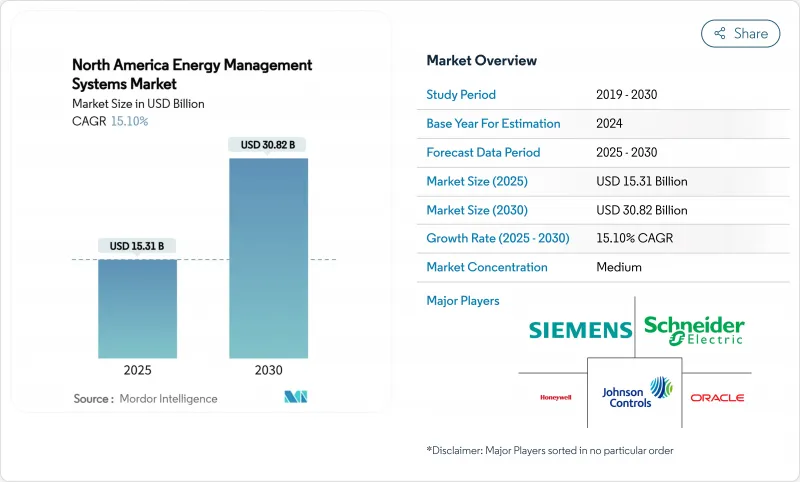

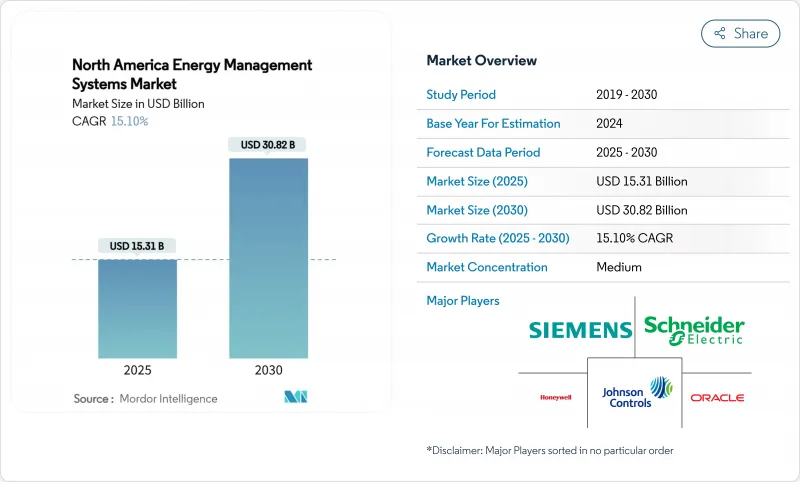

북미의 에너지 관리 시스템 시장 규모는 2025년에 153억 1,000만 달러, 2030년에는 308억 2,000만 달러에 이르고, CAGR은 15.10%를 나타낼 전망입니다.

불과 5년 만에 시장 규모가 두 배로 증가함에 따라 이 지역은 배출량을 줄이고 전력 사용을 최적화하는 지능형 소프트웨어 정의 인프라로 빠르게 이동하고 있다는 것을 뒷받침합니다. 연방 정부의 인센티브, 기업의 넷제로 의무화, AI를 활용한 최적화 도구의 급속한 진보가 이 상승의 주요 요인이 되고 있습니다. 미국의 이점, 클라우드 피벗 및 무선 연결은 모두 투자 회수 기간을 단축하여 채택을 가속화하고 있습니다. 동시에 중견기업과 공공기관은 리스크를 서비스 제공업체에게 전가하는 성능 기반 계약을 통해 새로운 비용 절감을 실현하고 있습니다. 데이터센터 부하 증가, 건축 기준법 강화, 유틸리티 요금의 역동적인 변동으로 북미 에너지 관리 시스템 시장의 대상이 더욱 확대되고 있습니다.

3,700억 달러의 인플레이션 감소법에 근거한 까다로운 세액 공제 및 리베이트는 리노베이션 투자 회수 기간을 단축하고 네트워크 제어 및 분석 플랫폼의 즉각적인 조달에 박차를 가합니다. 상업용 빌딩은 업그레이드 1평방 피트당 최대 5달러를 공제할 수 있게 되었으며, 캘리포니아와 같은 주에서는 20-35%의 절약을 목표로 하는 전체 리베이트를 제공하기 위해 2억 9,100만 달러를 확보했습니다. 국내 생산 크레딧은 현지 EMS 하드웨어의 생산을 장려하고 공급망을 완화합니다. 이 증거에서 Johnson Controls는 연방 및 주 정부 인센티브를 이용한 성과 계약으로 84억 달러의 고객 절감을 달성했다고 보고했습니다.

유틸리티는 2023년 동안 고도 측정 인프라를 호스팅하는 배전 자산에 대한 509억 달러를 포함하여 3,200억 달러를 그리드 업그레이드에 투자했습니다. AMI 데이터는 최신 플랫폼에 내장된 AI 엔진에 미세한 부하 곡선을 제공하여 가상 발전소(VPP)에 참여할 수 있습니다. 미국 에너지부는 2030년까지 80-160GW의 VPP 용량을 예측했습니다. 에지 애널리틱스는 응답 시간을 최대 92% 단축하여 거주자의 편안함을 유지하면서 유연성을 수익화할 수 있습니다. 멕시코의 230억 달러 그리드 프로그램은 호환 가능한 솔루션에 대한 국경을 넘어서는 수요를 추가합니다.

중간 규모 사무용 턴키 시스템은 유지 보수 비용 이전에 50,000달러를 초과할 수 있으며 수명 주기 비용은 초기 투자의 5배에 이를 수 있습니다. 지역 인센티브가 제한된 경우 주택 구매자는 더 큰 어려움을 느낍니다. 서비스형 에너지 계약은 위험을 완화합니다. Cobb County의 710만 달러 계약은 20년 동안 200만 달러의 유틸리티 절감을 보장합니다. 그럼에도 불구하고 반도체 부족과 더 깨끗한 칩 제조를위한 자본 수요는 단기적으로 하드웨어 가격을 상승시킵니다.

빌딩 에너지 관리 시스템은 2024년 북미 에너지 관리 시스템 시장에서 62%의 압도적 점유율을 유지했습니다. 그러나 가정용 에너지 관리 시스템은 스마트 스피커의 보급, 전력 회사 리베이트, 상호 운용 표준의 성숙을 배경으로 급속히 확대되고 있습니다. 이 부문의 2030년까지 연평균 복합 성장률(CAGR)은 17.23%를 나타내고 북미 에너지 관리 시스템 시장에서 가장 파괴적인 시장이 되었습니다.

참고 자료에 따르면 HEMS 도입으로 머신러닝 알고리즘이 HVAC 및 가전제품의 일정을 조정하면 가정 소비량이 20% 이상 줄어듭니다.Matter 프로토콜의 도입은 기기 페어링 절차를 단순화하고, 대중적인 확산을 가속화합니다. 산업용 EMS는 중간 틈새 시장을 차지하며 중공업 고객에게 프로세스별 분석 및 컴플라이언스 대시 보드를 제공합니다. 이러한 역학은 북미의 에너지 관리 시스템 시장의 다양성과 탄력성을 유지하고 있습니다.

서비스는 2024년에 43%의 점유율을 획득했으며, 2030년까지의 CAGR은 17.02%를 나타내고, 일회성 하드웨어 계약에서 지속적인 최적화 계약으로의 결정적인 전환을 강조했습니다. 지속적인 수익 흐름은 모니터링, 분석, 성과 위험을 공급자에게 전가하는 절약 보증 계약 등을 다룹니다. 하드웨어는 필수적이지만 상품화가 진행되는 반면 클라우드 소프트웨어 계층은 예측 제어를 통해 가치를 창출합니다.

서비스 중심의 계약은 대출, 복고 커미셔닝 및 운영자 교육을 번들로 제공하여 서비스형 에너지 제공을 위한 통합 경로를 형성합니다. Limbach Holdings는 데이터 중심의 검토를 통해 사이트 당 수백 가지의 실용적인 통찰력을 발견했으며 분석 기술이 순수한 장비 노하우를 능가한다는 것을 보여줍니다. 이러한 개발로 북미의 에너지 관리 시스템 시장은 자본 예산이 긴축되더라도 기세를 유지할 수 있습니다.

The North America energy management systems market size stood at USD 15.31 billion in 2025 and is projected to reach USD 30.82 billion by 2030, registering a firm 15.10% CAGR.

The doubling of value in just five years underlines the region's swift shift toward intelligent, software-defined infrastructure that cuts emissions and optimizes power use. Federal incentives, corporate net-zero mandates, and rapid advances in AI-enabled optimization tools are the primary forces behind this rise. US dominance, the cloud pivot, and wireless connectivity all accelerate adoption by shrinking payback periods. At the same time, mid-sized enterprises and public institutions unlock fresh savings through performance-based contracts that transfer risk to service providers. Rising data-center loads, strengthened building codes, and dynamic utility tariffs further widen the addressable pool for the North America energy management systems market.

Generous tax credits and rebates under the USD 370 billion Inflation Reduction Act cut retrofit payback periods and spur immediate procurement of networked controls and analytics platforms. Commercial buildings can now deduct up to USD 5.00 per square foot of qualifying upgrades, while states such as California have secured USD 291 million to deliver whole-home rebates that target 20-35% savings. Domestic production credits encourage local EMS hardware output and cushion supply chains. As evidence, Johnson Controls reports USD 8.4 billion in customer savings created by performance contracts that ride on federal and state incentive stacks.

Utilities invested USD 320 billion in grid upgrades during 2023, including USD 50.9 billion for distribution assets that host advanced metering infrastructure. AMI data feeds granular load curves into AI engines embedded in modern platforms and enables virtual power plant (VPP) participation. The US Department of Energy projects 80-160 GW of VPP capacity by 2030. Edge analytics shrinks response times by up to 92%, letting buildings monetize flexibility while preserving occupant comfort. Mexico's USD 23 billion grid program adds cross-border demand for compatible solutions.

Turnkey systems for mid-sized offices can surpass USD 50,000 before maintenance fees, and life-cycle costs often climb to five times the initial outlay. Residential buyers feel the pinch even more sharply when local incentives are limited. Energy-as-a-service contracts mitigate risk: Cobb County's USD 7.1 million deal guarantees USD 2 million utility savings over 20 years. Still, semiconductor shortages and the capital demands of cleaner chip fabrication inflate hardware prices in the near term.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Building Energy Management Systems retained a commanding 62% share of the North America energy management systems market in 2024, anchored by large commercial portfolios that prize operational transparency and tenant comfort. Yet Home Energy Management Systems are scaling swiftly on the back of smart-speaker ubiquity, utility rebates, and maturing interoperability standards. The segment's 17.23% CAGR through 2030 makes it the most disruptive pocket of the North America energy management systems market.

Annual data show HEMS installations reducing household consumption by more than 20% once machine-learning algorithms adjust HVAC and appliance schedules. Matter protocol adoption simplifies device pairing and propels mainstream appeal. Industrial EMS offerings occupy a middle niche, providing process-specific analytics and compliance dashboards for heavy manufacturing clients. Collectively, these dynamics keep the North America energy management systems market diversified and resilient.

Services captured 43% share in 2024 and delivered the highest 17.02% CAGR to 2030, underscoring a decisive tilt away from one-off hardware deals toward continuous optimization agreements. Recurring revenue streams cover monitoring, analytics, and guaranteed-savings contracts that shift performance risk to providers. Hardware is indispensable but increasingly commoditized, while cloud software layers create value through predictive controls.

Service-led engagements often bundle financing, retro-commissioning, and operator training, forming an integrated pathway to energy-as-a-service delivery. Limbach Holdings uses data-driven reviews to uncover hundreds of actionable insights per site, illustrating how analytics skills eclipse pure equipment know-how. These developments sustain the North America energy management systems market momentum even when capital budgets tighten.

The North America Energy Management Systems Market Report is Segmented by EMS Type (Building Energy Management Systems (BEMS), Home Energy Management Systems (HEMS), and More), Component (Hardware, Software, and Services), Deployment Mode (On-Premise, Cloud-Based, and More), End-User Sector (Commercial, Residential, and More), Communication Technology (Wired and Wireless), and Geography.