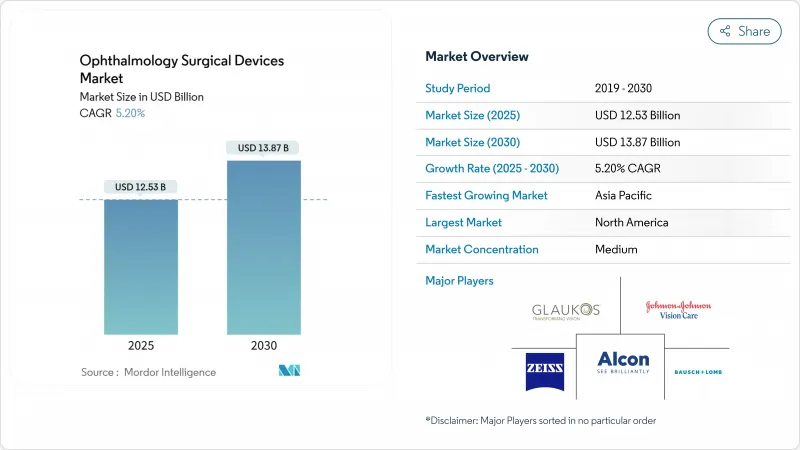

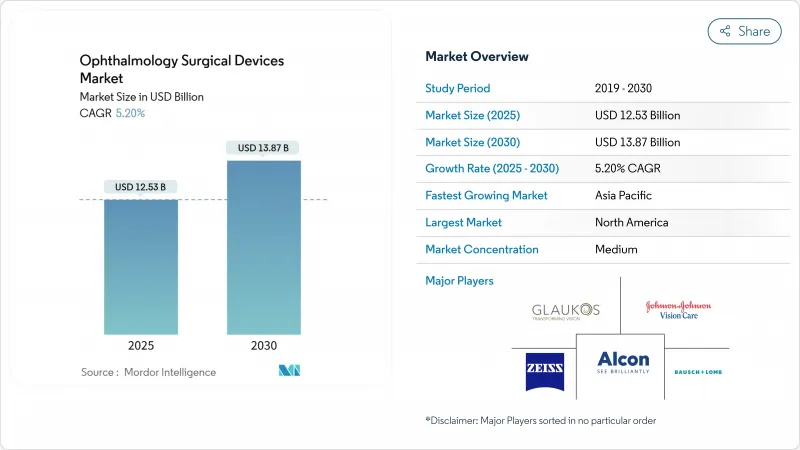

안과 수술 기기 시장 규모는 2025년에 125억 3,000만 달러, 2030년에는 138억 7,000만 달러에 이를 것으로 예상되며, 예측 기간의 CAGR은 5.20%를 나타낼 전망입니다.

지속적인 수요는 노화와 관련된 안과 질환의 세계적인 급증, 수술 범위의 확대, 신흥국 전반의 건강 관리 지출의 꾸준한 증가와 관련이 있습니다. 특히 파코시스템, 이미지 유도 현미경, 저침습 녹내장 임플란트 등의 견고한 제품 파이프라인을 통해 의료 제공업체는 수술 처리량을 높이면서 치료 성과를 향상시킬 수 있습니다. 북미에서는 외래 수술 센터(ASC)의 도입이 증가하고, 유리한 상환조정이 이루어지고, 아시아태평양에서는 저가격의 전용플랫폼을 이용 가능하게 되어 액세스가 더욱 넓어지고 있습니다. 한편, 주요 제조업체 간의 통합으로 진단, 계획 및 수술을 단일 워크플로우로 통합하는 통합 디지털 에코시스템이 구축되어 외과 의사의 생산성이 향상되고 프리미엄 제품의 차별화가 진행되고 있습니다.

백내장 수술 건수는 2036년까지 128% 증가할 것으로 예측되며, 85세 이상의 환자가 가장 큰 수요 증가를 낳습니다. 일본의 노인 인구는 이미 20%를 넘고 있으며, 외과 수술의 용량 확대의 기운이 넓게 높아지고 있습니다. WHO 비전 2030부터 국가별 실명 예방 계획에 이르기까지 수술 지연을 다루는 국가 프로그램은 많은 저소득 지역에서 보험 적용률을 향상시키고 있습니다. 2025년 호주에서 실시한 조사에서는 원주민의 백내장 수술률은 68%였는데 비선주민에서는 88.4%였습니다. 그러므로 서비스가 충분하지 않은 지역사회에 대응하고 안과 수술 기기 시장의 성장을 유지하기 위해 이동극장과 관민 파트너십이 대두되고 있습니다.

iStent나 Hydrus와 같은 MIGS 임플란트는 치료한 눈의 75% 이상으로 24개월째에 20%의 안압 하강을 가져오고, 녹내장 수술의 리스크 베네핏 프로파일을 일변시킵니다. INTEGRITY 시험에서는 iStent 무한 삽입 눈의 78.2%가 안압 20% 이상 감소의 임계값을 충족하고, 합병증 발생률은 3.3%로 기존의 트래베크렉토미를 크게 밑도는 것으로 보고되었습니다. MIGS를 백내장 절제술에 번들함으로써 외과의사는 한 번에 두 가지 질병을 다룰 수 있으며, 환자의 회복을 단축하고 지불자의 비용을 절감할 수 있습니다. 미국과 유럽의 일부에서는 MIGS와 백내장 수술의 병용이 보험 상환의 표준이 되어 MIGS의 보급을 가속화하고 안과 수술 기기 시장의 꾸준한 확대를 지원하고 있습니다.

최첨단 펨토초 레이저와 디지털 현미경은 50만 달러를 초과하는 지출을 강요하고 연간 서비스 계약은 5만 달러를 초과합니다. 중간 규모의 클리닉은 특히 증례 수가 적을 경우 진료 보수의 인하 압력이 이익을 낳기 때문에 투자 회수 기간이 연장되는 것에 직면합니다. 공인 엔지니어가 부족하기 때문에 센터는 고가의 임금을 제시하고 장기간의 교육에 투자하지 않을 수 없으며 수익성을 늦추고 있습니다. 지방에서는 자본 접근이 제한되어 있기 때문에 지리적 불평등이 확대되고, 설치율도 저하되어, 안과 수술 기기 시장에 브레이크를 걸고 있습니다.

백내장 시스템은 2024년 안과 수술 기기 시장의 41.6%를 차지하며, 세계적으로 연간 2,000만건 이상의 수술을 진행했습니다. 알콘의 CENTURION Vision System with ACTIVE SENTRY와 같은 첨단 플루이딕스 플랫폼은 보다 생리적인 안압을 유지하고, 내피세포의 손실을 줄이고 회복을 가속화합니다. 디지털 워크플로우 스위트는 생체계, 계산식, 클라우드 전송을 번들로 처리량과 외과 의사의 일관성을 향상시킵니다. 프리미엄 펨토 세컨드 레이저와 토릭 안구 렌즈 인젝터는 도시의 부유층을 끌어들이는 한편, 신흥 경제국의 대량생산 프로그램을 타겟으로 한 저가격의 페이코팩을 전용으로 제조하고 있습니다.

녹내장 수술 기기, 특히 트래비큘러 마이크로 바이패스 스텐트는 2025-2030년 CAGR이 8.9%로 예측되어 가장 급성장하고 있는 카테고리입니다. MIGS 교육의 보급, 장기 안전성 데이터의 성숙, 백내장 수술과의 조합으로 후보가 확대됩니다. 굴절 교정 및 망막 유리체 플랫폼의 점유율은 작지만, 렌즈 제작 시간을 10초 이하로 단축하는 SMILE pro 소프트웨어를 탑재한 Zeiss VISUMAX 800, 백내장과 망막의 용도를 교차하는 듀얼 모드 레이저와 같은 혁신의 혜택을 받고 있습니다. 따라서 기기 제조업체는 수익률을 보호하고 안과 수술 기기 시장을 확대하기 위해 부문을 넘어 시너지를 추구하고 있습니다.

북미는 2024년 세계 매출의 32.1%를 차지하며, 성숙한 상환의 틀, 조기 도입 외과의사 기반, 밀집한 ASC 네트워크에 지지되었습니다. 2025년 메디케어에 의한 2.9%의 ASC 비용 인상과 주요 학술 센터의 지속적인 자본 예산이 지역의 안정성을 지원하고 있습니다. 그럼에도 안구 렌즈의 보험료 인하가 가격을 압박하고 있으며, 병원은 공급 계약의 재협상과 구매 통합을 강요받고 있습니다.

아시아태평양의 2025년부터 2030년까지의 CAGR은 6.0%로 예측되며, 이는 세계에서 가장 빠른 속도입니다. 중국과 인도에서는 공공 실명 예방 운동이 참여 자격을 확대하고 있으며 국내 기업은 휴대용 전원으로 작동하는 저가의 파코 유닛을 확대하고 있습니다. 인도의 민간 안과 체인은 2025년에 새로운 자본 주입을 받아 지역 클리닉 전개 및 트레이닝 센터용으로 충당됩니다. 가처분 소득 증가와 도시화와 함께 이러한 요인은 백내장 수술 키트의 2자리 성장을 유지하고 보다 광범위한 안과 수술 기기 시장을 지원하고 있습니다.

유럽, 중동, 아프리카, 남미가 나머지 점유율을 차지하고 있습니다. 유럽에서는 MDR 규칙이 엄격하고 인증주기가 길어지고 있지만 디지털 현미경과 재생 각막 임플란트의 기술 혁신이 계속되고 있습니다. 걸프 협력 회의 국가는 최고 수준의 시스템을 수입하는 플래그쉽 안과 연구소에 자금을 제공하지만, 사하라 이남의 많은 국가들은 원격지에서 서비스를 제공하기 위해 자선 단체 지원의 이동식 극장에 의존하고 있습니다. 남미에서는 브라질과 아르헨티나가 기기 도입에 선도하고 있지만, 환율 변동은 조달 위험을 높이고 일관된 확대를 방해하고 있습니다. 지역 전체에서 외래 환자의 이동과 디지털 통합은 안과 수술 기기 시장의 통일 주제로 계속되고 있습니다.

The ophthalmic surgical devices market size stands at USD 12.53 billion in 2025 and is projected to reach USD 13.87 billion by 2030, reflecting a 5.20% CAGR over the forecast period.

Sustained demand is linked to the global surge in age-related eye disorders, expanding surgical coverage, and steady gains in healthcare spending across emerging economies. Robust product pipelines-especially in phaco systems, image-guided microscopes, and minimally invasive glaucoma implants-are enabling providers to improve outcomes while raising procedure throughput. Rising adoption of ambulatory surgical centers (ASCs) in North America, favorable reimbursement adjustments, and growing availability of purpose-built low-cost platforms in Asia Pacific are further widening access. Meanwhile, consolidation among key manufacturers is yielding integrated digital ecosystems that combine diagnostics, planning, and surgery into a single workflow, enhancing surgeon productivity and differentiating premium offerings.

Cataract procedure volumes are forecast to rise 128% by 2036, with patients aged 85+ generating the greatest incremental demand. Japan's elderly population already exceeds 20%, creating broad momentum for surgical capacity expansion. National programs tackling surgical backlogs-from WHO's Vision 2030 to country-specific blindness-prevention schemes-are improving coverage in many lower-income regions. Persistent disparity is still evident: a 2025 Australian study found Indigenous cataract surgical coverage at 68% versus 88.4% in non-Indigenous groups, underscoring the need for targeted outreach. Mobile theaters and public-private partnerships are therefore emerging to address underserved communities and sustain growth in the ophthalmic surgical devices market.

MIGS implants such as iStent and Hydrus deliver 20% intraocular-pressure (IOP) reductions in more than 75% of treated eyes at 24 months, transforming the risk-benefit profile of glaucoma surgery. The INTEGRITY study reported 78.2% of iStent infinite eyes meeting the >=20% IOP-reduction threshold with a 3.3% complication rate, well below conventional trabeculectomy. Bundling MIGS with cataract extraction allows surgeons to address two diseases in a single sitting, shortening patient recovery and cutting payor costs. Reimbursement codes covering combination procedures are now standard in the United States and parts of Europe, accelerating MIGS penetration and supporting steady expansion of the ophthalmic surgical devices market.

State-of-the-art femtosecond lasers and digital microscopes command outlays beyond USD 500,000, with annual service contracts topping USD 50,000. Mid-size clinics face stretched payback horizons as downward reimbursement pressure erodes margins, especially where case volumes are modest. Staffing costs compound the burden; shortages of certified technicians force centers to offer premium wages and invest in lengthy training, delaying profitability. Limited capital access in rural territories widens geographic inequality and tempers installation rates, placing a brake on the ophthalmic surgical devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cataract systems represented 41.6% of the ophthalmic surgical devices market in 2024, anchored by more than 20 million annual procedures worldwide. Advanced fluidics platforms such as Alcon's CENTURION Vision System with ACTIVE SENTRY maintain more physiologic intraocular pressure, decreasing endothelial cell loss and expediting recovery. Digital workflow suites bundle biometry, formula calculators, and cloud transfer, elevating throughput and surgeon consistency. Premium femtosecond lasers and toric IOL injectors attract affluent urban centers, whereas purpose-built low-cost phaco packs target volume programs in emerging economies.

Glaucoma surgery devices, especially trabecular micro-bypass stents, are the fastest-growing category with an 8.9% CAGR projected for 2025-2030. Widespread MIGS training, maturing long-term safety data, and pairing with cataract removal expand candidacy. Refractive and vitreo-retinal platforms hold smaller shares yet benefit from innovations such as Zeiss VISUMAX 800 with SMILE pro software, which cuts lenticule creation time below 10 seconds, and dual-mode lasers that bridge cataract and retinal applications. Device makers therefore pursue cross-segment synergies to defend margins and expand the ophthalmic surgical devices market.

The Ophthalmic Surgical Devices Market Report is Segmented by Product (Refractive Surgery Devices, Glaucoma Surgery Devices, Cataract Surgery Devices, and Other Surgical Devices), End-User (Hospitals, Specialty Ophthalmic Clinics, Ambulatory Surgery Centers (ASCs), and Other End-Users), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 32.1% of global revenue in 2024, underpinned by mature reimbursement frameworks, early adopter surgeon bases, and dense ASC networks. Medicare's 2.9% ASC fee boost for 2025 and sustained capital budgets at leading academic centers anchor regional stability. Nonetheless, premium IOL reimbursement compression is pressuring pricing, prompting hospitals to renegotiate supply contracts and consolidate purchasing.

Asia Pacific is projected to post a 6.0% CAGR from 2025 to 2030, the fastest pace worldwide. Public blindness-prevention drives in China and India are expanding eligibility, and domestic firms are scaling low-cost phaco units that operate on portable power. Private ophthalmology chains in India secured fresh equity infusions in 2025, earmarked for regional clinic rollouts and training centers. Alongside rising disposable income and urbanization, these factors sustain double-digit unit growth in cataract kits, supporting the broader ophthalmic surgical devices market.

Europe, the Middle East & Africa, and South America collectively represent the remaining share. Europe's stringent MDR rules have lengthened certification cycles, yet the region continues to innovate in digital microscopes and regenerative corneal implants. Gulf Cooperation Council nations are funding flagship eye institutes that import top-tier systems, whereas many sub-Saharan nations rely on charity-supported mobile theaters to serve remote areas. Brazil and Argentina lead South America in device adoption, but currency swings raise procurement risk and hinder consistent expansion. Across regions, outpatient migration and digital integration remain unifying themes in the ophthalmic surgical devices market.