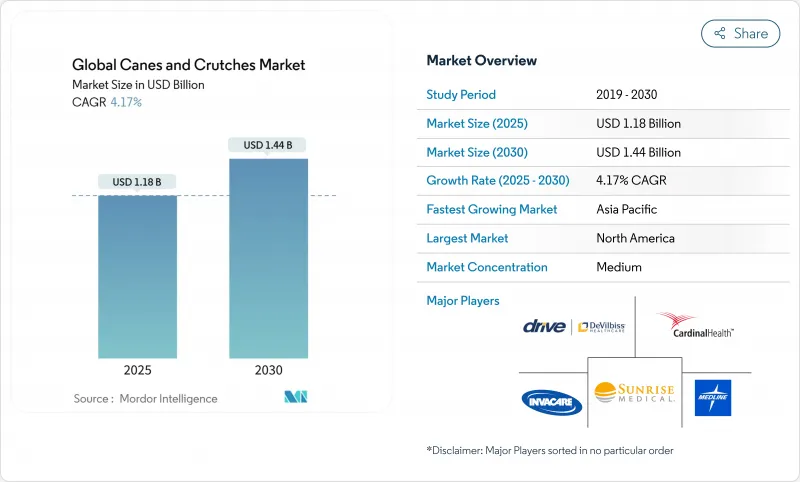

지팡이 및 목발 세계 시장 규모는 2025년에 11억 8,000만 달러, 2030년에는 14억 4,000만 달러에 이를 것으로 예측되며, 예측 기간의 CAGR은 4.17%를 나타낼 전망입니다.

수요는 기본적인 보행 보조구로부터 협조 간병 프로그램이나 자립 생활에의 소비자의 기대에 적합하는 접속형의 경량 기기로 꾸준히 이행하고 있습니다. 세계보건기구(WHO)는 2050년까지 25억 명이 보조기구를 필요로 할 것으로 예상하고 있습니다. 기술에 대응하는 건강 관리 시스템, 새로운 상환 코드, 근골격계 질환의 유병률의 상승은 고객층을 더욱 넓혀줍니다. 탄소섬유 복합재가 장비를 경량화하고 센서 통합을 가능하게 함에 따라 재료 과학은 전략적 요인이 되었습니다. 동시에 정책 입안자는 '로테크' 장비의 문서화 규칙을 엄격하게 하고, 공급업체는 임상적 가치를 정당화하고 제품 업데이트 사이클을 가속화할 필요가 있습니다.

유엔의 데이터에 따르면 후발 경제국가는 65세 이상의 인구비율이 급상승하고 있으며 지팡이 및 목발 시장의 장기적인 상승을 뒷받침하고 있습니다. 노인 인구 증가는 균형 보조기구 수요 증가에 직결 될뿐만 아니라 진행하는 운동 능력의 저하로 인한 대체품 수요 증가로 이어집니다. 일본과 같은 아시아 국가에서는 2025년까지 고령자 1인당 부양률이 2.4명까지 저하되고, 간병인의 능력이 박박해, 자조구의 보급이 촉진됩니다. 각국 정부는 건강 장수 정책과 상환 제도의 개선으로 대응하고, 이들이 함께 장기적인 구매 의욕을 유지합니다.

근골격계 질환으로 지팡이와 목발 시장에 만성적인 이용자가 끊임없이 유입되고 있습니다. 이러한 질병은 점진적으로 진행되기 때문에 장비의 수명주기와 교체 빈도가 길어집니다. 비침습적인 보조기구는 수술에 비해 비용 회피를 요구하는 지불자에게 어필하고 목발과 지팡이를 보존적 치료 전략의 중심에 둡니다. 좌석 없는 라이프 스타일이나 스포츠에 의한 스트레스로 관절에 손상을 받는 젊은층이 늘어남에 따라, 종래의 고령자층 이외에도 대응 가능한 수요가 퍼지고 있습니다.

휠체어, 스쿠터, 보행기는 특히 근력과 균형이 현저하게 손상된 사용자에게는 기능적인 대체품입니다. 메디케어의 전동이동기구에 대한 상세한 규칙에 따라 이러한 옵션은 특정 임상 프로파일에서 재정적으로 실현 가능합니다. 전동 어시스트 기술의 진보로 노력의 차이가 더욱 줄어들고, 목발을 완전히 회피하는 소비자도 나오고 있습니다.

2024년 지팡이 및 목발 시장에서 이 부문의 점유율은 55.23%로, 경도에서 중등도의 균형 장애를 가진 사용자를 위한 싱글 포인트, 쿼드, 오프셋 설계의 범용성이 확인되었습니다. 목발은 베이스야말로 작지만, 재활 프로토콜이 조기 보행에 중점을 두게 되고, 또 스마트 목발의 프로토타입이 기술에 정통한 클리닉을 끌어들이게 되었기 때문에 2030년까지 연평균 복합 성장률(CAGR) 4.41%로 확대할 것으로 예측됩니다. 겨드랑이형은 이용자의 피로나 신경압박의 리스크가 있기 때문에 인간공학에 근거한 팔뚝형에 수요가 유도됩니다. 하중 센서와 블루투스 모듈이 탑재된 스마트 송엽 지팡이는 부상 후 치료를 증거 기반 프로세스로 바꾸고 규정 준수를 추적하려는 치료사에게 호소합니다.

소재 대체의 고조가 제품 분할을 뒷받침하고 있습니다. 가벼운 탄소섬유 샤프트는 스윙 클리어런스를 개선하고 상체의 부담을 줄이기 위해 장기 사용자 채택을 뒷받침합니다. 아이스 칩, 회전식 페룰, 충격 흡수 그립 등의 액세서리 판매는 제조업체가 범용 프레임을 넘어 차별화를 도모하는 데 정기적인 수익층을 형성하고 있습니다. 목발의 처방은 종종 외래 수술을 수반하기 때문에 퇴원 계획 담당자는 지팡이 및 목발 시장에서 브랜드 선택의 중요한 게이트키퍼가 되었습니다.

알루미늄은 가격 성능비가 뛰어나 공구 라인이 확립되어 있기 때문에 2024년 매출은 37.46%에 달할 전망입니다. 그러나 탄소섬유는 CAGR 4.51%에서 가장 급성장하고 있습니다. 복합재 샤프트는 고 사이클 하중을 견디는 반면, 무게는 강철 샤프트의 절반 이하이므로 허약한 노인과 활발한 재활 환자에게도 지지됩니다. 게다가, 탄소섬유는 차세대 커넥티드 에이드의 필수 조건인 구조적 무결성을 손상시키지 않고 센서 어레이를 위한 내장 배선을 수용할 수 있습니다.

목재는 전통적인 미관을 선호하는 사용자를 위한 틈새 비계를 유지하지만 무게, 습기 및 유지 보수의 단점을 반영하여 점유율이 떨어지고 있습니다. 열가소성 엘라스토머는 미끄러지기 어려움과 진동 감쇠성이 작업 치료사로부터 다시 주목받는 팁과 인체 공학을 기반으로 한 핸들의 역할을 찾습니다. 헬스케어의 조달 정책이 라이프사이클의 탄소발자국의 저감을 받아들이는 가운데, 재활용 가능한 복합 수지가 지속가능성의 테코가 되어, 지팡이 및 목발 시장을 더욱 견인하고 있습니다.

지팡이 및 목발 세계 시장은 제품 유형, 재질, 최종 사용처, 유통 경로, 그리고 지역에 따라 세분화됩니다. 제품 유형으로는 지팡이(단일점 지팡이 등)와 목발(겨드랑이형 목발 등)이 포함되며, 재질은 목재, 알루미늄 등이 사용됩니다. 주요 최종 사용자는 병원 및 의원, 가정간호 환경 등이며, 유통 경로는 소매 약국 등을 중심으로 합니다. 지역적으로는 북미, 유럽, 아시아-태평양 등을 포함하며, 시장 예측은 미국 달러(USD) 기준의 가치로 제공됩니다.

북미는 2024년 세계 매출의 40.53%를 차지하고 장비 취득을 조성하는 메디케어 및 메디케이드 정책과 견고한 유통 인프라에 지지를 받고 있습니다. 이 지역의 지팡이 및 목발 시장 규모는 청구 표준화와 신속한 청구 처리를 촉진하는 HCPCS 코드를 업데이트함으로써 혜택을 누리고 있습니다. 높은 기술 보급률이 센서 대응 모델의 조기 도입을 촉구해, 공급자에게 가격 결정력을 주고 있습니다. 65세 이상의 고령자 비율이 해마다 증가하는 가운데, 인구동태는 계속해서 중심적인 추진력이 되고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)은 아시아태평양이 가장 빠른 4.52%를 보일 것으로 예측됩니다. 2040년에 89조엔에 달할 것으로 예측되는 일본의 헬스케어 지출은 급속하게 고령화가 진행되는 인구에 비용 효율적인 이동 보조 기구를 배치하는 것이 재정적으로 불가결하다고 강조하고 있습니다. 2060년까지 33조 4,000억 달러에 이를 것으로 예상되는 중국의 의료비는 잠재 고객층을 더욱 확대합니다. 지역정부는 기본적인 보행 보조구를 상환하는 지역보건 프로그램에 투자하고 있으며 수량 확대를 자극하고 있습니다. 중국과 인도의 현지 생산 클러스터는 리드 타임을 단축하고 육상 비용을 낮추어 지팡이와 목발 시장의 침투를 가속화합니다.

유럽은 견고하지만 느린 성장을 제공합니다. 일관된 CE 마크 프로세스가 시장 진입을 간소화하는 반면, 각 국가의 지불자는 엄격한 증거 요구 사항을 유지하고 공급업체는 데이터가 풍부한 스마트 장치를 요구합니다. 지속가능성 지령은 재활용 가능한 재료를 지지하고 탄소섬유의 채택을 가속화하고 있습니다. 대조적으로 중동, 아프리카와 남미는 개발 도상에서 발전 도상으로 전환하고 있습니다. 가처분 소득 증가와 보험 적용률의 향상에 의해 점차 보급이 진행되고 있지만, 유통망의 제약과 임상의밀도의 저하가 단기적인 진보를 억제하고 있습니다.

The global canes and crutches market size stood at USD 1.18 billion in 2025 and is expected to reach USD 1.44 billion by 2030, advancing at a 4.17% CAGR over the forecast period.

Demand moves steadily from basic walking aids to connected, lightweight devices that fit coordinated care programs and consumer expectations for independent living. Population ageing supplies the deepest demand pool, with the World Health Organization estimating 2.5 billion people in need of assistive products by 2050. Technology-ready healthcare systems, new reimbursement codes and rising musculoskeletal disease prevalence further widen the customer base. Materials science has become a strategic factor as carbon-fiber composites cut device weight and enable sensor integration. At the same time, policy makers tighten documentation rules for "low-tech" equipment, forcing suppliers to justify clinical value and accelerate product refresh cycles.

United Nations data show the share of people aged 65 and above rising sharply in the least-developed economies, confirming a prolonged upswing for the canes and crutches market. Larger elderly cohorts directly translate into higher demand for balance-support aids as well as replacements driven by progressive mobility decline. Asian countries such as Japan face support-ratio drops to 2.4 workers per senior by 2025, tightening caregiver capacity and encouraging uptake of self-help devices. Governments respond with healthy-ageing policies and reimbursement improvements, which together sustain long-range purchasing momentum.

Musculoskeletal disorders push a constant flow of chronic users into the canes and crutches market. These conditions advance gradually, extending device lifecycles and replacement frequency. Non-invasive aids appeal to payers seeking cost avoidance versus surgery, making crutches and canes central to conservative treatment strategies. As younger cohorts experience joint damage owing to sedentary lifestyles and sports stress, addressable demand widens beyond traditional senior demographics.

Wheelchairs, scooters and walkers present functional substitutes, especially for users whose strength or balance is severely impaired. Medicare's detailed rules for power mobility equipment make these options financially feasible for specific clinical profiles. Advancing power-assist technology narrows the effort gap further, prompting some consumers to bypass crutches entirely.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The segment held a 55.23% share of the canes and crutches market in 2024, confirming the versatility of single-point, quad and offset designs for users with light to moderate balance issues. Crutches, though smaller in base, are projected to expand at a 4.41% CAGR through 2030 as rehabilitation protocols emphasize early ambulation and as smart crutch prototypes attract technology-savvy clinics. Axillary models risk user fatigue and nerve compression, steering demand toward ergonomic forearm formats. Smart crutches equipped with load sensors and Bluetooth modules transform post-injury care into an evidence-based process, appealing to therapists intent on tracking compliance.

Rising material substitution underpins the product split. Lightweight carbon-fiber shafts improve swing clearance and reduce upper-body strain, boosting adoption among long-term users. Accessory sales such as ice tips, pivoting ferrules and shock-absorbing grips form a recurring-revenue layer that helps manufacturers differentiate beyond commodity frames. Because crutch prescriptions often accompany outpatient surgeries, hospital discharge planners have become a critical gatekeeper for brand choice in the canes and crutches market.

Aluminum delivered 37.46% revenue in 2024 thanks to its friendly price-performance ratio and established tooling lines. Carbon-fiber, however, represents the fastest growing slice at a 4.51% CAGR. Composite shafts withstand high cyclic loading while weighing less than half of steel counterparts, a benefit that resonates with frail seniors and active rehabilitation patients alike. In addition, carbon-fiber accommodates embedded wiring for sensor arrays without compromising structural integrity, a prerequisite for the next generation of connected aids.

Wood keeps a niche foothold serving users who favor traditional aesthetics, yet its declining share reflects weight, moisture and maintenance drawbacks. Thermoplastic elastomers find roles in tips and ergonomic handles, where slip resistance and vibration dampening gain renewed attention from occupational therapists. As healthcare procurement policies embrace lower life-cycle carbon footprints, recyclable composite resins add a sustainability lever that further propels the canes and crutches market.

Global Canes and Crutches Market is Segmented by Product Type (Canes [Single-Point Canes, and More], Crutches [Axillary Crutches, and More], and More), Material Composition (Wood, Aluminum, and More), End User (Hospitals & Clinics, Home-Care Settings, and More), Distribution Channel (Retail Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

North America anchored 40.53% of global revenue in 2024, supported by Medicare and Medicaid policies that subsidize device acquisition and by robust distribution infrastructures. The canes and crutches market size in the region benefits from updated HCPCS codes that standardize billing and facilitate quicker claims processing cms.gov. High technology adoption encourages early uptake of sensor-enabled models, giving suppliers pricing power. Demographic patterns remain a core driver, as the proportion of residents aged 65+ grows each year.

Asia-Pacific is forecast to post the fastest 4.52% CAGR through 2030. Japan's projected healthcare outlay of ¥89 trillion in 2040 underscores the financial imperative to deploy cost-effective mobility aids for a rapidly greying population. China's anticipated health spend reaching USD 33.4 trillion by 2060 further expands the prospective customer base. Regional governments invest in community health programs that reimburse basic walking aids, stimulating volume expansion. Local manufacturing clusters in China and India compress lead times and lower landed costs, accelerating penetration of the canes and crutches market.

Europe delivers solid yet slower growth. Harmonized CE-mark processes streamline market entry, while national payers maintain strict evidence requirements that push suppliers toward data-rich smart devices. Sustainability directives favor recyclable materials, accelerating carbon-fiber adoption. In contrast, Middle East & Africa and South America move from nascent to developing stages. Rising disposable incomes and insurance coverage improvements permit gradual uptake, though constrained distribution networks and lower clinician density temper short-term advances.