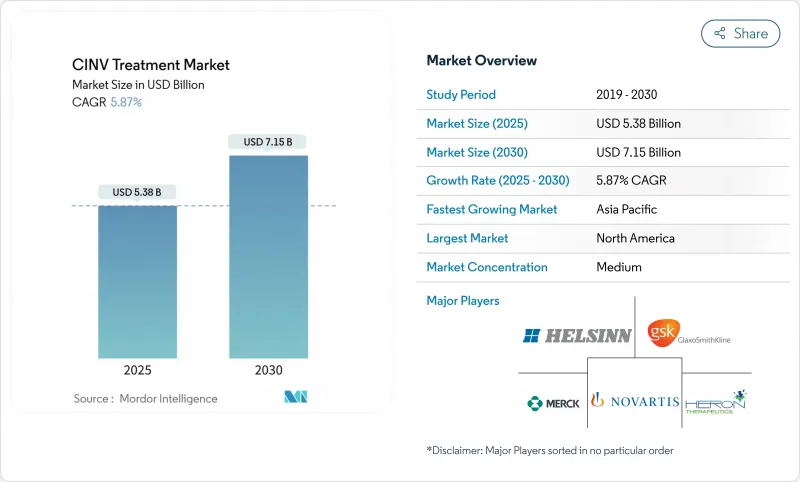

CINV 치료 시장의 규모는 2025년에 53억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.87%로, 2030년에는 71억 5,000만 달러에 달할 것으로 예측됩니다.

지속적인 수요는 암 이환율 확대, 고악성 화학요법의 사용 확대, 외래 및 가정 치료로의 꾸준한 전환으로 인해 발생합니다. 경구 및 서방형 제형은 분산된 케어 경로에 적합하고 어드히어런스를 향상시키기 위해 주사제의 과거 우위를 완화시키는 변화로서 지지를 모으고 있습니다. 주요 브랜드의 특허 만료는 당장의 가격 상승 압력이 되는 한편, 편리성, 합제, 개별 투여에 중점을 둔 차별화 제품으로 활로를 엽니다. 아시아태평양의 규제 조화와 암 영역의 증례 수 증가가 이 지역의 급성장을 견인하는 한편, 북미는 환급 체제와 임상시험의 인프라를 활용해 CINV 치료시장의 수익에 최대의 기여자로 계속되고 있습니다.

2024년 FDA가 승인한 획기적인 암 치료제는 치료 대상 환자를 확대하고 지지요법으로서 항구토제 수요를 강화하고 있습니다. 노인의 생존 기간이 길어지면 화학 요법과 관련된 구토의 위험에 노출되는 기간이 더 길어지고 항구토제의 사용은 종양학의 진보와 함께 확대됩니다. 신흥국 시장에서는 인구동태의 고령화 변화로 이러한 추세를 더욱 강화시켜야 하며, 노인 환자는 일반적으로 구토성이 높은 보다 적극적인 화학요법 프로토콜을 필요로 합니다. 게다가 암 검진 프로그램의 개선에 의해 악성 종양이 조기에 발견되면서 치료 기간이 길어져 환자 1인당의 항구토제 노출량이 누적되게 되었습니다.

안트라사이클린 기반의 요법과 백금 제형을 많이 사용하는 요법을 포함한 임상 프로토콜은 강력한 구토 예방에 의존하며 처방자는 더 나은 NK1 길항제를 선택하게 됩니다. 한 연구에서는 고위험 환자에 대해 올란자핀, 파로노세트론, 포스아프레피탄트를 병용한 경우 94.7%의 완전주효를 얻었습니다. 이러한 추세는 정밀 종양학이 보다 강력한 치료 접근법을 필요로 하는 환자 하위군을 확인함에 따라 가속화되어 진보된 항구토제에 대한 지속적인 수요를 창출하고 있습니다. 또한, 면역요법과 전통적인 화학요법의 통합은 특별한 관리 전략을 필요로 하는 새로운 항구토 프로파일을 생성합니다.

Sancuso와 같은 브랜드의 독점권 상실은 제네릭 의약품의 진입을 격려하고 평균 판매 가격을 낮추고 기존 기업의 R&D 재투자 모델을 어렵게 만듭니다. 기업은 인증된 제네릭, 가치 기반 계약, 라이프사이클 매니지먼트 이니셔티브 등의 방어 전략을 통해 대응하고 있지만, 이러한 접근법은 일반적으로 수익 감소를 막기보다는 오히려 지연시킵니다. 가격 압력은 의료 시장이 브랜드 지향보다 비용 효율성을 우선시하는 신흥 시장에서 강해져 제네릭 의약품 채용률을 가속화하고 있습니다.

5-HT3 수용체 길항제는 2024년 CINV 치료제 시장에서 44.87%의 점유율을 유지하였으며, 오랜 임상적 익숙성을 통해 그 지위를 구축하고 있습니다. 그러나 임상 의사가 지연기 보호를 위해 NK1 제형을 채택하는 경향이 강해지고 있기 때문에 이 부문의 성장은 소폭 유지될 전망입니다. NK1 길항제와 관련된 CINV 치료 시장 규모는 가이드라인 승인과 새로운 1일 1회 투여 제형의 등장으로 CAGR 6.71%로 증가할 전망입니다. 확고한 임상 증거가 NK1 길항제의 보급을 뒷받침하고, CINVANTI 등의 브랜드는 2035년까지 특허 보호 기간이 연장되기 때문에 혁신자는 가격 설정에 폭을 가질 수 있습니다.

도파민 길항제와 코르티코스테로이드의 상보적인 역할은 지속되고, 칸나비노이드는 난치성 사례에 대한 틈새 옵션으로 존재하고 있습니다. 올란자핀의 다중수용체 차단 작용을 지지하는 증거는 구조 요법의 취향을 바꾸고 있으며, 특히 단일 기전의 약물에서는 한계가 있는 획기적인 구토감에 효과적입니다. 병용 요법이 표준화됨에 따라 NK1 성분과 5-HT3 또는 코르티코스테로이드를 하나의 캡슐 또는 드롭으로 통합하는 제조업체는 워크 플로우의 효율성을 높이고 암 진료에 기여합니다.

북미는 확립된 임상 지침의 시행, 신속한 FDA 승인, 지지적 암 치료제에 대한 광범위한 보험 적용으로 2024년 세계 매출의 37.74%를 차지했습니다. 이 지역의 임상의는 응급약 사용의 감소를 나타내는 데이터를 통해 취득 비용이 높음에도 불구하고 서방형 혁신을 용이하게 채용합니다. 특허의 실효에 의해 연간 약가의 증가는 억제될 것으로 예상되지만, 암 이환율의 상승과 면역화학요법의 병용에 의한 사용량의 확대가 시장 전체의 가치를 지지하고 있습니다. 가치 기반 의료 모델은 주입 의자의 가동률과 재입원을 삭감하는 장시간 작용형 항구토제로 병원 시스템을 유도하고 있습니다.

아시아태평양은 중국, 인도 및 동남아시아 국가들이 종양학 인프라를 확대하고 규제 경로를 조화시켜 2030년까지 연평균 복합 성장률(CAGR) 7.08%로 성장할 것으로 예측됩니다. 중국의 국가 의약국은 2024년에 228건의 신약 승인 신청을 승인했으며, 그 중 37%는 항악성 종양제였습니다. 국내 업체들은 비용 경쟁력 있는 NK1 제네릭을 도입하고 다국적 기업들은 가속화된 패스웨이를 활용하여 합제를 출시합니다. 약물감시(의약품안전성감시)의 능력이 향상되어 공공병원에서의 데이터 주도 처방 통합이 보다 현실화됩니다.

유럽에서는 EMA의 일관된 승인과 기술 혁신과 비용 억제의 균형을 이루는 견고한 의료 기술 평가로 일관된 수요가 유지되고 있습니다. 각국의 환급위원회는 실제 임상에서의 유효성 데이터를 중시하고 응급 치료 및 재진단 감소를 입증하는 제품을 선호합니다. MEA와 남미 등 신흥 지역은 아직 개발도상지역이지만, 현지 생산에 적극적인 기업에 있어서는 전략적인 사업 확대 지역이며 단편적인 규제 상황을 극복할 수 있습니다.

The CINV Treatment Market size is estimated at USD 5.38 billion in 2025, and is expected to reach USD 7.15 billion by 2030, at a CAGR of 5.87% during the forecast period (2025-2030).

Sustained demand arises from expanding cancer prevalence, wider use of highly-emetogenic chemotherapy, and the steady migration of care toward outpatient and home-based settings. Oral and extended-release formulations gain traction because they fit decentralized care pathways and improve adherence, a shift that tempers the historical dominance of injectables. Patent expiries for key brands place near-term pressure on prices, yet they also open space for differentiated products that emphasize convenience, fixed-dose combinations, and personalized dosing. Asia-Pacific's regulatory harmonization and rising oncology caseload drive the fastest regional growth, while North America leverages reimbursement depth and clinical trial infrastructure to remain the largest contributor to CINV treatment market revenue.

Breakthrough oncology drugs cleared by the FDA in 2024 widened the treated patient pool, intensifying demand for supportive care antiemetics. Longer survival times among older populations further lengthen exposure to chemotherapy and related nausea risks, ensuring that antiemetic use scales alongside oncology advances. The demographic shift toward aging populations in developed markets compounds this trend, as older patients typically require more aggressive chemotherapy protocols with higher emetogenic potential. Additionally, improved cancer screening programs detect malignancies at earlier stages, leading to longer treatment durations and cumulative antiemetic exposure per patient.

Clinical protocols incorporating anthracycline-based or platinum-dense regimens hinge on robust antiemetic prophylaxis, steering prescribers toward premium NK1 antagonists. A study showed 94.7% complete response when olanzapine, palonosetron, and fosaprepitant were combined for high-risk patients.The trend accelerates as precision oncology identifies patient subgroups requiring intensified treatment approaches, creating sustained demand for advanced antiemetic solutions. Furthermore, the integration of immunotherapy with traditional chemotherapy creates novel emetogenic profiles that require specialized management strategies.

Loss of exclusivity for brands such as Sancuso intensifies generic entry, compressing average selling prices and challenging R&D reinvestment models for incumbents, particularly in regions where payers prioritize least-cost alternatives. Companies respond through defensive strategies including authorized generics, value-based contracting, and lifecycle management initiatives, but these approaches typically delay rather than prevent revenue erosion. The pricing pressure intensifies in emerging markets where healthcare systems prioritize cost-effectiveness over brand preference, accelerating generic adoption rates.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

5-HT3 receptor antagonists retained a 44.87% CINV treatment market share in 2024, a position built on long-standing clinical familiarity. Yet the segment grows modestly as clinicians increasingly adopt NK1 agents for delayed-phase protection. The CINV treatment market size tied to NK1 antagonists is on track to rise at 6.71% CAGR thanks to guideline endorsements and new once-daily formulations. Robust clinical evidence underpins NK1 uptake, and brands such as CINVANTI extend protection through 2035 patents, giving innovators pricing latitude.

Complementary roles for dopamine antagonists and corticosteroids persist, while cannabinoids remain a niche option for refractory cases. Evidence supporting olanzapine's multi-receptor blockade is altering rescue therapy preferences, especially for breakthrough nausea where single-mechanism drugs show gaps. As combination regimens become standard, manufacturers that integrate NK1 components with 5-HT3 or corticosteroids in a single capsule or infusion capture workflow efficiencies that resonate with oncology clinics.

The CINV Treatment Market Report is Segmented by Drug Class (5-HT3 Receptor Antagonists, NK1 Receptor Antagonists, Dopamine Antagonists, Cannabinoid Antagonists, and More), Formulation (Oral, Injectable, Transdermal, Sublingual), End User (Hospitals, Oncology & Specialty Clinics, Homecare Settings & ASCs), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 37.74% of global revenue in 2024 owing to established clinical guideline enforcement, rapid FDA approvals, and extensive insurance coverage for supportive oncology drugs. The region's clinicians readily adopt extended-release innovations despite higher acquisition costs when data show reduced rescue medication use. Patent expiries are expected to temper annual price growth, but volume expansion from rising cancer incidence and broader use of immuno-chemotherapy combinations sustains overall market value. Value-based care models are nudging hospital systems toward longer-acting antiemetics that cut infusion chair occupancy and readmissions.

Asia-Pacific is projected to grow at 7.08% CAGR through 2030 as China, India, and Southeast Asian countries expand oncology infrastructure and harmonize regulatory pathways. China's National Medical Products Administration cleared 228 NDAs in 2024, 37% for antineoplastic agents, catalyzing supportive-care demand. Domestic manufacturers introduce cost-competitive NK1 generics, while multinational firms leverage accelerated pathways to launch fixed-dose combos. Pharmacovigilance capacity is rising, making data-driven formulary inclusion more feasible across public hospitals.

Europe maintains consistent demand anchored by harmonized EMA approvals and robust health technology assessments that balance innovation with cost containment. National reimbursement boards emphasize real-world effectiveness data, favoring products that document reduced rescue therapy and hospital re-visits. Emerging regions in MEA and South America remain nascent contributors yet represent strategic expansions for companies willing to localize production and navigate fragmented regulatory landscapes.