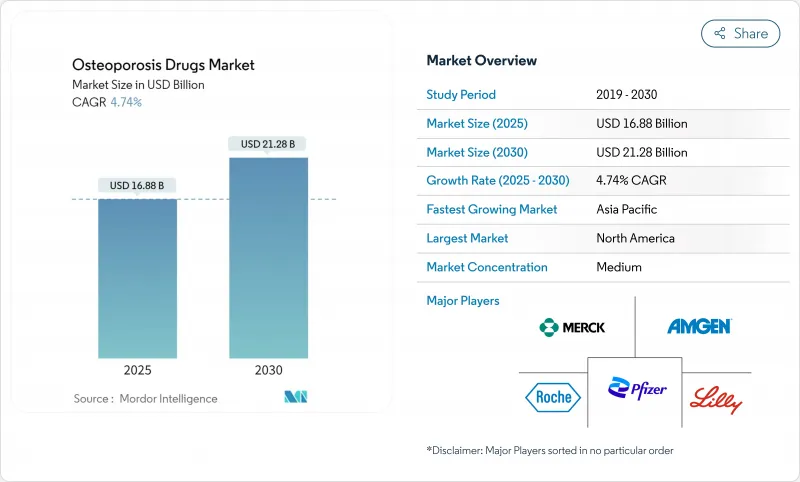

골다공증 치료제 시장은 2025년에 168억 8,000만 달러, CAGR 4.74%로 성장하여 2030년에는 212억 8,000만 달러에 이를 것으로 예측되고 있습니다.

이 궤적은 저가의 비스포스포네이트로부터 보다 신속한 골절 위험 감소를 약속하는 고가의 생물학적 제제 및 골형성 동화제로의 규율 있는 전환을 보여줍니다. 인구 고령화, 평균 수명 증가, 인공지능에 의한 기회 스크리닝을 지원하는 조기 진단은 치료 대상 환자를 계속 확대하고 있습니다. 치료와 전국 골절 등록을 연결하는 상환 제도 개혁은 치료까지의 시간을 단축하는 반면, 실제 임상에서의 증거 경로는 제품 승인 사이클을 단축하고 있습니다. 데노스맙의 특허 만료에 따른 바이오시밀러 의약품의 출시는 가격 경쟁에 박차를 가하는 동시에, 구입하기 쉬운 가격으로의 개선에 의해 골다공증 치료제 시장의 확대를 가져올 것으로 보입니다.

50세 이상이 주요 리스크 그룹으로, 연간 골다공증 치료제 골절은 2050년까지 630만 건에 달할 것으로 예상되며 아시아태평양이 대부분을 차지합니다. 고관절 골절 사망률은 12개월 이내에 20%에 달하며 뼈를 재건하고 2차 골절을 피하기 위해 신속하게 작용하는 치료 요건에 대한 수요에 박차를 가하고 있습니다. 일본에서는 골다공증 치료제의 진단률이 41%임에도 불구하고 지방 병원에서의 골밀도 검사율은 불과 14%에 그치고 있으며 진단 격차가 부각되고 있습니다. 메디케어는 2016년 180만 명의 수혜자의 골절 치료에 57억 달러를 지출했지만, 골절 후 환자의 80%는 여전히 치료되지 않았으며 접근 확대에 대한 비용 압력을 돋보이게 합니다. 이러한 인구통계학적 힘은 골다공증 치료제 시장의 각 약물 클래스에 대한 수년간 수요의 밑바닥을 강화하고 있습니다.

테리파라타이드(teriparatide)와 아발로파라타이드(abaloparatide)와 같은 동화 작용이 있는 약은 각각 65%, 86%의 척추 골절 감소를 달성하고, 항골 흡수제를 능가하며, 상당한 상환을 모으고 있습니다. FDA가 2024년에 아발로파라타이드(abaloparatide) 남성 환자에 대한 적용을 확대함으로써 미국 내 주소 지정 가능한 풀이 12% 증가했습니다. managedhealthcareexecutive.com. 골절 위험 감소 효과를 유지하는 것으로 나타났습니다. ucb.com. 일본의 실제 임상 증거는 고위험 코호트에서 심혈관계 모니터링과 함께 로모소주맙이 투여되는 것을 확인하고 라벨 경고에도 불구하고 임상적 신뢰를 의미합니다. springer.com. 보험 적용이 강화되고 가이드라인이 업데이트됨에 따라 골다공증 치료제 약물 시장을 확대하는 신진대사 제1선택 약물이 정당화됩니다.

2년 후 평균 복약률은 61.9%에 불과하며, 데노스맙의 갑작스런 중단은 골절 위험을 20% 증가시키는 뼈 흡수의 리바운드를 유발합니다. 데노스맙은 또한 사용 개시 후 30일 동안 저칼슘혈증과 피부과학적 안전성 신호가 집적되어 있습니다. 로모소주맙은 심근경색과 뇌졸중에 대한 박스 경고를 받았으며, 치료군의 0.8%가 심근경색을 경험한 반면 알렌드로네이트 제형에서는 0.3%였습니다. 비스포스포네이트 제형의 비복약률은월1회 또는 분기에 1회 투여하는 옵션이 있음에도 불구하고, 일본에서는 여전히 평균 23.3%입니다. 이러한 컴플라이언스 갭은 골다공증 치료제 시장, 특히 경구 시장의 성장을 깎고 있습니다.

2024년 골다공증 치료제 시장 점유율은 비스포스포네이트 제제가 37.40%를 유지하지만, 지불자와 의사가 보다 가치가 높은 선택지로 축족을 옮겼기 때문에 성장은 연율 1% 미만으로 둔화. 스클레로스틴 억제제(주로 로모소주맙)는 임상가가 심각한 위험 환자에게 신속한 골 형성 촉진을 선호했기 때문에 CAGR로 가장 빠른 5.23%를 보였습니다. 데노스맙을 중심으로 한 RANKL 억제제는 6개월 투여가 어드히어런스를 지원하기 때문에 생물학적 제제의 톱 셀러를 유지했습니다.

선택적 에스트로겐 수용체 조절제는 비스포스포네이트를 견딜 수 없는 여성을 위한 틈새 역할을 하고, 부갑상선 호르몬 유사체는 항골 흡수 유지 요법 이전의 교량 요법으로서의 역할을 했습니다. 파이프라인의 주목은 골 형성과 골 흡수 억제의 두 가지 프로파일을 기대할 수 있는 마이크로 RNA 조절제와 Wnt 신호 활성화제로 옮겨졌습니다. 칼시토닌의 사용량이 감소하고 그 효과가 의문시 되었기 때문에 제품의 라이프사이클이 단축되고, 연구개발 예산은 치료기간을 연장하고 골다공증 치료제 시장의 가치제안을 유지할 수 있는 차세대 생물학적 제제에 돌이켜졌습니다.

경구제는 알렌드론산 제네릭의 보급에 의해 2024년 매출의 65.60%를 차지하고 있지만, 주사제는 생물학적 제제의 보급을 반영하여 CAGR 5.89% 의 성장률을 기록했습니다. 데노스맙의 연간 2회의 피하 투여와 로모소주맙의월1회의 요법은 특히 다양성을 관리하는 노인 환자에서 매일 정제 투여에 비해 어드히어런스를 개선하였습니다.

재택간호사와 자가주사용 펜의 사용으로 통원 횟수가 감소하고, 메디케어에 의한 재택주사 보험 적용으로 자기부담액이 감소하였습니다. 졸레드론산의 정맥내 투여는 연간 1회 투여를 원하는 환자에게 유효성을 유지하였으나, 피하 생물학적 제형과의 격렬한 경쟁에 직면하였습니다. 신진대사 펩티드를 12주에 걸쳐 방출하는 하이드로겔 마이크로디포의 조사는 낮은 침습 투여에 대한 선호도를 더욱 기울일 수 있습니다. 신흥 시장에서는 콜드체인 물류가 여전히 병목이 되고 있지만, 패시브 운송 컨테이너나 약국용 냉장고에 대한 투자가 그 격차를 줄이고, 골다공증 치료제 시장의 새로운 주 매출이 창출되고 있습니다.

북미는 2024년에도 39.87%의 매출 점유율을 유지해 폭넓은 보험 적용 범위, 전문 약사 네트워크, 신규 승인 약제의 신속한 도입이 그 기반이 되고 있습니다. 메디케어 및 메디케이드 서비스 센터는 2025년 약물 치료 관리 핵심 목록에 골다공증 치료제을 추가하고 어드히어런스 향상과 골다공증 치료제 시장에 대한 추가 보충을 기대합니다. 캐나다의 의무적 골절 등록은 치료 상환과 가이드라인 준수의 연관성을 시작하여 지표 골절로부터 90일 이내의 첫 투여 포획을 개선했습니다.

아시아태평양은 가장 빠른 CAGR 7.01%로 성장을 지속하고, 2029년까지 연간 치료량으로 유럽을 추월할 것으로 예측되고 있습니다. 일본의 국민 모두 보험제도에서는 승인된 모든 골다공증 치료제 처방이 상환되지만, 농촌 지역에서는 진단 부족으로 인해 잠재적인 코호트가 남아 있습니다. 중국의 3차 병원 데이터에서는 데노스맙의 사용량이 전년 대비 78% 증가하고 있으며, 2024년의 국가상환약 리스트에 수재되는 것이 뒷받침하고 있습니다. 인도의 민간 병원에서는 로모소주맙의 스타터 투여를 포함한 골절 예방 패키지가 도입되어 골다공증 치료제 시장에 향후 순풍이 불 것임을 시사했습니다.

유럽은 안정적이지만 가격에 민감한 지역입니다. 유럽 의약청은 2024년 시판 후 데이터에 근거한 아발로파라타이드(abaloparatide)의 승인에서 볼 수 있듯이 라인 연장을 위한 실제 세계 증거를 수락하게 되었습니다. 각국의 의료기술평가기관은 지역 포뮬러에 들어가는 생물학적 제제에 대해 최대 25%의 대폭적인 할인을 협상하고 있으며, 수익 성장은 억제되고 있지만 환자의 접근은 확대되고 있습니다. 남미와 중동, 아프리카의 점유율은 여전히 한자리이지만, 공공기관에 의한 스크리닝 프로그램이 활발해지고, 세계적인 NGO가 비스포스포네이트 제제공급을 조성하고 있기 때문에 CAGR은 한자리대 중반으로 건전합니다. 개선 된 콜드체인 통로는 생물학적 제제의 침투를 촉진하기 시작하여 골다공증 치료제 약물 시장의 장기적인 확대로 이어지고 있습니다.

The osteoporosis drugs market generated USD 16.88 billion in 2025 and is forecast to advance at a 4.74% CAGR to reach USD 21.28 billion by 2030.

The trajectory shows a disciplined shift from low-priced bisphosphonates toward premium biologics and bone-building anabolic agents that promise faster fracture-risk reduction. Population aging, rising life expectancy, and earlier diagnosis-bolstered by opportunistic AI screening-continue to expand the treated patient pool. Reimbursement reforms that tie therapy to national fracture registries are speeding time-to-treatment, while real-world evidence pathways shorten product-approval cycles. Biosimilar launches following the denosumab patent cliff will add price competition yet simultaneously enlarge the osteoporosis drugs market by improving affordability.

Individuals aged 50 and above constitute the dominant risk group, and annual osteoporotic fractures are expected to reach 6.3 million by 2050, with Asia-Pacific carrying most of the future caseload. Hip-fracture mortality runs at 20% within 12 months, spurring demand for therapies that act quickly to rebuild bone and avert secondary fractures. In Japan, bone-density testing rates remain only 14% in rural hospitals despite 41% osteoporosis diagnoses, underscoring the diagnostic gap. Medicare spent USD 5.7 billion on fracture care for 1.8 million beneficiaries in 2016, and 80% of post-fracture patients still went untreated, highlighting cost pressures to expand access. These demographic forces cement a multi-year demand floor for every drugs class within the osteoporosis drugs market.

Anabolic drugs such as teriparatide and abaloparatide achieve vertebral-fracture reductions of 65% and 86%, respectively, outperforming antiresorptives and attracting premium reimbursement medpagetoday.com. The FDA's 2024 expansion of abaloparatide to treat male patients increased the addressable pool by 12% in the United States managedhealthcareexecutive.com. Sequential regimens that start with romosozumab then transition to denosumab preserve fracture-risk reductions over five years ucb.com. Japanese real-world evidence confirms that high-risk cohorts receive romosozumab with cardiovascular monitoring, signifying clinical trust despite label warnings springer.com. Stronger insurance coverage and updated guidelines legitimize the anabolic first-line approach, enriching the osteoporosis drugs market.

Average medication-possession ratios sit at only 61.9% after two years, and abrupt denosumab discontinuation triggers rebound bone resorption with a 20% higher fracture risk. Denosumab also shows hypocalcemia and dermatologic safety signals clustering in the first 30 days of use. Romosozumab carries boxed warnings for myocardial infarction and stroke; 0.8% of treated subjects experienced MI versus 0.3% on alendronate drugs.com. Bisphosphonate non-adherence still averages 23.3% in Japan despite monthly or quarterly dosing options. These compliance gaps shave growth from the osteoporosis drugs market, particularly in oral segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Bisphosphonates retained a 37.40% osteoporosis drugs market share in 2024, yet growth slowed to less than 1% annually as payers and physicians pivoted toward higher-value options. Sclerostin inhibitors, chiefly romosozumab, exhibited the fastest 5.23% CAGR as clinicians prioritized rapid bone-formation gains for severe-risk patients. RANKL inhibitors, anchored by denosumab, remained the top-selling biologic because six-month dosing supports adherence.

Selective estrogen receptor modulators held niche roles for women unable to tolerate bisphosphonates, while parathyroid hormone analogues served as bridge therapy before antiresorptive maintenance. Pipeline attention shifted to microRNA modulators and Wnt-signaling activators that promise dual bone-building and resorption-control profiles. Declining calcitonin use, owing to questionable efficacy, shortened product life-cycles and redirected R&D budgets toward next-generation biologics that can lengthen treatment duration and sustain the osteoporosis drugs market's value proposition.

Oral drugs still composed 65.60% of 2024 revenue because of generic alendronate's ubiquity, but injectables expanded at a 5.89% CAGR, reflecting biologic uptake. Denosumab's twice-yearly subcutaneous dosing and romosozumab's monthly regimen improved adherence relative to daily pills, particularly among elderly patients managing polypharmacy.

Home-health nurses and self-injection pens reduced hospital visits, while Medicare coverage for in-home injections lowered out-of-pocket costs. Intravenous zoledronic acid maintained relevance for patients seeking once-yearly dosing, yet its usage faced stiff rivalry from subcutaneous biologics. Research into hydrogel micro-depots that release anabolic peptides over 12 weeks could further tilt preferences toward minimally invasive delivery. Cold-chain logistics remained a bottleneck in emerging markets, but investment in passive shipping containers and pharmacy-grade refrigerators is narrowing the gap, unlocking new provincial sales for the osteoporosis drugs market.

The Osteoporosis Drugs Market Report Segments the Industry Into by Drug Class (Bisphosphonates, Selective Estrogen Receptor Modulators (SERMs) and More), by Route of Administration (Oral, Injectable, Others), and by Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America preserved its 39.87% revenue share in 2024, anchored by broad insurance coverage, specialty pharmacist networks, and quick uptake of newly approved agents. The Centers for Medicare & Medicaid Services added osteoporosis to its 2025 Medication Therapy Management core list, which is expected to raise adherence and push additional refills into the osteoporosis drugs market. Canada's mandatory fracture registries began linking treatment reimbursement to guideline adherence, improving first-dose capture within 90 days of index fracture.

Asia-Pacific recorded the fastest 7.01% CAGR and is projected to overtake Europe in annual treatment volumes by 2029. Japan's universal coverage reimburses every approved osteoporosis regimen, yet under-diagnosis in rural prefectures leaves a latent cohort untapped. China's tertiary-hospital data show denosumab usage rising 78% year on year, supported by inclusion in the 2024 National Reimbursement Drug List. India's private-sector hospitals introduced bundled fracture-prevention packages that incorporate romosozumab starter doses, suggesting future tailwinds for the osteoporosis drugs market.

Europe remains a stable yet price-sensitive region. The European Medicines Agency now accepts real-world evidence for line-extensions, as seen in abaloparatide's 2024 authorization based on post-marketing data. National health technology assessment bodies negotiate steep discounts-up to 25%-for biologics entering regional formularies, restraining revenue growth but widening patient access. South America and the Middle East & Africa still account for single-digit shares yet post healthy mid-single-digit CAGRs as public-sector screening programs ramp and global NGOs subsidize bisphosphonate supplies. Improved cold-chain corridors are beginning to unlock biologic penetration, seeding long-term expansion for the osteoporosis drugs market.