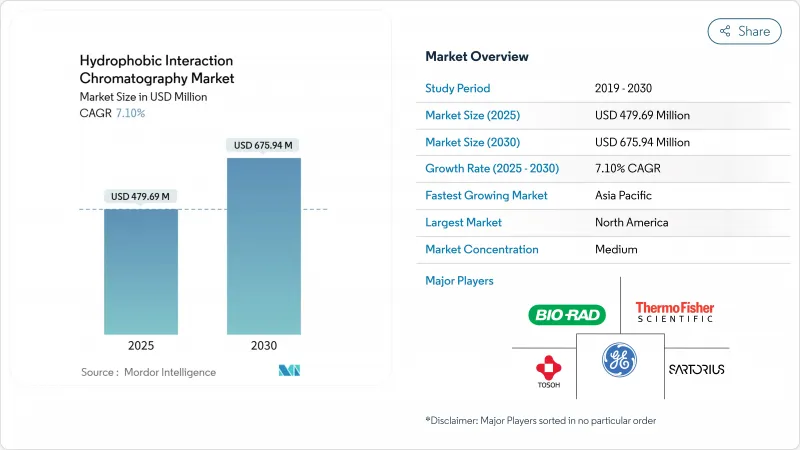

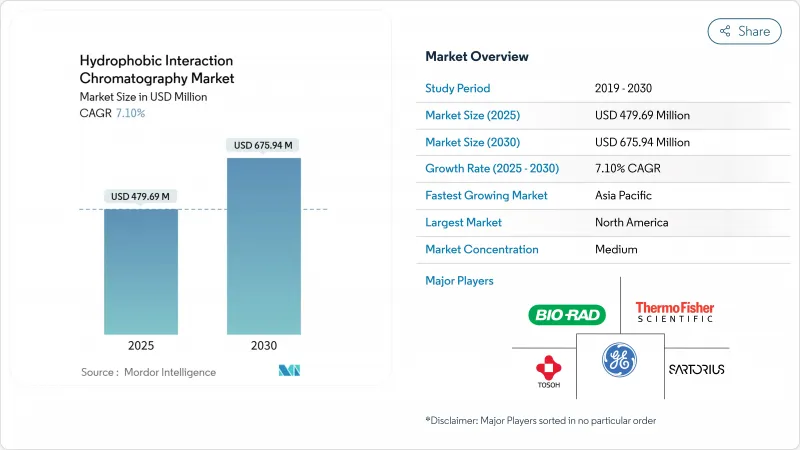

소수성 상호작용 크로마토그래피 시장은 2025년에는 4억 7,969만 달러, 2030년에는 6억 7,594만 달러에 이를 것으로 예측됩니다.

단일클론항체, 항체 약물 복합체 및 기타 복잡한 생물학적 제제의 다운스트림 연마에 대한 강력한 수요가 이러한 발전을 뒷받침하고 있으며, 제조업체는 숙주 세포의 단백질 수준이 비공식적인 기준값 100ppm 미만임을 보장하는 견고하고 고선택성 워크플로우를 요구하고 있습니다. Danaher의 15억 달러의 수지 확장 프로그램과 Samsung Biologics의 14억 6,000만 달러의 플랜트 업그레이드와 같은 생산 능력 향상은 정제 병목 현상을 증가시키는 반면, 세계 생산 헤드룸을 끌어올려 소수성 상호작용 크로마토그래피 시장 솔루션의 경제적 사례를 강화하고 있습니다. 믹스 모드 수지와 일렉트로스판 멤브레인의 기술 진보는 공정 트레인을 단축하고 용매 소비를 줄이고 업스트림 역가 상승에도 불구하고 비용 경쟁력을 유지합니다. 특히 미국과 유럽연합(EU)에서는 저염용출물을 중시하는 지역규제 프레임워크이 신청경로를 명확화하고 스케일업 리스크를 경감함으로써 보급을 더욱 가속화하고 있습니다.

항체가 상승으로 상업용 바이오리액터의 평균 캠페인은 5g/L를 넘어서고 하류의 병목 현상이 심각해지고 있습니다. 제조 경제학에 따르면 정화는 총 비용의 80%를 소비할 수 있으며, 제품 품질을 유지하는 더 적은 고용량 HIC 공정에 경영진의 초점을 맞추었습니다. 후지필름의 12억 달러를 건 노스캐롤라이나의 확장만으로 항체 전용으로 16만L가 추가되어 HIC 수지와 컬럼의 지역 수요가 즉시 높아집니다. 100ppm 미만의 경향이 있는 숙주 세포 단백질의 스펙은 HIC의 연마력을 후기 공정의 적격성 확인에 필수적인 것으로 하고 있습니다. 그 결과, 소수성 상호작용 크로마토그래피 시장공급업체는 중기 계획 주기를 통해 2자리 수익을 안정적으로 확보할 수 있습니다.

삼성 바이오로직과 롯데 바이오로직은 대규모 HIC 스위트를 갖춘 최첨단 다운스트림 홀을 중심으로 설계된 대규모 시설에 48억 달러 이상의 예산을 기록하고 있습니다. 의약품 검사 협력 체계 하에서 통일된 표준은 사양의 모호함을 해소하고 있기 때문에 구매자는 저비용 레거시 장비가 아닌 고성능 소수성 상호작용 크로마토그래피 시장 장비를 자유롭게 선택할 수 있습니다. 인천에 있는 Cytiva의 신공장과 같이 컬럼과 수지의 현지 생산은 리드타임을 단축하고 외환 익스포저를 줄이기 위해 다국적 기업은 이 지역에 대한 조달의 균형을 재검토하게 됩니다. 그 결과, 생산 능력의 증강은 수지의 인출에 직결되어 소수성 상호작용 크로마토그래피 업계의 수익 기반이 강화됩니다.

Industry 4.0 구상에서는 데이터 사이언스의 능력이 요구되지만, 그 능력은 여전히 부족하고, 기업이 지속적인 HIC 트레인을 전개할 때 임금 인플레이션과 프로젝트 지연을 일으키고 있습니다. Python이나 R과 같은 프로그래밍 언어는 이제 크로마토그래피 데이터 처리의 기본 요구 사항이지만, 이러한 기술을 가진 프로세스 엔지니어는 단지 일부에 불과하며 검증 타임라인을 길게 하고 있습니다. 파일럿 규모에서는 인건비가 원재료비를 상회하기 때문에 미충족의 역할은 영업이익률에 직접 영향을 미치고 소수성 상호작용 크로마토그래피의 신규 시장 도입이 지연됩니다. 벤더가 주최하는 연수 프로그램은 어느 정도는 인재 부족을 해소하지만, 신흥 시장에서의 사업 확대의 페이스는 여전히 인재 육성의 페이스를 상회하고 있어, 이것이 단기적인 시장의 성장을 억제할 가능성이 있습니다. 커리큘럼이 개선될 때까지 기술 부족은 소수성 상호작용 크로마토그래피 시장의 기세를 저해하는 직접적인 요인이 될 전망입니다.

컬럼이 2024년 매출의 41%를 차지하는 이유는 최종 사용자가 검증된 자동화 스크립트와 잘 결합되어 수정 없이 당국의 신청에 적합한 장치를 선호하기 때문입니다. 레이디얼 디자인이 인기를 끌고 있지만, 처리량 압력 손실의 트레이드 오프가 경제성을 좌우하고 있습니다. 최종 사용자는 견고한 팩 무결성 테스트와 입증된 세척 프로토콜을 중시하고 대체 장치가 대용량을 홍보하더라도 정평이 있는 컬럼 브랜드를 선택하기 때문에 소수성 상호작용 크로마토그래피 시장은 레거시 실적를 중심으로 정착하고 있습니다. 이 컬럼은 또한 타사 스키드 인티그레이터의 광범위한 네트워크를 통해 여러 플랜트 네트워크에서 조달과 검증을 단순화할 수 있다는 장점이 있습니다. 또한 스케일의 안정성과 친숙한 제어 인터페이스는 운영자의 훈련 부담을 줄여줍니다. 멤브레인 모듈은 소량의 공정에서 위력을 발휘하는 것, 배치 사이즈가 2,000L를 넘는 경우, 수지의 재이용에 의해 자본 지출을 장기 캠페인으로 상각할 수 있기 때문에 컬럼은 디폴트인 채입니다. 수지의 내부 확산 제약이 계속해서 유량의 상한을 결정하고 있지만, 공급업체는 현재 시스템 유압을 변화시키지 않고 용적 생산성을 두 배로 늘리기 위해 비드 구조를 최적화하고 있습니다. 규제 당국이 하드웨어의 전반적인 교환에 신중하기 때문에 컬럼은 소수성 상호작용 크로마토그래피 시장의 중심이 되는 것으로 보입니다.

수지는 저염에서 보다 우수한 선택성을 추구하는 혼합 모드 리간드의 급속한 채택으로 CAGR 9.8%와 가장 높은 성장 궤도를 지원하고 있습니다. 아가로스 매트릭스는 생체적합성과 높은 점유율을 차지하고 폴리머 비드는 알칼리 세척 및 고압 세척이 요구되는 분야에서 높은 점유율을 획득하고 있습니다. 제조업체 각 사는 보다 짧은 합성 경로를 사용하는 리간드 화학에 많은 투자를 하고, 리드 타임을 단축하고, ESG 보고 의무에 따라 탄소 강도를 삭감하고 있습니다. 퓨로라이트가 1억 5,000만 달러를 투자하여 펜실베니아에 건설한 아가로스 수지의 거점은 북미의 현지 공급을 크게 확대하고 지정학적 위험을 줄이고 지역 창고를 통해 서비스 수준을 향상시켰습니다. 바이어는 이러한 회복력을 수량과 가격을 고정하는 다년간의 이중조달 계약으로 보상해 소모품 조달팀에 있어서 소수성 상호작용 크로마토그래피 시장 규모를 안정시킵니다. 업스트림 밀도가 상승하는 경향이 있기 때문에 동적 용량이 조달 스코어 카드가됩니다. 따라서, 수지의 기술 혁신은 대응가능한 소수성 상호작용 크로마토그래피 시장 전체를 형성하는 결정적인 변수로 계속됩니다.

수십 년에 걸친 공정 특성 데이터의 축적과 많은 규제 전례가 있습니다. 공정 이관의 위험은 여전히 낮으며, 신뢰성으로 인해 품질 관리 팀은 익숙한 소금 구배 워크플로우에 머물러 있다는 것을 확신합니다. 기존의 생물 제제 포트폴리오의 검증 문서는 신제품 템플릿으로도 작동하므로 개발 일정이 단축되고 컨설팅 비용도 억제됩니다. 따라서, 소수성 상호작용 크로마토그래피 시장은 페닐 및 부틸과 같은 확립된 리간드에 의존하며, 이들 리간드는 다중 사이클 세척 요법 하에서 견고성을 충분히 이해하고 있습니다. 전환 비용은 소모품뿐만 아니라 전자 배치 기록의 모든 행에 이르기 때문에 재무 팀은 완전한 리엔지니어링이 아니라 단계적인 프로세스 강화를 선호합니다. 연속적인 설계에도 불구하고, 고전적인 충진 바닥은 스위칭 밸브 매트릭스 내에 편안하게 들어가기 때문에 설치 베이스가 더욱 보호됩니다.

소수성 상호작용 크로마토그래피는 소수성 상호작용과 정전기 상호작용을 연결하므로 개발자는 민감한 페이로드를 중성에 가까운 pH에서 용출시킬 수 있습니다. 바이러스 벡터 및 ADC 제품에 관한 규제 당국에 대한 신청 서류도 늘고 있으며, 후기 단계에서 예기치 않은 사태를 방지하는 품질 기능에 대한 신뢰도 높아지고 있습니다. 단백질 과학자들은 HCIC이 극단적인 염분이나 pH를 사용하지 않고 미묘한 글리코폼의 차이를 해결함으로써 제품의 열화를 피하고 효력을 유지할 수 있다는 점을 높이 평가했습니다. 공급업체는 현재 수지 스크리닝을 수개월이 아닌 몇 주로 단축하는 예측 시뮬레이션 도구를 제공하고 있으며, 개발 일정이 엄격한 소수성 상호작용 크로마토그래피 시장의 이용 사례를 확대하고 있습니다. 더 많은 바이오파머가 고도로 변형된 항체 스캐폴드에 축발을 두는 동안, HCIC의 차별화된 선택성은 반복 주문을 보장하고 플랫폼 채택에 대한 길을 엽니다.

북미는 현재 매출액의 37.5%를 차지하며, 혁신자, 수탁 제조업자, 공구 공급업체와 깊은 관계를 맺고 있습니다. 식품의약국은 지속적인 생산을 권장합니다. 식품의약국은 인라인 모니터링에 대한 기대를 명확히 하는 가이던스를 발표하고, 시험적·상업적 환경에서 멤브레인 기반의 연속적인 HIC의 채택을 뒷받침하고 있습니다. 미국에서는 최근 생물 제제 인프라에 대한 세액 공제를 포함한 연방 정부의 우대 조치가 상당한 자본 비용을 낮추고 높은 처리량 컬럼 스키드의 주문을 지원합니다. 캐나다는 항체 의약품 시설에 대한 보완적인 투자를 추구하고 멕시코는 수지 수요 증가로 이어지는 지역 충전 마감 허브를 추진합니다. 이러한 네트워크가 서로 연결되어 국경을 넘어선 물류가 리드 타임을 단축하고 소수성 상호작용 크로마토그래피 시장의 발자취를 깊게 하고 있습니다.

유럽은 새로운 정제 기술의 신속한 상호 승인을 촉진하는 유럽 의약청(EEA)의 하모나이제이션 프레임워크에 견인되고 있습니다. 독일에는 바이오클러스터가 집적되어 있으며 이산화탄소 삭감 목표도 함께 공급업체는 ISO 14064 보고서에 적합한 저용매 HIC 워크플로우 설계에 주력하고 있습니다. 영국은 HIC가 중심적인 역할을 하는 바이러스 벡터 정제를 필요로 하는 첨단 치료 애플리케이션을 신속하게 진행함으로써 브렉짓 후 생명 과학의 지위를 지키고 있습니다. 남유럽 국가들은 EU 부흥 기금을 활용하여 생물 제제 공장을 현대화하고 수출 품질 기준을 충족하기 위해 자동화 된 HIC 공정을 도입하고 있습니다. 환경, 사회, 거버넌스(ESG) 룰도 제조업체에 화학 실적가 적은 수지의 채택을 강요해 지역 소수성 상호작용 크로마토그래피 업계의 이야기를 더욱 형성하고 있습니다.

중국, 인도, 한국이 바이오파마의 자급자족을 확보하고 수탁제조의 흐름을 받아들이려고 경쟁하고 있기 때문에 아시아태평양의 CAGR은 가장 빠른 11.1%를 나타냅니다. 삼성 바이오 로직과 롯데 바이오 로직으로 대표되는 대규모 캠퍼스 프로젝트는 업스트림, 다운스트림 및 필링 마무리 유닛을 하나의 사이트에 통합하여 수지와 컬럼 수요를 장기적으로 둘러싸고 있습니다. 각국 정부는 투자회수기간을 단축하기 위해 세제우대조치와 가속상각을 실시하고, 현지 규제당국은 의약품검사협력계획의 무결성을 승인하여 수출통관을 원활하게 합니다. 일본의 이노베이터는 공정 개발의 엄격함을 도입하고 세계 공급업체와 협력하여 멤브레인 HIC 솔루션을 시험적으로 도입하고, 지역 전체에 기술 파급의 종을 뿌립니다. 동남아시아 국가는 소규모 다품종 생산 공장을 증설하고 모듈식으로 단납기 패키지를 제공하는 소수성 상호작용 크로마토그래피 시장공급업체 고객 기반을 확대하고 있습니다.

The hydrophobic interaction chromatography market stands at USD 479.69 million in 2025 and is forecast to reach USD 675.94 million by 2030, reflecting a 7.1% CAGR over the period.

Strong demand for downstream polishing of monoclonal antibodies, antibody-drug conjugates, and other complex biologics underpins this advance, as manufacturers seek robust, high-selectivity workflows that guarantee host-cell protein levels below informal 100 ppm thresholds. Capacity additions such as Danaher's USD 1.5 billion resin expansion program and Samsung Biologics' USD 1.46 billion plant upgrade raise global production headroom while amplifying purification bottlenecks, thereby reinforcing the economic case for hydrophobic interaction chromatography market solutions. Technology progress in mixed-mode resins and electrospun membranes shortens process trains, reduces solvent consumption, and keeps cost-of-goods competitive despite higher upstream titers. Regional regulatory frameworks that emphasize low-salt eluates, especially in the United States and European Union, further accelerate uptake by clarifying submission pathways and mitigating scale-up risk.

Rising antibody titers have moved average commercial bioreactor campaigns above 5 g/L, which intensifies downstream bottlenecks that only hydrophobic interaction chromatography market workflows currently address with proven robustness. Manufacturing economics reveal that purification at times consumes 80% of the total cost of goods, sharpening management focus on fewer, higher capacity HIC steps that retain product quality. Fujifilm's USD 1.2 billion North Carolina expansion alone adds 160,000 L dedicated to antibodies and immediately lifts regional demand for HIC resins and columns. Host-cell protein specifications trending below 100 ppm make the polishing power of HIC indispensable for late-stage process qualification. The knock-on effect is steady double-digit revenue visibility for hydrophobic interaction chromatography market suppliers through mid-term planning cycles.

Asia-Pacific governments are pouring incentives into GMP plants, and the region's stainless-steel volume is rising faster than anywhere else, opening a persistent gap for purification infrastructure.Samsung Biologics and Lotte Biologics together earmark more than USD 4.8 billion for large-scale facilities, each engineered around state-of-the-art downstream halls that feature sizable HIC suites. Harmonized standards under the Pharmaceutical Inspection Co-operation Scheme are eliminating specification ambiguity, so buyers are free to select higher-performance hydrophobic chromatography market equipment rather than the lowest-cost legacy gear. Local production of columns and resins, such as Cytiva's new plant in Incheon, reduces lead times and foreign-exchange exposure, prompting multinationals to re-balance sourcing toward the region. As a result, capacity increments translate directly to resin pull-through, strengthening the hydrophobic interaction chromatography industry revenue base.

Industry 4.0 initiatives mandate data-science competencies that remain scarce, driving wage inflation and project delays when firms roll out continuous HIC trains. Programming languages such as Python and R are now basic requirements for chromatography data handling, yet only a fraction of process engineers possess such skills, lengthening validation timelines. Labor costs outstrip raw-material spending by an order of magnitude at pilot scale, so unfilled roles directly dent operating margins and slow new hydrophobic interaction chromatography market installations. Vendor-hosted academies partially close gaps, but emerging-market buildouts still outpace talent development, which could temper near-term uptake. Until curricula evolve, the skills deficit will be an immediate drag on the hydrophobic interaction chromatography market momentum.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Columns dominate with 41% 2024 revenue because end-users favor equipment that pairs well with validated automation scripts and meets agency filings without amendments. Large axial configurations still headline high-volume installations, though radial designs gain popularity where throughput pressure drop trade-offs tilt economics. End-users lean on robust pack integrity testing and proven cleaning protocols, choosing established column brands even when alternate devices advertise higher capacity, thus anchoring the hydrophobic interaction chromatography market around legacy footprints. Columns also benefit from a wide network of third-party skid integrators, simplifying procurement and validation across multi-plant networks. In turn, scale stability and familiar control interfaces lessen operator training burdens, a decisive factor amid acute workforce shortages. Though membrane modules nibble at small-lot processes, columns remain the default when batch sizes exceed 2,000 L because resin reuse amortizes capital outlays over longer campaigns. Resin internal diffusion constraints continue to set flowrate ceilings, but suppliers are now optimizing bead architecture to double volumetric productivity without altering system hydraulics. As regulatory bodies stay cautious about wholesale hardware swaps, columns will remain centre-stage in the hydrophobic interaction chromatography market even as adjacent formats proliferate.

Resins underpin the highest growth trajectory at 9.8% CAGR due to rapid adoption of mixed-mode ligands pursuing better selectivity at lower salt. Agarose matrices command premium share on biocompatibility, while polymeric beads claim ground where alkaline cleaning or high pressure demands apply. Manufacturers channel heavy investment into ligand chemistry that uses shorter synthesis paths, cutting lead times and reducing carbon intensity in keeping with ESG reporting duties. Purolite's USD 150 million Pennsylvania site for agarose resin greatly enlarges North America's local supply, trims geopolitical risk, and elevates service levels through regional warehousing. Buyers reward such resilience with multi-year dual-sourcing agreements that lock volume and price, stabilizing the hydrophobic interaction chromatography market size for consumables sourcing teams. As upstream densities keep trending higher, dynamic capacity becomes the procurement scorecard; hence resin innovation remains the decisive variable that shapes the total addressable hydrophobic interaction chromatography market.

With decades of process characterization data and copious regulatory precedents. Process transfer risk remains low, and that reliability convinces quality leadership teams to stay with familiar salt-gradient workflows. Validation documentation from older biologics portfolios doubles as a template for new products, which compresses development calendars and curbs consulting spend. The hydrophobic interaction chromatography market, therefore, leans on established ligands like phenyl and butyl, whose robustness is thoroughly understood under multi-cycle cleaning regimens. Switching costs extend beyond consumables, touching every line in electronic batch records, so finance teams often prefer incremental process bolstering instead of full re-engineering. Even within continuous designs, classical packed beds nest comfortably inside switching valve matrices, further protecting their installed base.

Hydrophobic-charge induction chromatography is the fastest climber because it marries hydrophobic and electrostatic interactions, letting developers elute sensitive payloads at near-neutral pH. Its growing dossier of regulatory filings for viral vector and ADC products elevates confidence among quality functions that guard against late-stage surprises. Protein scientists appreciate HCIC for resolving subtle glycoform differences without extreme salt or pH, which avoids product degradation and preserves potency. Vendors now supply predictive simulation tools that shorten resin screening to weeks, not months, expanding the hydrophobic interaction chromatography market use case in strained development timelines. As more biopharmas pivot toward highly modified antibody scaffolds, HCIC's differentiated selectivity secures repeating orders and paves the way for platform adoption.

The Hydrophobic Interaction Chromatography Market is Segmented by Product (Columns {Axial Flow, Radial Flow} and Resins {Agarose-Based and More), Technology (Classical HIC, and More), Sample Type (Monoclonal Antibodies, Antibody-Drug Conjugates, and More), End User (Pharma & Biopharma Companies, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America commands 37.5% of current revenue and holds a deep bench of innovators, contract manufacturers, and tool suppliers whose proximity shortens supply chains and speeds service response. The Food and Drug Administration endorses continuous manufacturing. It publishes guidance that clarifies expectations for in-line monitoring, thereby emboldening adopters of membrane-based continuous HIC in pilot and commercial settings. United States federal incentives, including recent tax credits for biologics infrastructure, lower effective capital cost, and underpin orders for high-throughput column skids. Canada pursues complementary investments in antibody facilities, while Mexico advances regional fill-finish hubs that create incremental resin demand. As these networks interlink, cross-border logistics keeps lead times short and deepens the hydrophobic interaction chromatography market footprint.

Europe remains a powerhouse driven by the European Medicines Agency's harmonized framework, which facilitates quick mutual recognition of new purification technologies. Germany's concentration of biotech clusters, coupled with carbon-reduction targets, pushes suppliers to design low-solvent HIC workflows suited for ISO 14064 reporting. The United Kingdom safeguards its post-Brexit life-sciences status by fast-tracking advanced therapy applications, many requiring viral vector purification where HIC plays a central role. Southern European states leverage EU recovery funds to modernize biologics plants, inserting automated HIC steps to meet export quality tiers. Environmental, social, and governance (ESG) rules also force manufacturers to adopt resins with lower chemical footprints, further shaping the regional hydrophobic interaction chromatography industry narrative.

Asia-Pacific delivers the fastest 11.1% CAGR as China, India, and South Korea race to secure biopharma self-sufficiency and capture contract manufacturing flows. Massive campus-style projects, typified by Samsung Biologics and Lotte Biologics, integrate upstream, downstream, and fill-finish units in a single site, locking in long-term resin and column demand. Governments extend tax holidays and accelerated depreciation to shorten payback periods, while local regulators endorse Pharmaceutical Inspection Co-operation Scheme alignment, smoothing export clearance. Japanese innovators inject process-development rigor and collaborate with global suppliers to pilot membrane HIC solutions, seeding technology spill-overs region-wide. Southeast Asian nations add smaller multiproduct plants, thereby broadening customer bases for hydrophobic interaction chromatography market suppliers that offer modular, quick-turnaround packages.