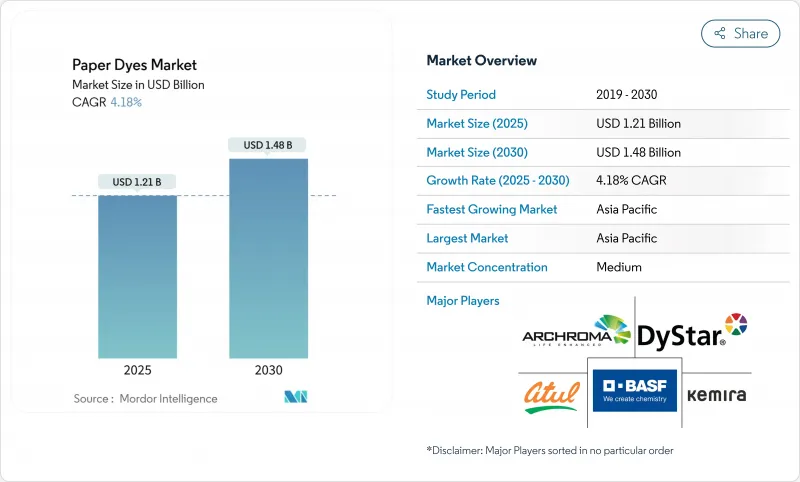

세계의 종이 염료 시장은 2025년에 12억 1,000만 달러, 2030년에는 14억 8,000만 달러에 이를 전망으로, CAGR 4.18%로 성장할 것으로 예측됩니다.

이 꾸준한 궤도는 플라스틱에서 종이 기반 포장으로의 구조적 전환과 전자상거래 출하에서 생생하고 일관성 있는 브랜드 그래픽에 대한 수요가 증가함에 따라 디지털 문서의 대안으로 시장의 탄력성을 반영합니다. 최신 잉크젯 라인과 원활하게 통합할 수 있는 액체는 컨버터의 다운타임 절감에 도움이 되며, 주요 염료 제조업체에 의한 능력 증강은 원료 공급의 균형을 유지하고 있습니다. 일회용 플라스틱을 제한하는 규제의 지원과 브랜드 오너가 재생 가능한 기재를 선호하는 경향이 그래픽 용지의 수량 축소에도 확대 전망을 보이고 있습니다. 리그닌 적합성 및 나노캡슐화된 화학물질에 대한 투자를 통해 공급업체의 차별화가 진행되어 식품과 접촉하는 용도와 고속 디지털 용도의 프리미엄 주문을 획득할 수 있습니다.

소매 브랜드는 일회용 플라스틱 금지에 대응하고 소비자의 종이에 대한 선호도에 부응하기 위해 석유 기반 기판을 재활용 가능한 섬유 기반 형식으로 대체하고 있습니다. 네슬레, 유니레버 및 기타 다국적 기업은 현재 특정 SKU에서 최대 97%의 플라스틱을 제거하고 있으며, 여러 재활용 루프를 통해 안정적인 성능을 유지하는 고성능 염료 주문을 가속화하고 있습니다. 유럽 연합(EU)의 일회용 플라스틱 지침이 만들어내는 규제의 확실성은 식품에 적합하고 이행을 방지하는 착색료를 필요로 하는 컨버터에 대한 설비 투자를 지원하고 있습니다. 지속 가능한 포장에 프리미엄을 지불하는 소비자의 의욕은 안정적이며, 염료 제조업체는 섬유 회수 시스템에서 알칼리 탈묵과 산화 표백을 견딜 수있는 새로운 제형에 대한 가격을 방어할 수 있습니다.

온라인 주문의 80% 이상이 골판지로 배송되며 소포의 양은 아시아태평양과 북미를 중심으로 계속 증가하고 있습니다. 풀필먼트 센터는 유지 보수가 적은 프린트 헤드용으로 설계된 액체 염료로 작동하는 고속 회전 잉크젯 라인이 필요하므로 대규모 개인화를 당일에 실현할 수 있습니다. 2024년에는 포장공장의 임대료가 20년 평균을 45% 웃돌았으며, 이는 구조적인 생산능력 확대의 명확한 신호로 종이 염료 시장이 예측기간에 걸쳐 유지됨을 보여줍니다.

기업 및 교육기관 사용자가 디지털 워크플로우를 가속화한 후 그래픽 용지 수요가 급격히 축소되었습니다. 유럽 제지산업연합(Confederation of European Paper Industries)은 2023년 종이 및 판지 생산량의 13% 감소를 기록해 그래픽 그레이드만으로도 28% 감소했습니다. 인쇄량을 50-70% 줄이는 원격 근무 프로토콜은 여전히 효과적이며 전자 서명 플랫폼은 하드 카피의 필요성을 줄입니다. 포장용 염료는 약간의 손실을 상쇄하지만 그래픽 용지의 축소는 특히 성숙한 지역에서 전체 톤수의 성장을 제한합니다.

액제는 2024년 매출의 51.92%를 차지하였고, CAGR 6.40%로 확대될 것으로 예측됩니다. 이는 전자상거래 포장의 업그레이드를 지원하는 고속 잉크젯 라인에서 매우 중요한 역할을 보여줍니다. 파우더 그레이드는 대량 수송이 용이한 반면, 분진 노출 규칙이나 분산 시간의 지연을 해결해야 합니다. 나노캡슐화된 액체 시스템은 현재 1,000시간이 넘는 프린트헤드의 듀티 사이클을 가능하게 하고, 컨버터를 위한 유지보수 셧다운을 최소화하고 OEE를 개선합니다. 온도 변화에 대한 안정적인 점도는 자동 투여를 지원하고 Just-in-Time 생산 목표를 따릅니다.

미니 에멀젼과 마이크로플루이딕스 캡슐화의 지속적인 진보로 보존성이 향상되고 25°C에서 보존된 경우 표준 제형에서는 6개월인 반면 12개월 이상 색조 강도를 유지할 수 있습니다. 결과적으로 컨버터는 재고 만료로 인한 평가 손실을 줄일 수 있습니다. 파우더 공급업체는 압축 및 방진 기술을 지원하지만, 디지털화된 공장에서는 액체 공급업체에 뒤처져 있습니다.

직접 염료는 비용 효율적인 배출 공정에서 선호되며 2024년 매출의 28.45%를 차지하였으며 대량의 라이너 보드 공장에서 우위를 유지하고 있습니다. 그러나, 반응 염료 분야는 우수한 내세탁성을 강점으로, CAGR 5.90%로 성장하고 있습니다. 이는 재활용을 견딜 수 있는 그래픽을 필요로 하는 고급 종이 사용자에 의해 뒷받침되고 있습니다. 섬유별 시험에 따르면, 면섬유를 많이 포함한 특수 등급은 반응성 염료로 41.45%의 염료 흡수를 기록하고 있는 반면, 다른 화학약품에서는 35.68%로 예상됩니다.

공급업체는 정착성을 희생하지 않고 전형적인 반응조 온도를 90°C에서 60°C로 낮추고 에너지 부하를 낮추고 탈탄소 목표로 제한되는 공장 채택을 확대합니다. 직접 염료는 중성 pH 하에서 쉽게 부착되기 때문에 여전히 인기있지만, 시장 점유율은 순환 경제의 의무에 따라 더 높은 가치의 화학 물질로 점차 대체되고 있습니다.

아시아태평양은 2024년 수익의 44.79%를 차지하며 선두를 유지하였으며 2030년까지 연평균 복합 성장률(CAGR) 5.70%로 성장할 것으로 예측되며 이는 세계 제조업의 핵으로서의 지위와 급속히 확대하는 소비자 시장을 반영하고 있습니다. 중국의 화학 산업의 패자인 Hengli, Wanhua 및 동업자들은 지역 자급률을 높이는 정밀 화학 프로젝트에 정부 인센티브를 투입하고 있습니다. 4,300,000명의 노동자를 고용하고 7,500개의 섬유 기업을 보유한 베트남은 골판지와 특수지의 소비를 밀어 올려 지역의 염료 사용량을 증가시킵니다.

북미는 전자상거래 풀필먼트의 성장과 다국적 식음료 기업의 적극적인 플라스틱 감축 선언에 힘입어 금액 기준으로 2위를 차지하고 있습니다. Archroma 사의 사우스 캐롤라이나 공장과 Solenis 사의 버지니아 공장은 현지에 특화된 공급을 실시하고 PFAS에 관한 규제가 명확해짐에 따라 컨버터 각사는 규정에 맞는 수성 시스템을 채용하게 되었습니다. 그래픽 페이퍼의 축소는 총 톤수를 억제하고 있지만, 환경에 최적화된 염료를 선호하는 프리미엄 등급의 주문은 인플레이션을 웃도는 가격 실현을 지원하고 있습니다.

유럽은 엄격한 REACH 개정과 펄프 가격 변동(북부 표백 침엽수 공예는 2024년 4월 1,380유로/톤을 기록)에 직면해 영업이익률을 압박받고 있습니다. 그러나 순환형 경제에 관한 규제와 리그닌 유래의 착색제의 연구개발에 대한 자금제공에 있어 유럽권은 리더십을 발휘하고 있으며, 현지 공급업체는 고가치로 환경에 최적화된 제품의 최전선에 위치하고 있습니다. 처리 회사는 배출 허가를 충족하기 위해 폐쇄 루프 수처리에 투자하고 폐수 무방류의 목표에 부합하는 저염분, 고배출 염료에 대한 수요를 높입니다.

The global paper dyes market stood at USD 1.21 billion in 2025 and is forecast to reach USD 1.48 billion by 2030, advancing at a 4.18% CAGR.

This steady trajectory reflects the market's resilience in digital-document substitution, supported by the structural migration from plastic to paper-based packaging and rising demand for vivid, brand-consistent graphics in e-commerce shipments. Liquid formulations that integrate seamlessly with modern inkjet lines are helping converters reduce downtime, while capacity additions by major dye makers keep raw material supply balanced. Regulatory tailwinds that restrict single-use plastics and brand owners' preference for renewable substrates underpin an expansionary outlook even as graphic-paper volumes contract. Investments in lignin-compatible and nano-encapsulated chemistries further differentiate suppliers, positioning them to capture premium orders in food-contact and high-speed digital applications.

Retail brands continue to replace petroleum-based substrates with recyclable, fiber-based formats to comply with single-use plastic bans and to meet consumer preference for paper. Nestle, Unilever, and other multinationals now eliminate up to 97% of plastic from certain SKUs, accelerating orders for high-performance dyes that remain stable through multiple recycling loops. Regulatory certainty created by the European Union's Single-Use Plastics Directive supports capital investment in converters that require food-contact-compliant, migration-safe colorants. Consumer willingness to pay premiums for sustainable packaging has held steady, allowing dye producers to defend pricing for novel, colorfast formulations that tolerate alkaline de-inking and oxidative bleaching in recovered-fiber systems.

Over 80% of online orders ship in corrugated formats, and parcel volumes continue to rise-particularly in Asia-Pacific and North America-creating concentrated demand for vivid graphics that elevate the unboxing experience. Fulfillment centers require rapid-turn inkjet lines that run on liquid dyes engineered for low-maintenance printheads, enabling same-day personalization at scale. Building leases for packaging plants rose 45% above the 20-year average in 2024, a clear signal of structural capacity expansion that will sustain the paper dyes market over the forecast horizon.

Graphic-paper demand contracted sharply after corporate and educational users accelerated digital workflows. The Confederation of European Paper Industries recorded a 13% fall in paper and board production in 2023, with graphic grades alone down 28%. Remote-work protocols that cut printing volumes by 50-70% remain in force, while e-signature platforms reduce the need for hard copies. Although packaging dyes offset some losses, graphic-paper contraction limits overall tonnage growth, particularly in mature regions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Liquid offerings held 51.92% of 2024 revenue and are projected to expand at a 6.40% CAGR, reinforcing their pivotal role in high-speed inkjet lines that power versioned e-commerce packaging. Powder grades, although easier to transport in bulk, must contend with dust-exposure rules and slower dispersion times. Nano-encapsulated liquid systems now enable print-head duty cycles exceeding 1,000 hours, minimizing maintenance shutdowns and improving OEE for converters. Stable viscosity across temperature swings supports automated dosing, aligning with just-in-time production targets.

Ongoing advances in mini-emulsion and microfluidic encapsulation increase shelf life, preserving hue intensity for over 12 months when stored at 25 °C, compared with six months for standard formulations. As a result, converters see reduced write-offs from expired stocks. Powder suppliers respond with compaction and dust-suppressant technologies but still trail liquid rivals in digitally enabled plants.

Direct dyes, favored for cost-efficient exhaust processes, commanded 28.45% of 2024 sales, maintaining dominance in high-volume linerboard mills. Yet the reactive segment is advancing at a 5.90% CAGR on the strength of superior wash-fastness, an attribute prized by premium folding-carton users who require graphics to survive recycling. According to fiber-specific trials, cotton-fiber-rich specialty grades register dye uptake of 41.45% with reactivatives versus 35.68% for other chemistries.

Suppliers reduce typical reactive-bath temperatures from 90 °C to 60 °C without sacrificing fixation, lowering energy loads, and broadening adoption in mills constrained by decarbonization targets. Direct dyes remain a staple because they attach readily under neutral pH, but their market share is gradually ceded to higher-value chemistries that align with circular-economy mandates.

The Paper Dyes Market Report Segments the Industry by Form (Powder and Liquid), Type (Acidic, Basic, and More), Origin (Organic and Synthetic), Application (Printing and Writing, Packaging, Specialty, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific retained leadership with 44.79% of 2024 revenue and is forecast to rise at a 5.70% CAGR to 2030, reflecting its status as a global manufacturing nucleus and fast-expanding consumer market. China's chemical champions-Hengli, Wanhua, and peers-channel government incentives into fine-chemical projects that lift regional self-sufficiency. Vietnam, hosting 7,500 textile enterprises employing 4.3 million workers, boosts regional consumption of corrugated and specialty papers, translating into higher local dye usage.

North America ranks second by value, propelled by e-commerce fulfillment growth and aggressive plastic-reduction pledges from food and beverage multinationals. Archroma's South Carolina site and Solenis's Virginia complex provide localized supply, while regulatory clarity on PFAS pushes converters to adopt compliant, water-based systems. Although graphic-paper contraction tempers total tonnage, premium-grade orders that favor environmentally optimized dyes support above-inflation price realization.

Europe grapples with stringent REACH amendments and pulp-price volatility-Northern Bleached Softwood Kraft touched EUR 1,380 / t in April 2024-pressuring operating margins. Yet the bloc's leadership in circular-economy regulation and R&D funding for lignin-derived colorants positions local suppliers at the forefront of high-value, eco-optimized offerings. Converters invest in closed-loop water treatment to meet discharge permits, raising demand for low-salt, high-exhaustion dyes that align with zero-liquid-discharge ambitions.