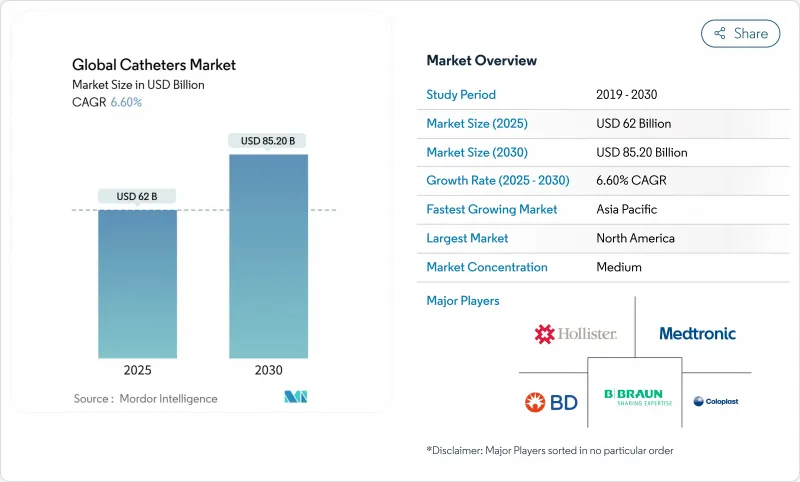

카테터 시장은 2025년에 620억 달러, CAGR 6.6%로 성장하고, 2030년에는 852억 달러에 이를 것으로 예측됩니다.

인구동태의 고령화, 만성 심혈관계 질환과 신장질환의 부담 증가, 저침습 수술의 폭넓은 수용이 수요를 자극하고 있습니다. 보다 스마트한 코팅, 임베디드 센서, AI 지원 설계를 실현하는 기술 사이클은 카테터 제품의 임상적 유용성을 더욱 확대합니다. 동시에 제조업체가 안정적인 품질과 가격을 유지하기 위해 노력하는 동안 특수 폴리머 및 실리콘 공급망 재구성이 전략적 초점이 되었습니다. 경쟁 포지셔닝은 단편화된 제품의 틈새 시장을 통합하고 지적 재산을 보호하기 위해 기술 혁신 파이프라인에서 경쟁 포지셔닝이 전환되고 있습니다. 재택 셀프 케어의 치료 기회는 여전히 크고, 지원적인 상환과 원격 의료 서비스에 의해 시설 밖에서의 치료 경로가 가능하게 되어, 대응 가능한 카테터 시장은 기존 병원 환경으로부터 크게 확대하고 있습니다.

심혈관 질환은 현재 6억 5,500만 명이 이환되고 있으며, 뇌졸중 이환율은 2019년부터 2024년에 걸쳐 15% 상승하여 혈전 제거 치료용 신경혈관 카테터의 채택을 촉진하고 있습니다. 만성 신장병은 8억 5,000만 명에 영향을 미치고, 선진지역의 혈액투석인구가 매년 6% 증가함에 따라 투석액세스 카테터 수요가 높아집니다. 이러한 역학적 기세는 카테터의 수량이 경기 사이클의 영향을 받기 어려워지고, 보다 광범위한 카테터 시장에서 필수적인 관리 도구로서의 역할을 강조합니다.

선진국의 헬스케어 시스템에서는 카테터를 이용한 수술이 심혈관 수술의 75%를 차지하고 있으며, 10년 전의 45%에서 증가하고 있습니다. 메드트로닉의 펄스 필드 어블레이션 플랫폼 PulseSelect는 2024년에 30%의 매출 성장을 기록했지만, 이는 재원 일수의 단축과 결과 개선을 시스템 전체에서 추진하고 있음을 반영하고 있습니다. Stereotaxis EMAGIN과 같은 로봇 내비게이션 솔루션도 방사선 피폭을 억제하면서 정밀도를 높입니다. 이러한 역학은 지불자가 절차의 효율성을 요구하는 동안 카테터 시장 전체의 지속적인 수요를 보강합니다.

일부 환경에서는 유치 카테터 감염률이 25%에 달하고 카테터 관련 혈류 감염으로 인한 사망률은 25%에 달할 전망입니다. 규제 당국이 감염 제어 프로토콜을 강화하는 동안, 장치의 체류 시간 제한 및 교체 빈도 증가는 비용을 증가시키고, 임상 워크플로우를 복잡하게 하고, 카테터 시장의 단기적인 기세를 억제하고 있습니다.

심혈관 카테터는 2024년에 카테터 시장의 28.7%를 차지했으며, 혈관 조영, 절제, 전기생리학의 각 분야에서 확립된 임상 프로토콜에 의해 지원되고 있습니다. 병원이 여러 크기와 구성을 일상적으로 재고하므로 이 성숙도에 따라 안정적인 수량이 확보됩니다. 심혈관 인터벤션용 카테터 시장 규모는 관상동맥 질환의 유행에 따라 견고하게 확대될 것으로 예측됩니다. 신경혈관 카테터는 뇌졸중 센터가 확장되고 기계적 혈전 제거 장치의 효능이 입증됨에 따라 매출 규모는 여전히 작으며 CAGR 7.3%로 확대됩니다. 스탠포드 대학의 미리스피너 기술은 기존 시스템의 50%에 비해 90%의 성공률을 기록해 기술 주도의 업사이드를 강조하고 있습니다.

기술 혁신의 파이프라인은 여전히 활성화되어 있습니다. 스티어러블 팁, 정교한 브레이딩, 더 부드러운 폴리머가 신경혈관 내비게이션을 향상시키고, 위험 프로파일을 좁히고, 새로운 절차 적응을 엽니다. 정맥 카테터는 병원 공급망에서 가장 생산적인 소모품이지만, 가격 설정이 상품화되어 마진 압력이 계속됩니다. 폐색 풍선에서 약물 용출형에 이르기까지 특수 디자인의 카테터는 가격이 비싸고 수익성을 압박합니다. 전체 카테터 시장에서는 임상적 증거, 상환의 명확성, 재료의 가용성에 따라 점유율이 달라집니다.

카테터 시장 보고서는 업계를 제품별(심혈관 카테터, 비뇨기 카테터, 정맥 카테터, 신경혈관 카테터, 기타 제품), 최종 사용자별(병원, 간호 시설, 기타 최종 사용자), 지역별(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)으로 분류합니다. 5년간의 과거 동향과 향후 5년간의 예측을 얻을 수 있습니다.

북미는 선진적인 병원 네트워크, 조기 기술 도입, 유리한 상환에 힘입어 2024년 전 세계 매출의 43.3%를 유지했습니다. FDA의 브레이크스루 디바이스 패스웨이는 신규 카테터 시장 진입을 앞당기고 메디케어의 보험 적용 확대는 고가치 디바이스로 몰아치게 됩니다. 하지만 성숙시장의 가격 압축과 병원 예산의 조사가 수량 성장의 발판이 되고 있습니다. 규제 상황의 안정적이고 예측 가능한 지불 상황으로 인해, 이 지역은 여전히 프리미엄 카테터 기술 실험실이 되고 있으며, 카테터 시장에 미치는 영향력을 확고히 하고 있습니다.

유럽은 의료기기 규제에 의해 형성되는 2위의 클러스터입니다. 엄격한 기술 문서와 시판 후 조사는 특히 소규모 기업의 경우 컴플라이언스 비용을 증가시키고 공급업체 기반을 통합할 수 있습니다. 감염 예방 우선순위와 항균제 스튜어드십은 코팅된 단일 사용 장비 수요를 자극합니다. 브렉짓(EU 이탈) 관련 물류 문제와 특정 해외 공급업체를 제거하는 움직임을 포함한 입찰 규칙의 변화는 공급망 계획을 복잡하게 하지만 국내 생산에 유리하게 작용할 수 있습니다. 결과적으로 유럽 카테터 시장은 신중하지만 품질에 중점을 둡니다.

아시아태평양은 가장 빠르게 성장하는 시장으로 2030년까지 연평균 복합 성장률(CAGR)은 8.3%를 나타낼 전망입니다. 의료 시스템의 근대화, 수술 건수 증가, 국민 모두 보험 제도에 대한 정부 투자가 수요의 저조로 이어집니다. 이 지역의 의료기술 지출은 2030년까지 2,250억 달러에 달할 것으로 예측됩니다. 인도와 동남아시아에서는 현지 제조 인센티브, 기술 이전 협정, 급성장하는 민간 병원 부문이 진입 장벽을 낮추고 있습니다. 하지만 이질적인 규제 체제와 가격 상한 정책에 의해 APAC 카테터 시장에서 규모 확대를 목표로 하는 기업에게는 미묘한 시장 진출 전략이 요구됩니다.

The catheters market stood at USD 62.0 billion in 2025 and is forecast to reach USD 85.2 billion by 2030, advancing at a 6.6% CAGR.

Demographic aging, a rising burden of chronic cardiovascular and renal disease, and broader acceptance of minimally invasive procedures continue to stimulate demand. Technology cycles that deliver smarter coatings, embedded sensors, and AI-aided designs further widen the clinical utility of catheter products. At the same time, supply-chain re-engineering for specialty polymers and silicone has become a strategic focus as manufacturers strive to maintain consistent quality and pricing. Competitive positioning pivots on innovation pipelines, as firms look to consolidate fragmented product niches and defend intellectual property. Opportunities remain strong in home-based self-care, where supportive reimbursement and telehealth services enable non-institutional treatment pathways, extending the addressable catheters market well beyond traditional hospital settings.

Cardiovascular disease now affects 655 million individuals, while stroke incidence climbed 15% from 2019-2024, driving adoption of neurovascular catheters for thrombectomy procedures . Chronic kidney disease impacts 850 million people and lifts demand for dialysis access catheters as hemodialysis populations in developed regions expand 6% annually. This epidemiological momentum makes catheter volumes less sensitive to economic cycles and underscores their role as essential care tools within the broader catheters market.

Catheter-based techniques represent 75% of cardiovascular procedures in developed healthcare systems, up from 45% ten years ago. Medtronic's PulseSelect pulsed-field ablation platform posted 30% revenue growth in 2024, reflecting a system-wide push to lower hospital stays and improve outcomes . Robotic navigation solutions such as Stereotaxis EMAGIN also enhance precision while curbing radiation exposure. These dynamics reinforce sustained demand across the catheters market as payers seek greater procedural efficiency.

Indwelling catheter infection rates touch 25% in some settings, with catheter-related bloodstream infections carrying mortality rates up to 25%. As regulators tighten infection control protocols, device dwell time restrictions and more frequent replacements raise costs and complicate clinical workflows, curbing short-term momentum in the catheters market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cardiovascular catheters delivered 28.7% of the catheters market in 2024, supported by entrenched clinical protocols across angiography, ablation, and electrophysiology. This maturity ensures stable volumes as hospitals routinely stock multiple sizes and configurations. The catheters market size for cardiovascular interventions is projected to widen at a steady clip in line with coronary disease prevalence. Neurovascular catheters, while still smaller by revenue, advance at a 7.3% CAGR as stroke centers expand and mechanical thrombectomy devices prove efficacy. Stanford's milli-spinner technique posts 90% success versus 50% for legacy systems, underscoring technology-led upside.

Innovation pipelines remain active. Steerable tips, refined braiding, and softer polymers elevate neurovascular navigation, narrowing risk profiles and opening new procedural indications. Intravenous catheters stay the highest-volume consumable in hospital supply chains, but margin pressures persist given commoditized pricing. Specialty designs-ranging from occlusion balloons to drug-eluting configurations-command premium pricing and cushion profitability. Across categories, clinical evidence, reimbursement clarity, and material availability shape share shifts inside the broader catheters market.

The Catheters Market Report Segments the Industry Into by Product (Cardiovascular Catheters, Urology Catheters, Intravenous Catheters, Neurovascular Catheters, Other Products), by End User (Hospitals, Long Term Care Facilities, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America). Get Five Years of Historical Trends Plus Forecasts for the Next Five Years.

North America retained 43.3% of global revenue in 2024, underpinned by advanced hospital networks, early technology adoption, and favorable reimbursement. The FDA's breakthrough-device pathway has quickened market entry for novel catheters, while Medicare coverage expansions offer tailwinds for high-value devices. Even so, mature-market price compression and hospital budget scrutiny put a ceiling on volume growth. Regulatory stability and predictable payment landscape still make the region a testing ground for premium catheter technologies, cementing its influence on the catheters market.

Europe stands as the second-largest cluster, shaped by the Medical Device Regulation. Stringent technical documentation and post-market surveillance raise compliance costs, especially for small firms, potentially consolidating supplier bases. Infection-prevention priorities and antimicrobial stewardship stimulate demand for coated and single-use devices. Brexit-related logistics challenges and shifts in public-tender rules, including moves to exclude certain foreign suppliers, complicate supply-chain planning yet may favor local manufacturing. The net impact is a cautious but quality-focused European catheters market.

Asia-Pacific is the fastest-growing theater, expanding at an 8.3% CAGR through 2030. Health-system modernization, rising surgical volumes, and government investment in universal care strengthen underlying demand. The region's medical-technology spending is projected to hit USD 225 billion by 2030. Local manufacturing incentives, technology-transfer agreements, and a burgeoning private-hospital segment in India and Southeast Asia lower entry barriers. Nevertheless, heterogeneous regulatory regimes and price-cap policies require nuanced go-to-market strategies for firms seeking to scale in the APAC catheters market.