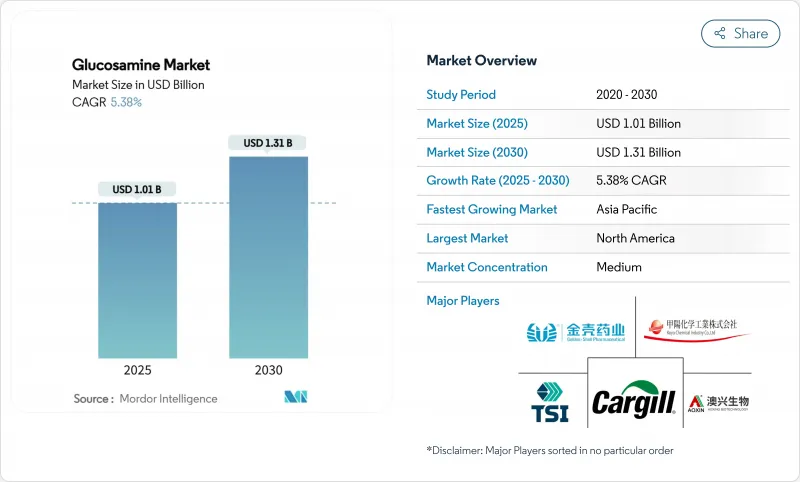

글루코사민 시장은 2025년에 10억 1,000만 달러로 추정되고, 2030년에는 13억 1,000만 달러에 이를 전망으로, CAGR 5.38%로 성장할 것으로 예측됩니다.

시장 성장의 원동력이 되고 있는 것은 건강한 노화에 대한 주목의 고조, 예방 헬스케어에의 접근성 개선, 각 지역의 규제 틀의 진화입니다. 북미는 확립된 소매 약국망과 높은 소비자 의식으로 시장을 선도하고 있지만, 아시아태평양은 가처분소득 증가와 영양보조식품 유통채널 확대에 힘입어 가장 높은 수량 성장을 보이고 있습니다. 발효 기술의 진보는 알레르겐 위험을 줄이고 안정적인 원료 공급을 보장하여 비용 효율성을 높입니다. 게다가 2024년 3월 FDA에 의한 신고 절차의 개정에 의해 제품 출시의 타임라인이 단축되어, 제형이나 기능성 식품의 기술 혁신이 가속화하고 있습니다.

골관절염의 증례는 전 세계적으로 현저하게 증가하고 있으며, 특히 선진지역과 개발도상지역에서 유병률이 높아지고 있습니다. 이 질환은 주로 여성과 노인이 앓고 있으며 평생 동안 관절 관리를 위한 보충제가 필요합니다. 세계적인 신체장애의 주요 원인인 변형성 관절증은 직장 생산성 저하, 건강 관리 비용 증가, 장기적인 의료 요구를 통해 경제적 손실을 가져옵니다. 지속적인 건강 부담, 세계 인구의 고령화, 관절 건강에 대한 의식 증가가 글루코사민 제품에 대한 안정적인 수요를 유지하고 있습니다. 골관절염의 만성적 성질은 지속적인 관리를 필요로 하며 시장의 안정성을 지원합니다.

미국인은 영양 보충제를 정기적인 건강 루틴에 포함합니다. 청소년과 노인 모두 예방 의료를 중시하기 때문에 글루코사민, 콘드로이친, 메틸 설포닐 메탄(MSM)을 함유한 관절 보충제의 판매가 증가하고 있습니다. 이러한 보충제는 특히 활동적인 개인과 노인 관절의 건강과 이동성을 지원합니다. 개인화된 영양 용도, 구독 서비스 및 원격약국(Telepharmacy) 플랫폼의 상승은 보충제 소비를 촉진하고 디지털 채널을 통해 글루코사민 시장을 확대하고 있습니다. 이러한 디지털 플랫폼을 통해 소비자는 보충제에 편리하게 접근할 수 있으며, 동시에 건강 목표와 필요에 따라 개별화된 권장 사항을 얻을 수 있습니다.

글루코사민은 주로 새우나 게 등의 조개류를 원료로 하고 있지만, 조개류의 입수 가능성의 변동에 의한 생산의 중단이나 비용 상승에 직면하고 있습니다. 해양오염, 기후 변화, 해수온도 상승 등의 환경과제는 많은 지역에서 서식환경을 악화시켜 조개 개체수를 줄이고 있습니다. 지속 불가능한 어획과 남획은 글루코사민 추출에 필수적인 조개를 더욱 고갈시킵니다. 동남아시아에서는 새우 양식장이 큰 질병 발생에 휩싸여 조개 생산량이 현저하게 감소하고 있습니다. 해양생태계를 보호하기 위해 어획할당이나 계절적인 금어 등의 규제조치가 실시되고 있으며 이 또한 공급을 억제하고 있습니다. 게다가 주요 수출국 중에서 특히 중국과 베트남에서의 지정학적 긴장과 무역의 혼란은 시장에 예측 불가능성을 가져옵니다. 이러한 요인을 종합하면 글루코사민 생산자에게는 공급의 불안정화, 비용의 상승, 생산계획의 과제가 존재하고 있습니다.

조개류 유래의 글루코사민은 확립된 공급망과 깊은 소비자층으로 인해 혜택을 받으며, 2024년 시장 점유율 79.85%를 유지하였습니다. 게와 새우 껍질에서 추출하는 종래의 방법은 기존의 수산가공 폐기물의 흐름을 활용하여 폐기물 이용에 의한 비용효율과 환경이익을 창출하고 있습니다. 그러나 발효 유래 대체 식품은 알레르기 회피, 지속가능성에 대한 우려, 공급망의 다양화 전략이 원동력이 되어 2030년까지 연평균 복합 성장률(CAGR) 7.86%의 성장을 나타낼 전망입니다.

인공효소 바이오시스템을 포함한 고급 생산 방법의 개발은 발효에 의한 전분에서 글루코사민으로의 높은 전환 효율을 가능하게 했습니다. 이 혁신적인 생산 방법은 제품의 품질을 유지하면서 환경에 미치는 영향을 크게 줄입니다. 발효 공정은 재생 가능한 자원과 관리되는 제조 조건을 이용하여 안정적인 제품 품질을 제공합니다. 이 생산 방법은 특히 친환경 제품을 추구하는 소비자들 사이에서 공급 안전 문제와 소비자 선호도 모두에 대응하는 지속 가능한 대안을 제공합니다.

글루코사민 시장 보고서는 유형별(황산글루코사민, 염산글루코사민 등), 공급원별(조개류 유래, 발효 유래, 기타), 용도별(영양 보충제, 반려동물 및 동물용 보충제 등), 지역별(북미, 유럽, 아시아태평양, 남미 등)으로 분류되어 있습니다. 시장 세분화는 위의 모든 부문에 대해 금액 기준으로 표시됩니다.

북미는 확립된 헬스케어 인프라, 관절 건강 보충제에 대한 높은 소비자 의식, FDA 감독하의 양호한 규제 틀에 힘입어 2024년에 39.21%의 점유율로 시장의 주도권을 유지하였습니다. 이 지역은 주요 의료기관에서 실시되는 광범위한 임상 연구와 약국 체인 및 전문 소매점의 강력한 유통망으로 이익을 얻고 있습니다. 소비자의 지출 패턴은 글루코사민을 일상적인 건강 관리 요법에 통합하는 추세를 반영하며, 의약품 등급 제형에 보험이 적용될 수 있습니다. 베이비붐 세대의 노령화가 지속적인 수요를 창출하는 한편, 젊은 소비자는 피트니스나 웰니스의 동향에 영향을 받은 예방적 보충제 전략을 점점 채용하게 되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 8.15%로 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 이는 중산층 인구 확대, 의료지출 증가, 서구식 영양 접근에 대한 의식의 고조가 원동력이 되고 있습니다. 중국과 인도는 국내 생산 능력과 전통적인 의료를 통한 자연 건강 제품의 수용으로 혜택을 받는 역동적인 시장입니다. 일본은 정교한 기능성 식품 시장을 보유하고 있습니다. 아시아태평양의 제조 비용과 특히 발효 유래 제조의 이점은 세계 글루코사민 공급망의 소비 및 수출 허브로 자리매김하고 있습니다.

유럽은 엄격한 규제 감독과 증거를 기반으로 한 건강 관리 접근법을 특징으로 하는 성숙 시장입니다. 유럽식품안전국의 건강강조표시에 대한 엄격한 평가 프로세스는 신규 진입기업에 장벽이 되는 한편, 승인된 강조표시가 있는 기존 제품을 보호하고 있습니다. 소비자의 선호는 증거 기반 의료를 중시하는 이 지역의 특성을 반영하여 임상 문서가 첨부된 제약 등급 제형을 선호합니다. 이 시장은 골관절염 연구를 수행하는 강력한 연구 기관과 약국 채널을 통한 확립된 유통으로 이익을 얻고 있습니다. 영국에서는 영양보조식품과 기능성식품의 독립적인 평가 프레임워크가 개발되어 규제의 조화에 계속 영향을 미치고 있습니다.

The glucosamine market is estimated to be valued at USD 1.01 billion in 2025 and is expected to reach USD 1.31 billion by 2030, growing at a CAGR of 5.38%.

The market growth is driven by increased focus on healthy ageing, improved access to preventive healthcare, and evolving regulatory frameworks across regions. North America leads the market due to its established retail pharmacy network and high consumer awareness, while the Asia-Pacific region demonstrates the highest volume growth, supported by increasing disposable incomes and expanding nutraceutical distribution channels. Advancements in fermentation technology reduce allergen risks and ensure stable raw material supply, enhancing cost efficiency. Additionally, the FDA's revised notification procedures in March 2024 have reduced product launch timelines, enabling increased innovation in dosage forms and functional foods .

Osteoarthritis cases worldwide have increased significantly, with higher prevalence rates in developed and developing regions. The condition predominantly affects women and older adults, who require joint-care supplements throughout their lives. As a major cause of global disability, osteoarthritis results in economic losses through reduced workplace productivity, higher healthcare costs, and long-term medical care needs. The persistent health burden, aging global population, and growing awareness of joint health maintain consistent demand for glucosamine products. The chronic nature of osteoarthritis requires continuous management, supporting market stability.

The United States population regularly incorporates dietary supplements into their health routines. Both young and older adults emphasize preventive healthcare, which increases the sales of combination joint supplements containing glucosamine, chondroitin, and Methylsulfonylmethane (MSM). These supplements support joint health and mobility, particularly among active individuals and aging populations. The rise of personalized nutrition applications, subscription services, and tele-pharmacy platforms drives supplement consumption and expands the glucosamine market through digital channels. These digital platforms enable consumers to access supplements conveniently while receiving personalized recommendations based on their health goals and requirements.

Glucosamine, primarily sourced from shellfish like shrimp and crabs, faces production disruptions and cost inflation due to fluctuations in shellfish availability. Environmental challenges, including ocean pollution, climate change, and rising sea temperatures, have degraded habitats and diminished shellfish populations in numerous regions. Unsustainable harvesting and overfishing practices further deplete the shellfish shells essential for glucosamine extraction. In Southeast Asia, shrimp farms have grappled with disease outbreaks, leading to marked declines in shellfish production. To safeguard marine ecosystems, regulatory measures such as harvesting quotas and seasonal bans have been implemented, but they also curtail supply. Moreover, geopolitical tensions and trade disruptions in major exporting nations, particularly China and Vietnam, introduce unpredictability to the market. Collectively, these factors contribute to supply instability, escalating costs, and challenges in production planning for glucosamine producers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Shellfish-derived glucosamine maintains 79.85% market share in 2024, benefiting from established supply chains and consumer familiarity. Traditional extraction methods from crab and shrimp shells leverage existing seafood processing waste streams, creating cost efficiencies and environmental benefits through waste utilization. However, fermentation-derived alternatives exhibit 7.86% CAGR growth through 2030, driven by allergy avoidance, sustainability concerns, and supply chain diversification strategies.

The development of advanced production methods, including artificial enzymatic biosystems, enables high conversion efficiency from starch to glucosamine through fermentation. This innovative production method significantly reduces environmental impact while maintaining product quality. The fermentation process utilizes renewable resources and controlled manufacturing conditions, resulting in consistent product quality. This production method offers a sustainable alternative that addresses both supply security concerns and consumer preferences, particularly among those seeking environmentally responsible products.

The Glucosamine Market Report is Segmented by Type (Glucosamine Sulfate, Glucosamine Hydrochloride (HCl), and More), Source (Shellfish-Derived, Fermentation-Derived, and Others), Application (Nutritional Supplements, Pet and Veterinary Supplements, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). Market Sizing is Presented in USD Value Terms for all the Abovementioned Segments.

North America maintains market leadership with 39.21% share in 2024, supported by established healthcare infrastructure, high consumer awareness of joint health supplements, and favorable regulatory frameworks under FDA oversight. The region benefits from extensive clinical research conducted at major medical institutions and strong distribution networks through pharmacy chains and specialized retailers. Consumer spending patterns reflect integration of glucosamine into routine healthcare regimens, with insurance coverage occasionally available for pharmaceutical-grade formulations. The aging baby boomer demographic creates sustained demand, while younger consumers increasingly adopt preventive supplementation strategies influenced by fitness and wellness trends.

Asia-Pacific emerges as the fastest-growing region with 8.15% CAGR through 2030, driven by expanding middle-class populations, increasing healthcare expenditure, and growing awareness of Western nutritional approaches. China and India represent particularly dynamic markets, benefiting from domestic manufacturing capabilities and acceptance of traditional medicine natural health products. Japan's sophisticated functional foods market. The region's manufacturing cost advantages, particularly for fermentation-derived production, position Asia-Pacific as both a consumption and export hub for global glucosamine supply chains.

Europe represents a mature market characterized by stringent regulatory oversight and evidence-based healthcare approaches. The European Food Safety Authority's rigorous evaluation processes for health claims create barriers for new entrants while protecting established products with approved claims. Consumer preferences favor pharmaceutical-grade formulations with clinical documentation, reflecting the region's emphasis on evidence-based medicine. The market benefits from strong research institutions conducting osteoarthritis studies and established distribution through pharmacy channels. Brexit implications continue affecting regulatory harmonization, with the UK developing independent evaluation frameworks for dietary supplements and functional foods.