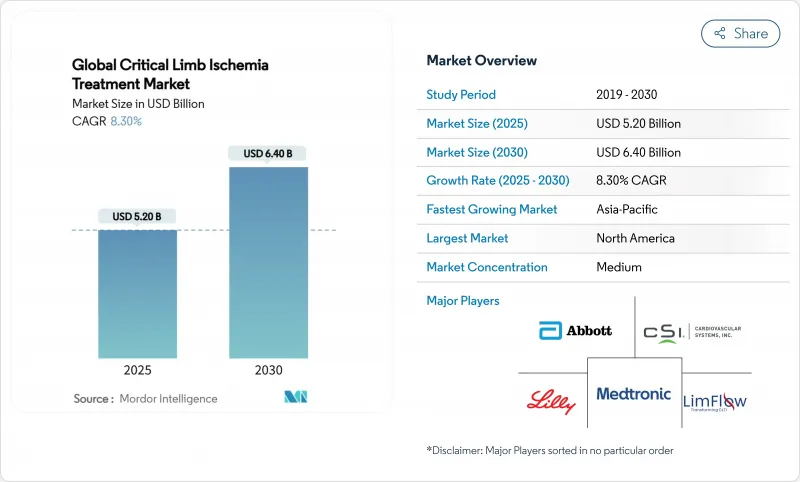

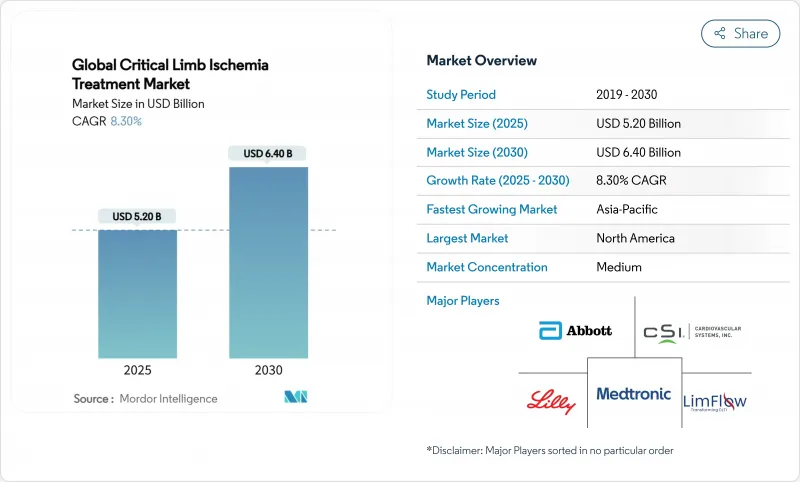

중증 하지허혈 치료 시장은 2025년에 52억 달러, 2030년에는 64억 달러에 이를 것으로 예측되며, 예측 기간의 CAGR은 7.5%로 예상됩니다.

평균 수명 증가, 당뇨병 이환율의 급상승, 첨단 하지(BTK) 혈관 내 치료 기술의 급속한 임상 도입이 이러한 확대를 지원하고 있습니다. 의료 시스템의 우선 순위도 변화하고 있습니다. 병원 프로그램에서는 절단보다 사지 온존을 중시하는 경향이 강해지고 있으며, 그 이유는 집학적인 구지 경로가 장기적인 비용이 낮고, QOL(생활의 질)도 우수하기 때문입니다. 풍선 혈관성형술에 비해 재개입률을 48% 감소시킨 Abbot사의 Esprit BTK 재흡수성 스캐폴드와 같은 획기적인 규제 당국의 승인은 새로운 장치에 대한 의사의 신뢰를 높여 대처 가능한 환자 풀을 크게 넓혔습니다. 유전자, 세포 및 GLP-1 기반 약물 요법의 병렬 진보는 단순히 폐색된 동맥을 재개방시키는 것이 아니라 미세혈관의 병태를 역전시키는 것을 목적으로 하는 새로운 치료 도구의 출현을 시사하며, 한때는 선택의 여지가 없는 것으로 여겨진 환자의 임상적 선택을 더욱 확대하고 있습니다.

세계적인 당뇨병 이환율 증가는 대사 기능 장애가 동맥 석회화와 미세 혈관 장애를 촉진하기 때문에 중증 하지허혈의 사례 수를 증가시키고 있습니다. 최근 집단 연구에서는 가이드라인에 따른 혈행 재건에도 불구하고 당뇨병성 허혈 환자의 절단률이 21.7%였고, 이들 환자의 96.9%가 심한 QOL 장애를 보고한 것으로 기록되었습니다. 이러한 발견은 Abbot의 Esprit BTK 스캐폴드와 같은 보다 내구성 있는 BTK 솔루션에 대한 수요를 강화하고 있습니다. STRIDE 시험은 세마글루티드가 이 집단에서 6분 동안 보행 거리를 26m 향상시키고 심혈관계 사건을 감소시켰으며, 대사 조절이 절단으로의 진행을 지연시킨다는 것을 시사합니다. 그 결과 혈관 내분비 통합 프로그램은 세계의 사지 온존 센터에서 급증하고 있습니다.

약물 용출 기술은 무릎 병변에서 일반적인 혈관 성형술을 대체합니다. 보스턴 사이언티픽의 AGENT 풍선은 2025년 1월부터 메디케어의 과도기적 통과 상태를 획득하여 BTK 병변에서 표적 병변의 혈행 재건술 위험을 50% 감소시켰습니다. 같은 시기에 이루어진 FDA의 메타 분석은 파클리탁셀의 안전성에 대한 이전의 우려를 해소하고 CLI 적응 환급 경로를 재개했습니다. 그 후 IN.PACT Global의 5년간의 데이터에서 임상적 혈행 재건술로부터의 해방은 69.4%로 나타났으며, 복잡한 해부학적 구조에서 약물 코팅의 내구성에 대한 실제 증거가 통합되었습니다. 시장 경쟁의 중심에는 보다 적은 약물 투여량으로 동등한 효능을 발휘하는 차세대 제제가 있으며, 개존성을 유지하면서 56%의 약물 투여량 절감을 목표로 하는 서모딕스의 선댄스 플랫폼이 그 예입니다. 이러한 요인을 종합하면, 안전성의 과도한 우려로 인해 지금까지 꺼려지고 있던 지역 병원에서의 의사에 의한 도입이 확대되어, 중증 하지허혈 치료 시장이 계속 확대될 전망입니다.

6명의 사망으로 이어진 이나리사의 클롯트리버 XL과 20명의 부상자를 낸 Philips의 택 시스템 등 중증 허혈 치료기에 관한 연속적인 클래스 I 리콜에 의해 규제 당국의 경계가 높아지고 있습니다. 미국 FDA는 현재 BTK에 특화된 보다 풍부한 안전 데이터셋을 요구하고 있으며, 특히 사지 보존를 전문으로 하는 소규모 혁신자의 경우 승인 일정이 장기화되고 시험 비용이 증가합니다. 병원은 또한 제품 평가위원회로 엄격하게 대응하여 시판 후 광범위한 감시가 나타날 때까지 신기술 도입을 연기할 수도 있습니다. 이러한 보호는 궁극적으로 환자의 이익으로 이어지지만 단기적인 상업적 채용 곡선은 평탄화되어 심사 기간 동안 중증 하지허혈 치료 시장 전체의 성장을 억제합니다.

2024년 중증 하지허혈 치료 시장의 69.8%는 치료 기기가 차지하였고, 약제 코팅 풍선(DCB), 약제 용출 스텐트(DES), 혈관내 결석 파쇄 시스템, 취약한 BTK 혈관용으로 설계된 재흡수성 스캐폴드 등이 그 중심에 있습니다. DCB와 DES는 미국에서의 보험 적용이 부활하고 재개입을 줄이는 강력한 증거에 힘입어 28억 달러 이상의 매출을 기록했습니다. 혈관내 결석파쇄술은 가장 급속히 침투하고 있는 하위 부문이며, 2024년 후반에 일본의 보험 적용을 확보한 쇼크 웨이브의 플랫폼만으로 전년 대비 75%의 매출 성장을 기록했습니다. 색전 방지 필터는 또한 원위로부터의 유출이 제한되는 긴 만성 완전 폐색(CTO)에 시술자가 작업할수록 중요성이 높아지고 있습니다. 이러한 역학으로 인해 장치 치료로 인한 중증 하지허혈 치료 시장의 규모는 2025년 36억 달러에서 2030년 46억 달러로 확대될 전망이며, 장치별 CAGR은 5.0%가 될 것으로 예측됩니다.

수술 이식편과 하이브리드 수술실은 여전히 다중 수준 질환에 대한 임상적 타당성을 유지합니다. 대퇴골 경골 우회술은 자가 정맥이 여전히 업계 표준이지만 등록 데이터는 정맥의 질이 나쁜 경우 HePTFE가 사지 보존와 동등하다는 것을 보여 주며 PFAS 관련 반대에도 불구하고 완만한 이식 수요를 유지합니다. 재생 접근법은 가장 매력적인 장기 보존법입니다. XyloCor의 XC001 혈관신생 유전자 치료는 무수술 CLI에서 12개월 후 운동부하의 피크 타임을 109초 개선하고, 제2상 줄기 세포 시험은 위약에 대해 36% 높은 관류 지수를 보이고 있습니다. 이러한 연구는 유전자 및 세포 치료 수익이 2030년까지 연평균 복합 성장률(CAGR) 17.5%를 달성할 것을 뒷받침합니다. 세마글루티드의 STRIDE와 리바록사반의 최근 제네릭 의약품 승인은 전신 요법의 사용을 확대하고 2030년까지 9억 달러의 의약품 매출을 창출할 것으로 예측됩니다. 이러한 개발을 종합하면 중증 하지허혈 치료 산업은 장비 중심의 치료에서 생물학적 정보를 기반으로 한 통합 치료 경로로 꾸준히 전환하고 있음을 알 수 있습니다.

아시아태평양은 2024년 세계 매출의 21.3%를 차지하였며 CAGR 9.1%로 성장할 것으로 예측됩니다. 중국은 2024년에 110만 명 이상의 말초 동맥 질환을 가진 신규 환자를 등록했으며, 그 중 23%가 조직 결손을 보이며 실질적인 미충족 요구가 존재함을 시사하고 있습니다. 2024년에는 60개 이상의 국산 말초 의료기기가 국가 의료 제품 관리국(National Medical Products Administration)의 인가를 취득했으며, 중국에서만 중증 하지허혈 치료 시장의 규모는 2030년까지 12억 달러에 달하고, 매년 10.4% 확대될 것으로 예측됩니다. 동시에 인도의 EU MDR과 장치 규칙의 조화는 심혈관조영실 인프라에 대한 외자 유치를 촉진합니다.

북미는 유리한 환급, 성숙한 사지 보존 네트워크, LimFlow 동맥 형성 및 AI 트리아지 알고리즘과 같은 획기적인 플랫폼의 조기 채용으로 2024년 세계 매출의 46.4%를 유지하였습니다. 이 지역은 메디케어의 일괄 지불 모델이 장기 무절단 생존율을 높이기 때문에 CAGR 6.4%로 계속 확대될 전망입니다. 유럽 시장은 규제의 파란을 극복하고 있습니다. PFAS의 규제는 인공 혈관 공급을 감소시킬 수 있지만, EU의 재흡수성 폴리머의 패스트트랙 지정은 장기적인 혼란을 완화시킬 수 있습니다. 그럼에도 불구하고 프랑스와 독일에서는 가격 억제 정책이 실시되고 있으며, ASP의 확대가 억제되어 있기 때문에 유럽의 CAGR은 4.2%에 그치고 있습니다. 반면, 걸프 협력 회의 입찰은 IVL과 상처 치료 소모품의 번들이 증가하고 있으며, 절단이 지배적이었던 패러다임에서 점차 다변화되고 있음을 보여줍니다.

The critical limb ischemia treatment market stood at USD 5.2 billion in 2025 and is expected to reach USD 6.4 billion by 2030, reflecting a 7.5% CAGR over the forecast period.

Growing life expectancy, the sharp rise in diabetes prevalence, and rapid clinical adoption of advanced below-the-knee (BTK) endovascular technologies underpin this expansion. Health-system priorities are also shifting: hospital programs increasingly emphasize limb preservation rather than amputation because multidisciplinary salvage pathways show lower long-term costs and superior quality-of-life outcomes. Breakthrough regulatory approvals such as Abbott's Esprit BTK resorbable scaffold, which lowered reintervention rates by 48% versus balloon angioplasty, have raised physician confidence in novel devices and opened sizable addressable patient pools. Parallel progress in gene, cell, and GLP-1-based pharmacotherapies signals an emerging therapeutic toolbox that aims to reverse microvascular pathology rather than merely reopen occluded arteries, further broadening clinical options for patients once considered no-option candidates.

Escalating global diabetes incidence propels critical limb ischemia case volumes because metabolic dysfunction accelerates arterial calcification and microvascular compromise. Recent cohort studies recorded 21.7% amputation rates among diabetic CLI patients despite guideline-directed revascularization, while 96.9% of those patients reported severe quality-of-life impairment.These findings intensify demand for more durable BTK solutions such as Abbott's Esprit BTK scaffold, which achieved 74% composite efficacy versus 44% with plain angioplasty. Diabetes also heightens interest in dual-benefit pharmacology: the STRIDE trial showed semaglutide improving 6-minute walk distance by 26 m in this cohort and lowering cardiovascular events, suggesting metabolic modulation can postpone progression to major amputation. As a result, integrated vascular-endocrine programs are proliferating within limb-preservation centers worldwide.

Drug-eluting technologies continue to displace plain angioplasty in below-the-knee lesions. Boston Scientific's AGENT balloon, granted Medicare Transitional Pass-Through status from January 2025, cut target lesion revascularization risk by 50% in BTK disease. A contemporaneous FDA meta-analysis resolved earlier paclitaxel-safety concerns, reopening the reimbursement pathway for CLI indications. Five-year IN.PACT Global data have since shown 69.4% freedom from clinically driven revascularization, consolidating real-world evidence for drug coating durability in complex anatomy. Market competition is now centered on next-generation formulations that deliver equivalent efficacy with lower drug doses, exemplified by Surmodics' Sundance platform that targets 56% drug-dose reduction while preserving patency. Collectively, these factors continue to expand the critical limb ischemia treatment market by widening physician uptake in community hospitals previously deterred by safety overhang.

Consecutive Class I recalls involving CLI devices-such as Inari's ClotTriever XL linked to 6 deaths and Philips' Tack system pulled after 20 injuries-have heightened regulatory caution. The U.S. FDA now requires richer BTK-specific safety datasets, prolonging approval timelines and elevating trial expense, especially for small innovators specializing in limb salvage. Hospitals also respond by tightening product-evaluation committees, sometimes deferring new technology uptake until extensive post-market surveillance emerges. While these protections ultimately benefit patients, near-term commercial adoption curves flatten, tempering overall critical limb ischemia treatment market growth during the review window.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Devices commanded 69.8% of the critical limb ischemia treatment market in 2024, anchored by drug-coated balloons (DCBs), drug-eluting stents (DES), intravascular lithotripsy systems, and resorbable scaffolds designed for fragile BTK vessels. DCBs and DES together generated more than USD 2.8 billion, buoyed by reinstated U.S. coverage and robust evidence for reduced reintervention. Intravascular lithotripsy is the fastest-penetrating subsegment; Shockwave's platform alone posted 75% year-on-year sales growth after securing Japanese reimbursement in late 2024. Embolic-protection filters also gain importance as operators tackle long chronic total occlusions (CTOs) where distal runoff is limited. With these dynamics, the critical limb ischemia treatment market size attributed to device therapy is forecast to expand from USD 3.6 billion in 2025 to USD 4.6 billion in 2030, representing a 5.0% device-specific CAGR.

Surgical grafts and hybrid operating suites nonetheless retain clinical relevance for multilevel disease. Autologous vein remains gold standard for femorotibial bypass, but registry data show HePTFE's limb-salvage equivalence when vein quality is poor, sustaining modest graft demand despite PFAS-related headwinds. Regenerative approaches deliver the most compelling long-term upside: XyloCor's XC001 angiogenic gene therapy improved peak treadmill time by 109 seconds at 12 months in no-option CLI, while Phase 2 stem-cell trials reported 36% greater perfusion index versus placebo. These studies support a 17.5% CAGR for gene- and cell-therapy revenue through 2030, albeit from a low base. Pharmaceuticals re-emerge as an adjunct: semaglutide's STRIDE and rivaroxaban's recent generic approval broaden systemic therapy use, generating a projected USD 900 million in drug sales by 2030. Collectively, these developments indicate the critical limb ischemia treatment industry is steadily migrating from device-centric rescue toward integrated, biologically informed care pathways.

The Critical Limb Ischemia Treatment Market is Segmented by Treatment Type, Including Devices (Embolic Protection Devices, Peripheral Dilatation Systems, and More), Drugs (Antiplatelet Drugs, Antihypertensive Agents, Lipid-Lowering Agents, and More), and Surgery (Bypass Surgery and Amputation), Along With Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Asia Pacific contributed 21.3% of global revenue in 2024 and is forecast to grow at a 9.1% CAGR, the fastest regional trajectory worldwide. China registered more than 1.1 million new peripheral artery disease admissions in 2024, 23% of whom presented with tissue loss, underscoring substantial unmet need. Over 60 home-grown peripheral devices obtained National Medical Products Administration clearance in 2024, and the critical limb ischemia treatment market size for China alone is expected to reach USD 1.2 billion by 2030, expanding 10.4% annually. Simultaneously, India's device-rule harmonization with EU MDR catalyzes foreign direct investment in cath-lab infrastructure; secondary-city hospitals are now equipped for DCB procedures that were previously limited to tertiary centers.

North America retained 46.4% of global revenue in 2024 due to favorable reimbursement, mature limb-salvage networks, and early adoption of breakthrough platforms such as LimFlow's arterialization and AI triage algorithms. The region will continue to expand at 6.4% CAGR as Medicare's bundled payment models reward long-term amputation-free survival-metrics strongly correlated with high-cost device utilization. European markets are navigating regulatory turbulence: PFAS restrictions could contract supply of vascular grafts, but the EU's fast-track designation for resorbable polymers may mitigate long-term disruption. Nonetheless, price-control policies in France and Germany dampen ASP expansion, capping European CAGR at 4.2%. Elsewhere, Latin America and the Middle East & Africa remain early-stage; Brazil's public-hospital procurement now authorizes DCBs in 10 states, while Gulf Cooperation Council tenders increasingly bundle IVL and wound-care consumables, signaling gradual diversification away from amputation-dominant paradigms.