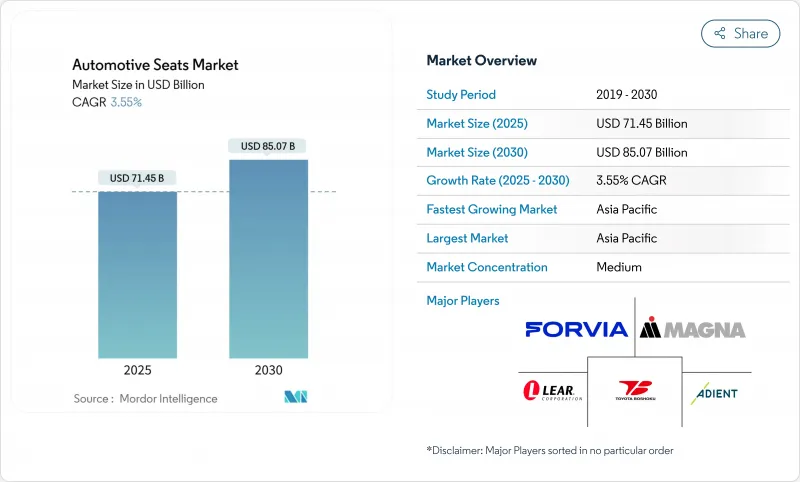

자동차 시트 시장 규모는 2025년에 714억 5,000만 달러, 2030년에는 850억 7,000만 달러에 이르고, CAGR은 3.55%를 나타낼 전망입니다.

전동화, 자율주행 기능, 프리미엄 컴포트 지향의 높아짐이 시트 프레임, 쿠션, 일렉트로닉스의 재설계를 뒷받침하고 있기 때문에 성장은 플러스를 유지하고 있습니다. 자동차 제조업체는 배터리의 무게를 보완하기 위해 더 가벼운 구조를 계속 지정하고 소비자는 평균 판매 가격을 인상하는 파워드 환기 마사지 기능을 선호합니다. 원재료의 변동과 엄격한 안전 규칙으로 인해 밸류체인 전체에 비용 압력이 가해지지만 Tier 1 공급업체는 자동차 프로그램에 깊이 통합되어 가격 결정력을 유지하고 있습니다. 아시아태평양은 중국, 인도, 일본 공장이 내연식과 전기식 플랫폼의 생산 능력을 확대하여 양적 수요와 기술 채택을 선도하고 있습니다.

2024년에는 세계 자동차 판매 대수의 54%를 SUV가 차지하게 되어 자동차 1대당 시트 함량이 증가하고 강화 사이드 볼스터, 다열 구성, 프리미엄 트림에 대한 수요가 높아집니다. 가처분 소득과 도시화가 SUV의 보급을 촉진하고, 아시아태평양의 제조업체가 혜택을 받습니다. 2023년 SUV 판매 대수의 20%는 완전한 전기자동차이며 배터리의 질량을 상쇄하는 경량 프레임과 통합된 열 관리에 대한 새로운 주문을 유발합니다. 국제에너지기관(IEA)의 보고에 따르면 대부분의 SUV는 여전히 화석연료로 움직이고 있으며, 액티브 냉각, 난방, 중량 최적화 쉘을 통합한 전동화 시트의 기술 혁신에는 큰 가능성이 남아 있습니다.

한때는 고급 브랜드에 한정되어 있던 프리미엄 기능이, 중간 부문의 모델에도 탑재되게 되어 왔습니다. 리어 코퍼레이션의 컴포트 맥스 플랫폼은 난방 및 환기 응답 시간을 40% 단축하고 조립 복잡성을 반감시켜 OEM의 대규모 배치를 가능하게 합니다. 환기 시트는 CAGR 6.12%에서 가장 빠르게 성장하는 기술 분야입니다. 마사지 시스템에는 탑승자의 스트레스를 줄이는 생체 피드백이 통합되어 시트가 웰니스 허브로 변모하고 소프트웨어 지원 업그레이드로 지속적인 수익을 기대할 수 있습니다.

철강 가격은 2020년부터 2021년에 걸쳐 2배 이상으로 상승했고, 차량 1대당 원재료 가격은 2,200달러에서 4,125달러로 상승하여 시트 공급업체의 마진을 압박했습니다. 시트 쿠션의 90% 이상을 차지하는 폴리우레탄 폼은 원유 가격의 변동을 따르기 때문에 제조업체는 프로그램 중반에서 가격 전가가 어려운 비용 상승에 노출됩니다. 공급업체는 쿠션의 모양을 재설계하여 폼의 부피를 줄이고 재활용 폴리머 블렌드를 인증함으로써 대응합니다.

합성 피혁은 2024년에 자동차 시트 시장 점유율의 48.75%를 차지했고, CAGR 5.44%로 성장했습니다. 오리지널 장비 프로그램은 안정적인 시보, 방오성, 간소화된 청소를 평가하여 함대 서비스의 보증 클레임을 줄입니다. 패브릭은 여전히 엔트리 모델로 정착하고 있는 반면, 가죽은 톱 엔드에서 존속하지만, 지속가능성에 대한 우려와 조달의 불안정성에 직면하고 있습니다. 아마나 마와 같은 천연섬유는 OEM이 순환형 소재를 추구하는 가운데 시트백이나 쿠션 보강재에 채택되고 있지만, 가격 프리미엄이 여전히 대량 전개의 제한이 되고 있습니다.

도요타의 SofTex 트림은 가죽보다 생산시 CO2 배출량을 85% 줄여 차량 평균 배출량 목표 달성에 기여하고 있습니다. 콘티넨탈과 마그나는 혼합 재료의 접착제를 제거하여 재활용을 용이하게하는 바이오 발포 패드를 프로토타입하고 있습니다. 이러한 신흥경제 국가들은 유럽의 순환경제지령에 대응하기 때문에 자동차 사용 후 쉽게 분해할 수 있도록 설계된 단일 소재의 쿠션으로의 시프트를 시사하고 있습니다.

수동식 어저스터는 신흥 시장과 베이스 트림의 비용 감응도를 반영하여 2024년 세계 점유율의 58.25%를 여전히 차지하고 있습니다. 그러나 벤틸레이티드 변형은 CAGR 6.12%를 기록했으며, 더운 지역이나 추운 지역에서 구매자가 얼마나 따뜻한 편안함을 강조하는지 보여줍니다. 북미에서는 히티드 옵션이 여전히 정평이지만, 파워 어저스터는 이코노미 라인과 럭셔리 라인의 가교가 되어 복잡한 HVAC를 통합하지 않고 메모리 프로파일과 램버 모듈을 제공합니다.

자세와 활력 징후를 추적하는 스마트 시트는 프리미엄 EV에서 빠르게 발전하고 있습니다. 현대 Transys는 기아 EV9에 저에너지 탄소섬유 히터, 동적 바디 케어 알고리즘, 틸트 어웨이 워크 인 기능을 패키징하고 완전히 소프트웨어로 정의된 편안한 양산의 길을 입증했습니다. 공급업체는 또한 OTA(Over-the-Air) 지원 제어 장치를 통합하여 향후 판매 시점을 넘어 수익을 늘릴 수 있는 기능의 잠금을 해제할 수 있습니다.

아시아태평양은 중국의 전기자동차 붐, 인도의 급성장하는 컴팩트 SUV 부문, 일본의 시트 일렉트로닉스에의 지속적인 투자에 의해 견인되어 매출 46.85%, CAGR 3.75%로 성장할 것으로 예상됩니다. 중국의 신차 판매에 있어서의 전기자동차의 보급률은 2025년에 45%를 보일 것으로 예측되고 있어, 시트 제조업체는 경량 프레임이나 일체형 냉각 설계의 개발에 여념이 없습니다. 전동 삼륜차나 배달용 밴에 보조금을 내는 인도의 정책은 고부하 사이클에 적합한 내구성이 높고 유지보수가 적은 트림에 대한 수요를 가속시킵니다. 도요타 방직과 같은 일본의 혁신적인 기업은 스윙 의자 모션과 개인화된 오디오를 갖춘 휴식 시트를 발표했으며, 이 지역이 전반적인 승객의 편안함을 추구하고 있음을 보여줍니다.

유럽에서는 배출가스 감축과 재활용 가능성이 중요합니다. 재료의 추적성과 수명주기 탄소 회계를 강화하는 규정이 도입되었으며, 바이오 발포재를 사용한 시트와 쉽게 분리 가능한 커버가 권장됩니다. 포르비아의 트럭용 시트 플랫폼은 기존 설계보다 CO2 배출량을 40% 줄이고 컴플라이언스와 드라이버의 편안함을 양립할 수 있음을 입증합니다. 픽업과 SUV 점유율이 높은 북미에서는 미드 트림 모델에서 인공 호흡과 시트 히터의 표준화가 진행되고 있습니다. 공급업체는 디트로이트 및 멕시코 제조 기지와 가까이 있는 것을 활용하여 금속 프레스 및 쿠션 생산을 현지화하고, 물류 위험을 줄이고, 미국-MCA의 지역 컨텐츠 규칙을 준수합니다.

중동, 아프리카, 남미는 장기적인 확장 가능성을 가지고 있습니다. 각국 정부는 자동차 생태계를 발전시키기 위해 현지 조립을 지원하고 있으며, 견고한 도로 요건을 충족하는 간소화되고 비용 효율적인 벤치 시트 및 점프 시트 기회를 창출하고 있습니다. 라이드 헤일링 및 미니버스 분야에서 플릿이 구입함으로써 서비스 인프라가 제한된 환경에서도 가동 시간을 유지할 수 있는 청소가 용이한 합성 피혁과 퀵 스왑 시트 모듈 수요가 확대됩니다.

The automotive seat market size is valued at USD 71.45 billion in 2025 and is expected to reach USD 85.07 billion by 2030, reflecting a steady 3.55% CAGR.

Growth stays positive as electrification, autonomous driving features, and a rising preference for premium comfort push redesigns of seat frames, cushions, and electronics. Automakers continue to specify lighter structures to compensate for battery weight, while consumers favor powered, ventilated, and massage functions that lift average selling prices. Raw-material volatility and stringent safety rules place cost pressure across the value chain, yet Tier-1 suppliers maintain pricing leverage because of their deep integration with vehicle programs. Asia Pacific leads volume demand and technology adoption as Chinese, Indian, and Japanese plants expand capacity for both internal-combustion and electric platforms.

SUVs reached 54% of global car sales in 2024, increasing seat content per vehicle and lifting demand for reinforced side bolsters, multi-row configurations, and premium trim. Asia Pacific manufacturers benefit as disposable income and urbanization lift SUV penetration. Electric SUVs draw further momentum; 20% of 2023 SUV sales were fully electric, triggering new orders for lightweight frames and integrated thermal management that offset battery mass. The International Energy Agency reports that most SUVs still run on fossil fuel, leaving substantial potential for electrified seat innovation that integrates active cooling, heating, and weight-optimized shells .

Premium features once limited to luxury brands increasingly appear in mid-segment models. Lear Corporation's ComfortMax platform cuts heating and ventilation response times by 40% and halves assembly complexity, enabling OEM rollouts at scale . Ventilated seats represent the fastest-growing technology slice at 6.12% CAGR because thermal comfort helps EVs preserve driving range. Massage systems now incorporate biometric feedback to reduce occupant stress, transforming seats into wellness hubs and opening recurring revenue through software-enabled upgrades.

Steel prices more than doubled between 2020 and 2021, and raw-material content per vehicle rose from USD 2,200 to USD 4,125, compressing margins for seat suppliers. Polyurethane foam, covering more than 90% of seat cushions, tracks oil price swings, exposing manufacturers to cost spikes that are difficult to pass through mid-program. Suppliers respond by redesigning cushion geometries to reduce foam volume and by qualifying recycled polymer blends.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Synthetic leather held 48.75% of the automotive seat market share in 2024 and is projected to grow at a 5.44% CAGR, underscoring its dual appeal of affordability and premium look. Original-equipment programs value their consistent grain, stain resistance, and simplified cleaning, which lowers warranty claims in fleet service. Fabric remains entrenched in entry models, whereas genuine leather persists at the top end but faces sustainability concerns and sourcing volatility. Natural fibers such as flax and hemp enter seat backs and cushion reinforcements as OEMs pursue circular materials, but price premiums still limit volume deployment.

Toyota's SofTex trim produces 85% lower CO2 during manufacture than genuine leather, helping the company align with fleet-average emissions goals. Continental and Magna prototype bio-foam pads that ease recycling by eliminating mixed material adhesives. Such developments signal a shift toward mono-material cushions designed for straightforward disassembly at vehicle end-of-life to meet European circular-economy directives.

Manual adjusters still anchor 58.25% of global share in 2024, reflecting cost sensitivity in emerging markets and base trims. Ventilated variants, however, post a 6.12% CAGR, showing how buyers reward thermal comfort in both hot and cold climates. Heated options remain a staple in North America, while power adjusters form a bridge between economy and luxury lines, offering memory profiles and lumbar modules without complex HVAC integration.

Smart seats that track posture and vital signs are advancing quickly in premium EVs. Hyundai Transys packages low-energy carbon-fiber heaters, dynamic body-care algorithms, and tilt-away walk-in functions within the Kia EV9, proving a mass-production path for fully software-defined comfort. Suppliers are also embedding over-the-air-enabled control units, allowing future features unlock that spread revenue beyond the point of sale.

The Automotive Seat Market Report is Segmented by Material Type (Synthetic Leather, Fabric, and More), Technology (Standard (Manual) Seats, Powered Seats, and More), Sales Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Seat Type (Bench/Split-Bench Seats, Bucket Seats, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific leads with 46.85% revenue and a 3.75% CAGR outlook, fueled by China's electric-vehicle boom, India's fast-growing compact-SUV segment, and Japan's sustained investment in seat electronics. China is forecast to reach 45% EV penetration in new-car sales in 2025, keeping seat suppliers busy with lighter frames and integrated cooling designs. Indian policies that subsidize electric three-wheelers and delivery vans accelerate demand for durable, low-maintenance trim suited to high-usage duty cycles. Japanese innovators such as Toyota Boshoku unveil relaxation seats with swing-chair motion and personalized audio, demonstrating the region's push toward holistic passenger comfort.

Europe focuses on emissions reduction and recyclability. Regulations tighten material traceability and lifecycle carbon accounting, encouraging seats built from bio-based foams and easily separable covers. FORVIA's truck seat platform claims 40% lower CO2 than conventional designs, proving compliance can coexist with driver comfort. North America, characterized by high pickup and SUV share, shows rising standardization of ventilated and heated seats in mid-trim models. Suppliers leverage proximity to Detroit and Mexico fabrication hubs to localize metal stamping and cushion production, reducing logistics risk and meeting US-MCA regional-content rules.

The Middle East, Africa, and South America provide long-run expansion potential. Governments support local assembly to develop automotive ecosystems, creating opportunities for simplified, cost-efficient bench and jump seats that meet rugged-road requirements. Fleet purchases in ride-hailing and mini-bus sectors open demand for easy-clean synthetic leather and quick-swap seat modules that preserve uptime in environments with limited-service infrastructure.