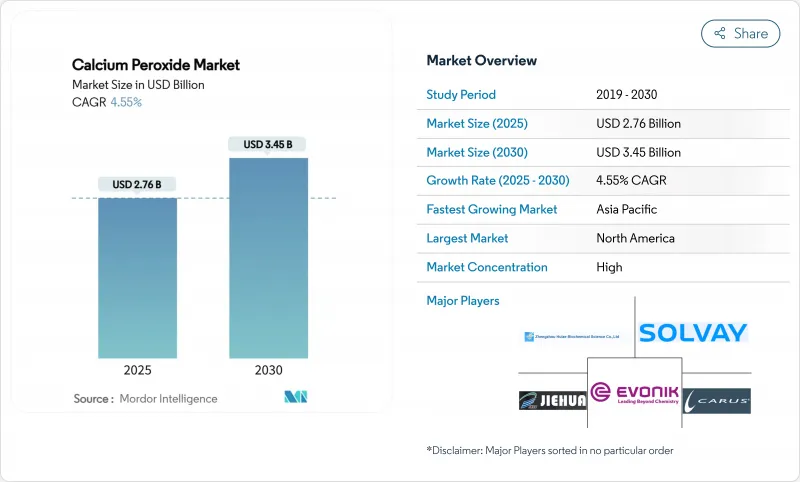

과산화칼슘 시장 규모는 2025년에 27억 6,000만 달러, 2030년에는 34억 5,000만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 4.55%를 나타낼 전망입니다.

현재의 기세는 유해한 부산물을 남기지 않고 수산화칼슘과 산소로 분해하는 산화제에 대한 지속적인 수요에 기인합니다. 성장 요인으로는 직물 컨디셔닝의 대규모 채택, 환경 복구 프로젝트 확대, 정밀 농업 종자 펠릿화에 광범위한 사용 등이 있습니다. 경쟁의 중심은 엄격한 규제 기준을 충족하면서 처리 사이클을 단축하고, 수질을 개선하고, 발아율을 높이는 용도에 특화된 배합입니다. 생산자는 또한 수직 통합과 지역 생산 능력 향상으로 원료 가격 변동에 대비합니다. 위험은 취급 위험, 불안정한 석회 및 탄산 칼슘 비용, 저렴한 과산화물로 인한 대체 압력에 관한 것입니다.

종래의 프루핑 대신에 노타임 도우 공정이 채택됨에 따라, 산업용 베이커리에서의 과산화칼슘 수요가 증가하고 있습니다. 20-35ppm의 최적 첨가율은 글루텐 강도, 수분 유지력, 냉동 반죽의 안정성을 향상시켜 대규모 베이커리 공장 간의 품질 표준화에 도움이 되고 있습니다. 유럽에서는 아조디카본아미드의 규제가 금지되어 있지만, 분해 생성물이 건강 위험을 최소화하기 때문에 이 화합물은 추가로 지지됩니다. 북미와 유럽의 생산 규모 확대는 다국적 식품 그룹에 안정적인 공급을 보장합니다. 소매 채널에서 냉동식품과 퍼베이크드 식품의 소비 확대는 과산화칼슘 시장의 장기적인 수량 성장을 지원하고 있습니다. 인라인 산화제 주입을 통합하는 장비 업그레이드도 채택을 간소화합니다.

나노입자 등급은 치아 미백용 젤과 구강 세정제로 지지를 모으고 있습니다. 이것은 산소의 방출이 에나멜질을 밝게 하면서 바이오필름을 억제하기 때문입니다. 임상 연구는 과산화수소보다 상아세관으로의 침투가 좋고, 지각 과민성을 감소시키는 것으로 나타났습니다. 주요 구강 케어 브랜드는 과산화칼슘을 "친화적인 산소"성분으로 자리 매김하고 깨끗한 라벨의 동향에 맞추고 있습니다. 아시아태평양의 급속한 도시화로 프리미엄 화이트닝 제품에 대한 소비자층이 확대되어 가까운 미래 수요가 더해집니다. 미국, 유럽연합(EU), 일본의 규제 당국의 승인은 OTC와 프로용 양 라인의 상품화를 원활하게 합니다.

과산화칼슘은 강한 산화제로 분류되며 유기물과의 접촉은 화재를 심화시키고 분진은 눈, 피부, 호흡기를 자극합니다. 창고에는 가연물로부터의 격리, 온도 관리, 국소 배기 장치가 필요합니다. 이러한 조치는 특히 신흥 시장의 소규모 가공업자에게 컴플라이언스 비용을 증가시킵니다. 확립된 직업 노출 한계가 없기 때문에 규제 불확실성이 증가하고 공장 승인이 지연될 수 있습니다. 훈련과 개인보호구(PPE)의 요구 사항은 또한 총 소유 비용을 증가시키고 과산화 칼슘 시장의 비용 중심 부문의 급속한 보급을 억제합니다.

식품 등급은 2024년 과산화칼슘 시장 점유율의 56.66%를 차지했으며 엄격한 식품 안전 규범 하에서 일관된 산화제 성능을 필요로 하는 세계 베이커리 그룹의 정착된 수요를 반영합니다. 프리미엄 공급업체는 FCC 및 ASTM 벤치마크에 적합하며 고속 믹서에서 균질한 분산을 허용하는 좁은 입자 크기 스팬을 유지하는 제품을 제공합니다. 산업용 등급은 토양 정화, 수산 양식, 정밀 농업의 규모 확대에 따라 2030년까지의 CAGR이 5.12%가 될 것으로 예측됩니다. 오랄 케어 및 의약품 용도의 특수 나노입자는 이득이 크고 화학 메이저의 연구개발 투자를 끌고 있습니다.

북미와 유럽의 규제 감사는 공급자의 선택 기준을 강화하고 유효한 위험 분석 계획을 가진 오랜 생산자를 선호합니다. 한편, 산업용 등급의 제조업자는 산소 수율, 수불용성, 유동성을 중시하고 정화 계약자의 투여장치 요건을 충족하도록 하고 있습니다. 아시아태평양의 직파 쌀과 연못 처리의 채택은 산업 학년의 지속적인 톤수 증가를 지원합니다. 한편으로는 엄격한 인증, 다른 한편으로는 성능의 커스터마이즈가 상호 작용하는 것으로, 전체적인 밸런스가 유지되고, 과산화칼슘 시장의 장기적인 저견도를 지지하고 있습니다.

북미는 엄격한 정화법, 기술적으로 진행된 베이커리 부문, 과산화칼슘 기반 산소 공여체를 선호하는 정밀 파종 도구의 조기 전개로 2024년 매출 점유율 38.34%로 선두에 올랐습니다. 미국 환경보호청(Environmental Protection Agency)의 브라운필드 보조금은 사이트 운영 위험을 줄이는 고형 산화제에 대한 수요를 지속적으로 자극하고 있습니다. 캐나다는 브리티시 컬럼비아 주에서 자원 부문의 토양 정화와 양식 시험에서 이어지며, 멕시코는 미국 공급망에 의존하는 식품 가공 수출로 이익을 얻고 있습니다. 하류의 과산화칼슘 생산에 공급하는 Engro사의 투자와 같은 과산화수소 플랜트의 능력 증강은 원료의 안전성을 높입니다.

아시아태평양의 2030년까지의 CAGR은 6.33%를 나타내고, 대규모 양식 사업과 직접 파종 쌀의 채택이 이를 뒷받침합니다. 일본의 장어 양식장과 베트남의 새우 양식 연못은 연못의 산소화 용도의 넓이를 나타내고 있으며, 매월 정기 수요를 견인하고 있습니다. 중국의 오염지 회복 의무, 인도의 기계화 이식기, 한국의 구강 관리 혁신 생태계는 모두 응용 분야의 다양성을 확대하고 있습니다. 중국과 말레이시아 지역 제조업체는 물류 비용 절감과 납품 사이클 단축으로 인해 석회암 광상 부근에 새로운 공장을 건설하여 이 지역의 과산화칼슘 시장 경쟁력을 강화합니다.

유럽에서는 베이커리 라인에서 아조디카본아미드가 단계적으로 철수되어 독일, 프랑스, 영국의 베이커리가 과산화칼슘의 대체품으로 이행하고 있습니다. 폴란드와 이탈리아의 오래된 산업 지역에서는 토양 정화가 더욱 진행되고 있습니다. 북유럽의 고가치 양식 부문은 침전물의 산화 체계를 시험적으로 도입하여 이용 사례를 늘리고 있습니다. 남미와 중동, 아프리카에서는 브라질의 세라드 간척과 이집트의 티라피아 연못이 아시아태평양으로부터의 기술 이전을 이용하고 있으며, 새로운 가능성을 가져오고 있습니다. 인프라의 격차와 규제의 변동은 성장 경사를 완만하게 하고 있지만, 여전히 세계의 과산화칼슘 시장에 톤수를 증가시키고 있습니다.

The Calcium Peroxide Market size is estimated at USD 2.76 billion in 2025, and is expected to reach USD 3.45 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Current momentum comes from sustained demand for an oxidizing agent that decomposes into calcium hydroxide and oxygen, leaving no hazardous by-products. Growth levers include large-scale adoption in dough conditioning, expanding environmental remediation projects, and wider use in seed pelleting for precision agriculture. Competitive activity centers on application-specific formulations that shorten processing cycles, improve water quality, or raise germination rates while meeting strict regulatory standards. Producers also hedge against feedstock price swings by vertical integration and regional capacity additions. Risks relate to handling hazards, volatile lime and calcium carbonate costs, and substitution pressure from lower-priced peroxides.

Demand for calcium peroxide in industrial bakeries rises as no-time dough processes replace traditional proofing. Optimum addition rates of 20-35 ppm improve gluten strength, moisture retention, and frozen dough stability, helping large bakers standardize quality across plants. Regulatory bans on azodicarbonamide in Europe further favour the compound because its breakdown products pose minimal health risks. Production scale-up in North America and Europe secures a consistent supply for multinational food groups. Greater consumption of frozen and par-baked items in retail channels sustains long-term volume growth for the calcium peroxide market. Equipment upgrades that integrate inline oxidant dosing also streamline adoption.

Nanoparticle grades are gaining traction in tooth whitening gels and mouthwashes because slow oxygen release inhibits biofilms while brightening enamel. Clinical studies show better penetration into dentinal tubules than hydrogen peroxide, reducing sensitivity. Major oral-care brands position calcium peroxide as a "gentle oxygen" ingredient, aligning with clean-label trends. Rapid urbanisation in the Asia Pacific widens the consumer base for premium whitening products, adding near-term demand. Regulatory approvals across the United States, European Union, and Japan smooth commercialisation for both OTC and professional lines.

Calcium peroxide is classified as a strong oxidizer; contact with organics can intensify fires, and the dust irritates eyes, skin, and respiratory tracts. Warehouses require isolation from combustible materials, temperature control, and local exhaust ventilation systems. These measures raise compliance costs, especially for small processors in emerging markets. Absence of an established occupational exposure limit adds regulatory uncertainty and may delay plant approvals. Training and personal protective equipment requirements also elevate the total cost of ownership, restraining rapid diffusion in cost-conscious segments of the calcium peroxide market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Food Grade accounted for 56.66% of the calcium peroxide market share in 2024, reflecting entrenched demand from global bakery groups that require consistent oxidant performance under strict food safety codes. Premium suppliers deliver products that conform to FCC and ASTM benchmarks and maintain a narrow particle-size span, enabling homogeneous dispersion in high-speed mixers. Industrial Grade is forecast to post a 5.12% CAGR to 2030 as soil remediation, aquaculture, and precision agriculture gain scale. Specialty nanoparticle variants aimed at oral-care and pharmaceutical uses command higher margins, attracting R&D investments from chemical majors.

Regulatory audits in North America and Europe reinforce supplier selection criteria, favouring long-standing producers with validated hazard-analysis plans. Meanwhile, Industrial Grade formulators emphasise oxygen yield, water insolubles, and flowability to meet remediation contractors' dosing equipment requirements. Adoption of direct-seeded rice and pond treatment in Asia Pacific underpins sustained tonnage growth for Industrial Grade. The interplay of stringent certification on one side and performance customisation on the other maintains overall balance and undergirds long-term resilience of the calcium peroxide market.

The Calcium Peroxide Market Report is Segmented by Grade (Food Grade, Industrial Grade), Application (Dough Conditioner, Seed Disinfectant, Bleaching Agent, Oxidizing Agent, and More), End-User Industry (Food and Beverage, Agriculture, Mining, Pulp and Paper, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America led with a 38.34% revenue share in 2024 thanks to stringent remediation legislation, a technologically advanced bakery sector, and early deployment of precision seeding tools that favour calcium peroxide-based oxygen donors. The United States Environmental Protection Agency's brownfield grants continue to stimulate demand for solid-form oxidants that lower site operation hazards. Canada follows with resource-sector soil clean-up and aquaculture trials in British Columbia, while Mexico benefits from food-processing exports that hinge on US supply chains. Capacity additions in hydrogen peroxide plants, such as Engro's investment that feeds downstream calcium peroxide production, enhance raw material security.

Asia Pacific posts the fastest regional CAGR at 6.33% to 2030, propelled by large-scale aquaculture operations and direct-seeded rice adoption. Japanese eel farms and Vietnamese shrimp ponds illustrate the breadth of pond-oxygenation uses, driving recurring monthly demand. China's contaminated-land restoration mandates, India's mechanised rice planters, and South Korea's oral-care innovation ecosystem all expand application diversity. Regional manufacturers in China and Malaysia commission new plants close to limestone deposits to trim logistics costs and shorten delivery cycles, reinforcing competitiveness of the calcium peroxide market in the region.

Europe's trajectory is shaped by the phased withdrawal of azodicarbonamide from bakery lines, pushing bakeries in Germany, France, and the United Kingdom toward calcium peroxide alternatives. Soil remediation in old industrial belts of Poland and Italy presents additional volume. Northern Europe's high-value aquaculture sector pilots sediment oxidation regimes, adding another use case. South America and the Middle East & Africa provide emerging potential, with Brazil's Cerrado reclamation and Egypt's tilapia ponds drawing on technology transfer from Asia Pacific. Infrastructure gaps and regulatory variability temper the growth slope yet still feed incremental tonnage into the global calcium peroxide market.