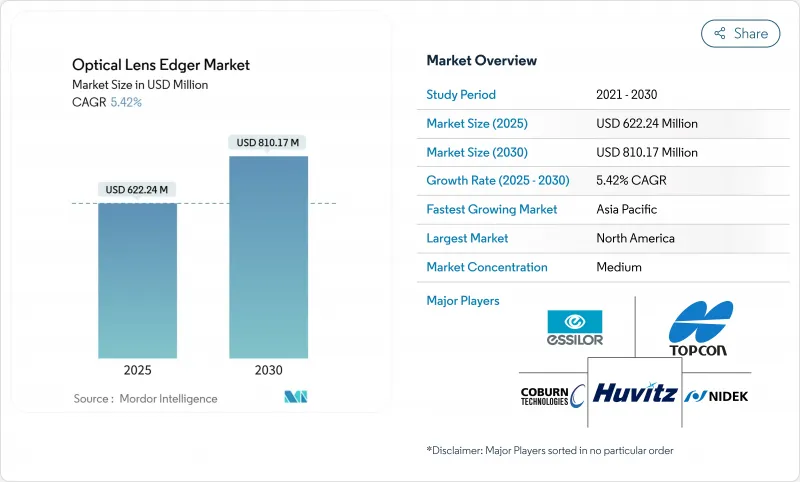

광학 렌즈 에저 시장은 2025년에 6억 2,224만 달러, 2030년에는 8억 1,017만 달러에 이르고, CAGR 5.42%로 성장할 것으로 예상됩니다.

현재의 성장 패턴은 근시 유병률 증가, 노안 인구 증가, 소비자용 및 산업용 기기에서 정밀 광학 부품의 사용 확대라는 강력한 믹스를 반영합니다. 자동화된 패턴리스 컴퓨터 수치 제어(CNC) 장치는 마무리 오차를 줄이고 복잡한 자유형 렌즈 형상을 수용할 수 있기 때문에 현재는 기술 기준을 정하고 있습니다. 점포 내에 마무리 실험실을 건설하는 지역 소매 체인, 초박형 카메라용 광학 부품을 요구하는 스마트폰 제조업체, 광학 서비스를 일원화하는 병원은 모두 수요 곡선에 영향을 주고 있습니다. 프리미엄 다이아몬드 휠공급 체인 제약과 공기 중 먼지 처리에 관한 규칙의 엄격화는 비용면에서 역풍이 되지만, 대부분의 선도적인 벤더들은 위험을 억제하기 위해 수직 통합을 추구하고 있습니다.

2020년에는 세계 인구의 30% 가까이가 근시가 되었으며, 2050년에는 복잡한 처방 렌즈에 의지하고 있는 10억명의 강도 근시의 사람들을 포함해 50%가 될 것으로 예측되고 있습니다. 자유 형상 에지에 의해 고굴절률 기판은 박형을 유지하면서, 소비 전력 요건을 충족할 수 있기 때문에 광학 렌즈 에저 시장은 혜택을 받습니다. 원격 근무 문화는 스크린 사용 시간을 늘리고 옥외 노출을 줄이는데, 이는 근시 진행을 앞당깁니다. 경제적으로 아시아 성인은 이미 연간 3,280억 달러를 근시 교정에 소비하고 있으며, 고급 마감 도구에 대한 구매력이 지속되고 있음을 보여주고 있습니다. 신형 에저는 알고리즘을 통합하여 블루라이트 필터 렌즈 제조를 용이하게 하여 실험실이 프리미엄 주문을 획득할 수 있도록 합니다.

지역 체인은 점포 전개를 가속화하고, 컴팩트한 엣지 랩을 짜넣어, 당일 배송을 약속합니다. 파리미키는 국내 635점포, 해외 74점포를 전개해, 각 점포에서 렌즈의 마무리를 자사에서 실시해, 외부랩의 비용을 삭감하는 것과 동시에 서비스 스피드를 향상시키고 있습니다. 사무실 내 시스템은 1건당 5-15달러의 비용 절감이 가능하며, 하루 50조를 넘으면 즉시 투자 회수가 가능합니다. 기기 제조업체 각 사는 중급의 자동장치를 2만-5만 달러의 레인지에 위치시키고, 신규 참가자에게 있어서 저렴한 가격과 정밀도의 교량을 하고 있습니다.

1일 일회용 렌즈는 2023년 영국의 소프트 렌즈 장착률의 78.8%로 성장했습니다. EVO ICL과 같은 굴절 교정 수술 옵션은 젊은 사용자에게 안경을 사용하지 않는 기간을 연장합니다. 이러한 변화는 성숙한 소매 채널에서 대량 생산 렌즈의 에지 수요를 완화시키고 있지만, 산업용 및 진단용 광학 부품은 여전히 불안정합니다.

자동 모델은 최대 수익 풀을 만들었으며 2024년에는 54.81%의 광학 렌즈 에저 시장 점유율을 획득했습니다. 폐쇄 루프 서보 모터와 패턴리스 트레이스는 마무리 시간을 단축하고 불합격률을 줄이고 다초점 렌즈의 당일 납품을 가능하게 합니다. 자동 플랫폼과 관련된 광학 렌즈 에저 시장 규모는 중견 소매업체가 수동 벤치에서 탈퇴함에 따라 2030년까지 연평균 복합 성장률(CAGR) 5.8%로 확대될 것으로 예측됩니다. 자본 예산이 부족한 곳에서는 수동 기계가 뿌리 깊지만 개조된 자동 기계가 2차 시장에 진입하기 때문에 점유율은 감소에 직면하고 있습니다. 반자동 시스템은 능력과 비용을 교차하지만, 점유율은 6.47%에 그치고 장기적인 매력은 제한적입니다. 블로커와 에저의 일체형 디자인은 바닥 면적을 줄이고 워크플로우를 간소화하여 단위 성장률이 가장 높습니다.

통합을 통해 공급업체는 소프트웨어, 에지 및 코팅을 하나의 인클로저에 번들로 제공합니다. 프라운호퍼 IPT의 48시간 광학 셀은 성형, 레이저 절삭 및 에지 마감을 하나의 트럭으로 수행하는 공장 대응 블록을 나타내며 차세대 제품 라인에 박차를 가하는 템플릿이 될 수 있습니다. 공급업체는 수동으로 캘리브레이션 없이 CR-39에서 폴리카보네이트로 전환하기 위해 AI 구동 파라미터 라이브러리를 통합합니다. 이러한 기능은 하드웨어 마진이 줄어들더라도 시스템의 가치가 높아지는 이유를 명확하게 보여줍니다.

북미는 2024년 42.72%로 가장 큰 수익 슬라이스를 만들었습니다. 안과 검진에 대한 강력한 보험 적용, 프리미엄 코팅 소비자 수용, 독립 검안사의 치밀한 네트워크가 장비 회전에 박차를 가하고 있습니다. 많은 개업의들이 1시간 서비스를 요구하고 사무실 내 실험실로 이동하여 자동 에저의 보급을 확대하고 있습니다. 이 지역은 또한 현지에 서비스 거점을 제공하는 선도적인 제조업체를 보유하고 있기 때문에 가동 중지 시간의 벌칙은 낮게 유지되고 기술 업데이트를 촉구합니다. 광선 피폭에 관한 안전 가이드라인이 먼지 제거 기준을 엄격하게 해, 실험실을 최신의 밀폐 시스템으로 유도합니다.

아시아태평양은 2025-2030년 CAGR 7.15%로 가장 빠르게 성장할 것으로 예상되고 있습니다. 싱가포르와 같은 시장에서는 도시의 10대 청소년의 근시율이 80%를 넘어 처방량을 유지하는 요인이 되고 있습니다. EssilorLuxottica는 이 지역에서 8.2% 증가를 기록했는데, 이는 매장 내 가장자리를 통합한 체인 개발의 반영입니다. 중국은 밸류 렌즈를 우대하는 조달 규칙에 의해 가격 압력을 완화하고 실험실을 다초점 마무리로 유도하여 마진을 유지합니다. 일본의 파리미키(Paris Miki) 안경 체인은 정밀성을 최우선으로 하며, AI 대응 블로커 수요에 박차를 가합니다. 인도와 동남아시아는 가처분 소득이 프리미엄 렌즈 업그레이드를 가능하게 하고 새로운 레인을 엽니다.

유럽에서는 기술 업데이트 사이클과 특수 용도에 견인되어 안정적인 수요를 보이고 있습니다. 로덴스톡의 체코공장으로의 마무리 전환은 비용 최적화를 강조하지만 품질 수준은 여전히 높습니다. 콘택트렌즈 채택은 유럽 전반에 걸쳐 5.2% 증가하고 수량은 뻗어나지만, 엄격한 동심도를 필요로 하는 다초점 하드 렌즈의 틈새 기회를 자극합니다. 라틴아메리카와 중동은 소규모 설치 기반에서 시작하지만, 관민 파트너십이 시력 검사 이니셔티브에 자금을 제공함으로써 두 자릿수 단위 성장률을 기록하고 있습니다.

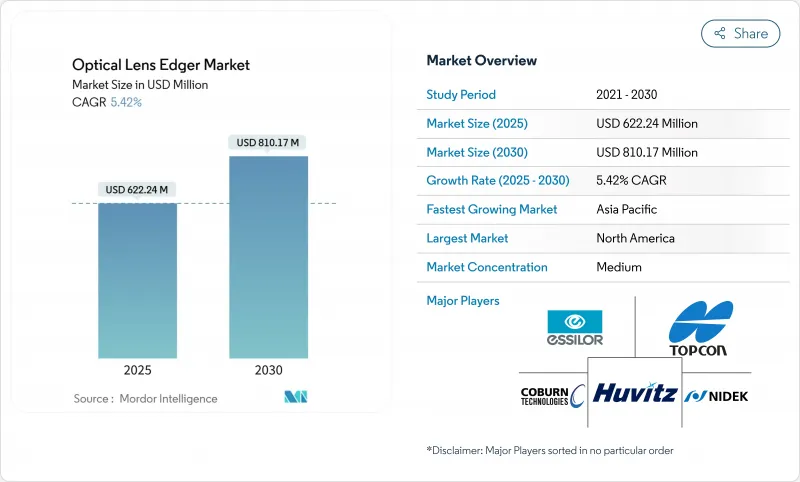

The optical lens edger market generated USD 622.24 million in 2025 and is forecast to reach USD 810.17 million by 2030, advancing at a 5.42% CAGR.

The current growth pattern reflects the powerful mix of rising myopia prevalence, a larger presbyopic population, and the widening use of precision optics across consumer and industrial devices. Automatic, pattern-less computer-numerical-control (CNC) units now set the technology benchmark because they reduce finishing errors and accommodate complex freeform lens geometries. Regional retail chains that build in-store finishing labs, smartphone makers that demand ultra-thin camera optics, and hospitals that centralize optical services all feed the demand curve. Supply chain restraints for premium diamond wheels and stricter rules on airborne dust disposal introduce cost headwinds, yet most leading vendors pursue vertical integration to limit risk.

Nearly 30% of the world's population lived with myopia in 2020; projections point to 50% by 2050, including 1 billion high myopes who rely on complex prescription lenses . The optical lens edger market benefits because freeform edging allows high-index substrates to retain thin profiles while meeting power requirements. Remote work culture amplifies screen time and shortens outdoor exposure, both linked to faster myopia progression. Economically, Asian adults already spend USD 328 billion yearly on myopia correction, signaling sustained purchasing power for advanced finishing tools. New edgers integrate algorithms to ease blue-light filter lens production, enabling labs to capture premium order value.

Regional chains accelerate store rollouts and embed compact edging labs to promise same-day delivery. Paris Miki operates 635 outlets in Japan and 74 abroad, each equipped to finish lenses in-house, cutting external lab fees while improving service speed. In-office systems trim USD 5-15 per job, yielding quick payback when volumes exceed 50 pairs a day. Equipment makers position mid-tier automatic units at the USD 20,000-50,000 range, bridging affordability and precision for new entrants.

Daily disposable lenses grew to 78.8% of UK soft-lens fits in 2023, reflecting consumer tilt toward lower maintenance eyewear . Refractive surgery options such as EVO ICL extend spectacle-free intervals for younger users. These shifts temper high-volume lens edging demand in mature retail channels, though industrial and diagnostic optics remain insulated.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Automatic models generated the largest revenue pool and captured 54.81% optical lens edger market share in 2024. Their closed-loop servo motors and patternless tracing shorten finishing time, reduce reject rates, and enable same-day delivery for multifocal lenses. The optical lens edger market size tied to automatic platforms is forecast to expand at 5.8% CAGR through 2030 as mid-tier retailers move away from manual benches. Manual machines persist where capital budgets are tight, yet their share faces erosion as refurbished automatic units enter the secondary market. Semi-automatic systems bridge capability and cost, but only 6.47% share confirms limited long-run appeal. Integrated blocker-edger designs post the highest unit growth because they cut floor space and streamline workflows, a key metric for urban clinics with limited real estate.

Consolidation drives suppliers to bundle software, edging, and coating in one enclosure. Fraunhofer IPT's 48-hour optics cell indicates how factory-ready blocks encompass forming, laser ablation, and edge finishing in a single track, a template that could spur next-generation product lines. Vendors embed AI-driven parameter libraries to switch from CR-39 to polycarbonate with no manual recalibration. Such features underscore why system value rises even as hardware margins compress.

Optical Lens Edger Market is Segmented by Type (Manual, Automatic, and More), Application (Eyeglass Lens, Microscope Lens, and More), by End User (Independent Optical Stores, Ophthalmology Hospitals & Clinics, and Others), and Geography. The Market Provides the Value (in USD Million) for the Above-Mentioned Segments.

North America generated the largest revenue slice at 42.72% in 2024. Strong insurance coverage for eye exams, consumer acceptance of premium coatings, and a dense network of independent optometrists fuel equipment turnover. Many practitioners shifted to in-office labs for one-hour service, extending automatic edger penetration. The region also hosts major manufacturers that offer local service hubs; therefore, downtime penalties remain low and encourage technology updates. Safety guidelines on optical-radiation exposure tighten dust-extraction standards, pushing labs to modern enclosed systems.

Asia-Pacific is the fastest riser at 7.15% CAGR from 2025-2030. Myopia incidences above 80% among urban teens in markets such as Singapore feed sustained prescription volumes. EssilorLuxottica logged 8.2% revenue lift in the region, mirroring chain expansion that embeds in-store edging. China moderates price pressure through procurement rules that favor value lenses, steering labs toward multifocal finishing to preserve margins. Japan's Paris Miki chain prioritizes precision, spurring demand for AI-enabled blockers. India and Southeast Asia open fresh lanes as disposable incomes permit premium lens upgrades.

Europe exhibits stable demand driven by technology refresh cycles and specialized applications. Rodenstock's migration of finishing to Czech plants underscores cost-optimization, yet quality bars remain high. Contact-lens adoption-up 5.2% across Europe-tempers unit volumes yet stimulates niche opportunities in multifocal hard lenses that need tight concentricity. Latin America and the Middle East start from small installed bases but post double-digit unit growth where public-private partnerships fund vision-screening initiatives.