 수요가 발생하고 있습니다. 병원은 또한 입원 중 만성 합병증을 관리하기 위해 모니터링 장비를 더 많이 재고해야합니다. 평균 자기부담액 1,199.24달러의 입원비에 따른 경제적 스트레스를 통해 구매 매니저는 수입품보다 비용 효율적인 국산품을 선호하게 되었습니다.

의료기기관리법의 초안에서는 시판후 조사가 확대되어 컴플라이언스 위반에 대한 벌칙이 강화되고 있습니다. 국내 이노베이터는 신속한 승인 획득의 혜택을 받지만, 다국적 기업은 보다 긴 심사 사이클과 추가 문서 요건에 직면해 상업적 스케줄을 지연시킵니다. 따라서 병원은 새로운 수입 의료기기의 채택을 연기하고 기존 SKU에 대한 의존을 유지하고 있습니다. 새로운 법적 틀은 또한 업데이트 신청을 지원하기 위해 실제 임상 증거에 대한 투자를 늘릴 것을 제조업체에게 의무화하고 컴플라이언스 비용을 높이고 있습니다. 이러한 제약이 있음에도 불구하고, 지역에 뿌리를 둔 임상 평가를 완료한 기업은 결국 지방의 가치 기반 구매 이니셔티브에서 우대를 확보할 수 있을지도 모릅니다.

일회용 병원 용품은 2024년 중국 병원 용품 시장 점유율의 38.45%를 차지했으며, 안정적인 수량 성장을 이어가고 있습니다. 일회용 주사기, 장갑 및 수술용 드레이프의 중국 병원 용품 시장 규모는 노인 및 만성 질환 집단의 치료 건수가 증가함에 따라 확대될 것으로 예측됩니다. 고급 카테터 카테고리에서는 여전히 수입 브랜드가 우위를 차지하고 있지만, 지방의 입찰 상한을 충족하는 가격대에서 상품화된 일회용 기구를 공급하는 현지 기업이 늘고 있습니다. RFID 태그가 있는 수술용 팩과 같은 기술적 업그레이드는 새로운 규제 당국의 보고 의무에 맞게 보다 정확한 추적성을 지원합니다.

멸균 및 소독 기기는 원내 감염 목표와 중앙 무균 서비스 부문의 업그레이드에 견인되어 2025-2030년의 CAGR은 가장 빠른 9.54%를 기록할 전망입니다. 도시의 병원에서는 노후화된 에틸렌 옥사이드 시스템을 사이클 타임을 단축하고 노동 안전성을 향상시키는 저온 과산화수소 플라즈마 유닛으로 대체하고 있습니다. 자동 세척 소독기의 중국 병원 용품 시장 규모는 삼차 병원이 ISO 13485의 완벽한 준수를 향해 움직이기 시작하면서 확대되고 있습니다. 국내 제조업체는 IoT 대시보드를 포함한 경쟁력 있는 가격으로 현지 서비스를 제공하는 멸균기로 가치 체인을 향상시켜 다국적 공급업체가 누려온 역사적인 프리미엄을 침식하고 있습니다.

The China Hospital Supplies Market size is estimated at USD 13.45 billion in 2025, and is expected to reach USD 17.62 billion by 2030, at a CAGR of 9.09% during the forecast period (2025-2030).

Expansion of hospital infrastructure, intensified infection-control protocols, and localization policies that prioritize domestic manufacturers are collectively shaping demand patterns. Disposable supplies continue to dominate procurement lists because single-use items minimize infection risk and streamline workflows, while sterilization solutions draw heightened interest as hospitals tackle hospital-acquired infection rates. Centralized purchasing mechanisms have increased volume predictability but have also intensified price competition, prompting suppliers to balance cost efficiencies with quality assurances. These factors are converging to redistribute competitive advantage toward local firms that can meet tender price caps without sacrificing regulatory compliance.

China reported 39,000 hospitals and 10.37 million hospital beds in 2024, indicating the broadest capacity expansion in the country's history. New and renovated facilities in tier-2 and tier-3 cities require comprehensive clinical inventories ranging from basic disposables to advanced diagnostic systems. Government grants tied to regional medical-center programs compel hospital administrators to acquire standardized, high-quality supplies that align with national tender lists. Bed growth also stimulates stable procurement for patient-care items such as infusion sets, wound dressings, and catheters. Local manufacturers that can guarantee rapid fulfillment and competitive pricing are well positioned to capture incremental orders as construction projects reach completion.

Older adults already account for 66.3% of chronic-disease cases, and 33.7% experience multimorbidity, placing sustained pressure on acute-care wards. Procedure volumes for cardiology, oncology, and dialysis services are rising, creating downstream demand for consumables ranging from surgical drapes to implantable devices. Hospitals must also stock higher quantities of monitoring equipment to manage chronic comorbidities during inpatient stays. The financial stress associated with average out-of-pocket hospitalization costs of USD 1,199.24 has led purchasing managers to favor cost-efficient, domestically produced items over imported equivalents.

The draft Medical Device Administration Law expands post-market surveillance and increases penalties for non-compliance. While domestic innovators benefit from fast-track pathways, multinational firms face longer review cycles and additional documental requirements, delaying commercial timelines. Hospitals therefore postpone the adoption of new imported devices, sustaining reliance on existing SKUs. The new legal framework also obliges manufacturers to increase investment in real-world evidence to support renewal applications, boosting compliance costs. Despite the constraints, companies that complete localized clinical evaluations may eventually secure preferential slots in provincial value-based purchasing initiatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Disposable hospital supplies claimed 38.45% of China hospital supplies market share in 2024 and continue to experience steady volume growth because single-use items reduce cross-contamination risk and simplify waste-management protocols. The China hospital supplies market size for disposable syringes, gloves, and surgical drapes is projected to expand in tandem with rising procedure counts among elderly and chronic-disease cohorts. Imported brands still dominate premium catheter categories, but local firms increasingly supply commoditized disposables at price points that meet provincial tender caps. Technological upgrades such as RFID-tagged surgical packs support more precise traceability, aligning with new regulatory reporting obligations.

Sterilization & disinfection equipment is poised to register the fastest 9.54% CAGR over 2025-2030, driven by hospital-acquired infection targets and upgrades to central sterile services departments. Urban hospitals are replacing aging ethylene-oxide systems with low-temperature hydrogen-peroxide plasma units that reduce cycle times and improve occupational safety. The China hospital supplies market size for automated washer-disinfectors is expanding as tertiary hospitals move toward full ISO 13485 compliance. Domestic manufacturers have moved up the value chain with competitively priced, locally serviced sterilizers that incorporate IoT dashboards, thereby eroding the historic premium enjoyed by multinational suppliers.

The China Hospital Supplies Market Report is Segmented by Product Type (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, Sterilisation and Disinfectant Equipment, Disposable Hospital Supplies, and Other Product Types), End User (Public Hospitals, Private Hospital, Specialty and Rehabilitation Centers). The Market Forecasts are Provided in Terms of Value (USD).